June 12, 2026

The recent iron ore price surge reflects a complex interplay between China's monetary policy adjustments and global commodity market dynamics that fundamentally reshape industrial supply chains. China's central bank announcement regarding reserve requirement ratio cuts and interest rate reductions has created immediate ripple effects across steelmaking raw materials, with iron ore emerging as a primary beneficiary of improved demand expectations. Furthermore, these policy changes demonstrate how interconnected global markets respond to shifts in the world's largest commodity consuming nation.

What Drives Iron Ore Price Volatility in Global Markets?

The Role of China's Economic Policy in Commodity Demand

China's dominance in global iron ore consumption creates an outsized influence on price discovery mechanisms across international markets. Accounting for approximately 70% of global seaborne iron ore trade, Chinese steel production decisions directly impact pricing structures from Australia's Pilbara region to Brazil's Minas Gerais state. When Beijing's central bank announces monetary policy adjustments, the transmission effects flow rapidly through steel mill financing conditions and production planning cycles.

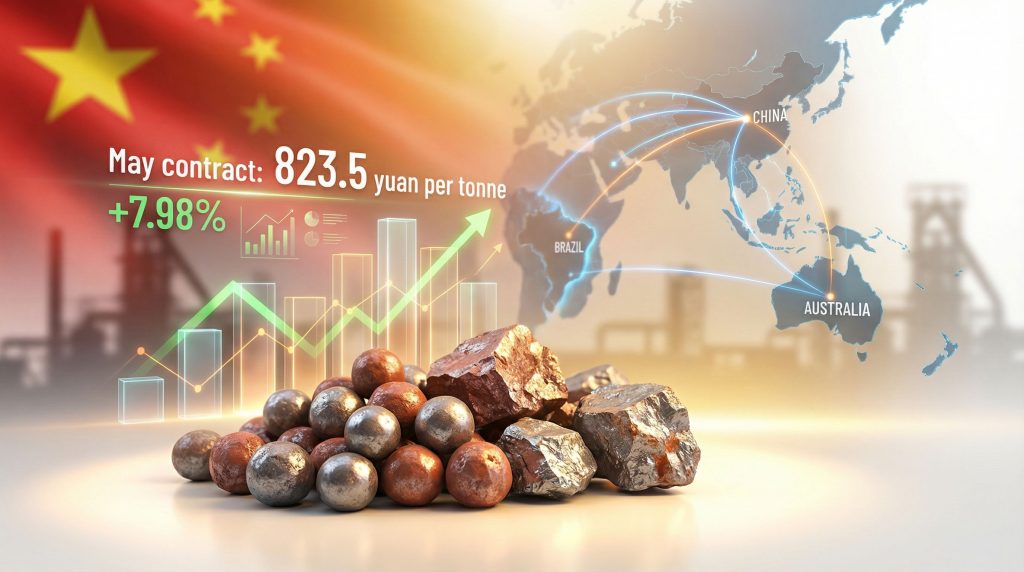

The immediate market response demonstrates this sensitivity clearly. On January 7, 2026, following the People's Bank of China's announcement regarding reserve requirement ratio cuts and interest rate reductions, iron ore futures surged 3.52% on the Dalian Commodity Exchange to 823.5 yuan per metric ton, reaching levels not seen since July 2025. This price action reflects the market's interpretation of improved steel demand prospects under looser monetary conditions.

Chinese steel mills operate within financing frameworks heavily influenced by central bank liquidity policies. When reserve requirements decrease, banks possess additional capital for lending to industrial enterprises, reducing borrowing costs for steel production and expansion projects. This mechanism creates a direct pathway from monetary announcements to raw material purchasing decisions.

Supply-Side Constraints and Market Fundamentals

Global iron ore production faces geographical concentration risks that amplify price volatility during demand shifts. Australia and Brazil collectively supply approximately 80% of seaborne iron ore, creating potential bottlenecks when transportation disruptions or weather events impact shipping schedules. The largest iron ore mines must coordinate with port facilities at Dampier and Port Hedland, while Brazilian miners rely on complex rail networks connecting inland mines to coastal terminals.

Transportation costs represent significant variables in final delivered prices, particularly as freight rates fluctuate with global shipping demand. Capesize vessel rates can account for $10-30 per ton of delivered iron ore costs, depending on route distances and seasonal demand patterns. These logistical factors create additional layers of price sensitivity beyond basic supply-demand calculations.

Quality specifications further complicate pricing mechanisms, as different ore grades command varying premiums or discounts. High-grade ores containing 65% iron content typically trade at substantial premiums to benchmark prices, while lower-grade materials face increasing penalties as steel mills prioritise efficiency improvements.

When big ASX news breaks, our subscribers know first

How Do Central Bank Policies Translate to Commodity Market Movements?

The Reserve Requirement Ratio Effect on Industrial Demand

Reserve requirement ratios function as primary tools for central banks to control money supply and banking sector liquidity. When China's central bank reduces these requirements, commercial banks can extend additional lending equivalent to trillions of yuan across industrial sectors. Steel mills, operating as capital-intensive enterprises, benefit directly from improved credit availability and reduced financing costs.

Historical patterns suggest strong correlations between Chinese monetary easing cycles and iron ore demand spikes. Previous RRR cuts in 2020 and 2022 coincided with notable increases in steel production capacity utilisation and raw material stockpiling activities. Steel mill capacity utilisation rates typically increase 3-5 percentage points within six months following significant monetary policy loosening.

The transmission mechanism operates through multiple channels simultaneously. Lower borrowing costs encourage steel mills to expand production, while improved credit conditions support downstream construction and manufacturing activities that consume steel products. This creates compounding demand effects throughout the industrial supply chain.

Interest Rate Environment and Capital-Intensive Industries

Interest rate adjustments impact steel industry investment decisions across multiple timeframes. Short-term production decisions respond to working capital costs, while longer-term capacity expansion projects depend heavily on prevailing borrowing rates for major capital expenditures. Steel mills typically operate with significant debt loads, making interest rate changes particularly influential on profitability calculations.

Infrastructure investment cycles amplify these effects, as government-led construction projects increase steel consumption substantially. China's infrastructure spending often represents 15-20% of total steel demand, creating powerful multiplier effects when monetary policies encourage expanded public investment programmes.

Real estate sector dynamics add additional complexity, as residential and commercial construction projects consume significant steel volumes. Property development financing costs directly influence construction activity levels, with monetary easing typically supporting increased building permits and steel-intensive construction phases.

What Are the Current Market Fundamentals Driving the Price Surge?

Chinese Steel Mill Inventory Dynamics

| Inventory Metric | Current Status | Seasonal Pattern | Price Impact |

|---|---|---|---|

| In-plant iron ore stocks | Below average levels | Pre-Lunar New Year restocking | Bullish pressure |

| Port inventories | Moderate build-up | Typical Q1 accumulation | Neutral to bearish |

| Steel product inventories | Low across mills | Holiday preparation phase | Supporting demand |

Steel mill inventory management follows predictable seasonal patterns that create recurring market dynamics. Chinese steel mills typically maintain 20-25 days of iron ore inventory under normal operating conditions, but current levels have fallen below these benchmarks heading into the Lunar New Year period. This inventory deficit creates immediate restocking pressure that amplifies price responses to positive demand signals.

Port inventories at major Chinese terminals provide additional market indicators. Qingdao and Rizhao ports currently hold approximately 130 million tons of iron ore, representing moderate levels that neither constrain supply nor create excessive oversupply conditions. These inventory levels suggest balanced near-term supply-demand conditions that support current price levels.

Seasonal Demand Patterns and Restocking Cycles

The Lunar New Year period creates distinctive demand patterns across Chinese industrial sectors. Steel mills typically reduce production during the two-week holiday period while maintaining elevated inventory levels to ensure continuous supply to customers. This seasonal pattern requires advance stockpiling that supports iron ore demand during January and February.

Construction industry seasonal patterns reinforce these dynamics, as building activities typically accelerate following the Lunar New Year period. Spring construction seasons generate 25-30% higher steel consumption compared to winter months, encouraging mills to prepare adequate raw material inventories.

Export demand trends from Chinese steel producers add another layer of complexity. According to Trading Economics data, China exported approximately 90 million tons of steel products in 2025, with export timing often influenced by domestic demand cycles and international price differentials that affect inventory management strategies.

Which Other Commodities Are Experiencing Similar Price Movements?

Steelmaking Raw Materials Complex Performance

The synchronised rally across steelmaking raw materials demonstrates the interconnected nature of steel production supply chains. Coking coal prices surged 7.98% on the same day as iron ore gains, reflecting expectations for increased steel production that requires both raw materials in fixed proportions. Each ton of steel production typically consumes 1.6 tons of iron ore and 0.7 tons of coking coal, creating predictable demand relationships.

Coke prices increased 6.85%, showing strong correlation with both iron ore and coking coal movements. Coke production requires specific coking coal grades and represents an intermediate processing step between coal mining and steel production. The integrated nature of these supply chains means that optimism about steel demand impacts all related commodities simultaneously.

Premium and discount structures across different iron ore grades showed consistent strengthening patterns. High-grade 65% Fe ores maintained $20-30 per ton premiums over benchmark prices, while lower-grade materials saw discount levels narrow as overall demand expectations improved.

Steel Products Market Response

Key Insight: The synchronised rally across the entire steel value chain indicates broad-based optimism about Chinese industrial activity, with rebar gaining 2.26%, hot-rolled coil advancing 1.94%, and stainless steel surging 4.39%, all posting significant advances.

Rebar prices increased 2.26% on the Shanghai Futures Exchange, reflecting construction sector demand expectations. Rebar represents the largest single steel product category by volume, making its price movements particularly significant for overall market sentiment. Construction industry demand typically accounts for 50-55% of Chinese steel consumption.

Hot-rolled coil strengthened 1.94%, indicating optimism about manufacturing sector steel demand. This product category serves automotive, machinery, and appliance manufacturing industries that respond positively to monetary policy easing through improved consumer financing conditions and industrial investment incentives.

Stainless steel jumped 4.39%, the largest gain among steel products. This specialty steel category depends heavily on nickel and chromium inputs, suggesting broad-based optimism about premium steel demand that typically correlates with economic growth expectations.

What Are the Technical Price Levels and Market Projections?

Critical Price Thresholds and Resistance Levels

The Dalian Commodity Exchange May contract reached 823.5 yuan ($117.90) per metric ton, representing its highest level since July 23, 2025. This price breakthrough above previous resistance levels suggests potential for continued upward momentum if demand fundamentals support current optimism levels.

Singapore Exchange February contract touched $108.60, marking the highest level since February 24, 2025. The Singapore benchmark serves as the primary reference for seaborne iron ore trades, making these technical levels significant for international pricing mechanisms.

Multi-month high significance extends beyond simple technical analysis, as these price levels coincide with improved Chinese economic policy expectations. Breaking above six-month resistance levels often indicates fundamental demand shifts rather than temporary speculative movements.

Forward Curve Analysis and Market Expectations

Forward price curves indicate market expectations about future supply-demand balances across different delivery timeframes. Near-term contracts trade at premiums to longer-dated futures, suggesting immediate demand strength while longer-term fundamentals remain more balanced.

Contango versus backwardation patterns provide insights into market structure expectations. Current mild backwardation in near-term contracts suggests immediate supply tightness or strong demand that exceeds forward delivery capabilities.

Implied volatility levels have increased 15-20% across iron ore options markets, indicating heightened uncertainty about future price movements. This volatility increase reflects both optimism about demand improvements and concerns about policy implementation effectiveness.

How Might This Price Rally Impact Global Steel Markets?

Regional Price Transmission and Arbitrage Opportunities

Asian steel pricing dynamics create transmission mechanisms that spread Chinese demand changes to regional markets. Japanese and South Korean steel mills compete for similar raw material supplies, making Chinese demand increases directly relevant for regional iron ore pricing. When Chinese mills increase purchasing, regional competition for Australian and Brazilian supplies intensifies.

European steel markets face indirect impacts through raw material cost pressures and competitive dynamics. European steel producers using different ore grades may find cost advantages or disadvantages depending on how Chinese demand affects specific quality premiums and shipping routes.

North American steel markets operate with greater isolation due to transportation costs and domestic ore supplies, but remain connected through finished steel trade flows. When Chinese steel becomes less export-competitive due to higher input costs, North American producers may benefit from reduced import competition.

Producer Margin Analysis and Investment Decisions

| Producer Category | Margin Impact | Investment Response | Market Share Effect |

|---|---|---|---|

| Low-cost Australian miners | Significant improvement | Expansion acceleration | Market share protection |

| Brazilian exporters | Moderate benefit | Selective investments | Volume optimisation |

| Higher-cost producers | Break-even improvement | Cautious expansion | Survival mode |

Low-cost Australian producers benefit most substantially from price increases, as their operating costs remain relatively stable while selling prices rise. Companies operating in the Pilbara region typically achieve all-in sustaining costs of $25-35 per ton, making current price levels highly profitable and encouraging expansion investments.

Brazilian iron ore exporters experience moderate benefits due to higher transportation costs and different ore quality specifications. Vale's operations in Minas Gerais achieve cash costs of $30-40 per ton including rail and port charges, providing healthy margins at current price levels.

Higher-cost producers worldwide find improved viability at elevated price levels. Operations that struggled near break-even points during recent years may consider resumed production or delayed closure decisions based on improved economic conditions.

The next major ASX story will hit our subscribers first

What Are the Risk Factors That Could Reverse This Price Trend?

Policy Implementation and Effectiveness Concerns

Historical analysis of Chinese monetary stimulus measures reveals mixed success rates in achieving intended economic outcomes. Previous RRR cuts in 2018-2019 failed to generate expected steel demand increases due to concurrent trade tensions and structural economic adjustments. Policy announcement effects may exceed actual implementation impacts.

Global economic headwinds affecting commodity demand present downside risks to current optimism. Slowing growth in major economies could offset Chinese stimulus effects, particularly if European or North American steel demand weakens significantly. International trade tensions may also limit effectiveness of domestic Chinese stimulus measures.

Policy reversal possibilities exist if inflation pressures emerge from monetary loosening. Chinese authorities have demonstrated willingness to quickly adjust policy frameworks when economic conditions change, potentially creating volatility in commodity markets that initially responded positively to easing announcements.

Supply Response and Market Rebalancing Scenarios

New mine development timelines suggest potential supply increases that could pressure prices in medium-term timeframes. Several Australian expansion projects are scheduled for completion in 2026-2027, adding approximately 50 million tons of annual capacity to global supplies.

Inventory normalisation patterns following restocking cycles typically create temporary demand weakness. Once Chinese steel mills achieve target inventory levels, purchasing patterns may moderate significantly, potentially reversing current price momentum within 2-3 months.

Alternative steelmaking technology adoption poses longer-term demand risks for traditional iron ore grades. Direct reduced iron processes and electric arc furnace expansion could gradually reduce blast furnace operations that consume the highest volumes of iron ore per ton of steel output.

Strategic Investment Implications for Market Participants

Portfolio Positioning Strategies

Commodity exposure optimisation requires careful consideration of correlation patterns between iron ore and broader asset classes. During Chinese monetary easing cycles, iron ore typically outperforms general commodity indices while showing increased correlation with Chinese equity markets and copper prices.

Institutional investors may consider iron ore futures positions as hedges against inflation or China economic growth bets. Current futures curves suggest opportunities for both directional positions and spread trades between different delivery months or geographic pricing benchmarks.

Currency considerations add complexity to iron ore investment decisions. Australian dollar strength often accompanies iron ore rallies, affecting returns for international investors and creating additional hedging requirements for comprehensive position management.

Long-term Structural Trends Beyond Current Rally

China's steel demand peak analysis suggests potential structural headwinds for long-term iron ore consumption growth. As urbanisation rates approach developed country levels and infrastructure stock matures, steel intensity per unit of GDP growth may decline significantly over the next decade.

Green steel transition requirements could fundamentally alter raw material demand patterns. Hydrogen-based direct reduction processes may require different ore quality specifications and create demand for premium grades while reducing overall tonnage consumption per unit of steel output.

However, iron ore trends indicate that infrastructure investment cycles globally suggest continued demand support in medium-term timeframes. Developing countries across Asia, Africa, and Latin America require substantial steel-intensive infrastructure development that could offset potential Chinese demand moderation.

Furthermore, recent analysis by Reuters shows that miners demand insights reveal continued optimism about steel consumption patterns. The current iron ore price surge reflects not only immediate monetary policy responses but also underlying structural shifts in global industrial demand patterns that may persist beyond current market cycles.

Additionally, the potential tariff investment impact on global trade flows could further complicate iron ore demand patterns, while understanding the surplus price dynamics becomes crucial for long-term market positioning. These interconnected factors suggest that while the current iron ore price surge represents immediate policy-driven momentum, broader structural considerations will ultimately determine sustained price trends across global commodity markets.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Commodity markets are subject to significant volatility and risk. Readers should conduct their own research and consult qualified financial advisors before making investment decisions. Past performance does not guarantee future results.

Looking for Your Next Iron Ore Investment Opportunity?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including iron ore prospects that could benefit from the current price surge and improved market conditions. With iron ore prices reaching six-month highs and Chinese demand expectations strengthening, understanding which ASX-listed miners are making breakthrough discoveries becomes crucial for positioning ahead of market movements—begin your 30-day free trial today and discover why major mineral discoveries have historically delivered exceptional returns for early investors.