June 10, 2026

The global economy's vulnerability to energy supply disruptions has become starkly apparent as markets grapple with the Iran war and impact on oil prices following recent geopolitical tensions. The interconnected nature of modern economies creates cascading risks when critical energy infrastructure becomes compromised, revealing how dependent industrial societies remain on stable petroleum flows despite decades of diversification efforts.

Understanding Energy Market Transmission Mechanisms During Crisis Periods

Energy security frameworks operate through multiple interdependent channels that can amplify or dampen price volatility depending on the nature and scope of supply disruptions. When geopolitical events affect major transit chokepoints, the economic consequences propagate through both physical and financial markets at different speeds and magnitudes.

Furthermore, the Iran war and impact on oil prices demonstrates how modern energy markets respond to supply chain disruptions. Since February 28, 2026, when U.S. and Israeli strikes on Iranian infrastructure led to the closure of the Strait of Hormuz, oil prices have surged over 50%, creating ripple effects across global commodity markets. These developments have influenced broader oil price movements and regional energy strategies.

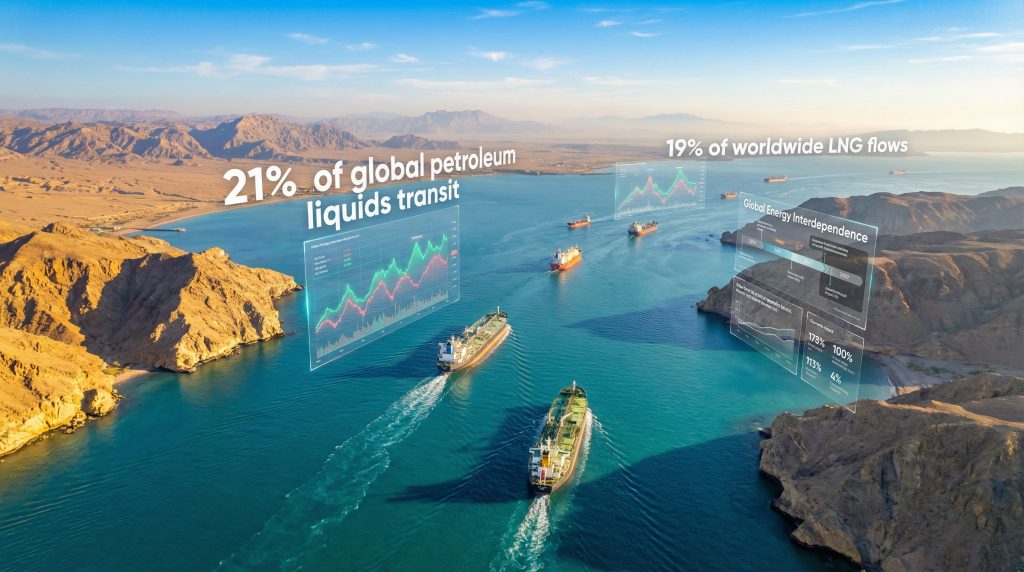

Physical Supply Constraint Dynamics

The Strait of Hormuz closure represents more than a regional shipping disruption. This narrow waterway typically handles approximately 21% of global petroleum liquids transit and 19% of worldwide LNG flows, representing roughly $1.2 trillion in annual energy trade value.

Current market conditions reveal the severity of physical supply constraints:

• LNG supply offline: Approximately 20% of global LNG supply is currently inaccessible due to Gulf shipping restrictions

• Price acceleration: Oil benchmarks have increased over 50% within six weeks of the initial conflict

• Alternative routing pressures: Shipping companies are redirecting cargoes through longer routes, adding $2-5 per barrel in transportation costs

In addition, the immediate price response to physical disruptions typically occurs within 24-72 hours, as demonstrated by current WTI crude trading at $90.99 and Brent crude at $94.93 as of April 15, 2026. This volatility is closely connected to natural gas trends affecting the broader energy complex.

Financial Market Amplification Effects

Modern commodity markets exhibit heightened sensitivity to geopolitical signals due to algorithmic trading systems that process news sentiment in real-time. Alexander Franke, head of risk and trading at Oliver Wyman, observed that most market participants were surprised by the Iran-Hormuz scenario, noting that "before the conflict started, there was strong market conviction that prices would fall rather than spike."

The financial amplification occurs through several mechanisms:

Automated Trading Responses: Algorithmic systems now execute approximately 60-73% of commodity futures trades, creating millisecond-level price responses to news events. Social media posts by political figures have demonstrated greater immediate market impact than fundamental supply reports.

Leveraged Position Unwinding: Commodity traders suffered billions in losses due to incorrect positioning ahead of the conflict. These firms had contractual obligations requiring them to source replacement cargoes at steep costs when their anticipated supply sources became unavailable.

Cross-Asset Correlation Increases: During crisis periods, traditional portfolio diversification breaks down as commodities, equities, and currencies begin moving in tandem, amplifying systematic risk across asset classes.

When big ASX news breaks, our subscribers know first

Regional Vulnerability Assessments and Economic Dependencies

Different geographic regions exhibit varying degrees of vulnerability to Middle Eastern energy disruptions based on their import dependencies and alternative supply access.

Asia-Pacific Energy Dependencies

Asian economies demonstrate the highest exposure to Gulf energy supplies, with regional countries importing approximately 65% of their petroleum requirements from Gulf states. South Korea's recent decision to lock in 273 million barrels of crude through non-Hormuz routes illustrates the strategic repositioning occurring across the region.

Regional Response Patterns:

• China: Utilising stockpiled Iranian oil to cushion against supply disruptions

• Indonesia: Redirecting purchases toward Russian suppliers to avoid Middle East risks

• Japan: Deploying $10 billion in assistance to help Southeast Asian nations cope with energy price shocks

These developments coincide with Saudi exploration licenses initiatives that could reshape regional energy supplies in the medium term.

European Union Adaptation Strategies

While the EU maintains relatively lower direct exposure to Gulf supplies (approximately 15% of total imports), the region experiences significant price transmission effects due to global market integration. European policymakers are considering reduced energy taxes as the Hormuz crisis drives costs higher across the continent.

The EU's diversification efforts toward Azerbaijani and Israeli gas supplies provide some buffer against Middle Eastern disruptions, but cannot fully insulate the region from global price movements.

North American Market Resilience

North America demonstrates the greatest resilience to Middle Eastern supply disruptions, with only 8% of imports coming directly from Gulf states. The U.S. position as a net crude exporter provides additional flexibility, though domestic consumers still face price impacts through global market integration.

Canada's oil companies are reportedly holding back investment despite windfall profits, suggesting cautious capital allocation during volatile periods. This cautious approach reflects broader concerns about US economy tariffs and their potential impact on North American energy trade.

Economic Transmission Through Inflation Channels

Energy price shocks propagate through multiple economic channels, creating both direct and indirect inflationary pressures that can persist long after initial supply disruptions resolve.

Direct Economic Impacts

Transportation and heating costs represent the most immediate transmission channels for energy price increases. Economic research indicates that each $10 per barrel increase in oil prices typically translates to 0.3-0.8% impact on consumer price indices, depending on regional energy intensity and consumption patterns.

Current Sectoral Impacts:

| Sector | Impact Magnitude | Timeline |

|---|---|---|

| Transportation | High (direct fuel costs) | Immediate |

| Petrochemicals | Very High (input costs) | 2-4 weeks |

| Manufacturing | Medium (energy inputs) | 1-3 months |

| Consumer Discretionary | Medium (reduced spending power) | 3-6 months |

Indirect Economic Consequences

Second-round effects emerge as energy-intensive industries pass through higher costs to consumers and adjust production schedules. China's petrochemical sector has already begun cutting output as costs climb, while Norwegian oil export earnings have surged 68% amid the Iran war and impact on oil prices.

GDP Impact Modelling: Economic analysis suggests varying recession probabilities based on sustained oil price levels. Current price levels around $90-95 per barrel, if maintained for 2-3 months, could reduce GDP growth by 0.2-0.5% with recession probabilities in the 15-25% range.

Central Bank Policy Responses to Energy-Driven Inflation

Central banks face complex trade-offs when responding to energy-driven inflation, as traditional monetary policy tools may prove ineffective or counterproductive during supply-constrained periods.

Policy Dilemma Framework

Hawkish Response Risks: Raising interest rates during supply disruptions can amplify economic slowdowns without addressing underlying supply constraints. Higher rates may strengthen currencies, potentially improving terms of trade but reducing export competitiveness.

Accommodative Response Risks: Maintaining loose monetary policy during energy price surges risks unanchoring inflation expectations and creating asset price bubbles during periods of heightened uncertainty.

Historical Response Patterns

Analysis of previous energy crises reveals differentiated central bank approaches:

• Federal Reserve: Typically tolerates temporary energy-driven inflation while monitoring core measures and employment data

• European Central Bank: Shows greater sensitivity to headline inflation measures due to price stability mandate

• Emerging Market Central Banks: Face more severe policy trade-offs due to currency vulnerabilities and import dependencies

Current market conditions suggest central banks are adopting cautious approaches, with some officials signalling willingness to look through temporary energy price increases if broader economic conditions remain stable. These considerations are influenced by OPEC meeting impact assessments and global production strategies.

Long-Term Structural Adaptations and Investment Implications

Energy security concerns are driving structural changes in how economies organise energy procurement, storage, and consumption patterns. These adaptations create both risks and opportunities for investors across multiple sectors.

Strategic Reserve Expansion

Governments are accelerating strategic petroleum reserve buildouts following demonstrated vulnerabilities during the Iran conflict. This represents approximately $50-100 billion in annual investment globally, creating demand buffers that may support higher baseline prices.

Private Sector Inventory Adjustments: Companies are increasing operational inventory levels by 15-30 days of supply, requiring additional working capital but providing protection against short-term disruptions.

Supply Chain Diversification Investments

The crisis has accelerated geographic supplier redistribution patterns, with long-term contracts shifting toward more stable regions. Transportation route redundancy investments are creating new infrastructure corridors that may permanently alter global energy flows.

Regional Energy Hub Development: Countries are investing in becoming regional energy distribution centres, creating infrastructure that can serve multiple supply sources and demand destinations.

Investment Strategy Frameworks for Energy Market Volatility

Professional investors are employing multiple approaches to navigate energy-related macroeconomic volatility, balancing defensive positioning with opportunistic strategies.

Portfolio Risk Management Approaches

Defensive Positioning Strategies:

• Energy sector overweighting: Direct exposure to upstream oil and gas companies during supply disruption periods

• Currency hedging: Protection for portfolios exposed to oil-importing economies

• Inflation-protected securities: Allocation increases to TIPS and similar instruments

Opportunistic Investment Themes:

• Volatility trading: Capitalising on extreme price swings in energy derivatives markets

• Distressed opportunities: Targeting energy-intensive industries facing margin pressure

• Geographic arbitrage: Exploiting regional energy price differentials

Sector Performance Patterns

Energy conflicts typically create predictable sector rotation patterns that sophisticated investors can anticipate:

Outperforming Sectors During Energy Crises:

- Traditional Energy Companies: Upstream oil and gas producers with low-cost assets

- Alternative Energy Infrastructure: Solar, wind, and storage technologies benefiting from energy security concerns

- Energy Efficiency Technologies: Companies providing solutions to reduce energy consumption

Underperforming Sectors:

- Transportation and Logistics: Airlines, shipping companies, and trucking firms facing higher fuel costs

- Energy-Intensive Manufacturing: Steel, aluminum, and chemical producers with high energy input costs

- Consumer Discretionary: Retailers and service providers affected by reduced consumer spending power

BP's recent financial results illustrate these dynamics, with the company reporting exceptional oil trading profits while simultaneously increasing net debt from $22 billion to $25-27 billion due to higher working capital requirements amid price volatility.

The next major ASX story will hit our subscribers first

Market Resolution Indicators and Crisis Management

Several indicators can signal when energy-related economic stress begins subsiding, providing guidance for investment timing and policy responses.

Price Action Resolution Signals

Futures Market Normalisation: Backwardation reduction in oil futures curves typically indicates that markets expect supply disruptions to resolve. Current steep backwardation suggests continued supply stress expectations.

Volatility Index Behaviour: Oil volatility indices (OVX) above crisis thresholds indicate continued uncertainty. Normalisation below historical averages suggests market confidence in resolution.

Cross-Asset Correlation Patterns: Decreasing correlations between energy prices and other asset classes indicate reduced systematic risk transmission.

Fundamental Market Improvements

Supply Source Reactivation: Alternative supply sources coming online or strategic reserve releases can provide immediate relief. Current market conditions show limited reserve deployment, suggesting continued supply tightness.

Demand Destruction Evidence: Economic data showing reduced energy consumption due to high prices indicates natural market adjustment mechanisms taking effect.

Reuters columnist Taosha Wong noted that "because oil and gas are physical commodities vital to economic functioning, supply disruptions immediately lead to higher prices, with price upside often much larger than downside potential." This positive convexity creates asymmetric risk-return profiles that investors must consider.

Policy Intervention Effectiveness

Government intervention success can be measured through preservation of real purchasing power, employment stability in energy-intensive sectors, and trade balance adjustment speeds. Current policy responses appear focused on diplomatic solutions rather than market interventions.

Furthermore, according to the Brookings Institution, the Iran conflict's energy shocks are not yet fully realised, suggesting potential for further market disruption. Additionally, analysis from MarketWatch indicates that while oil markets believe the worst is over, the damage suggests otherwise.

The Iran war and impact on oil prices demonstrates how quickly geopolitical events can reshape global energy markets and economic relationships. Trump's recent social media statements suggesting the conflict is "very close to over" and hinting at diplomatic deals this week illustrate how political developments continue driving market sentiment even as physical supply constraints persist.

Understanding these complex transmission mechanisms enables better preparation for future disruptions and more effective policy responses. Economic resilience requires both short-term crisis management capabilities and long-term structural adaptations that reduce vulnerability to critical supply chain failures. The current crisis serves as a reminder that despite technological advances and diversification efforts, the global economy remains fundamentally dependent on stable energy supplies for continued prosperity.

Looking to Capitalise on Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including energy-critical materials that could benefit from current market disruptions. With oil prices surging over 50% due to geopolitical tensions, subscribers gain actionable insights into energy sector opportunities that could outperform during supply crisis periods. Begin your 14-day free trial today to position yourself ahead of volatile energy markets.