May 9, 2026

The Clock Beneath the Sand: Why Physics May Force Iran's Hand Before Diplomacy Does

Every geopolitical standoff eventually runs into something that cannot be negotiated, sanctioned, or bombed into submission. For Iran in the spring of 2026, that immovable force is not a naval fleet or a diplomatic ultimatum. It is the subsurface physics governing oil reservoirs that were first drilled when much of the modern world was still colonial territory.

Iran's oil industry geological time bomb is not a metaphor. It is a measurable, data-driven countdown with a hard physical endpoint. Understanding why requires stepping away from the headlines and into the reservoir itself, where the real leverage in this standoff is quietly accumulating.

When big ASX news breaks, our subscribers know first

What Actually Happens Underground When Production Stops

Most people visualise oil fields as underground lakes waiting to be pumped dry. The reality is far more complex, and that complexity is precisely what makes Iran's situation so precarious.

Iran's primary producing fields, concentrated in Khuzestan Province in the country's southwest, sit within the Asmari carbonate formation: a fractured limestone geology that operates on gravity-driven drainage mechanisms. Unlike younger, higher-pressure reservoir systems found elsewhere in the Persian Gulf, Asmari-formation fields lack robust natural drive mechanisms such as active aquifer support or gas-cap pressure. This means oil mobility depends entirely on carefully maintained flow conditions. Disrupt those conditions, and the system does not gradually slow down. It breaks.

The sequential process of reservoir damage during a shut-in follows a distinct pattern:

- Flow cessation removes the dynamic pressure relationship that keeps crude mobile throughout the formation.

- Gravity settling begins immediately, with crude oil moving downward toward the reservoir base under its own weight.

- Viscosity increase compounds the problem. Southern Iranian crude carries elevated sulfur content, and high-sulfur oil becomes significantly more viscous as temperatures equilibrate during a shutdown, making the settled crude far harder to mobilise mechanically.

- Pressure dissipation accelerates without active injection programs or natural replenishment. In a gravity-drainage carbonate system, there is nothing to replace the lost drive energy.

- Restart failure becomes increasingly likely as the energy required to lift settled, viscous crude through aging wellbores exceeds the economic value of what can be recovered.

Stephen Innes of SPI Asset Management described the physical consequences of valve closure in stark terms: crude settles to the reservoir bottom and becomes viscous and thick, requiring significant propulsion to bring back to the surface. Innes assessed that the process of rebuilding pressure and successfully resuming flow could take up to a year, with many industry professionals viewing extended shutdowns as functionally terminal for production given the prohibitive restart costs involved. (RFE/RL, April 30, 2026)

The Two-to-Three-Week Threshold That Changes Everything

Not all shut-ins are equal. The distinction between a brief operational pause and a prolonged shutdown is where Iran's geological vulnerability becomes strategically decisive.

Mehdi Moslehi, a UK-based Iranian oil sector risk consultant with a decade of industry experience, identified the critical timing window with precision. Short production halts lasting up to two or at most three weeks can generally be reversed without severe consequences. Beyond that threshold, particularly in the high-sulfur wells that dominate southern Iran, reservoir pressure begins to drop in ways that become increasingly difficult and eventually economically unviable to reverse. (RFE/RL, April 30, 2026)

Furthermore, Iran's oil industry geological time bomb has been extensively documented by energy analysts who note the distinct cliff-edge nature of reservoir failure in mature carbonate systems. The following table illustrates how shutdown duration correlates with restart feasibility across Iran's field types:

| Shutdown Duration | Restart Feasibility | Primary Technical Risk | Estimated Recovery Timeline |

|---|---|---|---|

| 1 to 3 weeks | High | Minimal pressure loss | Days to weeks |

| 3 to 8 weeks | Moderate | Viscosity surge, partial pressure drop | Several months |

| 8 weeks or more | Low to Very Low | Severe pressure depletion, wellbore damage | One year or longer |

| Indefinite | Near impossible in mature fields | Permanent production loss | Unknown or potentially terminal |

"The geological damage threshold in Iran's mature carbonate fields is not a gradual curve. It is closer to a cliff edge. Once reservoir pressure falls below a critical minimum, conventional lift methods become economically unviable, and enhanced recovery programmes may cost more than the recoverable reserves are worth."

This physical reality is underscored by Goldman Sachs research issued on April 23, 2026, which assessed oil sector vulnerability across Persian Gulf producers. The firm's note stated that Iran and Iraq carry a disproportionately high share of production from reservoirs operating at relatively low pressure compared to other Gulf producers. Crucially, the Goldman Sachs assessment qualified recovery prospects after a prolonged closure as potentially only partial, a hedge that implies structural output loss rather than a temporary dip. (Goldman Sachs research note, April 23, 2026, as cited by RFE/RL)

The Storage Countdown: Iran's Hardest Deadline

Understanding the geology explains why shut-ins are catastrophic. Understanding the storage situation explains when they become unavoidable.

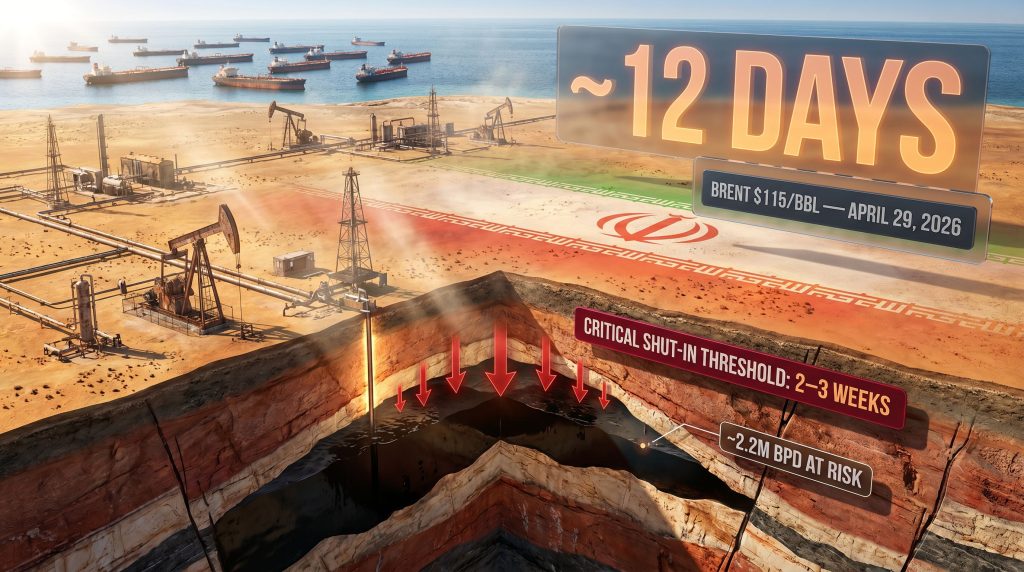

The U.S. naval blockade enforcement began on April 13, 2026. Since that date, shipping analytics firm Kpler reported in its April 27, 2026 analysis that no confirmed tanker had successfully exited the U.S. blockade zone. The enforcement geography is a critical detail: the blockade sits not at the Strait of Hormuz itself but further south, between the Gulf of Oman and the Arabian Sea. Several tankers cleared the Strait but then failed to clear the secondary enforcement zone, making the entire Hormuz passage commercially irrelevant for Iranian exports. (Kpler shipping analytics, April 27, 2026, as cited by RFE/RL)

As of late April 2026, Kpler estimated Iran had approximately 12 days of remaining onshore storage capacity. With southern Khuzestan fields producing roughly 2.2 million barrels per day and offshore fields already partially curtailed at around 500,000 barrels per day, the arithmetic is unforgiving. Storage saturation forces a binary choice:

- Option A: Halt production to prevent overflow, triggering the geological damage cascade described above.

- Option B: Locate alternative export routes before storage capacity is exhausted.

Kpler analyst Homayoun Falakshahi framed the shifting balance of pressure with clarity. Where Iran previously held a time advantage in the standoff, that dynamic had fundamentally changed by late April. Falakshahi assessed that global economic systems can absorb crude prices in the $100 to $120 per barrel range, but warned that a full Strait of Hormuz closure would push prices materially beyond that threshold. (RFE/RL, April 30, 2026)

On April 29, 2026, Brent crude surged to $115 per barrel after the Wall Street Journal reported that U.S. President Donald Trump had directed aides to prepare for an extended blockade, contributing to broader oil market disruption across global commodity exchanges. (Wall Street Journal, April 29, 2026, as cited by RFE/RL)

Are There Any Viable Escape Routes?

Iran's search for alternatives to tanker exports reveals a geography of constraint that has no easy solution.

Rail Delivery to China: Limited Relief

Iran's dominant crude buyer is China, and proposals to deliver oil by rail have surfaced as a potential pressure valve. The logistics are theoretically possible, but the economics and volumes tell a different story. A single Very Large Crude Carrier (VLCC) transports approximately 2 million barrels in a single voyage. Rail freight carries a fraction of that volume per journey, at substantially higher per-barrel transportation cost. Even an aggressive rail programme could not come close to replicating tanker-scale throughput, meaning it might ease storage pressure at the margins without preventing saturation at current production volumes.

The Shadow Fleet: A Deteriorating Asset

Iran maintains a sanctioned tanker fleet of approximately 29 vessels, with roughly half exceeding 20 years of operational age. A significant portion carries extreme risk designations from maritime safety monitoring organisations. The environmental stakes are substantial: a major incident involving these aging hulls could produce an oil spill exceeding the scale of the 1989 Exxon Valdez disaster, with estimated coastal cleanup costs ranging from $860 million to $1.6 billion. Critically, the blockade enforcement zone prevents even willing shadow fleet operators from departing, making fleet condition secondary to the geographic constraint. In addition, geopolitical trade tensions have further eroded the diplomatic cover that shadow fleet operators traditionally relied upon.

The Saudi Asymmetry: Infrastructure Iran Doesn't Have

The starkest comparative disadvantage is infrastructural. Saudi Arabia operates the East-West Pipeline, an overland route connecting its Eastern Province fields to Red Sea export terminals at Yanbu. This bypass insulates Saudi production from Strait of Hormuz disruptions entirely. Iran has no equivalent overland export infrastructure. Its geographic dependency on Hormuz passage is absolute, creating an endurance asymmetry that systematically disadvantages Tehran in a prolonged standoff.

The Contrarian View: Can Any Fields Actually Survive a Shutdown?

The geological picture is not uniformly bleak across all of Iran's production portfolio. The Columbia University Energy Policy Centre has noted that brief production halts in certain field types can allow natural reservoir drainage to redistribute hydrocarbons, with the potential to improve flow rates upon restart. However, this benefit is field-specific and most applicable to formations with active aquifer support or gas-cap drive mechanisms, which are precisely the characteristics absent in southern Iran's dominant carbonate systems.

Iran's West Karoun fields, including the Azadegan development, represent a meaningful exception. These newer production areas share geological characteristics more analogous to Iraqi fields, with moderate rather than extreme shut-in risk profiles. West Karoun currently produces approximately 500,000 barrels per day, with development potential to reach 1 million barrels per day if investment continues. These assets represent Iran's most resilient production base.

The differentiated risk picture across Iran's portfolio can be summarised as follows:

| Field Type | Shut-In Risk Level | Restart Complexity | Long-Term Outlook |

|---|---|---|---|

| Mature southern carbonate fields (Ahvaz, Gachsaran) | Very High | Extreme | High permanent loss risk |

| South Pars gas fields | High | Significant | Duration-dependent |

| West Karoun newer fields (Azadegan) | Moderate | Manageable | Best recovery potential |

| Offshore fields | Moderate to High | Complex | Already partially curtailed |

The next major ASX story will hit our subscribers first

Global Markets Are Already Pricing in the Worst Case

The commodity cascade radiating from the blockade extends well beyond crude oil. Energy markets are pricing in escalation scenarios that, until recently, would have been considered extreme tail risks. Consequently, the oil price shock reverberating through global markets has begun to reshape energy investment strategies well beyond the Persian Gulf.

Key market disruption indicators as of late April to early May 2026 include:

- Global jet fuel exports reached a 10-year seasonal low in April 2026.

- More than 40 India-bound vessels remained stranded near the Strait of Hormuz.

- Lufthansa publicly warned that a sustained Strait of Hormuz closure would add approximately $2 billion in additional fuel costs to its operations.

- European gas traders were actively pricing in scenarios where winter natural gas prices could double.

The following scenario framework illustrates the price trajectory under different resolution timelines:

| Scenario | Brent Price Range | Duration Assumption | Global Economic Impact |

|---|---|---|---|

| Partial blockade, negotiations active | $100 to $115 per barrel | Weeks | Elevated but manageable |

| Extended blockade, no diplomatic resolution | $115 to $130 per barrel | One to three months | Significant supply shock |

| Full Hormuz closure | $130 to $150-plus per barrel | Unknown | Severe global recession risk |

| Iran well shut-ins confirmed | Price spike plus structural supply loss | Long-term | Permanent reduction in OPEC capacity |

"This is not merely a short-term price event. If Iran's mature southern fields suffer permanent reservoir damage, the consequences for global supply will outlast the conflict by years, removing hundreds of thousands of barrels per day from accessible OPEC capacity on a structural basis."

Escalation Options and Their Limits

Iran's potential responses to the blockade are constrained by the same geopolitical risks that the blockade was designed to exploit.

The most plausible escalation pathway involves Iran directing its Houthi proxy forces in Yemen to target Saudi Arabia's East-West Pipeline or disrupt shipping through the Bab al-Mandab Strait. Roughly 10 percent of the world's seaborne oil transits through Bab al-Mandab, making it a high-impact chokepoint. However, this option carries escalation risks that have grown considerably as the United States has expanded its military presence in the region, signalling the potential for a return to direct hostilities in response to proxy actions.

The market's working assumption, as assessed by Innes of SPI Asset Management, is that a negotiated resolution will emerge within approximately three weeks from late April 2026, driven precisely by the kind of geological pressure described throughout this analysis. (RFE/RL, April 30, 2026)

The Long-Term Supply Equation Nobody Is Discussing

The most underappreciated dimension of Iran's oil industry geological time bomb is what happens after any eventual diplomatic resolution.

Years of sanctions have already constrained field maintenance programmes, pressure management investments, and reservoir management expertise. The current blockade-induced shutdown risk sits on top of a production base that has been declining in reservoir health for decades. Even in an optimistic scenario where a deal is reached before critical damage thresholds are crossed, Iran's return to pre-crisis production levels is far from guaranteed. Furthermore, understanding the broader oil geopolitics shaping these dynamics is essential for any realistic assessment of long-term supply recovery.

Goldman Sachs' qualification that recovery may be only partial after a prolonged closure has significant OPEC-level implications. A structurally reduced Iranian production ceiling would alter OPEC's internal balance of power, change spare capacity calculations across the cartel, and potentially shift long-term market share toward Gulf producers with newer, higher-pressure field portfolios. In addition, the global crude outlook for 2025 and beyond already reflected tightening supply assumptions that this crisis has only accelerated.

The Iraq parallel is instructive. Iraq shares similar low-pressure reservoir characteristics with Iran and has experienced its own disruption-recovery cycles. Post-disruption production recovery in Iraq has historically been slower and less complete than initial estimates suggested, providing a directional reference point for what partial recovery actually means in practice.

Key Data Reference: Iran's Oil Sector Under Pressure

| Metric | Data Point | Source Context |

|---|---|---|

| U.S. blockade enforcement start | April 13, 2026 | Naval enforcement begins |

| Remaining storage capacity (late April 2026) | Approximately 12 days | Kpler, April 27, 2026 |

| Southern field production at risk | 2.2 million barrels per day | Mature Khuzestan fields |

| Offshore fields already curtailed | Approximately 500,000 barrels per day | Industry monitoring |

| West Karoun production potential | Up to 1 million barrels per day | If development continues |

| Brent crude price, April 29, 2026 | $115 per barrel | Post-extended blockade signal |

| Market price tolerance ceiling | $100 to $120 per barrel | Kpler analyst assessment |

| Bab al-Mandab seaborne oil share | Approximately 10 percent of global flow | Escalation risk context |

| Lufthansa additional fuel cost estimate | $2 billion | Full Hormuz closure scenario |

| Shadow fleet vessel count | Approximately 29 tankers, half over 20 years old | Maritime monitoring data |

| Critical shut-in threshold | Two to three weeks | High-sulfur southern well expertise |

| Restart timeline post-prolonged shutdown | Up to one year or more | Expert consensus |

Three Scenarios for What Comes Next

The resolution pathways for Iran's geological crisis map onto three broad scenarios with materially different long-term supply consequences:

Scenario A: Negotiated resolution within three weeks. Reservoir damage remains limited. Mature southern fields sustain manageable pressure losses. Production recovery achievable within months, though full pre-crisis output may not return given pre-existing maintenance deficits.

Scenario B: Extended blockade of six to eight weeks. Significant pressure loss occurs across mature fields. Recovery becomes a multi-year project. Structural output reduction of several hundred thousand barrels per day becomes the baseline expectation.

Scenario C: Full Strait of Hormuz closure. Structural production loss across southern fields becomes effectively permanent. Global supply loses a material portion of OPEC capacity at a time when replacement sources are constrained. Oil prices enter territory where demand destruction and recession risk become primary market forces.

The geological vulnerability of Iran's ageing fields has been a subject of concern among energy analysts long before the current blockade brought it into sharp geopolitical focus. Iran's oil industry geological time bomb does not care about the outcome of diplomatic negotiations. It operates on its own timeline, governed by reservoir physics that have been building for eighty-plus years of continuous extraction. The blockade has not created this vulnerability. It has simply started the clock.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial, investment, or trading advice. Price forecasts, production estimates, and scenario projections are drawn from third-party analyst assessments and carry inherent uncertainty. Readers should conduct independent research and consult qualified professional advisers before making any investment decisions. Energy market conditions referenced reflect information available as of late April to early May 2026 and are subject to rapid change.

Want to Track the Next Major Commodity Market Shift Before the Crowd Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying actionable opportunities across oil, gas, and mineral commodities as geopolitical disruptions reshape global supply chains — begin your 14-day free trial today and explore how historic discoveries have generated exceptional returns for investors who moved ahead of the market.