June 12, 2026

The contemporary maritime insurance landscape reveals complex interdependencies between geopolitical stability and global trade flows. When shipping corridors face elevated security risks, insurers must rapidly recalibrate their risk models, often resulting in coverage suspensions that cascade through international supply chains. Understanding these dynamics requires examining the regulatory frameworks governing marine insurance, the decision-making hierarchies within Protection and Indemnity (P&I) clubs, and the economic thresholds that trigger market-wide coverage withdrawals. Furthermore, the insurance and naval escorts for Gulf traffic represents a critical intersection of commercial maritime operations and national security interests.

Understanding War Risk Coverage in Critical Shipping Lanes

Maritime insurance operates through a dual-structure system that separates standard Hull and Machinery coverage from War Risk insurance. This framework emerged from substantial shipping losses during 20th-century conflicts and became standardised through Institute Clauses developed by the International Underwriting Association of London. War Risk coverage specifically addresses damages resulting from hostile acts, including missile attacks, drone strikes, mining operations, and acts of terrorism or piracy.

The Lloyd's of London Joint War Committee (JWC) maintains the authoritative designation of "listed areas" requiring Additional War Risk Premiums (AWRP). These areas undergo continuous evaluation based on documented hostile activity, proximity to active conflict zones, and verified threats to commercial shipping. Current JWC-listed areas span multiple continents, including sections of the Black Sea, various African maritime zones, and specific South American waters.

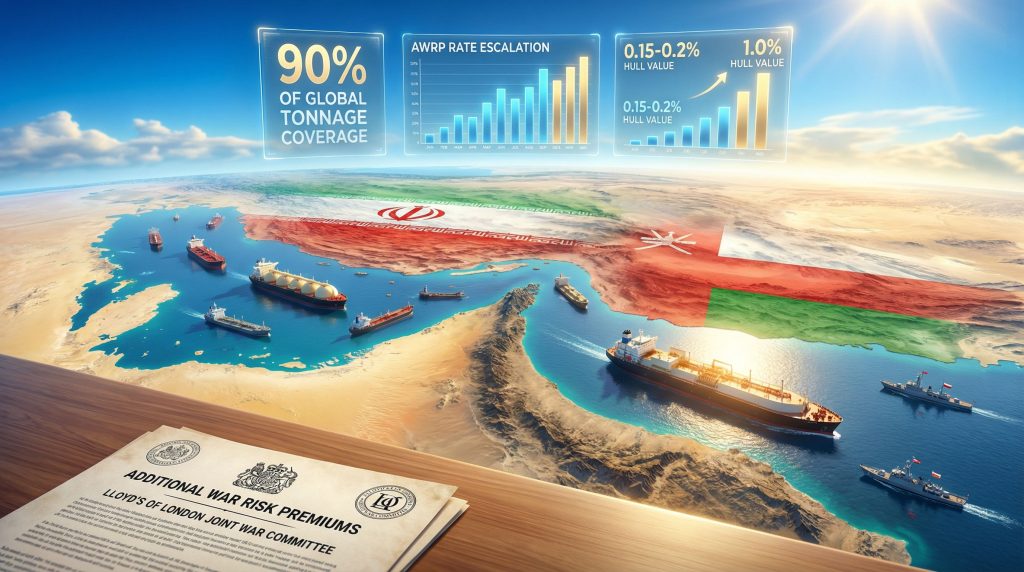

AWRP Rate Escalation Examples:

• Pre-conflict Gulf rates: 0.15-0.2% of hull and machinery value

• Crisis-period rates: Approximately 1.0% of hull value

• Impact on 2 million barrel VLCC: Additional $740,000-$890,000 per voyage

• Total insurance burden increase: 500% escalation from baseline levels

The calculation methodology treats AWRP as a percentage of a vessel's total insured Hull and Machinery Value, encompassing the hull structure, main and auxiliary machinery, equipment and fittings, and the vessel's commercial value as a productive asset. This comprehensive valuation approach ensures that premium calculations reflect the full economic exposure insurers face in high-risk transit zones.

Regulatory Framework Governing P&I Club Decisions

Protection and Indemnity clubs operate under complex reinsurance arrangements that create cascading decision-making effects. When reinsurers determine that risk levels exceed acceptable thresholds, they communicate this through coverage suspension notices, premium escalations beyond commercially viable levels, or aggregate limit reductions. These secondary market decisions directly constrain primary insurance availability, as P&I clubs depend on reinsurance capacity to maintain their coverage offerings.

The recent suspension of war risk coverage by major P&I clubs including London P&I, Steamship Mutual Underwriting Association, American P&I, Gard, Swedish Club, Skuld, and NorthStandard P&I illustrates this cascade effect. Reinsurers cancelled coverage before primary clubs formally suspended policies, demonstrating how reinsurance market dynamics drive coverage availability decisions.

When big ASX news breaks, our subscribers know first

What Triggers Insurance Market Withdrawals from Strategic Waterways?

Insurance market withdrawals occur when risk assessment models indicate that premium calculations cannot adequately compensate for potential claims severity. Unlike standard commercial insurance where premium escalation typically maintains coverage availability, marine war risk insurance faces binary decision points where insurers choose complete withdrawal over continued exposure management. Consequently, the US‑China trade impact on global supply chains becomes amplified during such maritime insurance crises.

Risk Assessment Criteria:

• Threat Environment Analysis: Documentation of active hostile activity frequency and severity

• Geographic Specificity: Precise location data correlating incidents to transit routes

• Vessel Vulnerability Factors: Size, speed, defensive capabilities, and cargo type considerations

• Historical Loss Patterns: Claims frequency and severity data from comparable risk periods

The Strait of Hormuz traffic decline exemplifies these threshold effects. Traffic volumes dropped 94% from baseline levels, with only three tankers recorded transiting during peak crisis periods. This dramatic reduction reflects not only direct security concerns but also the practical impossibility of obtaining adequate insurance coverage at any premium level.

Economic Thresholds for Coverage Cancellation

Marine insurers evaluate multiple factors beyond premium adequacy when making coverage decisions. Concentration risk represents a critical consideration, as multiple vessels facing simultaneous loss potential can exceed aggregate coverage limits. Regulatory pressure from capital adequacy requirements further constrains insurer flexibility, particularly when geographic risk concentration threatens overall portfolio stability.

The reinsurance market capacity constraints create binding limitations on primary insurance availability. When perceived risk in specific geographic zones exceeds reinsurers' aggregate risk appetite, they effectively force coverage suspensions regardless of premium levels that primary insurers might theoretically accept. In addition, the oil price rally during such crises compounds the economic pressures on shipping companies already facing elevated insurance costs.

Market Concentration Vulnerabilities:

The five largest P&I clubs control approximately 90% of global tonnage coverage, creating systemic vulnerabilities when multiple insurers simultaneously withdraw from regions.

This concentration creates feedback loops where individual club decisions influence market-wide coverage availability, potentially transforming localised risk assessments into broad-based coverage crises affecting entire shipping corridors.

The Strait of Hormuz: A Strategic Chokepoint Analysis

The Strait of Hormuz serves as the world's most critical energy transit corridor, handling approximately 21 million barrels per day under normal operating conditions according to U.S. Energy Information Administration data. This throughput represents roughly 21% of global petroleum liquids trade, with additional substantial LNG volumes transiting to reach Asian markets.

Daily Energy Transit Comparison:

| Chokepoint | Crude Oil (mb/d) | LNG Volume | Strategic Importance |

|---|---|---|---|

| Strait of Hormuz | ~21,000 | Major LNG flows | Critical for Gulf exports |

| Suez Canal | ~5,500 | Moderate LNG traffic | Europe-Asia connector |

| Strait of Malacca | ~16,000 | Significant LNG volumes | Asia-Pacific gateway |

The economic value of daily commodity flows through Hormuz fluctuates with energy prices but consistently represents billions of dollars in daily trade value. Current market disruptions demonstrate the immediate global impact when this corridor faces operational constraints. Moreover, tariffs impact markets in complex ways that often interact with energy transit disruptions to create compounding economic effects.

LNG Infrastructure Dependencies

Qatar's Ras Laffan LNG export terminal, with 77 million tonnes per year capacity, represents a critical component of global LNG supply infrastructure. Production halts at this facility create immediate supply shortages for major energy-importing nations, particularly in Asia and Europe where long-term purchase agreements depend on consistent Qatari LNG deliveries.

German Chancellor Friedrich Merz's observations regarding energy price impacts reflect broader European concerns about supply security. European energy markets face particular vulnerability due to limited alternative LNG supply sources and pipeline capacity constraints that prevent rapid supply diversification during crisis periods.

How Do Government Insurance Programs Address Maritime Crisis Response?

Government intervention in maritime insurance markets typically occurs through specialised agencies equipped with political risk insurance authorities. The U.S. Development Finance Corporation represents one model for emergency response, offering coverage at competitive rates when private markets withdraw from strategically important corridors.

President Trump recently announced that the United States will provide insurance coverage and possible Navy escorts for all ships travelling through the Persian Gulf and Strait of Hormuz. This unprecedented move represents a significant escalation in government intervention within maritime insurance markets, demonstrating how insurance and naval escorts for Gulf traffic can become matters of national policy during geopolitical crises.

Emergency Maritime Security Measures:

- Direct Insurance Provision: State agencies providing coverage when private markets suspend operations

- Naval Escort Coordination: Military convoy arrangements with allied forces for high-value shipments

- Alternative Route Development: Government subsidisation of longer shipping routes to maintain supply chains

- Strategic Reserve Deployment: Coordinated release of strategic petroleum reserves to offset supply disruptions

The legislative framework enabling political risk insurance typically includes emergency authorities that allow rapid deployment without standard regulatory approval processes. These mechanisms prove essential when private insurance market withdrawals threaten national economic security or strategic resource flows.

Naval Escort Protocols Under International Maritime Law

Military escort operations operate under complex legal frameworks balancing sovereign immunity protections with commercial shipping requirements. Naval vessels maintain sovereign immunity under international maritime law, but escorted commercial ships retain civilian status and associated legal vulnerabilities. Furthermore, the Trump administration's announcement marks a significant shift in how governments approach maritime security in critical shipping lanes.

Military escort vessels operate under sovereign immunity, but commercial ships retain civilian status and associated legal vulnerabilities under international maritime law.

Freedom of navigation doctrine applications provide legal justification for escort operations in international waters, though practical implementation requires careful coordination with regional maritime authorities and adherence to established convoy protocols.

What Are the Economic Implications of War Risk Premium Surges?

The escalation from baseline AWRP rates of 0.15-0.2% to crisis levels of 1.0% represents a 500% increase in insurance costs, but these premiums remain secondary to freight rate impacts during market disruptions. VLCC rates reaching Worldscale 500 levels create voyage costs approaching $30 million for major crude oil shipments, making AWRP costs approximately 4.5% of total transportation expenses.

AWRP Rate Impact Analysis:

| Vessel Type | Pre-Crisis AWRP | Crisis AWRP | Cost Increase | Total Voyage Impact |

|---|---|---|---|---|

| 2M barrel VLCC | $450,000-$600,000 | ~$1,340,000 | $740,000-$890,000 | ~4.5% of total costs |

| Product Tanker | $200,000-$300,000 | ~$670,000 | $370,000-$470,000 | Variable by route |

| LNG Carrier | $300,000-$500,000 | ~$1,000,000 | $500,000-$700,000 | Route-dependent |

These calculations demonstrate that while AWRP escalation creates substantial additional costs, the broader freight rate impacts dominate overall shipping economics during crisis periods. The relationship between insurance costs and freight rates creates complex optimisation challenges for energy companies managing global supply chains. However, market volatility hedging strategies become increasingly important during such periods of heightened uncertainty.

Supply Chain Disruption Modelling

Alternative routing calculations reveal the broader economic implications of corridor closures. Shipments redirected from West Africa, Brazil, and the United States to Asian markets face substantially longer transit times and correspondingly higher freight costs, creating cascading price pressures throughout global energy markets.

ExxonMobil's strategic response illustrates how integrated energy companies leverage geographic diversification to manage disruptions. The company's global asset portfolio, trading operations, and long-term charter fleet provide operational flexibility, though Hormuz closure still requires active portfolio reoptimisation to maintain supply chain efficiency.

How Do Insurance Market Dynamics Influence Global Trade Flows?

P&I club decision-making hierarchies create systematic vulnerabilities in global shipping coverage. The concentration of coverage authority among major clubs means that coordinated withdrawal decisions can effectively close entire shipping corridors to commercial traffic, regardless of individual shipowner risk tolerance or cargo value considerations.

Reinsurance market pressures amplify these effects by creating binding constraints on primary insurance capacity. When reinsurers establish geographic exclusions or aggregate limit reductions, primary insurers face binary choices between complete coverage suspension or accepting potentially catastrophic exposure levels.

Market Concentration Risks in Marine Insurance

The dominance of major P&I clubs in global tonnage coverage creates systemic risk concentration that extends beyond individual club decision-making. When multiple clubs simultaneously withdraw from specific regions, the remaining capacity often proves insufficient to maintain normal commercial shipping operations. Consequently, developing an energy security strategy requires understanding these insurance market dynamics and their impact on critical supply chains.

Member Consultation Processes:

• Risk Assessment Sharing: Clubs coordinate threat analysis and loss projections

• Reinsurance Capacity Planning: Joint evaluation of aggregate risk exposure limits

• Geographic Risk Pooling: Collaborative approaches to managing regional concentration risks

• Emergency Response Coordination: Protocols for rapid coverage adjustments during crisis periods

These coordination mechanisms, while designed to manage systemic risk, can inadvertently amplify market disruptions when clubs reach similar risk assessment conclusions simultaneously.

The next major ASX story will hit our subscribers first

What Policy Tools Can Governments Deploy During Shipping Insurance Crises?

Government response options extend beyond direct insurance provision to encompass comprehensive maritime security frameworks. International coordination mechanisms through the International Maritime Organisation (IMO) provide standardised crisis response protocols, though implementation varies significantly among member nations based on resource availability and strategic priorities.

Bilateral shipping security agreements offer targeted solutions for specific trade corridors, allowing nations to establish mutual defence arrangements for commercial shipping operations. These agreements typically include provisions for shared naval escort costs, coordinated threat intelligence, and reciprocal port access during emergency situations.

Multilateral Insurance Pool Arrangements:

• Sovereign Risk Sharing: Government-backed insurance pools spreading risk across multiple nations

• Emergency Capacity Provision: Standby insurance mechanisms activated during private market withdrawals

• Cross-Border Coverage Coordination: Harmonised insurance frameworks reducing regulatory barriers

• Strategic Asset Protection: Specialised coverage for critical infrastructure and supply chains

These tools require advance preparation and international cooperation to prove effective during actual crisis periods, as emergency implementation faces significant regulatory and logistical constraints.

How Do Freight Markets Respond to Insurance Coverage Gaps?

Freight futures markets demonstrate complex relationships between insurance availability and shipping rate expectations. VLCC futures declining from Worldscale 380 to Worldscale 335 while spot rates reached Worldscale 500 illustrates market participants' expectations that current crisis conditions may prove temporary, with forward-looking pricing incorporating probability-weighted resolution scenarios.

The divergence between spot and futures pricing reflects uncertainty about conflict duration and resolution pathways. Futures market participants must balance immediate supply disruption impacts against potential rapid normalisation if diplomatic or military resolution occurs more quickly than current conditions suggest.

Worldscale Pricing Mechanism Adjustments

The Worldscale pricing system provides standardised freight rate calculations, but extreme market conditions test the system's ability to reflect actual operating costs and risk premiums. Worldscale 500 levels represent unprecedented pricing for major crude oil routes, indicating that standard pricing mechanisms require adjustment during severe market disruptions.

Forward curve implications for energy companies include hedging strategy reassessment and supply contract renegotiation considerations. Long-term purchase agreements may include force majeure provisions, but practical implementation depends on specific contract language and the duration of shipping disruptions.

What Are the Long-Term Regulatory Implications?

Insurance market reform considerations emerging from current disruptions include enhanced systemic risk oversight for marine coverage and potential government backstop mechanism development. The concentration of coverage authority among major P&I clubs suggests regulatory attention may focus on preventing coordinated withdrawal scenarios that effectively close critical shipping corridors.

International regulatory harmonisation needs include standardised crisis response protocols and coordinated emergency insurance capacity deployment. Current national approaches to maritime insurance regulation create gaps in crisis response capability, particularly for smaller nations lacking comprehensive government insurance programs.

Energy Security Policy Adaptations

Strategic route diversification requirements may emerge as governments recognise the vulnerability created by excessive dependence on single shipping corridors. These policies could include mandated supply source diversification for critical energy imports and investment incentives for alternative transportation infrastructure development.

Public-Private Partnership Frameworks:

• Risk Sharing Arrangements: Government participation in commercial insurance markets during crisis periods

• Infrastructure Investment Coordination: Joint development of alternative supply routes and storage capacity

• Emergency Response Protocol Standardisation: Harmonised procedures for rapid crisis response deployment

• Strategic Asset Protection Programs: Specialised coverage for critical infrastructure and supply chains

These adaptations require balancing market efficiency considerations with national security requirements, creating complex regulatory frameworks that must address both commercial viability and strategic resilience objectives.

Case Study: Historical Insurance Crisis Responses

The 1980s Iran-Iraq War, known as the "Tanker War," provides relevant precedent for understanding insurance market responses to prolonged shipping corridor disruptions. During this period, AWRP rates fluctuated significantly based on threat levels, though comprehensive historical rate data remains proprietary to insurance brokers and not systematically published.

The 2022 Black Sea insurance market crisis following Russia's invasion of Ukraine created partial precedents for current coverage withdrawal patterns. Initial premium escalation gave way to reinsurance capacity constraints that became binding, forcing several P&I clubs to suspend coverage in specific zones while some vessels continued transit under uninsured or self-insured conditions.

COVID-19 Crew Change Insurance Modifications:

During the pandemic, marine insurers adapted coverage terms to address crew change restrictions and port access limitations. These modifications demonstrated the industry's capacity for rapid policy adjustment during unprecedented circumstances, though the current geopolitical crisis presents different risk assessment challenges.

The Bab el-Mandeb strait has maintained JWC listed area status for extended periods due to regional instability and piracy risks, with AWRP rates fluctuating between 0.5-1.5% of hull value during low-activity periods and escalating significantly during documented threat escalations.

How quickly can government insurance programs replace private coverage?

Implementation typically requires 30-60 days for full operational capacity, depending on existing regulatory frameworks and inter-agency coordination mechanisms. Emergency authorities can accelerate this timeline, but practical deployment involves complex coordination between multiple government agencies and international partners.

What legal protections exist for vessels under naval escort?

Military escort vessels operate under sovereign immunity, but commercial ships retain civilian status and associated legal vulnerabilities under international maritime law. Escort arrangements do not transfer sovereign protection to commercial vessels, though they may provide practical security benefits during transit through high-risk areas.

How do AWRP calculations affect smaller shipping companies?

Smaller operators face disproportionate impacts due to limited risk diversification capabilities and reduced negotiating power with insurers. Unlike major shipping companies with global fleet portfolios, smaller operators cannot spread AWRP costs across multiple routes and cargo types, making individual voyage economics more sensitive to premium escalations.

What alternatives exist when private insurance becomes unavailable?

Options include government-backed political risk insurance, self-insurance arrangements, alternative routing through lower-risk corridors, and temporary cargo storage until insurance markets stabilise. Each alternative involves trade-offs between cost, timing, and risk exposure that require careful evaluation based on specific cargo and route requirements.

Disclaimer: This analysis is based on publicly available information and industry reports. Maritime insurance markets remain volatile during geopolitical crises, and specific coverage terms and availability change rapidly. Shipping companies should consult directly with qualified insurance brokers and legal advisors for current market conditions and coverage options. Forward-looking statements regarding market recovery timelines and policy developments represent analytical assessments subject to significant uncertainty.

Understanding insurance and naval escorts for Gulf traffic requires recognising the complex interplay between private market risk assessment, government policy response, and international maritime law frameworks that govern crisis response mechanisms in critical shipping corridors.

Ready to Capitalise on Maritime and Energy Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of broader market movements in energy, commodities, and resource sectors. With shipping insurance crises creating ripple effects across global supply chains and energy markets, discover how major mineral discoveries can generate substantial returns whilst traditional trading routes face unprecedented challenges.