July 7, 2026

The Material That Makes Clean Energy Possible — And Why Its Supply Chain Is Broken

There is a single material class sitting at the intersection of every major clean energy technology deployed at scale today. Neodymium-iron-boron sintered permanent magnets, universally known in the industry as NdFeB magnets, are not optional components in electric vehicle drivetrains or offshore wind turbines. They are foundational. Without them, the torque density required for compact EV traction motors cannot be achieved, and direct-drive wind turbines lose the mechanical simplicity that makes them cost-competitive at gigawatt scale.

The problem is not that NdFeB magnets are scarce in nature. The problem is that the infrastructure required to transform rare earth ore into finished sintered magnets has been built almost entirely within one country over the past three decades. China currently accounts for an estimated 85 to 90 percent of global NdFeB magnet production capacity, having systematically developed every stage of the value chain from mining through to final fabrication. For manufacturers in Europe, North America, Japan, South Korea, and Australia, this is not merely a commercial inconvenience. It is a structural vulnerability with direct implications for defence procurement, energy security, and industrial competitiveness.

The Lynas JS Link Malaysian magnet factory deal, formalised in mid-2026, represents one of the most substantive attempts yet to build a commercially viable alternative outside China's orbit.

When big ASX news breaks, our subscribers know first

Understanding the Rare Earth Value Chain Before Assessing This Deal

To appreciate why the Lynas JS Link Malaysian magnet factory deal matters, it helps to understand how radically different the three stages of the rare earth supply chains value chain are from one another.

| Stage | Description | Where Value Is Created | China's Market Share |

|---|---|---|---|

| Mining | Extraction of rare earth-bearing ore from the ground | Raw material volume | ~60% of global production |

| Separation & Refining | Chemical processing to isolate individual rare earth oxides and metals | Purity and specification control | ~85-90% of global capacity |

| Magnet Fabrication | Alloying, pressing, sintering, and magnetising NdFeB components | Finished product margin | ~85-90% of global output |

What this table reveals is a critical insight that many investors and policymakers miss: simply mining more rare earths outside China does not solve the magnet supply problem. A country or company can produce substantial quantities of neodymium and praseodymium concentrate and still have no pathway to market if sintered magnet manufacturing capacity does not exist outside China to absorb it.

Lynas Rare Earths (ASX: LYC) has spent years addressing the refining gap as the world's largest non-Chinese rare earth refiner. Its Lynas Advanced Materials Plant (LAMP) in Kuantan, Malaysia, produces separated rare earth products including neodymium-praseodymium (NdPr) oxide, which is the primary feedstock for NdFeB magnet production. The JS Link partnership is now designed to address the next gap: converting that refined material into finished magnets on Malaysian soil.

What the Lynas JS Link Malaysian Magnet Factory Deal Actually Involves

The Core Investment Structure

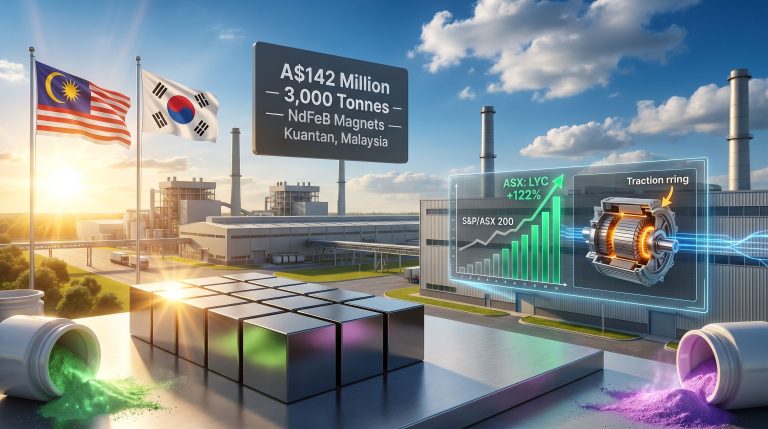

The agreement brings together Lynas Rare Earths as both a material supplier and an equity investor, committing approximately A$50 million toward a facility with a total development budget of RM600 million (roughly US$142 million). JS Link, a South Korean permanent magnet manufacturer, is the industrial partner responsible for developing and operating the factory, with land acquisition in Pahang state already confirmed and active development underway. Malaysia's Prime Minister has confirmed that the investment will meaningfully boost the country's rare earth sector.

Critically, this arrangement has progressed beyond a non-binding memorandum of understanding. The combination of confirmed land acquisition, committed capital, and pilot production activity by JS Link places this squarely in the category of an active development project rather than a feasibility exercise.

Partner Profiles and Strategic Fit

| Partner | Role | Key Differentiator |

|---|---|---|

| Lynas Rare Earths (ASX: LYC) | NdPr material supplier and equity investor | World's largest non-Chinese rare earth refiner; LAMP facility already operating in Kuantan |

| JS Link | Factory developer and magnet manufacturer | South Korean producer bringing Asian manufacturing discipline and magnet sintering expertise to its first dedicated large-scale facility |

The geographic logic here is deliberate. Lynas's LAMP refinery is already located in Kuantan, Pahang. Placing the JS Link magnet factory in the same state eliminates the need to export refined NdPr material to a third country for processing, then re-import finished magnets. It compresses the supply chain laterally, reducing logistics costs, export compliance complexity, and the carbon footprint of material transport.

Production Targets and Material Flows

The facility is designed to reach a nameplate capacity of 3,000 tonnes per annum of NdFeB sintered permanent magnets. To contextualise that figure: global NdFeB magnet demand was estimated at approximately 200,000 tonnes per year as of the mid-2020s, with projections pointing toward sustained growth driven by EV adoption and offshore wind deployment. A 3,000-tonne facility does not resolve the global supply concentration problem on its own, but it establishes a commercially replicable template and anchors non-Chinese supply chain credibility in a way that paper commitments cannot.

End-Use Demand Driving the Strategic Logic

The commercial rationale for this investment is anchored in hard demand fundamentals. Consider the key application sectors:

-

Electric vehicle traction motors: Each EV motor requires approximately 1 to 2 kilograms of NdFeB magnets. With global EV sales forecast to exceed 40 million units annually by the early 2030s, annual magnet demand from this segment alone could surpass 60,000 tonnes.

-

Offshore wind turbines: Direct-drive generators, which are increasingly preferred in offshore applications for their reduced maintenance requirements, can require up to 600 kilograms of permanent magnets per megawatt of installed capacity. A single 15 MW offshore turbine therefore requires up to 9 tonnes of NdFeB magnets.

-

Industrial robotics and automation: Precision servo motors and actuators in advanced manufacturing rely on high-coercivity sintered magnets that cannot be substituted with ferrite alternatives without severe performance losses.

-

Defence and aerospace systems: Guidance systems, electric propulsion platforms, radar components, and unmanned aerial vehicle motors all depend on NdFeB magnets classified under critical materials frameworks in the United States, European Union, Japan, and Australia.

Furthermore, the critical minerals demand outlook makes a compelling case for accelerating investment in non-Chinese manufacturing capacity. As one industry expert has noted:

NdFeB magnets are not interchangeable with lower-grade alternatives in high-performance applications. The energy product density of sintered NdFeB, measured in megagauss-oersteds (MGOe), can reach values of 50 to 55 MGOe in premium grades, compared to roughly 4 MGOe for ceramic ferrite. This performance gap is why demand is structurally inelastic.

Why Pahang, Malaysia Is the Right Address for This Factory

Malaysia's emergence as a rare earth processing hub is not accidental. The LAMP facility's presence in Kuantan transformed the region into the only location outside China with operating commercial-scale rare earth separation infrastructure. Co-locating magnet manufacturing in the same state builds on this existing cluster rather than starting from zero.

Beyond proximity to feedstock, Malaysia offers several structural advantages for downstream rare earth processing:

-

Established industrial zone infrastructure in Pahang with access to port logistics through the Port of Kuantan

-

A regulatory environment with demonstrated experience processing complex rare earth licensing, given LAMP's multi-year operational history

-

Access to a technically skilled workforce in the chemical processing and advanced manufacturing sectors

-

Strategic positioning within Southeast Asia's broader critical minerals ecosystem, which is attracting increasing investment from Japan, South Korea, the United States, and the European Union

How Malaysia Compares to Other Indo-Pacific Processing Hubs

| Country | Key Initiative | Stage | Strategic Partners |

|---|---|---|---|

| Malaysia | Lynas LAMP refinery + JS Link magnet factory | Operational (refining) / Active development (magnets) | South Korea (JS Link), Australia (Lynas) |

| Japan | JOGMEC-backed rare earth supply diversification | Advanced partnership framework | Multiple producing nations |

| South Korea | Domestic processing push via industrial policy | Planning and early investment | Malaysia, Australia |

| Australia | Mt Weld mining + downstream strategy | Operational (mining), developing (downstream) | Malaysia, United States |

| United States | Domestic processing via IRA provisions | Multiple projects in early stages | Australia, Canada |

What This Means for Lynas's Commercial Evolution

For Lynas shareholders, the JS Link partnership signals a meaningful shift in how the company intends to participate in the rare earth value chain. Historically, Lynas's revenue has been generated primarily through the sale of separated rare earth products, with NdPr oxide being the highest-value output. That model positions Lynas as a commodity seller exposed to spot price volatility in NdPr markets, which have historically been volatile and subject to China's rare earth strategy of pricing influence.

By taking an equity stake in the downstream magnet facility, Lynas gains exposure to value-added margin that sits above the commodity layer. Magnet manufacturers typically earn margins determined by fabrication efficiency, product specification quality, and customer relationships rather than raw material spot prices alone. This structural shift is exactly the kind of vertical integration that analysts have long argued non-Chinese producers need to pursue to escape the commodity price trap.

Lynas has also bolstered its position through record production results alongside this strategic partnership, reinforcing investor confidence in its broader growth trajectory. Lynas CEO Amanda Lacaze has publicly acknowledged that manufacturers globally are actively searching for non-Chinese sources of permanent magnets, and that the commercial opportunity for qualifying supply partners is substantial. The JS Link deal operationalises that thesis.

Key Risks Investors Should Monitor

No capital allocation at this stage of development is without risk. Investors evaluating Lynas's position in this partnership should track the following carefully:

-

Regulatory and environmental permitting timelines in Malaysia, which have historically been subject to community consultation processes around rare earth processing activities

-

JS Link's demonstrated ability to scale from pilot production to commercial volumes, given that this facility represents the company's first large-scale dedicated magnet factory

-

NdFeB magnet pricing dynamics, particularly the risk that Chinese producers respond to new non-Chinese capacity by reducing export prices to undercut emerging competitors

-

NdPr feedstock pricing, which determines the input cost economics for the magnet facility and remains subject to rare earth processing challenges and market cyclicality

-

Geopolitical risk, including the possibility that trade policy shifts, export controls, or diplomatic tensions affect the commercial environment in which the facility operates

Indicative Development Milestones

| Milestone | Status |

|---|---|

| Land acquisition in Pahang | Confirmed |

| Capital commitment (A$50m Lynas equity) | Announced |

| Pilot production by JS Link | Underway |

| Factory construction commencement | Active development phase |

| Equipment installation and commissioning | Pending |

| Ramp to full 3,000 tpa capacity | Target stage |

The next major ASX story will hit our subscribers first

The Geopolitical Dimension That Elevates This Beyond a Commercial Transaction

It would be a mistake to evaluate the Lynas JS Link Malaysian magnet factory deal purely on commercial terms. The geopolitical context surrounding rare earth magnet supply chains has intensified substantially since 2023, with export control actions, trade policy reviews, and critical minerals legislation in the United States, European Union, Japan, and Australia all pointing toward the same conclusion: over-reliance on Chinese magnet supply creates unacceptable strategic risk. Consequently, the energy security risks associated with single-source dependency have moved from theoretical concern to active policy priority.

South Korean industrial expertise is a notable element in this partnership. South Korean manufacturers have developed sophisticated capabilities in precision magnetic materials through their roles as global leaders in consumer electronics, EV battery technology, and advanced manufacturing. JS Link's involvement brings this technical discipline into a facility that will supply markets extending well beyond South Korea.

For defence and advanced technology procurement officers across allied nations, a commercially operating NdFeB sintered magnet facility anchored by non-Chinese rare earth feedstock is not merely commercially interesting. It represents a qualifying supply chain node in an environment where supply chain provenance is increasingly a requirement, not a preference. Indeed, the rare earth processing challenges that have historically constrained non-Chinese producers make this Malaysian facility all the more strategically significant.

Frequently Asked Questions

What is the Lynas JS Link Malaysian magnet factory deal?

It is a partnership between Lynas Rare Earths (ASX: LYC) and South Korean magnet manufacturer JS Link to develop a NdFeB sintered permanent magnet production facility in Pahang state, Malaysia, with a total development budget of RM600 million and a target annual output of 3,000 tonnes.

How much is Lynas investing in the Malaysian magnet factory?

Lynas is contributing approximately A$50 million as an equity investor in the facility.

Where will the factory be built?

The factory is being developed in Pahang state, Malaysia, in strategic proximity to Lynas's existing LAMP refinery in Kuantan.

What type of magnets will the facility produce?

The facility will produce neodymium-iron-boron (NdFeB) sintered permanent magnets, the highest-performance commercial magnet type used in EV motors, wind turbines, industrial robotics, and defence systems.

Is this deal confirmed or still a memorandum of understanding?

The agreement has advanced beyond a non-binding MOU stage. Land acquisition by JS Link is confirmed and development activity is underway, with capital committed by Lynas.

How does this partnership reduce Chinese dominance in magnet supply chains?

By pairing Lynas's non-Chinese NdPr refining output with JS Link's magnet fabrication expertise in a Malaysian facility, the partnership creates an end-to-end NdFeB magnet supply pathway that does not pass through Chinese processing infrastructure at any stage.

Key Takeaways

The Lynas JS Link Malaysian magnet factory deal is significant on multiple simultaneous levels:

-

It represents one of the largest confirmed downstream rare earth manufacturing investments in Malaysia's history at RM600 million total development cost

-

The 3,000 tpa NdFeB sintered magnet production target addresses a critical gap in non-Chinese supply chains for EV, wind energy, and defence applications

-

The co-location strategy in Pahang leverages Lynas's existing LAMP refinery infrastructure, creating genuine supply chain compression rather than geographic fragmentation

-

For Lynas as an ASX-listed company, the equity participation model shifts the business from pure commodity exposure toward value-added margin participation

-

South Korean technical expertise through JS Link adds manufacturing credibility that distinguishes this project from earlier non-Chinese magnet initiatives that remained at the conceptual stage

-

The broader geopolitical context surrounding critical minerals diversification continues to strengthen the commercial case for non-Chinese magnet supply, though investors should monitor execution risk carefully

This article contains forward-looking statements and references to development-stage projects. Readers should conduct their own due diligence and consult qualified financial advisers before making investment decisions. Past performance and project announcements do not guarantee future commercial outcomes.

Want to Track the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly converting complex mineral data into actionable insights for both traders and long-term investors — so start your 14-day free trial today and explore historic discoveries that have generated substantial returns to understand what early positioning in transformative resource plays can mean for a portfolio.