July 9, 2026

Chile's Mining Fiscal Architecture at a Crossroads

The economics of large-scale resource extraction are governed by a deceptively simple principle: capital flows toward certainty. A mine that takes a decade to build, another decade to reach peak output, and a third decade to recoup its investment cannot be financed against a backdrop of shifting sovereign tax obligations. This is not a peripheral concern for mining executives; it is the central variable in every feasibility model, every internal rate of return calculation, and every board-level decision about where to deploy capital in a world increasingly hungry for copper and lithium.

Chile, the country responsible for approximately 27% of global copper production, has spent the better part of a decade watching that certainty erode. Successive legislative cycles produced competing royalty proposals, prolonged permitting gridlock, and no durable framework for long-term fiscal stability. The result has been a gradual repricing of Chilean sovereign risk upward, even as critical minerals demand for the metals beneath its soil has never looked stronger.

The Kast mining tax plan in Chile, embodied in the Reconstruction and Economic Development bill known as the RED bill, is the most structurally ambitious attempt to reverse that trend in over fifty years.

When big ASX news breaks, our subscribers know first

What the RED Bill Actually Proposes: A Framework Analysis

Introduced in April 2026 and subsequently passed by the Chilean House of Representatives, the RED bill is currently navigating Senate debate as of mid-2026. Understanding it requires separating three distinct reform pillars that are often conflated in commentary.

Corporate Tax Reduction: A Phased Architecture

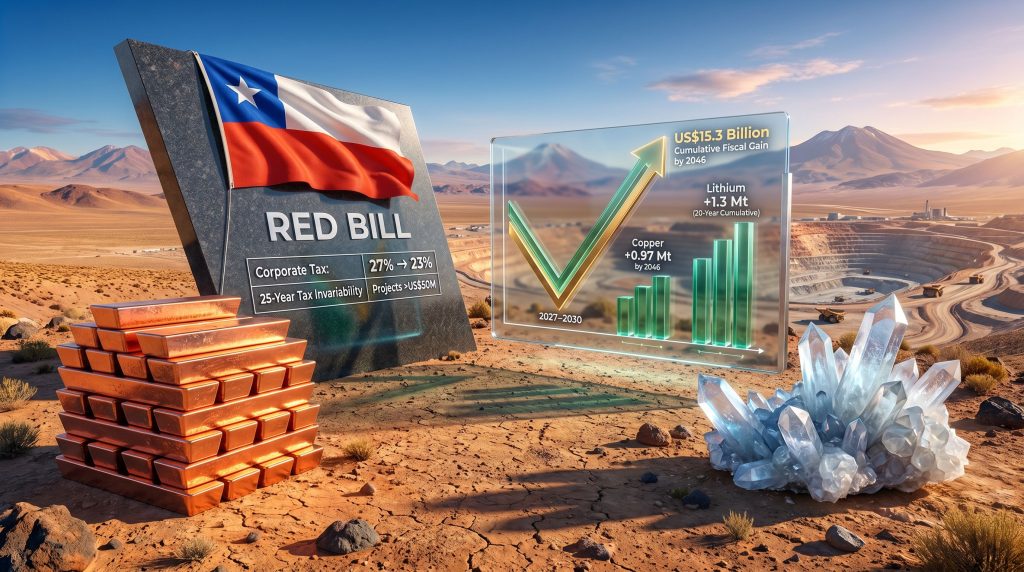

The headline measure is a reduction in the corporate tax rate from 27% to 23% for large enterprises, phased in across a four-year window from 2026 to 2029. Small and medium enterprises face a slightly longer transition, completing the same rate reduction by 2030.

| Reform Element | Current Position | Target Position | Timeline |

|---|---|---|---|

| Corporate Tax Rate (Large Enterprises) | 27% | 23% | 2026–2029 |

| Corporate Tax Rate (SMEs) | 27% | 23% | 2026–2030 |

| Effective Tax Cap (Foreign Investors) | Uncapped combination | 35% ceiling | Upon enactment |

| Mining Royalty Structure | Unchanged | Unchanged | No reform proposed |

The phased approach reflects deliberate fiscal conservatism. An immediate rate cut would generate short-term revenue pressure that could strain Chile's social spending commitments. By staggering the reduction, the government signals long-term intent while managing near-term budgetary exposure. Crucially, the bill introduces a 35% effective tax cap for foreign investors, combining corporate tax, royalties, and all other levies into a defined ceiling. This gives investors something they have not had before: a knowable maximum fiscal exposure.

What the RED bill does not touch is equally telling. The decision to leave Chile's existing mining royalty structure completely unchanged was not an oversight. The royalty debate has been among the most politically toxic in Chilean legislative history over the past five years, having consumed enormous political capital during the Boric administration. By ringfencing royalties entirely, the Kast government has chosen to advance what is achievable rather than reopen what nearly proved impossible.

The 25-Year Invariability Regime: Chile's Most Consequential Legal Innovation Since the 1970s

The mechanism that mining analysts and project developers are paying the closest attention to is not the tax rate itself but the 25-year tax invariability regime available to projects committing capital above US$50 million.

Under this structure, qualifying projects receive a legally binding guarantee that the royalty rates, corporate tax rates, and levy conditions applicable at the time of their investment approval cannot be altered for a quarter century. No future government can introduce new sector-specific levies or change the fiscal parameters to which these projects were underwritten.

The fundamental problem for mining investment is not the current tax rate. It is the risk that the tax rate three, five, or ten years from now will be materially different. A 25-year invariability regime directly severs that uncertainty from project valuations.

This matters because of a structural mismatch that is poorly understood outside the industry. Large copper operations typically require 15 to 30 years to recoup the capital invested in their development. A four-year political cycle represents noise relative to that timeline; a succession of four-year cycles, each capable of introducing new fiscal demands, represents existential risk to project economics. The invariability regime converts that multi-decade sovereign risk exposure into a manageable, bounded variable.

The historical parallel is instructive. Chile's Decree Law 600, repealed in 2015, provided a form of tax invariability for foreign investors. Its absence has been consistently cited in investment community analyses as a structural gap that raised the risk premium embedded in Chilean project discount rates. The RED bill's invariability regime is in many respects an evolution of that architecture, extended to a longer horizon and explicitly designed for the lifecycle realities of modern resource extraction. Furthermore, the Chile copper price outlook reinforces why long-term fiscal certainty is now critical to unlocking stalled project pipelines.

Permitting Reform: The Operational Constraint That Tax Cuts Alone Cannot Solve

Beyond fiscal architecture, the RED bill addresses what many project developers identify as their most immediate operational frustration: environmental approval timelines that routinely exceed 1,000 days for major mining projects.

Permitting speed is not simply an administrative inconvenience. Every additional day of pre-production delay represents holding costs on sunk capital, compressed project economic life, and reduced internal rates of return. A project that could begin generating revenue in year seven instead begins in year nine has materially different investment economics, regardless of what corporate tax rate applies once production starts.

Competing jurisdictions benchmark considerably faster. Canadian approvals in British Columbia and Ontario typically range from two to four years. Australian state-level processes vary but generally fall within two to five years. Chile's current profile places it toward the slower end of global comparisons, and the RED bill's permitting streamlining component is intended to close that gap through procedural reform and timeline mandates.

Projected Economic Outcomes: Reading the Production and Fiscal Modelling

Economic modelling associated with the RED bill produces projections that, if realised, would represent a structural shift in Chile's position within global critical mineral supply chains.

| Metric | Baseline Scenario | Reform Scenario | Incremental Gain |

|---|---|---|---|

| Copper Production by 2046 | 5.68 million tonnes | 6.65 million tonnes | ~0.97 Mt annually |

| Cumulative Copper Addition (20 years) | Baseline | Reform | 13.8 million tonnes |

| Cumulative Lithium Addition (20 years) | Baseline | Reform | 1.3 million tonnes |

| Peak Annual GDP Impact | Baseline | +~1.06% | ~1.06% uplift |

| Peak Annual Social Value Addition | Baseline | >US$12.1 billion | Above baseline |

| Cumulative Additional Fiscal Revenue | Baseline | Reform | US$15.3 billion |

The fiscal trajectory follows what economists describe as a V-shaped dynamic. In its earliest phase through 2026, the reform has negligible revenue impact. Between 2027 and 2030, as the tax rate reduction takes effect ahead of the production expansion it is designed to stimulate, there is a transitional period of reduced fiscal collections. The critical variable is whether the production expansion materialises on schedule.

The step-by-step fiscal logic works as follows:

- The corporate rate falls from 27% to 23%, reducing per-unit tax revenue on existing output

- Lower effective fiscal burden improves project internal rates of return, rendering previously marginal investments viable

- New projects advance through approvals and enter construction, expanding the production pipeline

- Expanded production volume at 23% generates greater absolute fiscal receipts than the contracted base would have at 27%

- The revenue crossover point is modelled to occur around 2031

- By 2046, cumulative net additional fiscal revenue reaches US$15.3 billion above the no-reform baseline

Analytical caution: These projections are model-dependent. They assume production growth materialises on the modelled timeline, commodity prices remain supportive through the investment cycle, and Senate passage does not materially dilute the reform's core provisions.

Global Benchmarking: Where Chile Stands After RED

| Jurisdiction | Corporate Tax Rate | Investment Stability Guarantee | Permitting Speed |

|---|---|---|---|

| Chile (Post-RED) | 23% (target) | 25-year invariability (>US$50M) | Reform in progress |

| Australia | ~30% (with state royalties) | No formal long-term guarantee | 2–5 years (state-variable) |

| Peru | 29.5% | No formal guarantee | 3–7 years |

| Canada (BC/Ontario) | ~26–27% | No formal guarantee | 2–4 years |

| Argentina (RIGI) | 25–35% | 30-year stability (qualifying projects) | Streamlined under RIGI |

| DRC | 30% | Limited | Highly variable |

The comparison with Argentina's RIGI regime is particularly relevant for investors assessing Latin American allocation decisions. Both frameworks share a philosophical architecture: long-duration legal certainty as the primary tool for attracting capital to large, long-gestation resource projects. The substantive difference lies in macroeconomic context. Chile's monetary and fiscal institutions are considerably more stable than Argentina's, meaning the invariability guarantee carries greater credibility as an enforceable legal commitment rather than a political aspiration. In addition, the Argentina lithium brine market presents a useful parallel, demonstrating how stability frameworks can redirect capital flows across competing jurisdictions.

Chile's structural differentiation advantage over Peru and Australia is the invariability regime itself. Neither jurisdiction offers a comparable long-term fiscal lock-in, meaning that investors allocating between these destinations must price ongoing sovereign risk into their Chilean peers' discount rates. The RED bill, if enacted in its current form, closes that pricing gap substantially.

The Lithium Dimension: Unresolved Tensions in a Critical Supply Chain

Chile holds the world's largest lithium reserves, concentrated in the Atacama salt flat, yet its share of global lithium supply has been losing ground to Argentina and Australia for several years. The underlying constraint is not geological but structural. The Chile lithium strategy has historically prioritised state-centric development through Codelco and SQM under framework agreements, creating an architecture that limits the pace at which private capital can be deployed.

The RED bill's invariability and corporate tax provisions apply to lithium development in principle, and the modelled 1.3 million tonne cumulative lithium addition over twenty years reflects an assumption that improved fiscal certainty will accelerate private-sector activity. What remains analytically unresolved is whether the state-ownership architecture represents a binding constraint that no fiscal reform can unlock on its own.

Lithium brine operations in the Atacama present unique technical characteristics that compound this policy challenge. Atacama brines are among the highest-grade lithium sources on the planet, with lithium concentrations that can reach 1,500–2,000 mg/L, compared to 200–400 mg/L in many other global brine deposits. The extraction process relies on solar evaporation in large pond systems, making water consumption a secondary concern relative to hard-rock operations but creating complex interactions with the fragile Atacama hydrological system. Environmental approvals for new or expanded brine operations therefore carry particularly high community and regulatory sensitivity, an obstacle that fiscal certainty alone does not resolve.

However, advances in direct lithium extraction technology may offer a path to accelerate Atacama output while reducing the environmental footprint of new operations, potentially easing some of the regulatory friction that has historically constrained development timelines.

If the invariability regime successfully de-risks private lithium development, Chile has a realistic window to recapture market share in battery-grade lithium supply chains. If Senate amendments dilute the regime's durability or scope, that opportunity may transfer to Argentina's emerging brine projects and Australian hard-rock producers within the current investment cycle.

Stakeholder Analysis: Who Gains, Who Pushes Back, and Why the Senate Is the Decisive Arena

Understanding the RED bill's passage probability requires mapping the stakeholder landscape across three dimensions.

Primary beneficiaries of the reform as currently drafted include:

- Large-scale foreign mining operators who gain both the 35% effective tax cap and 25-year invariability, directly reducing the sovereign risk premium in their project discount rates

- Approximately 150,000 domestic SMEs that benefit from the corporate tax reduction, representing more than 90% of all registered companies and over half of formal employment in Chile

- Copper and lithium project developers for whom permitting reform reduces pre-production holding costs

- The Chilean government itself, positioned to capture US$15.3 billion in incremental cumulative revenue if the production model proves accurate

Opposition arguments cluster around four themes:

- Distributional equity: critics contend the tax reduction disproportionately flows to large enterprises and their shareholders rather than workers or host communities

- Near-term revenue risk: the transitional fiscal gap between 2027 and 2030 creates budget pressure against elevated social spending expectations

- Production model uncertainty: the US$15.3 billion figure depends on production assumptions that commodity price softness or sustained environmental opposition could undermine

- Royalty omission: leaving royalties unchanged is characterised by some critics as prioritising investor interests at the expense of state participation in resource rents

The Senate dynamic is where these tensions converge into political risk. The Kast government does not hold a Senate majority, requiring negotiation with centrist and regional parties whose priorities vary from royalty adjustments to regional revenue-sharing provisions. Amendment scenarios that could reduce the invariability period below 25 years, raise the effective tax floor, or reintroduce royalty reform language would each erode the investment signal that the bill is designed to transmit. Notably, backing beyond the ruling coalition has already emerged for certain provisions, which may improve the bill's Senate prospects.

The next major ASX story will hit our subscribers first

Water Scarcity: The Structural Constraint That Fiscal Reform Cannot Address

One factor that receives insufficient attention in investment discussions about the Kast mining tax plan in Chile is the binding physical constraint of water availability in northern Chile's mining regions. The Atacama and surrounding areas are among the driest environments on Earth, and copper operations there depend on either freshwater extraction from aquifers that are under increasing stress, or on desalination infrastructure that adds significant capital and operating costs.

Several major copper expansion projects have faced permitting delays not because of fiscal uncertainty but because of contested water rights and aquifer impact assessments. The RED bill's permitting reform provisions address procedural speed but cannot alter the underlying hydrological realities that generate community opposition and regulatory scrutiny. Consequently, even in a fully enacted RED bill scenario, some projects in the modelled production uplift could face delays or cost escalations that compress the projected returns.

Assessing the Reform's Sufficiency: Strengths, Gaps, and the Path Forward

The RED bill represents a genuine structural improvement over Chile's recent fiscal trajectory. Its three core strengths are clear:

- The 25-year invariability regime is the most significant legal certainty mechanism in Chilean mining law since the 1970s, and it directly addresses the discount rate problem that has historically penalised Chilean project valuations

- The phased tax reduction is fiscally defensible, avoiding the budgetary shock of an immediate rate cut while delivering a credible long-term commitment

- Permitting reform, if implemented rather than merely legislated, targets the most operationally significant source of pre-production cost inflation in Chile's project pipeline

The gaps are equally identifiable:

- Royalties remain unaddressed, leaving the combined fiscal burden potentially above the threshold that some investors use to compare Chile against competing jurisdictions

- Senate amendment risk is material; a diluted invariability period or reintroduced royalty provisions could hollow out the bill's investor signal before it reaches implementation

- Environmental conflict and water scarcity represent structural frictions that no fiscal architecture can neutralise

- Permitting reform's effectiveness depends entirely on implementation fidelity, not legislative intent

Chile's competitive position in global critical mineral supply chains will ultimately be determined not by the text of the RED bill but by the quality of its execution, the durability of its legal guarantees across future political cycles, and the speed at which Chile's project developers can convert fiscal certainty into physical production. The Kast mining tax plan in Chile is necessary. Whether it is sufficient will take years to answer definitively.

This article is intended for informational purposes only and does not constitute financial, investment, or legal advice. Projections and modelling figures cited reflect analytical estimates and are subject to change based on legislative outcomes, commodity price movements, and operational variables. Readers should conduct independent due diligence before making investment decisions.

Want to Stay Ahead of ASX Mineral Discoveries Tied to the Critical Minerals Boom?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including copper and lithium plays positioned to benefit from shifting global supply chains — transforming complex market data into actionable investment insights for both new and experienced investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and start your 14-day free trial today to secure your market-leading advantage.