June 16, 2026

Industrial Metal Markets Navigate Complex Supply-Demand Dynamics

Global commodity markets reflect intricate patterns where supply-side constraints intersect with evolving demand structures across major consuming regions. Industrial metals, particularly copper, demonstrate how inventory buildups during seasonal lulls can mask underlying structural tensions between mine production capabilities and long-term consumption growth trajectories. Understanding these dynamics requires examining both immediate price consolidation patterns and multi-year demand redistribution trends that reshape global trade flows.

Market participants increasingly focus on inventory accumulation patterns as leading indicators of demand strength, while treatment charge movements signal upstream supply availability. The interplay between these factors creates price consolidation phases that often precede significant directional movements in industrial metal valuations.

When big ASX news breaks, our subscribers know first

Current Market Positioning and Price Consolidation Patterns

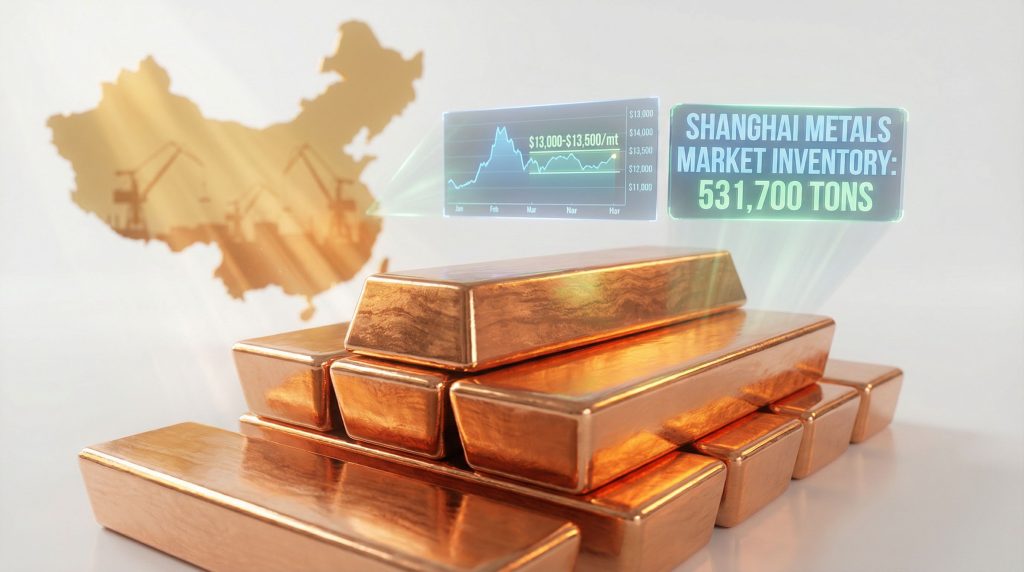

Copper price steadiness reflects a mature consolidation phase within the $13,000-$13,500 per metric ton trading range, where technical analysis reveals institutional positioning strategies operating during periods of reduced volatility. London Metal Exchange data shows spot copper trading at $13,285/mt as of late February 2026, representing a 0.3% decline that follows a brief two-day rally triggered by US trade policy announcements.

Volume patterns during this consolidation suggest accumulation behaviour rather than distribution, with bid-ask spreads narrowing as market participants await demand signals from major consuming regions. The trading range represents psychological support levels where previous price reversals occurred, creating technical floor dynamics that limit downside movement absent fundamental catalysts.

Furthermore, the current consolidation phase aligns with record‐high copper prices observed throughout 2025, suggesting market participants are reassessing valuation levels. According to KS Commodities Ltd trader perspectives, industrial metals currently lack fresh bullish drivers, emphasising the transition from momentum-driven trading to equilibrium-seeking market behaviour.

Treatment charge analysis provides upstream supply indicators that complement price consolidation assessment. When smelters reduce treatment charges, this signals abundant concentrate availability from mines, reducing upstream pricing power. Current treatment charge levels require comparison against five-year historical averages to assess whether supply constraints are intensifying or relaxing during consolidation periods.

The relationship between exchange-registered warehouse stocks and privately-held inventory levels offers additional insight into physical market tightness. London Metal Exchange warehouse data combined with regional inventory surveys provides comprehensive supply availability assessment across major consumption centres. However, these technical indicators must be balanced against global trade impact considerations that influence medium-term pricing dynamics.

Inventory Accumulation Across Global Consumption Centres

Shanghai Metals Market research indicates privately-held copper inventories reached 531,700 tons across major Chinese consumption centres including Shanghai, Guangdong, Jiangsu, Zhejiang, Chongqing, and Tianjin, representing the highest levels since early 2020. This inventory surge occurred during the Lunar New Year holiday period when industrial activity typically halts, suggesting seasonal positioning rather than fundamental demand weakness.

Regional inventory distribution patterns reveal geographic concentration of copper stockpiles, with Shanghai likely representing 25-35% of total inventory based on historical market share data. The ratio of privately-held inventory to exchange-registered warehouse stock indicates physical market dynamics, where simultaneous increases in both categories suggest new supply entering markets without corresponding consumption acceleration.

Key inventory metrics include:

• Days of supply coverage: Current inventory levels relative to average daily consumption rates

• Geographic distribution: Regional stockpile concentration across major industrial centres

• Seasonal adjustment factors: Historical inventory patterns during Lunar New Year periods

• Private versus exchange ratios: Indicators of physical market tightness and liquidity

Manufacturing sectors demonstrated price resistance behaviours, with many fabricators postponing purchases rather than accepting elevated price levels. This behavioural pattern suggests increased price elasticity of demand, where buyers shift purchases to future periods when expecting more favourable pricing conditions.

The inventory buildup timing relative to traditional Lunar New Year factory closures allows seasonal adjustment factors to isolate structural inventory components from cyclical accumulation patterns. Historical comparison with February inventory levels from 2015-2025 establishes baseline seasonal adjustment benchmarks for assessing whether current accumulation represents normal patterns or demand deceleration signals.

In addition, these inventory dynamics must be contextualised within broader copper supply crunch strategies that major industrial consumers are implementing to secure supply chains.

China Industrial Demand Recovery Timeline and Implications

China industrial demand patterns significantly influence global copper market dynamics, with manufacturing sector restart schedules serving as critical demand indicators. Chinese fabricator restart timing typically occurs in early March following Lunar New Year closures, though 2026 patterns suggest potential delays beyond historical norms.

National Bureau of Statistics data tracking manufacturing capacity utilisation rates through Industrial Production Index measurements provides quantitative assessment of recovery progress. The Manufacturing Purchasing Managers' Index disaggregates copper-consuming sectors including electrical equipment, machinery, and construction materials manufacturing, offering sector-specific demand visibility.

Regional recovery speed differentials emerge across major industrial provinces:

| Province | Recovery Timeline | Export Orientation | Copper Intensity |

|---|---|---|---|

| Guangdong | Fastest (mid-March) | High export focus | Electronics/machinery |

| Shanghai | Moderate (late March) | Mixed domestic/export | Industrial equipment |

| Jiangsu | Moderate (late March) | Manufacturing base | Construction materials |

Export manufacturing weakness creates additional complexity for fabricator restart decisions, as weak global demand signals encourage factory owners to delay restart timing for working capital preservation. Manufacturing PMI export order components indicate whether external demand constraints affect restart schedules beyond normal seasonal patterns.

Factory restart delays correlate with weak export orders for copper-containing products including electrical machinery, telecommunications equipment, and construction materials. Historical analysis comparing 2023-2025 restart dates against 2026 patterns reveals whether delays represent structural or cyclical adjustments to demand conditions.

Consequently, traders remain copper steady as traders await return of China industrial demand, highlighting the critical importance of Chinese manufacturing restart schedules.

Long-Term Consumption Geography Transitions

Global copper consumption patterns demonstrate fundamental geographic redistribution moving away from China-dominated demand toward diversified consumption across multiple developed and emerging markets. China's consumption share projections indicate decline from approximately 59% in 2026 to 57% in 2030, representing 200 basis point market share reduction over the forecast period.

US consumption growth trajectory anticipates reaching 2.2 million tons by 2031, increasing from current levels of approximately 1.8-1.9 million tons annually. This growth reflects infrastructure spending acceleration through federal programmes and renewable energy deployment initiatives requiring significant copper intensity per unit of installed capacity.

India represents the most dynamic emerging consumption market, with projections indicating 30%+ growth over the decade driven by:

• Electricity access expansion: Rural electrification programmes requiring transmission infrastructure

• Renewable capacity buildout: Solar and wind installations with high copper content requirements

• Industrial development: Manufacturing sector growth consuming electrical and mechanical applications

• Urban infrastructure: Construction activity in rapidly growing metropolitan areas

Consumption category analysis reveals how demand composition evolves across regions:

- Electrical and electronic applications (35-40% of consumption): Power transmission, telecommunications, consumer electronics

- Construction and architectural (25-30%): Plumbing systems, HVAC equipment, building wiring

- Industrial machinery (15-20%): Motors, transformers, mechanical equipment

- Transportation applications (10-15% and growing): Traditional vehicles and electric vehicle transition

The geographic redistribution carries implications for logistics infrastructure, refining capacity location decisions, and regional copper pricing dynamics. Transportation cost factors become increasingly important as consumption growth occurs farther from traditional mine supply sources.

For instance, understanding the global copper supply forecast becomes essential for assessing how these geographic shifts will impact regional pricing and supply chain strategies.

Mine Supply Constraints and Production Development Challenges

Structural supply limitations create long-term price floor dynamics through operational disruption frequencies and multi-decade project development timelines for new copper mines. BlackRock World Mining Trust analysis emphasises how operational disruptions combined with extended project lead times underpin structural deficits in base metals markets.

Greenfield copper mine development typically spans 8-12 years:

• Exploration and resource definition (2-4 years): Geological assessment and reserve calculation

• Environmental and social impact assessment (2-3 years): Regulatory compliance and community engagement

• Engineering and permitting (2-3 years): Technical design and regulatory approval processes

• Construction and commissioning (3-4 years): Physical development and production startup

These extended timelines create structural barriers preventing rapid supply expansion in response to price increases, establishing multi-year price support mechanisms independent of short-term demand fluctuations.

Major operational disruption categories include:

Labour disputes in Peru and Chile frequently affect operations representing 25-30% of global copper output, creating significant price volatility through supply interruption risks.

Environmental challenges at major operations, particularly Indonesian Grasberg mine complexities, demonstrate how technical difficulties can constrain production from large-scale operations. Water availability constraints affecting Chilean Atacama region operations represent long-term sustainability challenges for established production centres.

Treatment charge movements serve as leading indicators of upstream supply stress, where declining charges signal concentrate scarcity giving miners increased pricing power. Current global average treatment charges tracked against five-year historical averages reveal whether supply constraints are intensifying across the industry.

The next major ASX story will hit our subscribers first

Technology Sector Demand Acceleration and Infrastructure Requirements

Artificial intelligence deployment and data centre expansion create new categories of copper-intensive demand that supplement traditional industrial applications. Power infrastructure requirements for AI-linked data centres demonstrate significantly higher copper content per facility compared to conventional computing installations.

Data centre copper intensity factors:

• Power delivery systems: Electrical distribution requiring high-conductivity copper wiring

• Cooling infrastructure: Heat management systems with extensive copper components

• Backup power equipment: Uninterruptible power supply systems and emergency generators

• Connectivity hardware: Network infrastructure and telecommunications equipment

Electric vehicle transition programmes accelerate transportation sector copper consumption beyond traditional automotive applications. Each electric vehicle contains approximately 80-100 kilograms of copper compared to 20-25 kilograms in conventional vehicles, representing 3-4x consumption multiplication factor as adoption rates increase.

Renewable energy copper requirements per installed capacity:

| Technology | Copper Content (kg/MW) | Infrastructure Type |

|---|---|---|

| Solar photovoltaic | 3,500-4,000 | Wiring, inverters, transformers |

| Onshore wind | 4,000-5,000 | Generators, transmission cables |

| Offshore wind | 8,000-10,000 | Subsea cables, enhanced generators |

Grid modernisation programmes required for renewable energy integration demand extensive copper infrastructure for transmission line upgrades and distribution system enhancements. Smart grid technology deployment further increases copper intensity through advanced metering and control system installations.

Furthermore, these technological developments align with broader copper investment insights that emphasise the strategic importance of copper in the energy transition.

Investment Bank Forecasting Methodologies and Price Projections

Major investment banks employ varying methodologies for copper price forecasting, creating divergent projections that reflect different assumptions about supply-demand balance evolution. Citigroup projects $10,500/mt average pricing with $12,000/mt year-end targets, while JPMorgan anticipates Q2 peaks reaching $12,500/mt followed by moderation.

Goldman Sachs analysis suggests Q4 pricing declining toward $11,200/mt based on supply-demand rebalancing assumptions, contrasting with more bullish institutional perspectives emphasising structural deficit persistence. These forecast variations reflect different weighting of short-term inventory buildups versus long-term consumption growth trajectories.

Forecast reliability assessment requires examination of historical accuracy records for major bank commodity research teams. Model sensitivities to key variables including Chinese demand growth rates, mine supply disruption frequencies, and technology sector consumption acceleration provide insight into projection robustness.

Key forecasting variables and sensitivity ranges:

• Chinese consumption growth (2-4% annually): Impact on global demand baseline

• Mine disruption frequency (5-15% of global output annually): Supply constraint severity

• EV adoption rates (20-40% of new vehicle sales by 2030): Transportation demand acceleration

• Infrastructure spending ($1-3 trillion globally): Construction and utility demand

Portfolio positioning strategies require assessment of copper exposure through major mining equities versus futures contract positioning, with currency hedging considerations for international investments. Sector rotation timing between industrial metals and precious metals allocation depends on macroeconomic cycle positioning and inflation expectations.

However, recent analysis from Goldman Sachs forecasting copper prices suggests potential moderation from current levels, adding complexity to medium-term positioning strategies.

Market Signal Interpretation and Risk Assessment

Short-term technical indicators versus long-term fundamental analysis create signal divergence requiring careful interpretation by market participants. Current overbought technical conditions contrast with structural deficit fundamentals, suggesting different time horizon considerations for investment positioning strategies.

Critical monitoring metrics for copper market assessment:

• Chinese fabricator restart completion rates: Real-time demand proxy measurements

• Treatment charge movement direction: Supply tightness early warning indicators

• Exchange inventory drawdown speeds: Physical market stress assessments

• Manufacturing PMI correlations: Economic activity and consumption pattern relationships

Inventory buildups during seasonal periods may mask underlying consumption trends, requiring adjustment factors to isolate structural demand components from cyclical accumulation patterns. Policy-driven volatility from trade tariff adjustments creates temporary price movements that may not reflect fundamental supply-demand imbalances.

Risk management considerations:

Commodity price volatility requires diversification strategies combining direct copper exposure through mining equities with hedging instruments to manage downside price risks while maintaining upside participation potential.

Seasonal demand pattern analysis helps distinguish temporary market weakness from permanent consumption shifts, particularly important during post-holiday periods when manufacturing activity gradually returns to normal capacity utilisation levels.

The intersection of copper price steadiness with China industrial demand recovery timing creates investment opportunities for market participants who correctly assess whether current consolidation represents accumulation phases preceding demand acceleration or distribution phases indicating fundamental weakness in consumption growth trajectories.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and available data. Commodity investments carry significant risks including price volatility, operational disruptions, and macroeconomic factors beyond investor control. Past performance does not guarantee future results, and readers should conduct independent research and consult qualified financial advisors before making investment decisions.

Seeking Exposure to Copper Market Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant copper and industrial metal discoveries across the ASX, empowering investors to identify actionable opportunities before broader market recognition. Start your 14-day free trial today to gain access to real-time mineral discovery alerts and position yourself ahead of complex supply-demand dynamics shaping commodity markets.