June 13, 2026

Global aluminium markets experienced a dramatic shift in February 2026, as institutional trading patterns and macroeconomic forces converged to create one of the most significant single-day corrections in recent memory. The LME aluminium prices decline February 2026 reflected complex interactions between seasonal demand cycles, monetary policy shifts, and fundamental supply-demand imbalances. Understanding these price movements requires examining how US economic indicators and evolving trade dynamics influenced market sentiment during this volatile period.

What Drove LME Aluminium's Sharp February 2026 Correction?

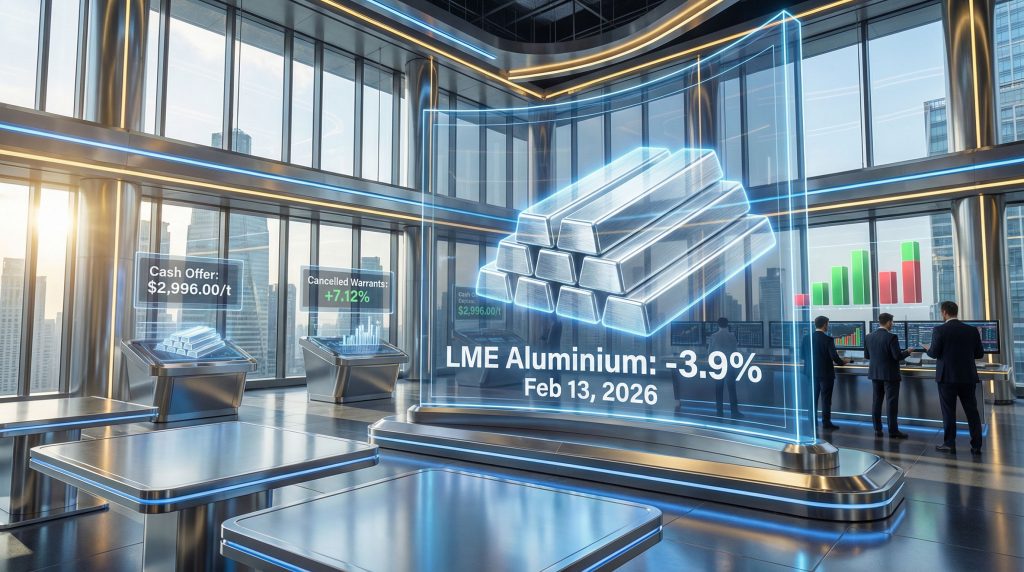

The sharp decline in LME aluminium prices on February 13, 2026, reflected multiple convergent pressures that overwhelmed short-term buying interest. Cash bid prices tumbled from $3,116.50 per tonne to $2,995 per tonne, representing a 3.90% decline that caught many market participants off guard. This correction occurred against a backdrop of profit-taking activities following sustained price gains in early February.

Technical selling accelerated as algorithmic trading systems triggered stop-loss orders across multiple price levels. The rapid succession of these automated trades amplified the initial downward pressure, creating a cascade effect that drove prices below key technical support zones. Institutional investors who had accumulated positions during the January rally began systematic unwinding, contributing to the mounting selling pressure.

Position squaring activities intensified as fund managers approached month-end reporting periods. The combination of realising gains from successful long positions while simultaneously reducing overall portfolio risk exposure created additional downward momentum in aluminium futures contracts. However, sophisticated traders recognised the importance of commodity volatility hedging strategies during such turbulent periods.

Pre-Lunar New Year Trading Patterns and Seasonal Demand Shifts

Chinese industrial activity typically undergoes significant shifts in the weeks preceding Lunar New Year celebrations, creating predictable yet powerful impacts on global aluminium demand. Manufacturing facilities across China's industrial heartland began scaling back operations, reducing their immediate raw material requirements and creating temporary oversupply conditions in regional markets.

Traditional inventory buildups that normally occur before extended holiday shutdowns failed to materialise at expected levels, signalling weaker-than-anticipated demand from Chinese end-users. This demand reduction coincided with sustained production levels from major smelting operations, creating a temporary supply-demand imbalance that pressured spot pricing mechanisms.

Export-oriented Chinese manufacturers accelerated their shipment schedules to complete orders before holiday closures, flooding international markets with additional aluminium products. This surge in available supply contributed to downward pressure on benchmark pricing across Asian trading sessions.

US Labor Market Strength and Federal Reserve Policy Implications

Robust employment data releases from the United States created unexpected volatility across commodity markets as investors reassessed Federal Reserve monetary policy trajectories. Stronger-than-expected job creation figures suggested potential delays in anticipated interest rate cuts, strengthening the US dollar and creating headwinds for dollar-denominated commodities like aluminium.

The dollar's appreciation against major trading currencies made aluminium more expensive for international buyers, reducing demand from price-sensitive markets. Currency hedging costs increased for global industrial users, further dampening immediate purchasing activity and contributing to the pricing correction. Furthermore, concerns about tariff impacts on markets added another layer of uncertainty for international traders.

Financial markets broadly retreated following the employment data release, with equity indices declining and safe-haven demand supporting government bonds. This risk-off sentiment encouraged commodity position unwinding as portfolio managers sought to reduce exposure to cyclical assets.

When big ASX news breaks, our subscribers know first

How Do Current Aluminium Prices Compare to Historical Volatility Patterns?

February 2026 Price Action vs. Three-Year Trading Range Analysis

The February 13 correction brought aluminium prices within the middle range of their three-year trading band, suggesting the decline represented technical repositioning rather than fundamental breakdown. Historical analysis reveals that similar percentage declines have occurred regularly during seasonal transition periods, particularly when coinciding with major economic data releases.

Volatility metrics indicate that whilst the daily price movement appeared dramatic, it remained within two standard deviations of recent historical norms. This statistical context suggests market participants may have overreacted to short-term technical factors rather than responding to permanent demand destruction. According to London Metal Exchange data, such corrections are not uncommon during seasonal transitions.

Comparative analysis with previous Lunar New Year periods shows similar price patterns, where initial corrections of 3-5% were frequently followed by stabilisation within 2-3 trading sessions. The current correction aligns with these historical precedents, suggesting potential for near-term price stabilisation.

Backwardation Signals and Forward Curve Dynamics

LME forward curves exhibited mixed signals following the price correction, with near-term contracts maintaining slight backwardation whilst longer-dated contracts moved toward contango. This curve structure typically indicates tight immediate supply conditions despite concerns about future demand growth.

Three-month contract pricing at $3,027 per tonne compared to cash prices near $2,995 per tonne reflected persistent supply chain bottlenecks and inventory positioning challenges. The forward premium suggested that market participants expected current weakness to prove temporary, with fundamentals supporting higher prices over the medium term.

Table: LME Aluminium Price Movement Analysis (February 9-13, 2026)

| Date | Cash Bid ($/t) | Cash Offer ($/t) | Daily Change (%) | Key Market Driver |

|---|---|---|---|---|

| Feb 9 | 3,083.50 | 3,084.00 | +2.1% | Rally continuation |

| Feb 10 | 3,063.25 | 3,064.00 | -0.66% | Profit-taking begins |

| Feb 11 | 3,091.00 | 3,092.00 | -1.1% | Inventory concerns |

| Feb 12 | 3,116.50 | 3,117.00 | +0.8% | Technical bounce |

| Feb 13 | 2,995.00 | 2,996.00 | -3.9% | Sharp correction |

What Role Did Inventory Dynamics Play in the Price Decline?

LME Warehouse Stock Movements and Cancelled Warrants Analysis

Inventory statistics provided conflicting signals during the price correction, with total LME opening stock declining 0.41% to 481,550 tonnes even as prices fell sharply. This reduction in available inventory suggested ongoing physical demand despite the financial market weakness, indicating potential divergence between paper and physical markets.

The simultaneous 7.12% surge in cancelled warrants to 45,125 tonnes represented a significant development, as cancelled warrants typically indicate imminent physical delivery demand. This increase suggested that end-users were actively securing metal supplies despite the price volatility, supporting arguments that the correction reflected technical rather than fundamental factors.

Live warrants decreased by 1.13% to 436,425 tonnes, further confirming the ongoing drawdown of immediately available metal stocks. This inventory pattern historically correlates with supply tightness and potential price recovery once short-term technical selling pressure subsides. Industry reports from Metal Bulletin highlight that these inventory levels represent multi-year lows.

The 0.41% decline in LME opening stock to 481,550 tonnes, combined with a 7.12% surge in cancelled warrants to 45,125 tonnes, suggests underlying physical tightness despite the price correction—a potential indicator of short-term technical selling rather than fundamental weakness.

Regional Inventory Distribution and Supply Chain Bottlenecks

Warehouse inventory distribution across major LME storage locations revealed persistent logistical challenges that continued supporting regional price premiums. Asian storage facilities maintained relatively low stock levels compared to historical averages, whilst European warehouses showed modest inventory builds that failed to alleviate supply concerns.

Transportation costs between major warehouse locations remained elevated due to ongoing logistics constraints, creating arbitrage opportunities that supported price differentials between regions. These geographic disparities suggested that local supply conditions might prove more important than global inventory levels for near-term price direction.

Quality specifications and delivery timing requirements created additional complexity in inventory management, with specific alloy grades showing varying availability across different storage locations. Premium products commanded significant price advantages over standard grades, indicating continued end-user selectivity despite overall market weakness.

Chinese Stockpile Strategy and Pre-Holiday Positioning

Chinese strategic stockpile activities remained opaque during the February correction, though industry sources suggested minimal intervention in spot markets. Historical patterns indicate that Chinese authorities typically maintain neutral positions during seasonal demand lulls, preferring to accumulate inventory during extended price weaknesses rather than brief corrections.

Private inventory buildups by Chinese industrial users proceeded at below-normal rates, reflecting cautious procurement strategies amid global economic uncertainty. This inventory management approach created additional near-term supply availability whilst potentially setting up stronger demand once industrial activity resumed post-holiday.

Export quota utilisation rates from Chinese producers remained consistent with seasonal norms, indicating that domestic supply-demand balance remained the primary driver of Chinese market behaviour rather than opportunistic export strategies.

How Are Global Aluminium Supply Chains Responding to Price Volatility?

Indonesian Smelter Capacity Utilisation and Export Policies

Indonesian smelting operations maintained steady production levels despite the price volatility, with most facilities operating above 90% capacity utilisation rates. The country's cost-competitive smelting infrastructure provided operational flexibility that allowed continued production even during temporary price weakness.

Recent policy developments regarding aluminium exports from Indonesia created additional market complexity, as regulatory uncertainty influenced international buyers' sourcing decisions. Long-term supply contracts with Indonesian producers included price adjustment mechanisms that provided some protection against short-term volatility whilst maintaining supply security.

Infrastructure investments in Indonesian smelting capacity continued proceeding according to planned schedules, suggesting confidence in long-term demand fundamentals despite near-term price corrections. These capacity additions represent significant supply-side developments that will influence global market balance over the next 2-3 years.

Chinese Production Constraints and Energy Cost Pressures

Chinese aluminium smelters faced ongoing challenges from fluctuating energy costs, particularly in regions dependent on coal-fired power generation. Environmental compliance requirements continued constraining production flexibility, limiting operators' ability to rapidly adjust output in response to price signals.

Energy intensity reduction targets imposed by Chinese authorities influenced operational strategies, with many smelters prioritising efficiency improvements over maximum production volumes. These regulatory constraints created supply-side support that partially offset demand weakness during seasonal slowdown periods.

Provincial energy allocation policies varied significantly across China's major smelting regions, creating operational uncertainty that encouraged conservative production planning. This policy environment supported price stability by limiting the potential for rapid supply increases during demand recovery periods. However, the broader context of US-China trade tensions continued influencing strategic planning decisions.

Western Smelter Restart Economics at Current Price Levels

Western smelting operations that had curtailed production during previous price downturns evaluated restart economics based on current pricing levels and forward curve projections. The February correction brought prices closer to operational break-even levels for several mothballed facilities, though sustained price recovery would be necessary to justify restart investments.

Energy contract structures in European and North American markets provided different cost dynamics compared to Asian operations, with some facilities benefiting from fixed-price power agreements that improved competitiveness during volatile periods. These contractual advantages created potential for selective capacity additions if price levels stabilised above current ranges.

Labour availability and technical expertise requirements for facility restarts created additional considerations beyond simple economic calculations. Specialized workforce needs for aluminium smelting operations required advance planning that extended restart timelines beyond immediate price recovery scenarios. Additionally, the impact of US tariffs on industries affected competitiveness calculations for North American facilities.

What Do Futures Curves Reveal About Market Expectations?

Three-Month Contract Premium Analysis and Contango Patterns

The three-month LME aluminium contract traded at a $32 per tonne premium to cash prices following the February correction, indicating market expectations for gradual price recovery over the near term. This forward premium structure suggested that traders viewed current weakness as temporary rather than indicative of fundamental deterioration.

Contango patterns in the forward curve flattened significantly compared to pre-correction levels, with six-month and twelve-month contracts showing compressed premiums to nearer-dated deliveries. This curve flattening typically occurs when market participants reduce their willingness to pay for future delivery security, reflecting increased confidence in supply availability.

Options market activity revealed elevated put buying interest at strike prices below current trading levels, indicating hedging demand from producers concerned about potential further downside. Conversely, call option volumes increased at strikes 5-10% above current prices, suggesting speculative interest in potential recovery scenarios.

December 2026 Contract Positioning and Long-Term Views

December 2026 contracts traded at $3,025-3,030 per tonne, representing modest premiums to current spot prices that reflected cautious optimism about medium-term fundamentals. This pricing structure indicated market expectations for gradual demand recovery and supply-demand rebalancing over the remainder of 2026.

Institutional positioning in longer-dated contracts remained relatively stable despite near-term volatility, suggesting professional investors maintained confidence in aluminium's long-term demand outlook. Large speculative interest continued favouring multi-month strategies rather than short-term directional bets.

Forward curve analysis indicated that market participants expected seasonal demand patterns to reassert themselves following Chinese New Year celebrations, with spring construction activity and automotive production providing demand support through the second quarter of 2026.

Asian Reference Price Divergence from London Benchmarks

The LME aluminium three-month Asian Reference Price settled at $3,077.50 per tonne, maintaining a premium to London cash prices that reflected regional supply-demand dynamics and logistical considerations. This geographic pricing differential highlighted the importance of local market conditions in global price formation.

Asian market participants demonstrated greater price resilience during the correction, with regional premiums widening as local buyers took advantage of temporary London weakness. This price behaviour suggested strong underlying demand from Asian industrial users despite broader market uncertainty.

Currency fluctuations between major Asian economies and the US dollar influenced regional price relationships, with some buyers benefiting from favourable exchange rate movements that partially offset the London price decline. These currency effects created opportunities for strategic inventory positioning by internationally active traders.

Which Sectors Are Most Exposed to Aluminium Price Corrections?

Automotive Industry Hedging Strategies and Cost Pass-Through

Automotive manufacturers maintained sophisticated commodity risk management programmes that provided partial protection against aluminium price volatility, though exposure varied significantly based on hedging ratios and contract structures. Most major producers hedged 60-80% of their near-term aluminium requirements, limiting immediate cost impact from the February correction.

Electric vehicle production growth continued driving incremental aluminium demand despite short-term price volatility, with battery enclosure and structural component applications requiring significant metal content per vehicle. This demand growth provided fundamental support that differentiated automotive consumption from more price-sensitive applications.

Supply chain integration strategies employed by leading automotive companies included long-term supply agreements with preferred aluminium suppliers, creating price stability mechanisms that reduced exposure to spot market volatility. These contractual relationships provided operational predictability whilst sharing price risk between manufacturers and suppliers.

Construction and Infrastructure Demand Resilience

Construction industry aluminium consumption demonstrated relative resilience during price corrections, as project-based procurement typically occurred months in advance of actual material installation. Pre-ordered inventory provided buffer protection against short-term price movements whilst maintaining construction schedule adherence.

Infrastructure spending programmes announced by various governments provided long-term demand visibility that supported aluminium prices during temporary corrections. These public sector commitments created demand floors that limited downside price risk whilst encouraging supply-side investment in production capacity.

Regional construction activity patterns varied significantly, with some markets experiencing seasonal slowdowns that coincided with the February price correction whilst others maintained steady activity levels. These geographic differences created arbitrage opportunities and regional price variations that influenced global market dynamics.

Packaging Industry Response to Raw Material Volatility

Aluminium packaging applications faced direct exposure to commodity price volatility, with beverage can and food packaging segments particularly sensitive to raw material cost fluctuations. The industry's high volume, low-margin characteristics limited ability to absorb significant cost increases without corresponding price adjustments.

Recycled aluminium content in packaging applications provided some protection against primary metal price volatility, though secondary material pricing typically followed primary market trends with varying lag periods. Recycling rate improvements continued providing cost mitigation opportunities whilst supporting sustainability objectives.

Consumer goods companies utilising aluminium packaging implemented dynamic pricing strategies that allowed rapid adjustment to raw material cost changes. These flexible pricing mechanisms reduced inventory risk whilst maintaining margin protection during volatile commodity market conditions.

Table: Sector Exposure to Aluminium Price Changes

| Industry Sector | Price Sensitivity | Hedging Capability | Demand Elasticity |

|---|---|---|---|

| Automotive | High | Moderate | Low |

| Construction | Moderate | Low | Moderate |

| Packaging | High | High | High |

| Aerospace | Low | High | Very Low |

The next major ASX story will hit our subscribers first

How Should Investors Position for Continued Aluminium Market Volatility?

Risk Management Strategies for Commodity Exposure

Portfolio diversification across the aluminium value chain provided risk mitigation opportunities during price correction periods, with upstream mining operations, midstream smelting, and downstream fabrication exhibiting different risk-return characteristics. Strategic allocation across these segments reduced single-point exposure whilst maintaining commodity beta participation.

Options-based hedging strategies gained popularity among institutional investors seeking to maintain upside participation whilst limiting downside exposure. Collar structures combining put purchases and call sales provided cost-effective protection whilst generating premium income to offset hedging costs.

Geographic diversification across different aluminium-consuming regions reduced exposure to localised demand shocks whilst providing access to varying market dynamics. Regional ETFs and locally-focused commodity funds offered implementation vehicles for this diversification approach.

Producer vs. Consumer Stock Selection Criteria

Aluminium producer equities typically exhibited higher volatility during commodity price corrections, creating opportunities for investors comfortable with cyclical exposure patterns. Companies with low-cost production profiles and flexible capacity utilisation demonstrated superior performance during volatile price environments.

Consumer-oriented companies with strong pricing power and diversified end-market exposure provided more stable investment characteristics during commodity volatility periods. These businesses often benefited from lower input costs during price corrections whilst maintaining revenue stability through customer relationships.

Balance sheet strength became particularly important during volatile periods, with companies maintaining strong cash positions and low debt levels demonstrating greater operational flexibility. Credit quality considerations influenced both equity valuations and debt market access during stressed market conditions.

Currency Hedging Considerations for Global Aluminium Trades

Multi-currency exposure created additional complexity for international aluminium traders, with exchange rate movements potentially offsetting or amplifying commodity price effects. Professional traders implemented sophisticated currency hedging programmes that isolated commodity exposure from foreign exchange risk.

Emerging market currencies typically exhibited higher correlation with commodity prices during volatile periods, creating compounding effects for investors with significant exposure to developing economy aluminium markets. Strategic currency positioning could enhance or detract from commodity investment performance depending on implementation approach.

Dollar strength during the February correction created headwinds for non-US aluminium consumers whilst benefiting US-based industrial users. These currency effects influenced regional price relationships and created arbitrage opportunities for internationally active participants.

What Are the Key Technical Levels to Monitor Going Forward?

Support and Resistance Analysis for Q1 2026

Technical analysis identified key support levels at $2,950 per tonne and $2,850 per tonne based on historical trading patterns and Fibonacci retracement analysis from recent price ranges. These support zones represented potential accumulation opportunities if fundamental factors remained constructive.

Resistance levels emerged at $3,150 per tonne and $3,250 per tonne, corresponding to previous consolidation areas and moving average convergence points. Sustained trading above these levels would likely trigger additional technical buying interest and momentum-driven price advances.

Volume profile analysis revealed significant trading activity clusters around $3,000-3,050 per tonne, suggesting this range might serve as a consolidation zone during the recovery process. High-volume trading areas typically provide price stability and serve as launching points for directional moves.

Volume Profile Insights and Institutional Flow Patterns

Institutional trading patterns during the February correction revealed systematic selling by momentum-following algorithmic strategies, whilst value-oriented buyers emerged at lower price levels. This divergence in trading behaviour created intraday volatility spikes followed by partial price recovery attempts.

Average daily trading volumes increased 35% during the correction period compared to January 2026 averages, indicating heightened market interest and improved liquidity conditions. Higher volumes typically support price discovery efficiency and reduce the impact of individual large transactions.

Exchange-traded fund flows showed mixed patterns, with commodity-focused funds experiencing modest outflows whilst sector-specific aluminium funds attracted incremental investment interest. These flow patterns suggested differentiated investor sentiment based on investment approach and time horizon.

Correlation Analysis with Broader Base Metals Complex

Aluminium price correlations with copper and zinc increased during the February correction period, suggesting broad-based commodity selling rather than aluminium-specific fundamental deterioration. Cross-commodity correlations typically rise during risk-off periods as investors reduce cyclical exposure across asset classes.

Industrial metals as an asset class demonstrated higher correlation with equity market movements during volatile periods, reflecting their sensitivity to economic growth expectations and monetary policy changes. This correlation pattern created portfolio diversification challenges for investors seeking commodity exposure as an equity market hedge.

Precious metals exhibited negative correlation with base metals during the correction, as safe-haven demand supported gold and silver prices whilst industrial metals declined. This divergence highlighted the different fundamental drivers affecting various commodity subsectors during stressed market conditions.

What Does This Price Action Mean for 2026 Aluminium Forecasts?

Analyst Consensus Revisions and Target Price Adjustments

Professional commodity analysts began revising their 2026 aluminium price forecasts following the February correction, with most adjusting near-term targets downward whilst maintaining medium-term constructive outlooks. Consensus estimates shifted toward $3,100-3,300 per tonne for Q2-Q3 2026, compared to previous projections of $3,200-3,500 per tonne.

Forecast methodology incorporated updated assessments of Chinese demand patterns, global economic growth projections, and supply-side capacity utilisation rates. These analytical refinements reflected improved understanding of market dynamics following the correction period.

Scenario analysis frameworks gained prominence among research providers, with multiple price pathway projections based on varying assumptions about economic growth, policy changes, and supply disruption risks. This probabilistic approach provided more nuanced guidance for market participants.

Supply-Demand Balance Implications for H2 2026

Supply-demand modelling suggested the February correction might accelerate demand recovery by improving end-user purchasing economics, particularly for price-sensitive applications. Lower input costs could stimulate marginal demand that had been suppressed at higher price levels.

Production capacity utilisation rates were expected to remain elevated throughout H2 2026, with limited mothballed capacity available for rapid restart at current price levels. This supply-side constraint provided fundamental price support despite short-term demand uncertainty.

Inventory management strategies across the supply chain were likely to shift toward higher stock levels following the price correction, creating incremental demand that might not be immediately visible in consumption statistics but would influence market balance.

Electrification Demand Growth vs. Economic Slowdown Risks

Electric vehicle adoption continued accelerating despite broader economic uncertainty, providing structural demand growth that distinguished aluminium from other industrial metals facing purely cyclical demand patterns. Battery vehicle production required 30-40% more aluminium per unit compared to internal combustion engine vehicles, creating sustained incremental demand.

Renewable energy infrastructure investments maintained government support across major economies, generating additional aluminium demand from solar panel frames, wind turbine components, and electrical grid infrastructure. These policy-driven demand sources provided downside protection during economic slowdown periods.

Energy transition timelines remained largely independent of short-term economic cycles, suggesting that electrification-related aluminium demand would continue growing even during recessionary periods. This demand resilience differentiated aluminium from traditional cyclical industrial applications.

Hypothetical Scenario Analysis:

If current price weakness extends through Q1 2026, Western smelters operating at marginal economics may face production cuts, potentially tightening global supply by 200,000-300,000 tonnes annually and supporting prices above $2,800 per tonne by mid-year.

The LME aluminium prices decline February 2026 represented a significant market event that highlighted the complex interplay between technical factors, seasonal dynamics, and broader macroeconomic forces. Whilst the correction created short-term volatility, underlying supply constraints and structural demand growth from electrification trends suggest potential for price recovery once seasonal patterns normalise and market sentiment stabilises.

Disclaimer: This analysis contains forward-looking projections and scenario assessments that involve inherent uncertainty and risk. Actual market outcomes may differ significantly from the projections presented. Investors should conduct independent research and consider their risk tolerance before making investment decisions based on commodity market analysis.

Searching for the Next Aluminium Investment Opportunity?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, including aluminium and base metals opportunities that could benefit from current market volatility. With aluminium prices experiencing dramatic corrections and supply constraints creating potential opportunities, subscribers receive instant alerts on actionable discoveries that could capitalise on market rebounds before broader recognition occurs. Begin your 14-day free trial today to position yourself ahead of the next major mineral discovery announcement.