June 18, 2026

The Architecture of Upstream Access: Why Frontier Licensing Rounds Reveal More Than Just Acreage

Every few years, a sovereign hydrocarbon licensing round captures the attention of upstream operators, independent explorers, and institutional capital alike. Not because of the acreage on offer, but because of what the fiscal terms, block structure, and bidder mix reveal about the host government's long-term supply calculus. When entry bonuses are set deliberately low, when production terms stretch to 25 years, and when the resource estimate exceeds 9 billion barrels of oil equivalent across 30 exploration tracts, the message is unambiguous: the state wants exploration activity broadened, not just deepened.

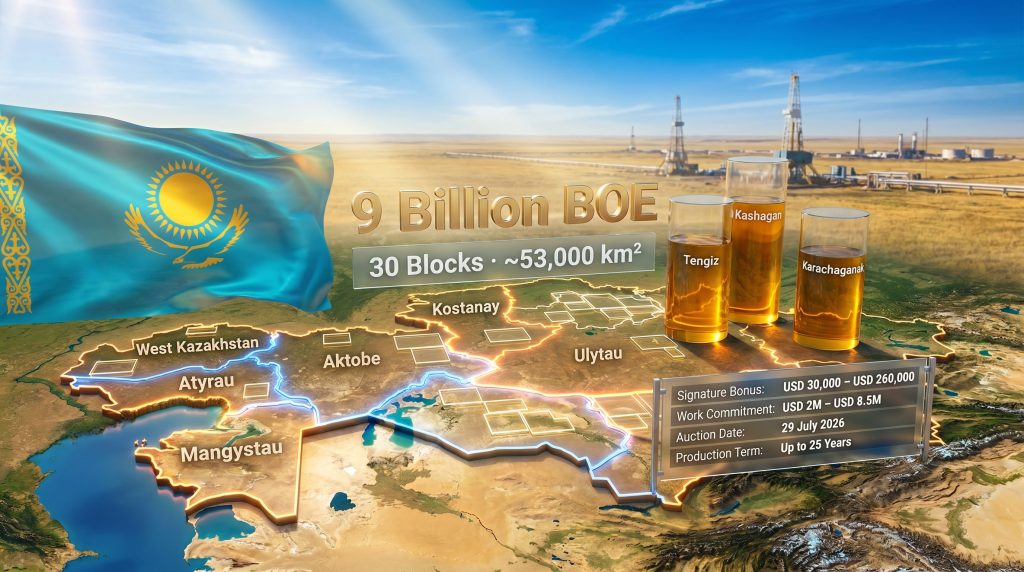

Kazakhstan's 12th Kazakhstan hydrocarbon licensing round is precisely that kind of signal. Spanning approximately 53,000 square kilometres across six distinct regions, it represents the country's most ambitious competitive exploration offering in years and carries implications well beyond the blocks themselves. Furthermore, understanding this round in context requires looking at the broader geopolitical risk landscape shaping resource competition globally.

When big ASX news breaks, our subscribers know first

What the 12th Round Actually Represents: Scope, Scale, and Sovereign Intent

Kazakhstan's Ministry of Energy has structured the 12th round as a dual-track exploration strategy, combining a competitive electronic auction with ongoing bilateral partnership agreements coordinated through state entities KazMunayGas and QazaqGaz. The auction itself is scheduled for 29 July 2026, with the application deadline falling on 30 June 2026.

The 30 subsoil plots span six regions: Aktobe, West Kazakhstan, Atyrau, Mangystau, Ulytau, and Kostanay. The combined preliminary resource estimate exceeds 9 billion barrels of oil equivalent, though it bears emphasising that this figure is based on early-stage geological assessments and remains subject to material revision as exploration data matures. Investors and operators should treat this number as directional rather than definitive.

Key Fiscal Parameters at a Glance

| Parameter | Detail |

|---|---|

| Blocks offered | 30 subsoil plots |

| Total acreage | ~53,000 km² |

| Estimated resource potential | >9 billion BOE (preliminary) |

| Signature bonus (minimum) | USD 30,000 |

| Signature bonus (maximum) | ~USD 260,000 (Tyubedzhik) |

| Work commitment (typical range) | USD 2–3 million per block |

| Highest work commitment | USD 8.5 million (Ustyurt-4) |

| Exploration term | Up to 6 years |

| Production term | Up to 25 years |

| Auction date | 29 July 2026 (electronic) |

| Application deadline | 30 June 2026 |

The signature bonus floor of USD 30,000 is deliberately modest. This is not an oversight in fiscal design; it is an intentional positioning that makes the round accessible to mid-tier independents and smaller exploration companies, not just integrated supermajors. Compare this to licensing rounds in West Africa or the North Sea where entry premiums can reach tens of millions of dollars before a single well is drilled, and the contrast becomes strategically meaningful. In addition, the global impact of exploration licences on capital allocation patterns offers a useful parallel for understanding how such design choices reshape investment flows.

A Basin-by-Basin Breakdown: Four Geological Fairways, Four Risk Profiles

Understanding the 12th round requires moving beyond acreage statistics into the geological architecture of Kazakhstan's exploration landscape. The 30 blocks span four primary exploration fairways, each carrying a distinct risk-reward relationship.

Precaspian Basin: Infrastructure Proximity as a Commercial Differentiator

Blocks affiliated with the Precaspian Basin sit closest to Kazakhstan's existing hydrocarbon infrastructure, including the Caspian Pipeline Consortium route and the broader KazTransOil system. For operators focused on capital efficiency, proximity to offtake infrastructure fundamentally reduces the total cost of getting barrels to market. This makes Precaspian blocks the most commercially de-risked tracts in the 12th round, even where sub-surface uncertainty remains.

North Ustyurt Platform: Basin-Scale Thinking Returns

The North Ustyurt platform represents a different proposition entirely. This is frontier-scale exploration territory where deeper structural concepts have attracted renewed attention from major international operators. BP's active engagement on both the Kazakhstani and Uzbek sides of the North Ustyurt Basin is a particularly telling indicator.

When a supermajor begins reassessing a basin across national borders simultaneously, it typically signals a thesis-level geological reappraisal rather than opportunistic block-picking. The Ustyurt-4 block, which carries the highest minimum work commitment in the 12th round at USD 8.5 million, reflects the capital intensity of this frontier environment.

South Torgay Province: A Proven Fairway With Established Operator Precedent

The South Torgay Basin hosts the Kumkol-Akshabulak trend, one of Kazakhstan's most established oil-producing corridors. CNPC's presence in this province through PetroKazakhstan provides both geological validation and a benchmark for development economics. Blocks in this region carry lower exploration risk relative to frontier plays but correspondingly narrower upside. For risk-averse operators or those seeking to build production-ready positions, South Torgay is the logical entry point.

Mangyshlak Peninsula: A Focused Opportunity Around a Discovered Asset

The Mangyshlak Peninsula offers a concentrated opportunity set anchored by the Tyubedzhik discovery, which sits adjacent to the established Dunga production trend on the Tyub-Karagan Peninsula. Tyubedzhik is notable as the only block in the 12th round carrying discovered reserves rather than purely prospective resources.

This distinction drives the higher entry premium of approximately USD 260,000 in signature bonus, reflecting reduced geological risk but increased entry cost relative to the round's other tracts.

Geological Note: Discovered reserves and prospective resources are fundamentally different categories under petroleum resource classification frameworks. A block with discovered reserves has already confirmed the presence of hydrocarbons through drilling; remaining uncertainty relates primarily to commerciality and recovery factor rather than the existence of the resource itself.

How Work Program Staging Manages Exploration Capital Exposure

One of the less-discussed but commercially significant features of Kazakhstan's 12th round is the phased structure of the mandatory work programs. Rather than requiring immediate drilling commitments, the framework allows operators to de-risk their positions progressively before committing to the highest-cost activities.

A typical work program proceeds as follows:

- Legacy seismic reprocessing — Operators apply modern processing algorithms to existing 2D and 3D seismic datasets, often revealing structural detail invisible to earlier vintage interpretation technology.

- New 2D seismic acquisition — Where legacy data is insufficient or absent, new regional 2D lines are acquired to map basin geometry and identify leads.

- 3D seismic acquisition — Required for blocks where prospect-level resolution is needed before drilling commitment; higher cost but substantially reduces well location uncertainty.

- Exploration well drilling — The minimum commitment of at least one exploration well, representing the highest capital event in the sequence and the point at which sub-surface uncertainty is resolved.

This staging architecture allows operators to calibrate their capital exposure at each decision gate and exit the program with defined minimum obligations if the geological picture deteriorates. It also explains why minimum work commitments in the USD 2–3 million range for most blocks do not represent the full cost of exploration, but rather the floor of contractually binding spend.

International Operator Landscape: Who Is Already in Kazakhstan's Upstream

The bilateral partnership track running alongside the 12th round provides important context for understanding which international operators have already secured their Kazakhstani upstream positions outside the competitive auction process.

| Operator | Partnership Channel | Notable Activity |

|---|---|---|

| BP | Bilateral (KMG/QazaqGaz) | Active on North Ustyurt (Kazakh and Uzbek sides) |

| Shell | Bilateral agreement | Zhanaturmys block signed March 2026 |

| Chevron | Bilateral | Established upstream presence |

| Eni | Bilateral | Ongoing exploration cooperation |

| Sinopec | Bilateral | State-to-state cooperation framework |

| CNOOC | Bilateral | Active partnership discussions |

| CNPC / PetroKazakhstan | Established presence | South Torgay via PetroKazakhstan |

Shell's agreement for the Zhanaturmys block, concluded in March 2026, is particularly significant as a leading indicator of renewed Western appetite for Kazakhstani acreage. Shell's return to active exploration engagement, following years of portfolio rationalisation across Central Asia, points to a recalibration of risk tolerance that other Western majors may follow.

The dual-track system itself deserves analytical attention. By offering both competitive auction blocks and bilateral partnership routes simultaneously, Kazakhstan effectively segments the market: companies with established relationships and technical credibility can negotiate directly with state entities, while newer entrants access the market through the transparent auction mechanism. This architecture maximises competition for blocks while preserving the state's ability to select strategically preferred partners for higher-complexity opportunities. Consequently, this approach bears comparison with exploration licences in Saudi Arabia, where similarly structured dual-track frameworks have emerged as a competitive norm.

The Production Concentration Problem: Why Exploration Expansion Is a Sovereign Imperative

Kazakhstan currently produces approximately 2.15 million barrels per day of crude oil and condensate, and the vast majority of that output originates from three legacy giant fields: Tengiz, Kashagan, and Karachaganak. This concentration creates a structural vulnerability that the 12th round is designed, at least in part, to address.

Giant fields are not permanent. They follow long-cycle decline curves, and the capital required to maintain plateau production in ageing supergiant assets is both enormous and intensifying. Tengiz's expansion through the Future Growth Project adds near-term capacity, but the medium-term reality is that Kazakhstan's export volumes depend critically on fields that were discovered decades ago and are already well into their production lives.

Strategic Context: An upstream portfolio concentrated in three fields, regardless of their scale, carries a systemic risk that broadened exploration cannot fully eliminate but can meaningfully mitigate. The 12th round is best understood as Kazakhstan's attempt to build an exploration pipeline capable of sustaining production diversity into the 2030s and beyond.

Export infrastructure dependency compounds this challenge. The bulk of Kazakhstani crude flows through the Caspian Pipeline Consortium system, creating a single-corridor vulnerability that has proven commercially disruptive on multiple prior occasions. Monitoring crude oil price trends remains essential for operators evaluating whether current economics justify the capital commitments these blocks require.

The next major ASX story will hit our subscribers first

Geopolitical and Regulatory Risk Factors: What Prospective Bidders Must Evaluate

No analysis of Kazakhstan's upstream opportunity is complete without a clear-eyed assessment of the risk environment. The Kashagan project's ongoing arbitration disputes between Kazakhstan and international operators represent a material uncertainty that new entrants cannot ignore. Furthermore, the market implications of trade wars on commodity pricing and upstream investment appetite add another layer of complexity to long-cycle capital decisions in this region.

Key risk factors for prospective bidders in the 12th round include:

- Arbitration environment: Active contractual disputes involving major Kashagan project participants create a baseline of regulatory uncertainty that affects investor confidence across Kazakhstan's upstream sector broadly.

- Export route concentration: Dependence on the CPC pipeline as the primary export corridor introduces single-point-of-failure risk for production economics and revenue timing.

- Preliminary resource estimates: The 9 billion BOE figure represents early-stage geological assessment. Operators should expect material variance between preliminary estimates and commercially recoverable volumes once exploration drilling has been completed.

- Work commitment enforceability: Minimum spend obligations under Kazakhstan's subsoil use legislation are legally binding. Non-performance carries contractual consequences that operators must factor into exploration budgeting.

- Sovereign policy evolution: As with all Central Asian jurisdictions, changes to fiscal terms, environmental requirements, or local content regulations during a licence's life represent a background risk that long-cycle capital allocation must accommodate.

According to reporting on Kazakhstan's licensing round, the 9 billion BOE headline figure has attracted significant international attention, though industry analysts consistently caution that the gap between geological potential and commercially recoverable volumes in frontier basins can be substantial.

How to Participate: A Step-by-Step Guide to the 12th Round Process

For operators evaluating participation, the process follows a defined sequence:

- Obtain the official block catalogue from Kazakhstan's Ministry of Energy, covering technical documentation for all 30 subsoil plots across the six target regions.

- Complete geological pre-screening, assessing basin affiliation, existing seismic coverage density, proximity to infrastructure, and analogue field performance within each fairway of interest.

- Model work commitment economics, mapping minimum spend obligations against exploration budgets, risked resource estimates, and corporate risk tolerance parameters.

- Prepare application documentation, including technical qualification evidence, financial capacity demonstration, and a proposed work program structured to Ministry requirements.

- Submit applications by 30 June 2026, the binding deadline ahead of the electronic auction.

- Participate in the electronic auction on 29 July 2026, where competitive bidding determines block allocation in cases of multiple qualified applicants.

- Execute the subsoil use agreement, formalising exploration rights and initiating the staged work program under Kazakhstani subsoil legislation.

Kazakhstan's Upstream Positioning in the Central Asian Competitive Context

Viewed against the broader Central Asian upstream competitive landscape, Kazakhstan occupies a structurally advantaged position. Its regulatory framework is more developed than several neighbouring jurisdictions, its infrastructure base is materially superior to frontier Central Asian markets, and its track record of attracting and retaining major international operator investment provides a degree of sovereign credibility that newer licensing environments cannot yet match.

For a detailed overview of how Kazakhstan's subsoil regulatory framework governs operator obligations and contractual protections, prospective bidders should review the applicable legal and regulatory documentation before submitting applications.

The 12th Kazakhstan hydrocarbon licensing round reflects a country that understands the competitive dynamics of attracting exploration capital in an era of compressed upstream investment budgets. Low entry thresholds, staged work commitments, and a transparent electronic auction process are deliberate design choices aimed at broadening participation beyond the established supermajor tier.

Whether the round achieves its exploratory objectives will ultimately depend on what the drill bit finds. However, the architecture of the round itself, from the USD 30,000 bonus floor to the 25-year production term, signals a government that is thinking carefully about how to sustain hydrocarbon revenues well into the next decade.

Disclaimer: This article contains forward-looking statements and preliminary resource estimates that are subject to material revision. The 9 billion BOE resource potential referenced represents early-stage geological assessment only and should not be construed as commercially recoverable reserves. Nothing in this article constitutes investment advice. Readers should conduct independent due diligence before making any investment or commercial decisions related to Kazakhstan's upstream sector.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

While Kazakhstan's licensing round illustrates how sovereign resource strategy shapes global capital flows, Discovery Alert's proprietary Discovery IQ model brings that same intelligence closer to home — delivering real-time alerts on significant ASX mineral discoveries the moment they are announced, turning complex geological data into actionable investment insights. Explore historic discoveries and their remarkable returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.