June 18, 2026

Legal Framework for Contract Suspension in Commodity Trading

Global commodity markets operate through complex contractual frameworks designed to protect parties when extraordinary circumstances prevent normal performance. The legal architecture governing these arrangements centers on force majeure clauses, which provide contractual relief when events beyond reasonable control make fulfillment impossible or commercially impractical.

Force majeure provisions in international energy trading require specific documentation standards to validate claims. Companies must demonstrate three critical elements: occurrence of an unforeseeable event, direct causal relationship between the disruption and contract non-performance, and absence of reasonable mitigation alternatives. This legal framework becomes particularly crucial during geopolitical crises affecting global supply chains, where force majeure on gasoline exports can have widespread ramifications.

Economic Triggers That Activate Force Majeure Protections

Economic disruptions of sufficient magnitude can trigger force majeure protections when they fundamentally alter market conditions beyond normal volatility ranges. Recent events in the Strait of Hormuz demonstrate how military escalation creates economic triggers that justify contractual suspension, with shipping traffic experiencing near-complete cessation following regional conflicts.

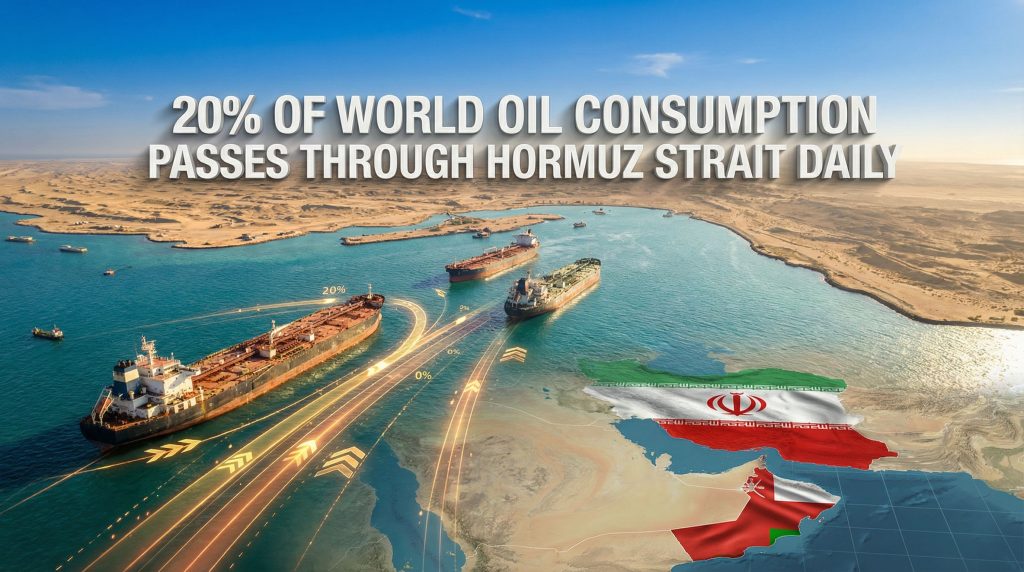

The threshold for economic force majeure typically involves supply chain disruptions exceeding historical volatility patterns, input cost increases making contract performance economically unfeasible, or inability to source replacement materials at commercially reasonable rates. Furthermore, when approximately 20% of global oil consumption normally transits through a single chokepoint, complete closure represents an economic shock exceeding standard contractual risk assumptions.

Geopolitical Risk Assessment in Energy Supply Chains

Energy supply chains face concentrated geopolitical exposure when sourcing patterns create dependency on politically volatile regions. Indian refineries demonstrate this vulnerability through their approximately 40% reliance on Middle Eastern crude sources, creating systematic risk when regional conflicts disrupt normal trade flows.

Effective geopolitical risk assessment requires monitoring regional conflict escalation indicators, maritime chokepoint security status, sanctions compliance implications, and alternative sourcing availability with associated cost premiums. However, companies implementing proactive risk management strategies often explore alternative supply sources months before disruptions occur, though implementation timelines may not match crisis development speed.

When big ASX news breaks, our subscribers know first

How Do Middle East Conflicts Impact Global Gasoline Trade Flows?

Strait of Hormuz Chokepoint Analysis

The Strait of Hormuz represents one of the world's most critical energy chokepoints, facilitating transit for approximately one-fifth of global oil consumption. This narrow maritime passage between Iran and Oman creates a strategic vulnerability where military action can instantaneously disrupt international energy flows.

Global Oil Transit Through Critical Maritime Passages

| Chokepoint | Daily Transit Volume | Share of Global Oil Trade | Strategic Vulnerability |

|---|---|---|---|

| Strait of Hormuz | ~21 million barrels | 20% | Iran-Oman control |

| Strait of Malacca | ~16 million barrels | 15% | Multi-nation transit |

| Suez Canal | ~5 million barrels | 5% | Egypt control |

| Bab el-Mandab | ~4.8 million barrels | 5% | Yemen-Djibouti corridor |

Critical Infrastructure Alert: Twenty percent of world oil consumption depends on unimpeded Strait of Hormuz navigation, making this chokepoint a global economic pressure point during Middle Eastern conflicts.

Recent military escalations have demonstrated the chokepoint's vulnerability, with shipping operations experiencing virtual cessation following Iranian military actions and retaliatory strikes. Consequently, this operational halt removes substantial daily crude and refined product flows from global markets, creating immediate supply gaps that ripple through international trading networks.

Regional Refinery Exposure to Supply Disruptions

Regional refineries with high export dependency face acute vulnerability during supply disruptions, particularly when their crude sourcing concentrates in geopolitically unstable regions. State-run facilities operating at significant scale amplify this exposure through their substantial daily processing volumes and export commitments.

Refinery Exposure Metrics During Supply Disruptions

- Production capacity: 500,000 barrels-per-day facilities represent major regional processing centers

- Export dependency ratios: Facilities exporting 40% of output face substantial contractual exposure

- Gasoline production volumes: Typical refineries allocate 25-30% of output to gasoline, representing 50,000-60,000 barrels daily at large facilities

- Contract settlement obligations: Export-dependent refineries carry penalty clauses for non-delivery

- Inventory buffer limitations: Most refineries maintain 15-30 day product inventories under normal operations

The financial impact multiplies when considering that a major refinery suspending force majeure on gasoline exports removes significant daily volume from international markets. For instance, a 500,000 barrel-per-day facility with 40% export dependency represents approximately 50,000-60,000 barrels of daily gasoline unavailable for contract fulfillment.

Alternative Sourcing Strategies During Crisis Periods

Alternative sourcing strategies require months-long development timelines, making crisis-period implementation challenging for companies lacking advance preparation. Strategic diversification planning often begins months before disruptions materialise, though actual sourcing transitions may not achieve operational status when emergency conditions arise.

Alternative Sourcing Timeline Components:

- Regulatory compliance verification (2-4 weeks)

- Supply contract negotiation (4-8 weeks)

- Logistics route establishment (2-6 weeks)

- Quality specifications matching (1-3 weeks)

- Price benchmarking and hedging (1-2 weeks)

- First cargo delivery (2-4 weeks from contract)

Government-level coordination enhances individual company efforts, with national energy security strategies encompassing crude oil, liquefied petroleum gas, and liquefied natural gas sourcing diversification. However, exploration of alternative sources does not guarantee immediate availability during crisis periods, as demonstrated by refiners declaring force majeure on gasoline exports despite ongoing diversification efforts.

What Are the Financial Implications of Export Contract Suspensions?

Market Price Volatility During Force Majeure Events

Force majeure declarations create cascading price pressures through multiple market mechanisms, amplifying volatility beyond normal supply-demand dynamics. Direct supply loss from major refineries combines with broader chokepoint closures to create compound supply shocks that fundamentally alter pricing expectations.

Price Volatility Mechanisms During Force Majeure:

- Immediate spot market supply reduction from suspended export volumes

- Hedging instrument repricing as risk models adjust to new supply realities

- Inventory draw expectations as downstream consumers deplete stocks

- Geopolitical risk premium application to remaining available supplies

- Logistics cost increases for alternative routing and emergency procurement

- Contango curve steepening as longer-term contracts price in extended disruptions

When a major refinery suspends 50,000+ barrels of daily gasoline exports simultaneously with broader Hormuz closure affecting 20% of global oil transit, markets experience dual-layer supply shock that compounds price volatility. Duration specifications extending across multiple months create sustained price support floors as market participants adjust inventory and hedging strategies.

Insurance Coverage for Political Risk in Energy Trading

Political risk insurance mechanisms in energy trading face complex coverage gaps during military conflicts, particularly when force majeure clauses provide contractual relief that may supersede insurance obligations. The intersection of war risk exclusions and political violence coverage creates ambiguous protection zones for energy exporters.

Political Risk Insurance Coverage Areas:

- War and civil unrest exclusions requiring separate specialised endorsements

- Expropriation and nationalisation risks for state-controlled resources

- Currency inconvertibility preventing payment completion

- Breach of contract by government entities affecting state-run refineries

- Sovereign financial obligation defaults impacting payment guarantees

- Chokepoint disruption coverage available through specialised providers

Insurance premium costs for energy contracts involving Middle East-dependent trade typically incorporate baseline political risk assumptions. Nevertheless, coverage may not extend to extraordinary military conflicts causing complete chokepoint closure. Companies often maintain self-insurance reserves alongside third-party coverage to address coverage gaps during extreme events.

Counterparty Risk Management in Volatile Regions

Counterparty risk management becomes critical when information asymmetries emerge during crisis periods, creating uncertainty about contract performance and financial stability. Furthermore, tariff impacts on markets add additional complexity to trader-refinery relationships that face stress when force majeure declarations require immediate contract restructuring without advance notification.

Recent events demonstrate how counterparty risk materialises through delayed communication channels, indirect confirmation sources, and limited transparency regarding operational status. When refineries invoke force majeure on gasoline exports through trader notifications rather than public announcements, counterparties face information disadvantages affecting risk assessment and hedging decisions.

Counterparty Risk Indicators:

- Communication delays between contract parties during crisis periods

- Indirect confirmation requirements when companies avoid direct public statements

- Information asymmetry regarding operational status and future performance capacity

- Credit exposure amplification as contract suspensions concentrate risk among remaining suppliers

India's Energy Security Strategy Amid Global Disruptions

Strategic Petroleum Reserve Capacity Analysis

India maintains strategic petroleum reserves designed to provide approximately 25 days of crude oil consumption during supply disruptions, representing a modest buffer compared to International Energy Agency recommendations of 90-day reserves for developed economies. This inventory capacity becomes critical during chokepoint closures affecting multiple supply routes simultaneously.

India's Energy Security Inventory Analysis

| Resource Type | Current Inventory | Duration Coverage | Strategic Adequacy |

|---|---|---|---|

| Crude Oil | Government reserves | 25 days | Below IEA standards |

| Gasoline | Refiner stockpiles | 25 days | Moderate coverage |

| Gasoil/Diesel | Combined reserves | 25 days | Industrial vulnerability |

| LPG | Distributed storage | 25 days | Household supply risk |

The 25-day inventory standard applies across refined products including gasoline, gasoil, and liquefied petroleum gas, creating synchronised depletion timelines if supply disruptions extend beyond one month. This relatively short coverage period necessitates rapid alternative sourcing arrangements during extended Middle Eastern conflicts.

Diversification Away from Middle Eastern Crude Sources

India's crude sourcing strategy demonstrates significant concentration risk, with approximately 40% of requirements fulfilled through Middle Eastern purchases beyond spot market transactions and domestic production. This dependency creates systematic vulnerability when regional conflicts disrupt normal trading relationships.

Government-level sourcing diversification encompasses crude oil, liquefied petroleum gas, and liquefied natural gas procurement from alternative geographic regions. However, diversification planning requires substantial lead times for contract negotiation, logistics establishment, and infrastructure adaptation to process different crude specifications. In addition, factors such as US policy on Venezuelan crude influence available alternatives.

Alternative Sourcing Considerations:

- Venezuelan crude exploration offering sanctions-compliant alternatives to Russian supplies

- African crude varieties providing different geographic risk profiles

- North American supplies though transportation costs may limit economic viability

- Southeast Asian refiners for refined product imports rather than crude processing

Impact on Domestic Fuel Pricing and Supply Chains

Domestic fuel pricing mechanisms face pressure when export-oriented refineries redirect production to local markets during international supply disruptions. This reallocation can temporarily increase domestic availability while reducing foreign exchange earnings from export sales, particularly given broader energy export challenges affecting regional economies.

State-run refineries operating dual domestic-export business models must balance contractual obligations with national energy security priorities during crisis periods. When force majeure suspends export commitments, these facilities can theoretically redirect output to domestic distribution networks, though infrastructure and logistics constraints may limit immediate reallocation effectiveness.

How Do Refineries Navigate Export Obligations During Crises?

Operational Flexibility in Product Allocation

Refinery operational flexibility becomes crucial when external disruptions require rapid product allocation adjustments between domestic and export markets. Facilities designed for high export ratios face complex optimisation decisions when international contracts become unfulfillable while domestic demand continues.

Case Study: Export-Dependent Refinery Operations

A state-run refinery processing 500,000 barrels per day with 40% export dependency must reallocate 200,000 barrels of daily production when export contracts face force majeure suspension. This reallocation affects:

- Product mix optimisation to match domestic demand patterns rather than export specifications

- Storage capacity utilisation as domestic distribution networks may not absorb full export volumes immediately

- Pricing dynamics when excess supply enters domestic markets during international disruptions

- Foreign exchange impact from reduced export revenue affecting company and national finances

Contract Renegotiation Strategies Post-Force Majeure

Contract renegotiation following force majeure events requires careful balance between maintaining long-term trading relationships and addressing changed market conditions. Refineries must demonstrate good faith efforts to resume normal performance whilst protecting against future disruption exposure.

Renegotiation Framework Components:

- Performance timeline revision accounting for ongoing geopolitical uncertainty

- Price adjustment mechanisms reflecting changed supply-demand dynamics

- Alternative delivery options using different shipping routes or product specifications

- Risk sharing arrangements allocating future disruption costs between parties

- Termination clause modifications providing enhanced flexibility for extraordinary circumstances

Legal Documentation Requirements for Valid Claims

Valid force majeure claims require comprehensive documentation demonstrating the causal relationship between external events and contract performance impossibility. Refineries must establish clear evidentiary chains linking geopolitical disruptions to specific operational constraints, particularly given ongoing US tariffs and inflation affecting global trade costs.

Documentation Requirements:

- Event timeline correlation between military actions and operational impacts

- Supply chain mapping showing dependence on disrupted routes or sources

- Mitigation effort evidence demonstrating attempts to maintain performance through alternative means

- Financial impact quantification of additional costs or lost opportunities

- Expert analysis supporting claims of performance impossibility rather than economic inconvenience

Regional Energy Market Restructuring in South Asia

Alternative Crude Oil Sourcing Partnerships

South Asian energy markets are experiencing fundamental restructuring as traditional Middle Eastern supply relationships face chronic instability. This restructuring requires development of new trading partnerships, logistics infrastructure, and financial arrangements to support diversified sourcing strategies.

Crude Oil Alternative Assessment

| Source Region | Price Competitiveness | Political Stability | Transportation Costs | Implementation Timeline |

|---|---|---|---|---|

| Venezuela | Moderate (sanctions impact) | Developing | High (distance) | 6-12 months |

| Russia | Variable (sanctions) | Moderate | Moderate | 3-6 months |

| Africa (West) | Competitive | Varies by country | Moderate | 4-8 months |

| North America | Premium pricing | High | High | 8-12 months |

Venezuelan crude exploration represents a strategic pivot away from sanctioned Russian supplies whilst maintaining cost competitiveness. However, implementation timelines extend across multiple quarters, requiring careful coordination between exploration announcements and operational capability development.

LNG and LPG Import Diversification Strategies

Liquefied natural gas and liquefied petroleum gas import diversification addresses both crude oil dependency and downstream product supply security. These markets offer different supplier options and transportation flexibility compared to crude oil pipelines and traditional tanker routes.

LNG/LPG Diversification Advantages:

- Multiple global suppliers reducing geographic concentration risk

- Flexible shipping arrangements allowing route optimisation during disruptions

- Shorter contract cycles enabling more rapid supplier transitions

- Storage infrastructure providing enhanced inventory management options

- Pricing transparency through established spot and futures markets

Infrastructure Development for Energy Independence

Regional infrastructure development focuses on enhancing energy independence through expanded storage capacity, alternative transportation routes, and domestic production capabilities. These investments require substantial capital commitments with multi-year payback periods, influenced by broader trends including Saudi exploration licenses affecting regional supply dynamics.

Strategic infrastructure priorities include expanded petroleum reserve capacity beyond current 25-day coverage, enhanced port facilities for alternative crude grades, and distribution network modifications supporting diversified product sourcing. However, infrastructure development timelines often exceed crisis duration, requiring sustained commitment regardless of immediate disruption resolution.

The next major ASX story will hit our subscribers first

What Can Energy Traders Learn from Recent Force Majeure Cases?

Contract Clause Optimisation for Future Disruptions

Recent force majeure events demonstrate the importance of precise contract language defining triggering events, notification requirements, and mitigation obligations. Traders must balance protection against extraordinary circumstances with maintaining commercial viability under normal market conditions.

Optimised Clause Elements:

- Specific event definitions beyond generic "acts of war" to include chokepoint closures and supply route disruptions

- Graduated response mechanisms allowing partial performance during limited disruptions rather than complete suspension

- Alternative performance options specifying substitute delivery methods, routes, or product specifications

- Cost allocation frameworks determining responsibility for additional expenses during alternative arrangements

- Duration limitations preventing indefinite contract suspension during extended geopolitical instability

Risk Assessment Methodologies for Export-Dependent Operations

Export-dependent refineries require enhanced risk assessment methodologies incorporating geopolitical analysis, chokepoint vulnerability evaluation, and alternative sourcing capability assessment. These frameworks must provide early warning indicators before disruptions materialise.

Risk Assessment Framework Components:

- Geopolitical monitoring systems tracking regional tension indicators and military escalation patterns

- Supply route vulnerability mapping identifying single points of failure in transportation networks

- Alternative sourcing feasibility analysis evaluating backup supplier capacity and implementation timelines

- Financial exposure quantification calculating potential revenue loss and penalty costs during disruptions

- Scenario planning exercises testing operational responses across different disruption severities and durations

Early Warning Systems for Geopolitical Supply Threats

Early warning systems for geopolitical supply threats must integrate political intelligence, military activity monitoring, and commercial shipping data to provide actionable insights before disruptions impact operations. These systems require coordination between government intelligence sources and private sector risk assessment capabilities.

Effective warning systems monitor escalating military rhetoric, unusual naval deployments, changes in shipping insurance rates, and commodity market sentiment indicators. However, the rapid escalation from normal operations to complete chokepoint closure demonstrates the limitations of early warning when military actions develop faster than commercial response capabilities.

Long-term Implications for Global Energy Trade Architecture

Shift Toward Regional Energy Partnerships

Global energy trade architecture is evolving toward enhanced regional partnerships as traditional long-distance supply chains face increased disruption risks. This shift requires development of new trading relationships, financial mechanisms, and infrastructure investments supporting regional energy security.

Regional partnerships offer advantages including reduced transportation distances, enhanced supply security through geographic diversification, and improved political alignment between trading partners. Nevertheless, regional arrangements may sacrifice cost optimisation achieved through global supply chain efficiency.

Technology Solutions for Supply Chain Resilience

Technology solutions for supply chain resilience encompass real-time tracking systems, predictive analytics for disruption forecasting, and automated contract management platforms enabling rapid response during crisis periods. These technologies require substantial investment with uncertain return profiles during normal market conditions.

Emerging Technology Applications:

- Blockchain-based contract management enabling automated force majeure processing and alternative arrangement implementation

- Satellite monitoring systems providing real-time shipping route status and alternative path optimisation

- Artificial intelligence risk assessment integrating multiple data sources for enhanced disruption prediction accuracy

- Digital twin modelling allowing scenario testing of supply chain modifications before implementation

Policy Frameworks for Energy Security Enhancement

Policy frameworks for energy security enhancement must balance market efficiency with supply reliability, requiring coordination between government strategic planning and private sector operational flexibility. These frameworks increasingly emphasise domestic reserve capacity, alternative sourcing relationships, and emergency response coordination.

Effective policy frameworks establish minimum inventory requirements, provide incentives for supply diversification investments, and create coordination mechanisms between government agencies and private sector energy companies during crisis periods. However, policy implementation requires sustained political commitment extending beyond immediate disruption resolution, as recent examples of Indian refiners declaring force majeure demonstrate the ongoing challenges faced by energy security planners.

Disclaimer: This analysis is based on publicly reported events and market observations. Energy market dynamics involve significant risks, and past performance does not guarantee future results. Readers should consult qualified professionals before making investment or operational decisions based on this information.

Ready to Capitalise on Energy Market Disruptions Before They Impact Prices?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including energy and commodity sectors experiencing supply chain disruptions. Subscribers gain actionable insights into companies positioned to benefit from global energy market volatility, ensuring investment decisions ahead of broader market recognition of emerging opportunities.