July 8, 2026

When Minority Stakes Become Majority Concerns: The Architecture of Australia's Critical Mineral Enforcement

Most investors assume that foreign ownership only becomes a regulatory problem when it crosses a controlling threshold. The conventional logic is straightforward: hold less than 50%, avoid scrutiny. But in the world of critical minerals, that assumption is dangerously outdated. Australia's regulatory framework has evolved to recognise something more nuanced: that coordinated minority stakes held by related foreign parties can exert strategic influence over an asset every bit as effectively as outright ownership. The ongoing situation involving China-linked Northern Minerals investors and the Jim Chalmers divestment order is the clearest demonstration yet of this principle in action.

When big ASX news breaks, our subscribers know first

Australia's Foreign Investment Framework: What the FATA Actually Empowers

The Foreign Acquisitions and Takeovers Act (FATA) is the legal backbone of Australia's foreign investment screening regime. Administered through the Foreign Investment Review Board (FIRB), it grants the federal Treasurer extraordinarily broad discretionary authority over transactions involving national security assets. This includes the power to issue interim prohibition orders, compel full divestment, and in cases of non-compliance, appoint a statutory agent to force-sell holdings on behalf of the offending investor.

What distinguishes the FATA from equivalent legislation in many other jurisdictions is its treatment of beneficial ownership. Australian law does not limit its scrutiny to direct shareholders. Offshore-registered entities, including those domiciled in the British Virgin Islands or other low-disclosure financial centres, are subject to beneficial ownership tracing rules that look through corporate structures to identify the ultimate controlling party.

For critical mineral assets, the thresholds triggering mandatory review are lower than those applied to general commercial investments. The Treasurer's powers become active well before a foreign party approaches majority control, particularly when the asset in question falls within the highest tier of national security classification.

How Does Australia Classify Critical Minerals for Regulatory Purposes?

Australia's critical minerals strategy established a tiered framework for assessing the strategic sensitivity of different mineral commodities. At the apex of this hierarchy sit heavy rare earth elements, particularly dysprosium and terbium, which occupy a category of strategic sensitivity that most other minerals, including lithium and cobalt, do not reach.

| Mineral Tier | Representative Elements | Strategic Application | Foreign Investment Scrutiny |

|---|---|---|---|

| Tier 1 | Dysprosium, Terbium | Defence guidance, EV motors, semiconductors | Mandatory review; divestment powers active |

| Tier 2 | Lithium, Cobalt | Battery supply chains, energy storage | Enhanced screening thresholds |

| Tier 3 | Graphite, Manganese | Industrial manufacturing | Standard FIRB notification |

The reason dysprosium and terbium sit in Tier 1 is not arbitrary. Dysprosium is a critical additive to neodymium-iron-boron permanent magnets, which are used in the precision guidance systems of missiles, drone propulsion units, and advanced radar equipment. Without dysprosium additions, these magnets lose their coercivity at elevated temperatures, rendering them ineffective for defence applications. Terbium serves complementary functions, enhancing the thermal stability of magnets used in electric motors and solid-state lighting systems.

Critically, more than 85% of global heavy rare earth processing capacity is concentrated within China, giving Beijing substantial leverage over the supply of these materials to Western defence and technology manufacturers. Furthermore, the broader challenges posed by rare earth supply chains underscore why an asset capable of producing dysprosium and terbium outside Chinese-controlled networks carries geopolitical significance that extends far beyond its commercial value.

Northern Minerals and the Browns Range Deposit: Why This Asset Is Strategically Exceptional

Located in the remote East Kimberley region of Western Australia, the Browns Range project is one of a small number of known heavy rare earth deposits outside of China that has reached a stage of development capable of supporting commercial production. This geological rarity is central to understanding why the ownership structure of Northern Minerals has attracted such sustained regulatory attention.

Heavy rare earth deposits are fundamentally different from the light rare earth concentrations that dominate global mine supply. Light rare earth elements, such as cerium and lanthanum, are far more abundant and widely distributed. Heavy rare earths, by contrast, are geochemically scarce and tend to concentrate in specific deposit types, including ion-adsorption clays, which are the predominant source in southern China.

Browns Range hosts xenotime mineralisation, a heavy rare earth phosphate mineral that is notably rare at economic grades outside of China. The deposit's xenotime-dominant profile means its production stream is skewed toward the highest-value, most strategically sensitive elements in the rare earth periodic group, a characteristic that very few non-Chinese deposits share.

Geological note: Xenotime is one of the primary host minerals for heavy rare earth elements, including dysprosium, erbium, and yttrium. Its occurrence at economically viable grades in a politically stable, Western-aligned jurisdiction is genuinely uncommon on a global scale, which is a key reason Browns Range attracts regulatory scrutiny that would not apply to a more typical mineral asset.

Northern Minerals completed a demonstration-scale plant at Browns Range and has produced separated rare earth oxides, including dysprosium oxide, making it one of the few non-Chinese operations to have demonstrated this full processing chain outside laboratory conditions. This operational precedent significantly elevates the asset's strategic profile compared to exploration-stage projects.

The Ownership Structure That Triggered Two Years of Regulatory Escalation

The regulatory concern at Northern Minerals was not triggered by a single large foreign acquisition. Instead, it emerged from the accumulation of multiple smaller stakes that, when assessed collectively, created a combined ownership bloc with the potential to exert coordinated influence over a strategically sensitive company.

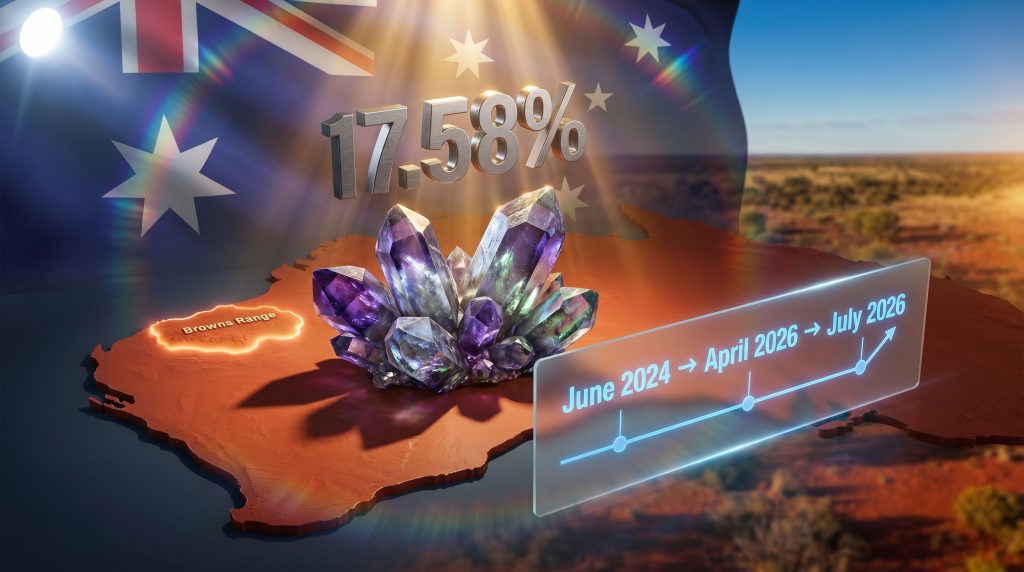

A combined shareholding of approximately 27% across six investors — five with connections to China or Hong Kong and one registered in the British Virgin Islands — created precisely the kind of concentrated foreign interest that Australia's beneficial ownership tracing rules are designed to surface. The specific divestment target under the July 2026 order covers a 17.58% combined stake held by this investor group, subject to a two-week compliance deadline.

Regulatory Insight: Under Australia's foreign investment rules, ownership concentration does not need to reach majority control to trigger national security concerns. Coordinated minority stakes held by related foreign parties can constitute effective influence over a strategically sensitive asset, particularly when those parties share common jurisdictional, commercial, or beneficial ownership connections.

This principle has significant implications for how foreign investors in ASX-listed critical mineral companies structure their holdings. The assumption that sub-threshold individual stakes are inherently low-risk is increasingly untenable when Australian regulators are actively aggregating related positions for the purpose of national security assessment.

A Chronology of Escalating Enforcement

The current divestment order did not arrive in isolation. It represents the second major regulatory intervention targeting Chinese-linked Northern Minerals investors, following a 2024 action that met with only partial compliance.

| Date | Regulatory Action | Outcome |

|---|---|---|

| June 2024 | First divestment order targeting five foreign investors including Indian Ocean International Shipping | Partial non-compliance; Federal Court proceedings initiated in 2025 |

| April 2026 | Interim prohibition order against Ying Tak (Hong Kong-based) | Voting and transfer rights suspended pending full review |

| July 2026 | Second full divestment order covering six shareholders (~17.58% combined stake) | Compliance deadline: July 2; outcome under observation |

The 2024 enforcement gap revealed a structural limitation in Australia's voluntary compliance model. When foreign investors calculate that the financial or strategic value of retaining a holding outweighs the legal risk of non-compliance, the deterrent effect of a divestment order alone is insufficient. The shift to Federal Court proceedings in 2025 marked a deliberate escalation, signalling that Australia's regulatory posture had moved from administrative enforcement to judicial compulsion.

The April 2026 interim order against Ying Tak was a different instrument. An interim prohibition order functions as a regulatory holding mechanism, suspending an investor's ability to vote or transfer shares while full divestment proceedings are prepared. It is a tool designed to prevent value extraction or strategic positioning in the period between regulatory identification of a problem and the issuing of a formal divestment directive.

Treasurer Jim Chalmers' public position on the matter has been unambiguous. He has stated that Australia maintains a rigorous and impartial foreign investment framework and that further measures would be deployed if necessary to protect national interests. This framing is deliberate: it communicates to non-compliant investors that the regulatory response will not be limited to the orders already issued.

Why Non-Compliance With a Sovereign Divestment Order Is Considered Extraordinary

Legal commentary on the Northern Minerals situation has consistently characterised foreign investor non-compliance with a Treasurer's divestment order as extraordinary. To understand why, it helps to examine what the legal consequences of defiance actually entail under the FATA.

Non-compliant parties face:

- Civil penalties under the FATA, which can be substantial and imposed on both the entity and responsible individuals

- Criminal liability in cases where non-compliance is found to be wilful

- Statutory divestiture, where the Treasurer appoints an agent with legal authority to execute a forced sale of the non-compliant holding at market prices, without the investor's consent

- Federal Court enforcement, where judicial orders can compel compliance through contempt proceedings

The 2025 Federal Court action against investors from the 2024 order established a direct enforcement precedent. For the six investors named in the July 2026 order, that precedent is not theoretical. It represents an active legal pathway that Australian regulators have already demonstrated a willingness to pursue.

The investor calculus behind continued non-compliance is not difficult to reconstruct. Browns Range is a genuinely rare asset: a Western-jurisdiction, demonstration-proven heavy rare earth project with established xenotime mineralisation at economic grades. However, reports suggest that China-linked investors continue to flout the divestment order, indicating that the option value of retaining a stake in such an asset outweighs, in some investors' calculations, the legal risks involved.

Jurisdictional complexity compounds the enforcement challenge. Entities domiciled in China, Hong Kong, or offshore financial centres do not face the same practical enforcement exposure as domestically registered Australian investors. Australian court orders cannot be directly executed against assets held offshore, and diplomatic sensitivities constrain the tools available to compel compliance across jurisdictional boundaries.

The next major ASX story will hit our subscribers first

How Australia's Approach Aligns With Allied-Nation Frameworks

Australia's enforcement actions against China-linked Northern Minerals investors do not occur in a geopolitical vacuum. They are part of a broader, coordinated shift among Western-aligned nations toward restricting Chinese investment in critical mineral supply chains. The growing tensions around critical minerals geopolitics have accelerated this trend considerably across Five Eyes nations.

| Country | Regulatory Mechanism | Notable Critical Mineral Action |

|---|---|---|

| Australia | FATA / FIRB | Northern Minerals divestment orders (2024, 2026) |

| United States | CFIUS | Multiple rare earth and battery material blocking orders |

| Canada | Investment Canada Act | 2022 forced divestments from lithium sector |

| United Kingdom | National Security and Investment Act | Rare earth and semiconductor screening regime |

Canada's 2022 directive, which required several Chinese-linked investors to exit stakes in lithium-focused companies, was among the earliest signals that Five Eyes nations were prepared to use investment screening tools aggressively in the minerals sector. The United States has deployed CFIUS to block or unwind Chinese acquisitions across rare earth processing, battery materials, and semiconductor-adjacent mineral assets. The United Kingdom's National Security and Investment Act extended similar powers to cover critical mineral transactions in 2021.

What distinguishes Australia's situation is the persistence of the non-compliance challenge. The fact that the 2024 order was not fully honoured, and that a second and broader order became necessary in 2026, suggests that the enforcement architecture, while legally robust, faces practical limitations when dealing with investors who are willing to test its boundaries. Consequently, the rising critical minerals demand driven by the global energy transition only intensifies these ownership disputes over rare strategic assets.

The Development Trajectory Risk: What Prolonged Ownership Uncertainty Means for Browns Range

Beyond the regulatory and geopolitical dimensions, the Northern Minerals situation raises a practical question that matters to the broader critical mineral supply chain: what happens to the Browns Range development timeline while ownership uncertainty persists?

Prolonged investor instability creates compounding problems for a project at this stage of development:

- Project financing becomes more difficult to secure when lenders and equity partners cannot assess the stability of the shareholder register

- Offtake agreements with Western allied-nation manufacturers, including those in the defence and EV sectors, are harder to negotiate when counterparties are uncertain about who will ultimately control the asset

- Development milestones may be delayed if management bandwidth is consumed by regulatory proceedings rather than operational execution

- Western-aligned capital that might otherwise fill the ownership gap created by divestment may adopt a wait-and-see posture until the shareholder register is fully resolved

The irony of this dynamic is that the regulatory intervention designed to protect a strategic asset can, if prolonged, itself become a risk to the asset's development. This is not an argument against enforcement; it is an argument for enforcement speed and finality.

Whether domestic Australian capital, sovereign wealth mechanisms, or Five Eyes-aligned institutional investors are positioned to absorb the divested stake at the conclusion of this process remains an open question. It is one that carries implications not just for Northern Minerals, but for the broader question of whether Australia can translate its regulatory authority over critical mineral ownership into genuine supply chain outcomes. Indeed, the broader challenge of China's rare earth restrictions further complicates the calculus for Western nations seeking alternative supply sources.

Frequently Asked Questions: Jim Chalmers' Northern Minerals Divestment Order

What Is the Jim Chalmers Northern Minerals Divestment Order?

A formal directive issued by Australia's Treasurer under the Foreign Acquisitions and Takeovers Act, requiring six shareholders with connections to China, Hong Kong, and the British Virgin Islands to divest a combined 17.58% stake in Northern Minerals, a Western Australian heavy rare earth company, on national security grounds.

Why Is Northern Minerals Considered a National Security Asset?

Northern Minerals operates the Browns Range deposit, which hosts xenotime mineralisation capable of producing dysprosium and terbium — heavy rare earth elements essential to the manufacture of defence guidance systems, electric vehicle motors, and advanced semiconductors. The deposit's heavy rare earth profile and its status as one of the few demonstration-proven non-Chinese sources of these materials places it at the apex of Australia's strategic mineral hierarchy.

What Happens If the Investors Refuse to Comply?

Under the FATA, the Treasurer can escalate to Federal Court enforcement, appoint a statutory divestiture agent to execute forced sales, and pursue civil or criminal penalties against non-compliant parties. Australia's 2025 Federal Court proceedings against investors from the 2024 order establish a direct enforcement precedent for exactly this scenario.

Is This the First Divestment Order Involving Northern Minerals?

No. A previous divestment order was issued in June 2024, targeting five foreign investors. Partial non-compliance with that order led to Federal Court action in 2025, making the 2026 order a second and more expansive enforcement intervention covering six shareholders.

How Does This Relate to Australia's Broader Critical Minerals Policy?

The divestment orders are consistent with Australia's 2023 Critical Minerals Strategy and align with allied-nation efforts by the United States, Canada, and the United Kingdom to limit Chinese investment in strategic mineral supply chains. They reflect a hardening regulatory posture that has moved from voluntary compliance expectations to active judicial enforcement.

This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. References to regulatory proceedings, ownership figures, and enforcement timelines are based on publicly available information current at the time of writing. Readers should seek independent professional advice before making investment decisions related to any of the companies, assets, or regulatory matters discussed. Forward-looking statements and scenario projections involve inherent uncertainty and should not be relied upon as predictive of future outcomes.

Want to Stay Ahead of Significant ASX Mineral Discoveries Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant, actionable alerts on high-potential mineral discoveries — including the rare earth and critical mineral sectors at the centre of today's most consequential geopolitical investment themes. Explore historic discoveries and their exceptional returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.