June 10, 2026

The Battery Metals Scramble Reshaping African Mining's Power Dynamics

The global push toward electrification has fundamentally altered the calculus of mining investment. Copper and cobalt, once peripheral to mainstream commodity portfolios, now sit at the centre of industrial strategy for nations and corporations alike. The Democratic Republic of Congo, which accounts for more than 70% of global cobalt output and ranks among the world's most prolific copper-producing nations, has become the defining battleground in this contest. Within that context, the story of how Lloyds expands role at DRC's Chemaf is not simply a corporate restructuring narrative. It represents a calculated attempt by an Indian industrial group to position itself within a supply chain that will define the next two decades of global energy infrastructure.

When big ASX news breaks, our subscribers know first

Why the Chemaf Acquisition Defies Simple Categorisation

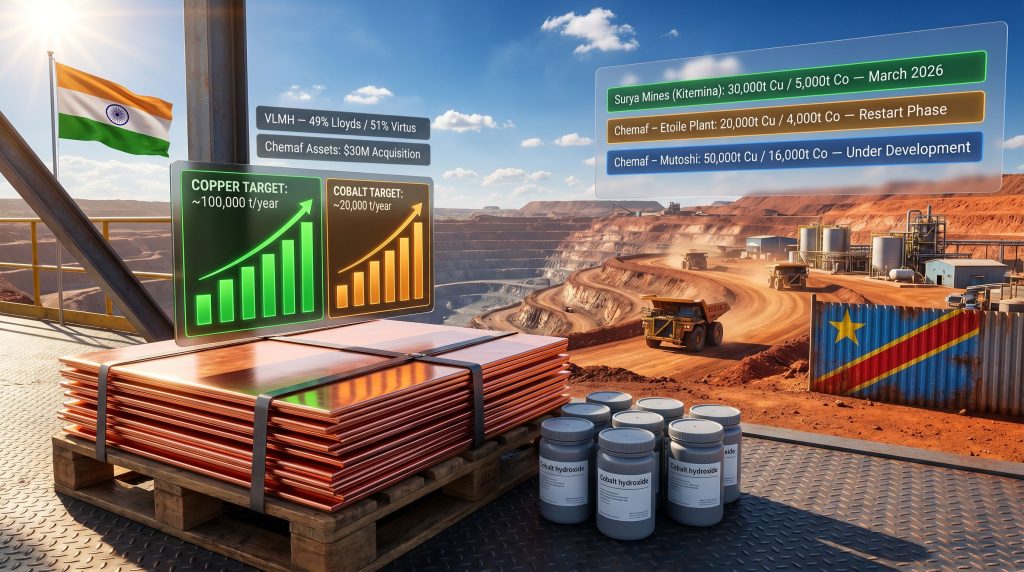

At first glance, the purchase of 100% of Chemaf's assets for $30 million through the Virtus Lloyds Minerals Holding (VLMH) joint venture appears modest. Lloyds holds 49% of VLMH, with Virtus Minerals retaining the remaining 51%. However, the acquisition price alone tells an incomplete story.

The more revealing figure is the estimated legacy debt burden attached to Chemaf: approximately $1 billion. This creates a debt-to-acquisition-price ratio of roughly 33 to 1, a ratio that signals not just distressed asset conditions but an extremely high-stakes operational rehabilitation challenge. Distressed asset acquisitions of this type are relatively common in the DRC's copper belt, where chronic underinvestment, commodity price cycles, and operational complexity have left numerous processing facilities underperforming relative to their installed capacity.

Acquiring a DRC copper-cobalt asset for $30 million while inheriting close to $1 billion in legacy obligations is not a conventional bargain. It is a structural bet on the acquirer's ability to generate enough cash flow, fast enough, to service obligations before creditor patience runs thin.

For Lloyds, the wager is that Chemaf's underlying asset quality justifies the risk. The Etoile plant carries a nameplate capacity of 20,000 tonnes per year of copper cathodes and 4,000 tonnes per year of cobalt. The under-development Mutoshi project, if completed on schedule, would add a further 50,000 tonnes per year of copper and 16,000 tonnes per year of cobalt. Combined, Chemaf alone could theoretically produce 70,000 tonnes of copper and 20,000 tonnes of cobalt annually, making it a genuinely significant platform by any measure. You can explore Virtus Minerals' community and acquisition activities for further context on the partnership's broader DRC commitments.

From Indian Iron Ore to Congolese Copper-Cobalt: Understanding Lloyds' Strategic Pivot

The Thriveni Connection and What It Means Operationally

Lloyds Metals and Energy's historical identity is rooted in Indian iron ore production, not hydrometallurgical copper-cobalt processing. Its affiliate, Thriveni Earthmovers, has built a reputation as one of India's largest private mining contractors, with deep expertise in coal extraction and large-scale open-pit operations. In 2025, Lloyds raised its ownership stake in Thriveni to approximately 80%, a consolidation move that significantly strengthened the group's integrated operational capability.

This vertical integration matters enormously in the DRC context. Owning a major mining contractor internally means Lloyds can deploy excavation and materials-handling expertise directly into African operations without relying on third-party contractors — a structural advantage that pure financial acquirers lack. However, it also highlights the group's primary knowledge base: bulk commodity extraction rather than the complex reagent chemistry and electrowinning processes that define copper cathode and cobalt hydroxide production.

Surya Mines as the Operational Template

Before assuming responsibility for Chemaf, Lloyds established its first African foothold through Surya Mines SARL, operating in Haut-Katanga province. The group controls Surya through a 50% stake in Nexus Holdco, which itself holds 90% of Surya Mines. The Kitemina hydrometallurgical plant at Surya carries an announced production capacity of 30,000 tonnes per year of copper cathodes and 5,000 tonnes per year of cobalt hydroxide, with operations commencing in March 2026. Surya also maintains an exploration programme across 16 mining concessions in the Likasi region.

The sequencing here is deliberate and strategically significant. By establishing Surya Mines first, Lloyds acquired not just a revenue-generating copper asset but an operational learning environment. Building institutional knowledge of DRC hydrometallurgical processing, workforce dynamics, regulatory interactions, and logistics infrastructure before taking on the far more complex Chemaf situation reflects a degree of operational discipline that is not universally present among new entrants to African critical minerals.

The Leadership Architecture at Chemaf: Capability Mapping

The formalisation of Chemaf's organisational structure, with an updated chart dated to late May and early June 2026, provides important governance signals about how Lloyds intends to operate the asset. Phillip Braun, CEO of Virtus, holds the formal CEO title at Chemaf, preserving the majority partner's board-level presence. The operational weight, furthermore, falls on two Lloyds-Thriveni executives.

| Executive | Role at Chemaf | Prior Background | Operational Scale |

|---|---|---|---|

| Soorya Prabhakaran | CEO-Designate | Thriveni iron ore, Odisha | Scaled production from 20Mt to 40Mt/year |

| Subramanian Alagappan | Deputy CEO | Coal, iron ore, open-pit mining | ~30 years across India, Indonesia, China, Mozambique |

Prabhakaran's track record of doubling iron ore output in Odisha from 20 million to 40 million tonnes per year demonstrates large-scale production ramp-up capability. Alagappan's nearly three decades of experience across multiple Asian and African jurisdictions brings cross-cultural operational depth that is difficult to replicate quickly. For additional detail on Soorya Prabhakaran's appointment as CEO-Designate, Lloyds' executive placement at Chemaf has been covered extensively in sector reporting.

The critical gap, however, is one that neither executive biography fully bridges: copper-cobalt hydrometallurgy. The technical requirements of solvent extraction and electrowinning (SX-EW), the process used to produce copper cathodes from oxide ores, differ substantially from iron ore beneficiation or coal extraction. DRC copper producers typically process ores through a sequence of crushing, leaching with sulphuric acid, solvent extraction, and electrowinning — each stage carrying its own chemistry management, reagent sourcing, and quality control challenges.

Cobalt recovery adds further complexity, often requiring separate precipitation circuits to capture cobalt hydroxide as a saleable product. Alagappan's dual role as both deputy CEO of Chemaf and country head for Lloyds and Thriveni in the DRC also raises questions about bandwidth. Managing two significant assets simultaneously in a challenging operating environment is a genuine execution risk, even for highly experienced operators.

Four Turnaround Challenges That Will Define Chemaf's Future

The Debt Structure Problem

The approximately $1 billion legacy debt inherited with the Chemaf acquisition is the most structurally constraining challenge Lloyds faces. This debt load does not simply represent a financial obligation; it actively limits the capital available for the plant restarts, equipment refurbishment, and workforce re-engagement that a successful operational turnaround requires. Creditor negotiations, phased repayment structures tied to production milestones, or asset-backed refinancing arrangements are likely pathways, but each carries its own execution risk and timeline uncertainty.

Restarting the Etoile Plant

The Etoile facility's installed capacity of 20,000 tonnes per year of copper cathodes and 4,000 tonnes per year of cobalt represents a meaningful production base if successfully restarted. However, bringing a care-and-maintenance facility back to full operating capacity in the DRC involves overcoming multiple simultaneous dependencies:

- Securing reliable power supply, a persistent challenge in Katanga given grid instability

- Sourcing sulphuric acid and other processing reagents, which require intact logistics chains

- Mobilising a skilled workforce, including electrolysis and chemistry technicians

- Confirming the structural and mechanical integrity of processing circuits after an extended shutdown period

The Mutoshi Expansion

The Mutoshi project represents the highest-value catalyst in the entire Chemaf investment thesis. At projected capacity of 50,000 tonnes per year of copper and 16,000 tonnes per year of cobalt, Mutoshi alone would be a major DRC copper asset by regional standards. The challenge is that development-stage projects in the DRC regularly face capital expenditure overruns and timeline extensions, driven by infrastructure constraints, permitting complexity, and equipment import logistics. No concrete public timeline for Mutoshi completion has been confirmed as of mid-2026.

Workforce Obligations

Outstanding wage arrears and contractual obligations owed to more than 3,000 employees and subcontractors represent a social and legal liability that cannot be deferred indefinitely. In the DRC's politically sensitive mining environment, unresolved workforce grievances can escalate into production disruptions, regulatory scrutiny, and reputational damage with the Congolese state — which is expected to receive a 10% direct equity stake in Chemaf as part of the transaction structure.

Of the four turnaround challenges, the debt burden and workforce obligations demand the most immediate capital allocation, while the Mutoshi project completion remains the single largest long-term value driver in the portfolio.

Scenario Modelling: Three Pathways to 100,000 Tonnes of Copper

Combining Surya Mines and a fully operational Chemaf, Lloyds has articulated a vision of approximately 100,000 tonnes of copper and 20,000 tonnes of cobalt per year across its DRC portfolio. Three scenarios bracket the range of possible outcomes.

| Scenario | Copper Output (t/year) | Key Assumptions |

|---|---|---|

| Full Execution | ~100,000 | Surya at capacity, Etoile restarted, Mutoshi completed on schedule |

| Partial Execution | 40,000–55,000 | Surya at 60–70%, Etoile restarted, Mutoshi delayed 18–24 months |

| Execution Failure | Below 35,000 | Debt stalls, Chemaf in care-and-maintenance, Surya as sole active asset |

The gap between the full execution and downside scenarios is enormous. Investors should note that Lloyds' communications have emphasised Chemaf's industrial potential rather than providing concrete production restart timelines. This communication pattern is common among operators managing complex turnarounds, where committing to specific milestones before operational readiness is confirmed carries its own credibility risk.

This scenario analysis is based on publicly available information and announced capacities. Actual production outcomes will depend on factors including debt resolution, capital availability, regulatory conditions, and operational execution. This content does not constitute financial or investment advice.

The next major ASX story will hit our subscribers first

The Geopolitical Dimension: India in the DRC's Critical Minerals Corridor

Chinese state-backed entities currently dominate DRC copper-cobalt production, controlling a substantial proportion of the country's output through integrated mining and processing assets. The entry of an Indian industrial group into this landscape carries significance beyond the corporate level, particularly given intensifying Congolese cobalt rivalry between global powers competing for supply chain influence.

India's broader strategic interest in reducing dependence on Chinese-controlled critical mineral supply chains has gained momentum as the country expands its domestic electric vehicle manufacturing ambitions and battery production targets. Lloyds' DRC expansion, driven by a privately controlled industrial group rather than a state-backed financing model, represents a structurally different approach to African resource acquisition compared to the long-term offtake and infrastructure financing packages that have characterised Chinese investment in the region.

The Thriveni operational model, centred on large-scale contracting expertise rather than passive financial ownership, could prove to be a genuine differentiator if Lloyds can demonstrate that Indian-led operators can execute complex African mining turnarounds successfully. A proven track record at Chemaf would position the Lloyds-Thriveni group as a credible alternative operating partner for future DRC copper-cobalt asset development, at a moment when diversification of the DRC's operator base is increasingly viewed as a strategic priority by Western governments and multilateral institutions.

The Congolese State's 10% Stake: Governance Complexity or Strategic Alignment?

The announced transfer of a 10% equity stake in Chemaf to the Congolese state reflects the requirements and expectations embedded in the DRC's mining regulatory framework. Post-transfer, the ownership architecture will involve Lloyds' 49% interest in VLMH sitting alongside Virtus' 51%, with the state holding a direct Chemaf stake. The DRC mineral wealth that underpins these arrangements remains central to why international investors continue to accept complex regulatory conditions in exchange for access.

State participation in major DRC mining assets is a structural feature of the country's mining code, designed to ensure that a portion of resource revenues flows directly to national accounts rather than entirely to foreign investors. In practice, this arrangement creates a dual dynamic: the state becomes a stakeholder with an interest in operational success, but it also introduces a governance layer that can slow decision-making in circumstances requiring rapid capital allocation or strategic pivots.

The DRC's history of mining contract renegotiations and regulatory evolution means that Lloyds must manage this relationship carefully. Beyond equity structure, the country's infrastructure realities — including unreliable grid power in Katanga, complex road logistics toward export corridors, and the operational implications of working across multiple regulatory bodies — will shape the pace at which the Chemaf turnaround can realistically progress. In addition, the broader context of the DRC cobalt export ban adds a further regulatory dimension that all operators, including Lloyds, must factor into production planning.

Key Asset Data: Lloyds' Full DRC Critical Minerals Platform

| Asset | Location | Copper Capacity (t/year) | Cobalt Capacity (t/year) | Status |

|---|---|---|---|---|

| Surya Mines (Kitemina) | Haut-Katanga | 30,000 | 5,000 | Operational from March 2026 |

| Chemaf Etoile Plant | DRC | 20,000 | 4,000 | Restart phase |

| Chemaf Mutoshi Project | DRC | 50,000 | 16,000 | Under development |

| Combined DRC Target | DRC | ~100,000 | ~20,000 | Subject to full execution |

Frequently Asked Questions

What assets does Chemaf operate in the DRC?

Chemaf's portfolio includes the Etoile processing plant, with nameplate capacity of 20,000 tonnes per year of copper cathodes and 4,000 tonnes per year of cobalt, and the under-development Mutoshi project, which is projected to produce 50,000 tonnes per year of copper and 16,000 tonnes per year of cobalt upon completion.

How does VLMH structure Lloyds' ownership of Chemaf?

Virtus Lloyds Minerals Holding (VLMH) acquired 100% of Chemaf's assets for $30 million. Lloyds holds 49% of VLMH and Virtus Minerals holds 51%. The Congolese state is expected to receive a separate 10% direct stake in Chemaf.

What is Lloyds' combined copper production target across its DRC portfolio?

Combining Surya Mines and a fully expanded Chemaf, Lloyds is targeting approximately 100,000 tonnes of copper and 20,000 tonnes of cobalt per year across its DRC operations. The cobalt export suspension impact on these targets remains an important variable that investors should monitor closely.

What are the primary risks to the Chemaf turnaround timeline?

The four core challenges are: a legacy debt burden of approximately $1 billion, the technical and logistical complexity of restarting the Etoile plant, uncertainty around the timeline and capital requirements for completing the Mutoshi expansion, and outstanding wage arrears owed to more than 3,000 employees and subcontractors. Furthermore, the Congo cobalt price impacts resulting from ongoing export restrictions could influence the revenue projections underpinning the turnaround business case.

The Road Ahead: Execution Risk Versus Strategic Potential

The Chemaf acquisition, viewed honestly, is a high-complexity, high-upside critical minerals bet. The strategic logic is coherent: secure distressed but potentially productive copper-cobalt assets in the world's most important cobalt jurisdiction, leverage Thriveni's large-scale operational capability to restart and expand production, and position the Lloyds group within the battery metals supply chains that electrification growth will increasingly depend upon. Consequently, Lloyds expands role at DRC's Chemaf carries implications that extend well beyond a single transaction.

The execution risk is equally substantial. A ~$1 billion debt load, a production facility requiring restart, an expansion project without a confirmed completion timeline, and obligations to thousands of workers represent a formidable combination of challenges. The leadership team's bulk commodity expertise is a meaningful asset, but the hydrometallurgical knowledge gap is real and will likely require external technical recruitment to bridge effectively.

By 2027 and 2028, the markers of credible progress will become clearer: whether the Etoile plant has achieved consistent production output, whether Mutoshi has reached a defined construction milestone, and whether the debt restructuring has been formalised in a way that does not constrain operational capital allocation. If those milestones are met, Lloyds will have established something genuinely significant: proof that an Indian-led private industrial group can execute a large-scale African critical minerals turnaround, outside the state-backed financing models that have defined the sector's recent history.

Readers seeking broader context on DRC copper-cobalt sector developments and African mining investment dynamics are encouraged to explore sector-focused reporting published by Ecofin Agency on Virtus' broader DRC copper-cobalt commitments.

Want to Track the Next Major Copper or Cobalt Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including battery metals opportunities across copper and cobalt — transforming complex commodity data into actionable insights for investors at every level. Explore historic returns from major mineral discoveries and begin your 14-day free trial today to position yourself ahead of the market.