May 19, 2026

The Procurement Calculus Behind Southeast Asia's Potash Market

Fertilizer markets across Asia operate on a fundamentally different logic than the spot-driven commodity exchanges familiar to Western traders. Rather than continuous price discovery through open markets, potash procurement across Southeast Asia is shaped by periodic, high-stakes tender events where centralised buyers aggregate national demand and negotiate directly with global producers. Understanding this architecture is essential to interpreting what Indonesia's latest move in the MOP market actually signals, and why the Indonesia tender to buy 20,000t white MOP matters far beyond the archipelago's borders.

Indonesia sits at the centre of this dynamic. As one of Southeast Asia's largest agricultural economies, its plantation sector, spanning palm oil, rubber, natural rubber, and staple food crops, generates structural, recurring demand for potassium-based fertilizers that does not fluctuate dramatically from year to year. What does fluctuate is the timing of procurement, and this is where the real market intelligence lies. Furthermore, commodity market volatility in 2025 has added additional complexity to procurement timing decisions across the region.

When big ASX news breaks, our subscribers know first

Why Indonesia Functions as a Regional Price Anchor

State-linked Indonesian importers have long operated as volume aggregators, consolidating national demand into single large-tranche tenders that carry enough weight to influence supplier pricing across the entire Southeast Asian region. Unlike smaller buyers in Vietnam, Thailand, or the Philippines, Indonesian procurement entities can credibly threaten to delay, cancel, or split tenders, and this leverage is deployed deliberately.

When one of these entities issues a tender, the agreed CFR price does not stay within Indonesian borders. Buyers across the region monitor award outcomes closely, using them as live price benchmarks before committing to their own procurement cycles. This cascading effect makes Indonesian tender results a de facto price discovery mechanism for Southeast Asian MOP markets more broadly.

The sophisticated procurement timing practised by Indonesian state-linked importers is less visible than exchange-based price signals, but arguably more consequential for regional price formation.

What Makes Indonesian Tenders So Influential?

The commodity prices impact on agricultural sectors across Southeast Asia means that Indonesia's procurement decisions reverberate through regional supply chains with considerable force. Consequently, even modest shifts in Indonesian award prices translate into measurable adjustments across neighbouring markets.

Two Tenders, One Strategy: Unpacking the Current Procurement Cycle

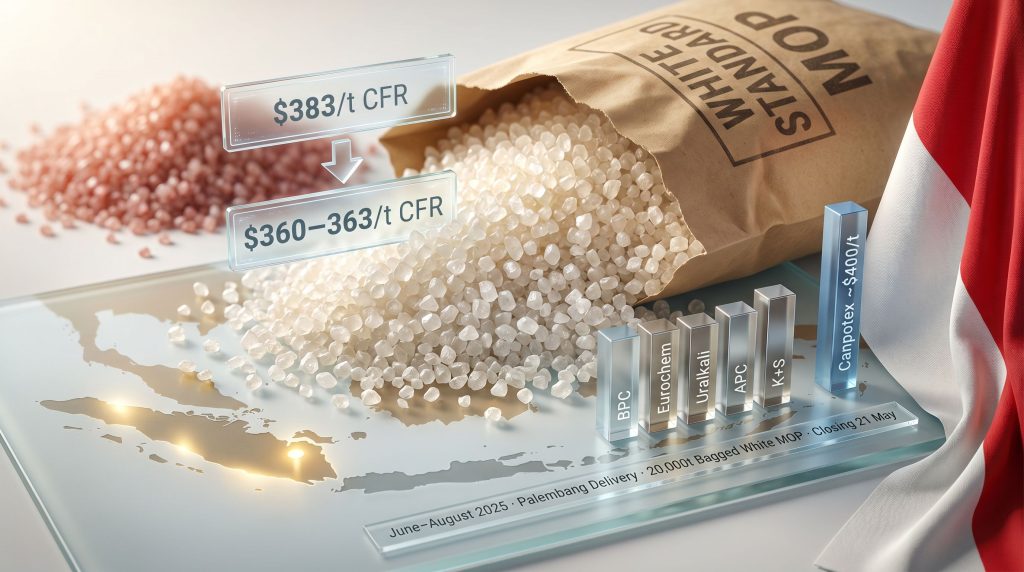

The current procurement sequence involves two interconnected actions by the same Indonesian importer. The first is a focused Indonesia tender to buy 20,000t white MOP, specifying bagged product for delivery to Palembang across a June-to-August 2025 window, with bids due by 21 May. The second is a substantially larger follow-on tender for the full volume previously cancelled: 120,000 tonnes of red standard MOP and 35,000 tonnes of white standard MOP, totalling 155,000 tonnes.

The cancelled tender, originally scheduled to close on 27 April, was withdrawn before any award was made. This was not a sign of market dysfunction. The importer was executing a well-established procurement tactic: deliberately pausing to wait for a definitive upstream price signal before locking in terms on a smaller, regionally exposed tender.

That price signal arrived when India's new standard MOP contract was concluded at $383 per tonne CFR with 180 days of credit terms, according to reporting by Argus Media. This settlement gave the Indonesian importer the anchor it needed to re-engage the market from an informed negotiating position.

The Logic of Procurement Sequencing

The sequencing of these two tenders also carries strategic intent. By issuing the smaller 20,000-tonne white MOP tender first, the importer effectively runs a price discovery exercise before committing to the much larger 155,000-tonne follow-on. The award price from the initial tender, if accepted at competitive levels, provides a real-world validation point for what the market will bear before the importer re-exposes itself to the larger volume.

This two-stage structure is more common in large Asian procurement cycles than is generally recognised. It allows buyers to test seller appetite without revealing total demand, potentially preventing suppliers from pricing opportunistically against a known large-volume buyer. In addition, supply chain disruptions in 2025 have made such cautious sequencing even more strategically valuable for large-volume buyers.

White MOP vs. Red MOP: Why Grade Specification Matters

The distinction between white and red standard MOP is frequently misunderstood outside the fertilizer trade. Both are muriate of potash (KCl) with comparable nutrient content, typically around 60% K₂O equivalent. The difference is entirely in processing and presentation.

| Attribute | White Standard MOP | Red Standard MOP |

|---|---|---|

| KCl Content | ~60% K₂O equivalent | ~60% K₂O equivalent |

| Colour | Off-white to cream granular | Reddish-pink granular |

| Processing | Additional beneficiation required | Standard ore processing |

| Price Premium | Modest premium over red MOP | Base reference price |

| Primary Uses | NPK blending, sensitive crops | Broad agricultural application |

| Key Suppliers | Canpotex, K+S, Eurochem | BPC, Uralkali, APC |

White MOP's premium over red MOP is driven by the additional processing required to remove iron oxide colouration from the ore body. This matters for compound NPK fertilizer manufacturing, where product uniformity and contamination risk affect blending efficiency and final product quality. Export-oriented agricultural supply chains, particularly those producing palm oil derivatives for international markets, often specify white MOP to meet quality assurance requirements at the downstream end.

The specification of bagged product in the current Indonesia tender to buy 20,000t white MOP reinforces this interpretation. Bagged delivery is characteristic of distribution through retail networks, agricultural cooperatives, and smallholder supply chains, rather than bulk industrial processing facilities. Packaging costs add a modest premium to CFR bid pricing, a factor that sophisticated suppliers incorporate into their offers.

Palembang as Destination: Reading the Agricultural Geography

The designation of Palembang as the delivery port carries more information than it might initially appear. As the capital of South Sumatra province, Palembang functions as the primary logistics hub for one of Indonesia's most productive plantation belts. South Sumatra is a major contributor to national palm oil and rubber output, both of which are potassium-intensive crops that require regular potash application across their productive lifespans.

A June-to-August delivery window aligns with seasonal agricultural calendars in this region, positioning the procurement to coincide with mid-year fertilizer application cycles rather than the peak planting season. This timing suggests the importer is managing inventory replenishment rather than responding to an emergency supply shortfall, which is consistent with the deliberate, strategic pacing of the tender sequence described above. However, resource export challenges facing the broader Asia-Pacific region remain a background consideration for procurement planners.

The $383/t India Contract and Its Influence on Indonesian Bidding

India's annual MOP contract negotiations with major global suppliers are the most closely watched pricing events in Asian potash markets. Because India purchases in volumes that dwarf most other single-country buyers, the agreed CFR price reflects genuine market equilibrium between major producers and a price-sensitive, high-volume buyer.

The settlement of India's new contract at $383/t CFR with 180-day credit terms establishes a functional ceiling for Indonesian negotiations. Indonesian buyers, operating with shorter credit terms and smaller volumes than India, will not accept prices at or above the Indian benchmark without pushing back. The implication is that competitive bids for the Indonesia tender to buy 20,000t white MOP are expected to cluster meaningfully below $383/t.

Market intelligence points to multiple major suppliers converging in the $360–363/t CFR range for this tender, reflecting a supply environment where sellers have limited pricing power relative to a well-informed, strategically patient buyer.

Supplier Competitive Positioning

| Supplier | Origin | Estimated CFR Bid Range | Competitive Assessment |

|---|---|---|---|

| BPC | Belarus | $360–363/t | Highly competitive |

| Eurochem | Russia | $360–363/t | Highly competitive |

| Uralkali | Russia | $360–363/t | Highly competitive |

| Arab Potash Company | Jordan | $360–363/t | Competitive, short freight |

| K+S | Germany | $360–363/t | Competitive |

| Canpotex | Canada | ~$400/t | Freight-disadvantaged |

The structural disadvantage facing Canpotex is worth examining in depth. Canadian potash exported to Southeast Asia must traverse Pacific shipping lanes from ports in Vancouver and Portland, adding roughly $30–50/t in freight costs compared to Middle Eastern or European origins on comparable CFR terms. This freight differential is not a temporary disruption; it is a permanent geographic reality that shapes the competitive landscape for every Asian MOP tender.

When Canadian-origin MOP is priced at approximately $400/t CFR into Southeast Asian ports while Belarusian, Russian, and Jordanian suppliers cluster at $360–363/t, the competitive gap is substantial enough to effectively exclude North American supply from price-sensitive tenders unless other factors intervene.

One such factor is the ongoing Western sanctions scrutiny applied to Russian and Belarusian supply corridors. Asian buyers, including Indonesian importers, have continued to procure from these origins, often through intermediary trading structures. However, global trade tensions have introduced additional uncertainty around documentation, banking, and insurance that some buyers prefer to avoid, potentially creating openings for higher-cost but less complex supply chains.

The next major ASX story will hit our subscribers first

Regional Price Contagion: How Indonesia's Award Ripples Outward

The consequences of the Indonesia tender to buy 20,000t white MOP and its anticipated follow-on extend well beyond domestic consumption. Buyers in Malaysia, Vietnam, Thailand, and the Philippines routinely delay their own procurement decisions until Indonesian tender outcomes are confirmed, using the agreed award price as a negotiating reference in their own supplier conversations.

This behaviour creates a cascading price discovery effect that amplifies the market significance of Indonesian procurement events far beyond the volumes involved. A $5/t movement in an Indonesian award price can translate into equivalent shifts across hundreds of thousands of tonnes of regional demand as downstream buyers adjust their expectations accordingly. Furthermore, the World Bank's analysis of potash market dynamics underscores how deeply interconnected Asian fertilizer procurement cycles have become in recent decades.

Short and Medium-Term Market Outlook

| Time Horizon | Market Dynamic | Likely Outcome |

|---|---|---|

| 0–30 days | 20,000t white MOP tender award | Confirms ~$360–365/t CFR floor for Southeast Asia |

| 1–3 months | 155,000t follow-on tender | Sets Q3 2025 regional price trajectory |

| 3–6 months | Post-India contract ripple effects | Supports price stability across Asian MOP markets |

| 6–12 months | Seasonal demand resurgence | Indonesian restocking ahead of 2026 planting calendar |

One scenario that market participants are discussing, though not universally accepted, involves partial volume awards. If the importer awards only a portion of the tendered volume in the initial 20,000-tonne tender, the effective price signal to the market may be softer than headline bid levels suggest, as unsold supply competes for alternative buyers and presses down the marginal clearing price for subsequent tenders.

Key Variables for Market Participants to Track

- Award confirmation and price on the 20,000t white MOP tender (closing 21 May) will deliver the first post-India-contract CFR data point for Southeast Asian white MOP

- Volume take-up in the subsequent 155,000-tonne follow-on tender will be the more consequential signal for regional Q3 2025 potash pricing

- Partial award risk carries downward price implications that extend beyond the immediate tender to affect competing bids across the region

- Canpotex's freight gap of approximately $37/t versus the $360–363/t cluster from other origins remains a structural barrier for North American competitiveness in this market

- Credit term differentials between the India settlement (180 days) and Indonesian terms add another pricing variable that suppliers must adjust for when submitting competitive bids

- Sanctions-related supply chain complexity from Russian and Belarusian origins introduces tail risks for buyers who may face financing or documentation complications, creating a speculative but plausible opening for alternative supply sources over time

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or commodity trading advice. Price estimates, bid ranges, and market projections referenced throughout reflect market intelligence and analytical frameworks at the time of writing and are subject to change. Readers should conduct independent due diligence before making any procurement or investment decisions based on the information presented here.

For ongoing potash market price assessments, trade flow analysis, and fertilizer procurement intelligence, Argus Media's fertilizer market coverage at argusmedia.com provides regularly updated data for market participants across the supply chain.

Want to Identify the Next Major Commodity Discovery Before the Market Moves?

While potash procurement cycles and regional price signals offer valuable context for commodity investors, the real opportunity often lies in being first to act on significant mineral discoveries — and that's precisely where Discovery Alert delivers an edge, using its proprietary Discovery IQ model to translate complex ASX announcements across 30+ commodities into clear, actionable insights the moment they are released. Explore historic examples of major discoveries and their extraordinary returns to understand the scale of opportunity, then start your 14-day free trial and position yourself ahead of the broader market.