July 22, 2026

The global energy landscape has entered a period of unprecedented volatility, with supply chain disruptions revealing structural weaknesses in import-dependent economies. Australia's position as one of the world's most petroleum-import-reliant developed nations exposes unique vulnerabilities that extend far beyond simple fuel price fluctuations. The Iran oil crisis impact on Australia demonstrates how interconnected modern economic systems create compounding effects that traditional economic models often underestimate.

Understanding these transmission mechanisms requires examining how energy dependencies intersect with geographic isolation, industrial structure, and monetary policy frameworks. The current market environment provides a stark illustration of these dynamics in action, offering insights into the systemic risks facing resource-rich nations that have paradoxically become energy-import dependent.

Australia's Structural Energy Import Dependency Crisis

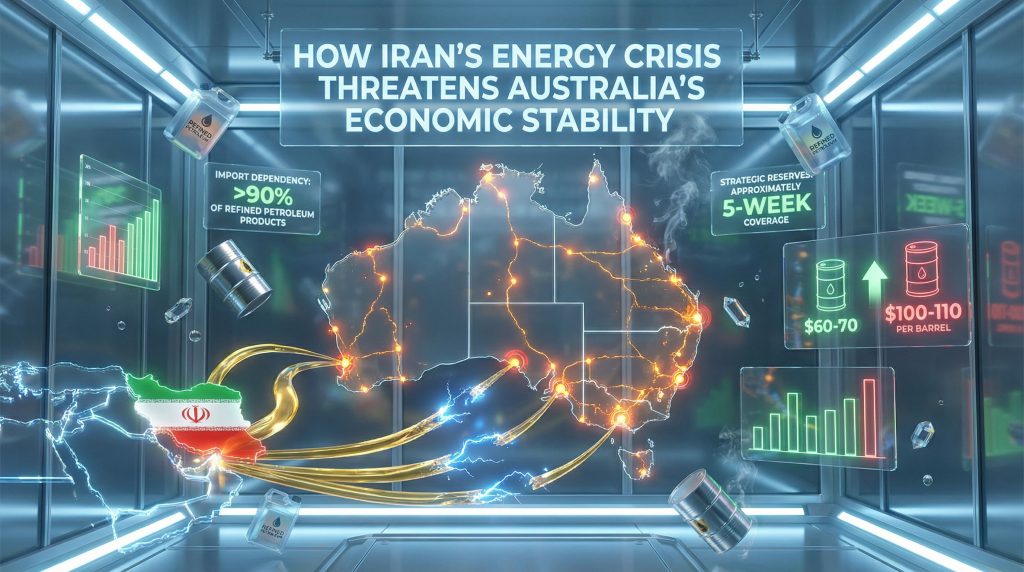

Australia's overwhelming reliance on imported refined petroleum products represents one of the most significant economic vulnerabilities facing the nation. Current data indicates that over 90% of refined petroleum products consumed domestically originate from overseas sources, primarily from Middle Eastern and Asian refineries.

This dependency has evolved over decades of systematic domestic refining capacity reduction. Where Australia once operated 14 refineries in 1985, the nation now relies on just three major facilities: Ampol's Lytton refinery in Queensland, BP's Kwinana facility in Western Australia, and remaining operations in New South Wales and Victoria. Each facility closure reduced strategic flexibility and increased exposure to external supply shocks.

Strategic petroleum reserves provide only 5-7 weeks of import coverage, according to Department of Climate Change, Energy, Environment and Water data. This buffer falls significantly short of International Energy Agency recommendations and creates acute vulnerability during extended supply disruptions.

The geographic concentration of supply sources amplifies risk exposure. Approximately 20-21% of globally traded petroleum flows through the Strait of Hormuz annually, according to U.S. Energy Information Administration analysis. Any disruption to this critical chokepoint directly impacts Australian fuel security due to heavy reliance on Middle Eastern suppliers.

Economic Transmission Pathways

Energy price volatility transmits through the Australian economy via multiple interconnected channels. Furthermore, the complexity of these transmission mechanisms reveals vulnerabilities that extend beyond immediate price impacts.

Primary transmission occurs through transport costs, where diesel price increases immediately affect freight distribution networks. Australian road transport accounts for 85-90% of land freight movement, consuming approximately 10-12 billion litres of diesel annually. Cost pass-through rates typically range from 60-90% within 2-4 weeks of fuel price increases.

Secondary effects emerge through embedded energy costs in goods and services. Cold chain logistics, essential for fresh produce distribution, rely heavily on diesel-powered refrigerated transport and backup power generation. Regional areas face particular vulnerability due to limited natural gas distribution infrastructure outside major urban centers.

Tertiary impacts manifest through wage-price spiral dynamics as cost-of-living pressures generate demands for compensation increases. Energy and fuel components represent approximately 9-10% of the Australian Consumer Price Index basket, meaning significant oil price movements create measurable inflationary pressure.

When big ASX news breaks, our subscribers know first

Geographic and Infrastructure Vulnerabilities

Australia's remote location from major refining centres creates compounding supply chain risks during disruption periods. Typical transit times from Persian Gulf refineries to Australian ports range from 25-35 days, compared to shorter European or North American supply routes.

This geographic disadvantage combines with infrastructure limitations to create systemic vulnerabilities:

- Limited domestic refining capacity eliminates supply chain redundancy

- Concentrated port facilities create single points of failure

- Extended supply lines increase exposure to shipping disruptions

- Just-in-time inventory models reduce buffer capacity during crisis periods

The systematic closure of domestic refineries reflected economic efficiency considerations but eliminated strategic flexibility. Asian refineries achieved superior economies of scale and operational cost advantages, making Australian facilities economically unviable under normal market conditions.

However, this efficiency optimisation created strategic vulnerability. During supply disruptions, Australia cannot increase domestic production to offset import shortfalls, unlike nations maintaining refining overcapacity for security purposes. Consequently, our oil price rally analysis reveals structural weaknesses in import-dependent economies.

Sectoral Impact Analysis and Vulnerability Assessment

Different sectors of the Australian economy face varying degrees of exposure to energy supply disruptions and price volatility. For instance, the agricultural sector demonstrates particular vulnerability due to mechanised farming dependencies.

Agriculture and Food Production Systems

Australian agricultural operations consume approximately 800-900 million litres of diesel annually for mechanised farming, transport, and processing activities. The sector faces dual pressure from fuel cost increases and fertiliser supply disruptions.

Fertiliser dependency creates additional vulnerability, as Australian agricultural operations spend AUD $1.2-1.5 billion annually on imported fertiliser products. Supply disruptions affecting major fertiliser exporters can simultaneously impact both input costs and availability.

Key agricultural vulnerabilities include:

- Limited substitutes for diesel-powered farm machinery

- Multi-month lag between cost increases and commodity price adjustments

- Export competitiveness pressure from lower-cost international producers

- Regional fuel distribution network constraints

Mining and Resources Sector Exposure

Remote mining operations represent particularly high-risk exposure to fuel cost volatility. The sector consumes 2-3 billion litres of fuel annually for extraction, haulage, and power generation at isolated sites lacking grid electricity access.

Mining operations typically face the following vulnerabilities:

| Vulnerability Factor | Impact Level | Mitigation Difficulty |

|---|---|---|

| Diesel dependency for mobile equipment | High | Moderate |

| Remote location fuel logistics | Very High | High |

| Export margin compression | Moderate | Low |

| Alternative energy infrastructure | High | Very High |

For most mining operations, a 10% fuel cost increase translates to 1-2% EBITDA margin compression. While high-value mineral producers can typically absorb these cost increases, lower-margin operations face significant profitability pressure.

Aviation and Tourism Industry Impacts

Australian aviation consumes approximately 8-10 billion litres of jet fuel annually for international operations and 2-3 billion litres for domestic flights. Aviation fuel represents 25-35% of airline operating costs, meaning significant price increases create substantial margin pressure.

Airlines typically pass 80-90% of fuel cost increases to customers through surcharges within 2-4 weeks. However, demand elasticity varies significantly:

- Business travel shows relatively low price sensitivity

- Leisure travel demonstrates higher elasticity, particularly for discretionary trips

- Regional routes face greater impact due to limited alternative transport options

Tourism sector implications extend beyond aviation costs. The industry generates AUD $45-50 billion in international visitor expenditure and AUD $50+ billion in domestic tourism annually, supporting approximately 270,000 jobs.

Monetary Policy and Inflationary Transmission Mechanisms

Oil price shocks create complex challenges for monetary policy frameworks. The Reserve Bank of Australia faces competing pressures when energy costs surge due to supply disruptions rather than demand increases.

Temporary supply shocks typically warrant monetary accommodation to avoid unnecessarily constraining economic activity. However, persistent disruptions risk embedding inflationary expectations into wage bargaining and pricing decisions across the economy.

Historical precedent from the 2008 oil crisis illustrates this policy dilemma. Initial RBA accommodation helped maintain economic stability, but subsequent tightening became necessary when inflation expectations began rising beyond target ranges.

Inflation Transmission Timeline

Energy cost increases flow through the economy via predictable pathways with varying time horizons. Moreover, understanding these transmission patterns helps policymakers and businesses prepare appropriate responses.

Immediate Impact (1-2 weeks):

- Direct fuel cost pass-through to consumers

- Transport sector margin compression

- Aviation fuel surcharge implementation

Short-term Effects (2-4 weeks):

- Freight cost increases reflected in wholesale prices

- Food distribution cost escalation

- Regional fuel supply tightening

Medium-term Transmission (4-8 weeks):

- Retail price adjustments across goods categories

- Wage pressure emergence in transport-intensive sectors

- Business input cost renegotiation

Long-term Embedding (8-16 weeks):

- Inflation expectation shifts in wage bargaining

- Service sector cost-of-living adjustments

- Monetary policy response implementation

Strategic Economic Vulnerabilities and System Risks

Australia's energy import dependency reveals broader structural economic vulnerabilities that extend beyond immediate price impacts. In addition, these systemic risks require comprehensive policy responses to address underlying structural weaknesses.

Supply Chain Concentration Risk

The geographic concentration of petroleum imports creates systemic risk through multiple channels:

- Source concentration: Heavy reliance on Middle Eastern and Asian suppliers

- Route concentration: Critical dependence on Strait of Hormuz shipping lanes

- Processing concentration: Limited domestic refining alternatives

This concentration eliminates redundancy that could provide stability during regional disruptions. Unlike diversified supply portfolios, concentrated sourcing amplifies the impact of any single-point failure. Furthermore, oil price trade-war impact demonstrates how geopolitical tensions can exacerbate supply chain vulnerabilities.

Emergency Response Capacity Limitations

Australia's strategic petroleum reserves provide minimal buffer against extended supply disruptions. The current 5-7 week coverage falls substantially short of recommended 90-day strategic reserves maintained by other International Energy Agency member nations.

Limited emergency response capacity constrains policy options during crisis periods:

- Reserve releases provide only temporary price relief

- Demand rationing creates severe economic disruption

- Alternative supplier activation requires weeks to implement

- Domestic production increases impossible due to refining capacity constraints

Long-term Structural Adjustment Pathways

Extended energy supply disruptions may catalyse fundamental changes to Australia's energy security infrastructure and economic structure. However, successful transition requires coordinated policy initiatives and significant investment commitments.

Energy Transition Acceleration

Crisis periods often accelerate adoption of alternative energy technologies and infrastructure. Consequently, energy transition strategies become increasingly important for long-term energy security:

- Renewable energy project development gains urgency and policy support

- Electric vehicle infrastructure expansion accelerates to reduce petroleum dependency

- Alternative fuel production capabilities receive increased investment attention

- Battery storage systems development addresses grid stability concerns

Investment Flow Redirection

Capital allocation patterns shift toward energy security infrastructure during supply crisis periods:

- Domestic refining capacity restoration projects gain economic viability

- Strategic reserve expansion programmes receive policy priority

- Supply chain diversification initiatives attract private and public investment

- Energy independence technologies receive accelerated research and development funding

The next major ASX story will hit our subscribers first

Economic Recovery Scenarios and Investment Implications

Multiple resolution pathways exist for current energy supply disruptions, each carrying different economic implications and investment opportunities. Furthermore, understanding these scenarios helps investors and policymakers develop appropriate response strategies.

Optimistic Resolution Scenario (3-6 months)

Diplomatic breakthrough restores normal shipping operations and supply chains:

- Oil prices normalise to historical ranges of US$70-80 per barrel

- Economic disruption remains contained to transport and energy-intensive sectors

- Inflation spike proves temporary without embedding expectations

- Monetary policy maintains current trajectory without emergency tightening

Investment implications: Cyclical recovery opportunities in transport, tourism, and discretionary consumption sectors.

Extended Disruption Scenario (6-18 months)

Sustained supply constraints require structural economic adjustments:

- Oil prices remain elevated above US$100 per barrel for extended periods

- Accelerated energy transition investments become economically compelling

- Significant monetary policy tightening required to contain inflation expectations

- Government intervention in strategic industries to ensure supply security

Investment implications: Energy security infrastructure, renewable technology, and inflation-protected assets gain investment priority.

Severe Disruption Scenario (18+ months)

Complete supply route closure triggers emergency economic measures:

- Emergency fuel rationing and allocation systems implementation

- Severe economic recession as energy constraints limit productive capacity

- Fundamental energy policy overhaul with massive infrastructure investment

- International cooperation agreements for emergency supply sharing

Investment implications: Defensive positioning in essential services, energy security technologies, and alternative transport solutions becomes critical.

How Will Australia Navigate This Energy Security Challenge?

Australia's response to current energy security challenges will likely require coordinated action across multiple policy domains. Moreover, the complexity of these challenges necessitates both short-term stabilisation measures and long-term structural reforms.

Immediate Stabilisation Measures

Short-term policy tools can provide temporary relief during supply disruptions:

- Strategic petroleum reserve releases to moderate price spikes

- Fuel excise tax adjustments to reduce consumer price impact

- Transport sector support programmes to maintain freight network viability

- Regional fuel security initiatives to prevent supply shortages in remote areas

However, these measures address symptoms rather than underlying vulnerabilities. Global trade impact analysis demonstrates how temporary measures require complementary structural reforms.

Medium-term Structural Reforms

Longer-term policy initiatives address underlying vulnerability sources:

- Energy security legislation development establishing strategic reserve requirements

- Domestic refining capacity incentive programmes improving supply chain resilience

- Alternative fuel transition support reducing petroleum import dependency

- International supply agreement diversification reducing geographic concentration risk

What Are the Long-term Implications for Australian Energy Security?

The Iran oil crisis impact on Australia reveals fundamental structural weaknesses that require comprehensive policy responses. Furthermore, understanding these vulnerabilities provides insights into necessary strategic adjustments for long-term economic resilience.

According to recent analysis by the Australian Financial Review, Australia faces particular vulnerability due to its geographic isolation and import dependency. Meanwhile, ABC News reports suggest that extended disruptions could trigger emergency rationing measures unprecedented in peacetime Australia.

The Iran oil crisis impact on Australia extends beyond immediate fuel costs to encompass broader economic security implications. These include supply chain vulnerabilities, inflationary pressures, and monetary policy challenges that require coordinated responses from government, industry, and financial markets.

Consequently, addressing these challenges requires understanding how US oil production decline affects global supply dynamics and Australia's relative position in international energy markets. The interconnected nature of global energy systems means that regional disruptions can create worldwide implications for import-dependent economies.

The Iran oil crisis impact on Australia therefore represents more than a temporary supply shock – it reveals structural vulnerabilities that require fundamental policy reconsideration and strategic investment in energy security infrastructure. Understanding these dynamics provides essential context for navigating an increasingly volatile global energy environment.

Disclaimer: This analysis contains forward-looking statements and economic projections that involve inherent uncertainties and risks. Historical precedents may not accurately predict future outcomes. Readers should conduct independent research and consult qualified financial advisors before making investment decisions based on this analysis.

Are You Prepared for Australia's Next Energy Security Challenge?

Australia's vulnerability to energy supply shocks creates unique opportunities for investors who can identify companies positioned to benefit from the nation's urgent need for energy security infrastructure and alternative solutions. Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries in critical minerals and energy transition metals, delivering actionable insights that help investors capitalise on Australia's strategic infrastructure development ahead of the broader market.