July 1, 2026

The Magnet Gap: Why Western Industry Has Been Exposed for a Decade

For all the policy ambition surrounding critical minerals security, the rare earth supply chain has a specific and largely unresolved vulnerability that sits downstream from mining and processing altogether. It is not about who digs the ore out of the ground, nor even who refines it into separated oxides. The real chokepoint is at the magnet manufacturing stage, and for more than a decade, this step has remained almost entirely concentrated within a single country.

Neodymium iron boron (NdFeB) sintered permanent magnets sit at the intersection of nearly every major clean energy and advanced manufacturing trend of the 21st century. They are the highest-energy-density permanent magnets commercially available, and no substitute material currently matches their performance across the temperature ranges and torque requirements demanded by modern electric vehicle traction motors and offshore wind turbine generators.

The consequence of this concentration is straightforward: without a viable, scaled magnet manufacturing base outside China, all the upstream investment in rare earth mining and processing ultimately feeds back into a Chinese-controlled manufacturing node before reaching the end user.

The Lynas Rare Earths Malaysian magnet factory deal, structured through a long-term partnership with South Korean company JS Link, is designed to directly confront this structural gap. Understanding why it matters requires understanding precisely where the gap exists, what makes NdFeB magnets technically irreplaceable, and what this specific deal architecture does that previous supply chain diversification announcements have not.

When big ASX news breaks, our subscribers know first

Why Processed Rare Earths Without Magnet Manufacturing Solves Only Half the Problem

The Value Chain Bottleneck Most Investors Overlook

Most public discussion of rare earth supply chain risk focuses on mining and processing, but the magnet manufacturing step is where the functional value is actually locked in. A tonne of separated neodymium-praseodymium (NdPr) oxide is an intermediate product. It becomes strategically critical only once it is converted into a sintered magnet with the right coercivity, remanence, and thermal stability characteristics for its end application.

The sintering process for NdFeB magnets is technically demanding. It involves precise alloy formulation, powder milling under inert atmosphere, magnetic field alignment during compaction, vacuum sintering at temperatures around 1,000 to 1,100 degrees Celsius, and post-sinter heat treatment. Chinese manufacturers have refined these processes over decades, creating a knowledge and capital infrastructure advantage that is genuinely difficult to replicate quickly.

This means that a rare earth producer which only mines and processes material, without a downstream magnet manufacturing partner or equity stake, remains a commodity supplier. Its customers, if they are Western manufacturers, must still route their magnet procurement through a Chinese supply chain. The Lynas Rare Earths Malaysian magnet factory deal disrupts this dependency by co-locating an NdFeB sintering operation with Lynas' existing processing infrastructure in Kuantan, Pahang.

The structural innovation here is not the existence of a magnet plant, but its geographic integration with a rare earth processing facility, eliminating the cross-border material transfer that has historically funnelled processed oxides back through Chinese manufacturing.

China's Dominance: Scale and Context

China currently accounts for an estimated 85 to 90 percent of global NdFeB magnet production, according to assessments by bodies including the International Energy Agency and the United States Geological Survey. Furthermore, this concentration is not solely the result of resource endowment. China's dominance in magnet manufacturing developed through sustained state industrial policy, technology transfer, and the construction of vertically integrated production clusters over multiple decades.

The consequence is that Western EV manufacturers, wind turbine producers, and defence contractors are structurally exposed to a single-source dependency for one of the most performance-critical components in their products. China's export restrictions on rare earth processing technologies and certain precursors in recent years have sharpened this risk considerably, accelerating demand for credible alternative production nodes.

Deal Architecture: The Lynas Rare Earths Malaysian Magnet Factory Partnership Explained

Financial Structure and Key Terms

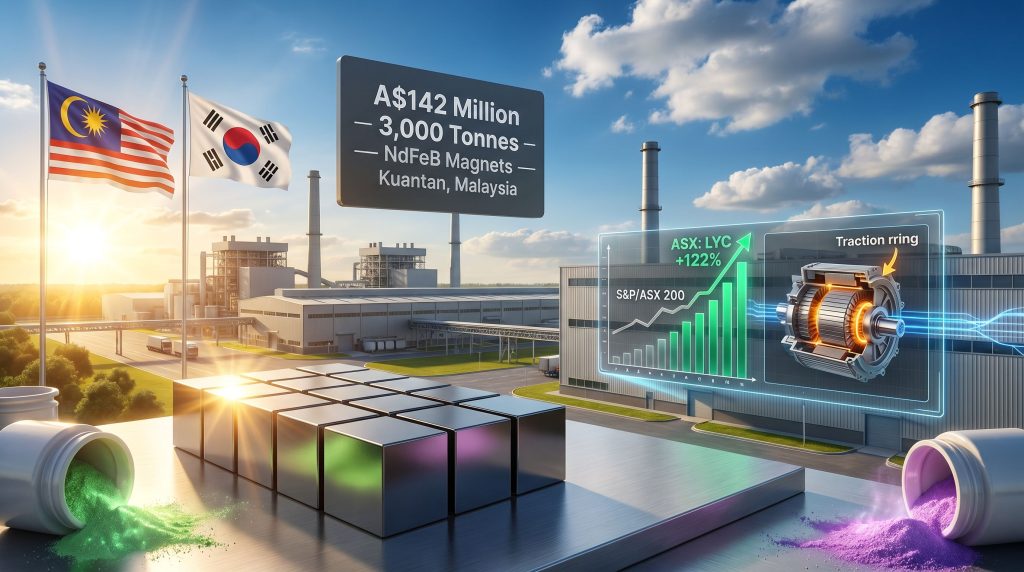

The Lynas Rare Earths Malaysian magnet factory deal involves a total project investment of approximately A$142 million, equivalent to roughly RM600 million. The specific financial and operational terms confirmed in the ASX announcement are as follows:

| Deal Component | Confirmed Detail |

|---|---|

| Total Project Value | A$142 million (approx. RM600 million) |

| Lynas Equity Investment | A$50 million in ordinary equity of JS Link |

| Resulting Ownership Stake | Approximately 4.58% of JS Link |

| Escrow Period on Lynas Equity | 3 years |

| Exclusive Supply Agreement Duration | Until January 2038 |

| Planned Annual Production Capacity | 3,000 tonnes of NdFeB sintered magnets |

| Projected Employment Creation | Up to 400 jobs in Malaysia |

Lynas will serve as the exclusive rare earth material supplier to JS Link's facilities in both South Korea and Malaysia through to January 2038. This creates a long-duration, captive demand structure that underpins Lynas' revenue visibility in its downstream segment while simultaneously giving JS Link supply certainty from a non-Chinese source.

The three-year escrow applied to Lynas' equity stake is a notable structural feature. It signals a commitment horizon that extends well beyond a conventional commercial agreement and aligns Lynas' capital at risk with the expected construction and ramp-up timeline for the facility.

Why Kuantan Is the Right Location

The decision to build the magnet factory in Kuantan, Pahang, adjacent to Lynas' existing Lynas Advanced Materials Plant (LAMP), reflects deliberate operational logic rather than geographic convenience alone.

- Logistics elimination: Processed rare earth oxides and metals produced at LAMP can transfer directly to the magnet facility without cross-border transport, reducing cost, lead time, and supply chain exposure.

- Existing infrastructure: LAMP represents years of capital investment in utilities, environmental systems, workforce development, and regulatory relationships that a greenfield site in another jurisdiction would need to replicate from scratch.

- Land acquisition confirmed: The Malaysian government has confirmed land acquisition for the JS Link facility is already complete, placing the project materially beyond a preliminary memorandum of understanding.

- Ten-year operating licence: Lynas holds an extended operating licence for its Malaysian processing operations, providing the regulatory stability necessary to justify long-term downstream investment alongside the plant.

JS Link's Manufacturing Credentials

JS Link brings established magnet manufacturing capability to the partnership, with existing operational plants in both South Korea and Malaysia. This is not a startup venture entering the NdFeB space for the first time. The combination of JS Link's magnet manufacturing process knowledge with Lynas Rare Earths' processing expertise and material supply creates a value chain integration that neither party could achieve independently at this scale and speed.

South Korea's position as a major hub for electric vehicle battery manufacturing and consumer electronics creates natural downstream demand for locally or regionally sourced NdFeB magnets, giving the Korea-Malaysia corridor a logical market anchor.

The Technical Significance of NdFeB Sintered Magnets

Why These Magnets Cannot Be Substituted

NdFeB sintered magnets are commercially irreplaceable across a specific set of high-performance applications for reasons grounded in fundamental materials science. Their energy product, measured in megajoules per cubic metre, exceeds that of samarium cobalt, ferrite, and alnico magnets by a significant margin. In applications where weight, volume, and magnetic field intensity are simultaneously constrained, NdFeB is the only practical solution.

Key application areas for the output of the Kuantan facility include:

- Electric vehicle traction motors: Each EV typically requires approximately 1 to 2 kilograms of NdFeB magnets. At projected global EV production volumes, this represents a rapidly scaling demand source.

- Direct-drive offshore wind turbines: Large offshore turbines using permanent magnet generators can require up to 2 tonnes of NdFeB magnets per unit, making wind energy one of the highest-volume demand drivers per installation.

- Consumer electronics and robotics: Hard disk drives, premium audio systems, industrial servo motors, and the rapidly growing robotics sector all depend on NdFeB magnets.

- Defence and aerospace: Guidance systems, radar equipment, and precision actuators in military applications require high-specification sintered magnets with controlled magnetic properties.

The Heavy Rare Earth Dimension: A Less Understood Requirement

A nuance that is frequently overlooked in mainstream supply chain coverage is the distinction between standard-grade and high-coercivity NdFeB magnets. In applications where motors operate at elevated temperatures, such as EV traction motors or industrial drives, a standard NdFeB alloy will suffer significant irreversible demagnetisation unless heavy rare earth elements are added to the grain boundaries.

Dysprosium (Dy) and terbium (Tb) are the two critical heavy rare earth additions that solve this problem. They are incorporated using grain boundary diffusion or alloy additions to dramatically improve the coercive force of the magnet at high operating temperatures. Without access to a secure dysprosium and terbium supply, a magnet manufacturer cannot produce the high-specification grades required by automotive and industrial customers.

This is where Lynas' parallel investment of approximately RM500 million to establish heavy rare earth production at its Malaysian operations becomes strategically critical. If delivered on the targeted timeline of 2025 to 2026, it would position Lynas as a full-spectrum rare earth input supplier, capable of providing both the light rare earths (neodymium, praseodymium) and the heavy rare earths (dysprosium, terbium) required for premium magnet grades. Very few non-Chinese entities can credibly claim this combination.

It is worth noting that heavy rare earth supply is even more geographically concentrated than light rare earth supply, with production overwhelmingly sourced from ionic clay deposits in southern China. A non-Chinese dysprosium and terbium production capability at commercial scale would represent a genuinely differentiated strategic asset.

Lynas' "Towards 2030" Strategy: From Processor to Supply Chain Architect

What Vertical Integration Actually Means in This Context

The language of vertical integration is used broadly in mining investment analysis, but its meaning in the rare earth context is specific and worth unpacking. In this case, vertical integration does not mean Lynas is building its own magnet factory. Instead, it is constructing a value chain position through equity ownership, exclusive long-term supply agreements, and geographic co-location that gives it economics, optionality, and strategic relevance at the downstream manufacturing stage without taking on the full capital and operational complexity of magnet sintering itself.

This structure reflects a sophisticated approach to value chain participation. Lynas retains its core competency in rare earth processing, while its equity stake in JS Link and the exclusive supply agreement provide exposure to the higher-value magnet market without the execution risk of building and operating a sintering facility in-house. Consequently, this positions the company as a genuine supply chain architect rather than simply a commodity processor.

Regulatory Clarity as a Foundation for Long-Term Investment

A structural precondition for any serious downstream investment in Malaysia was resolution of the regulatory uncertainty that had previously surrounded Lynas' operating licence. The extension of that licence for a further ten years, subject to the condition that radioactive waste production ceases by 2031 through thorium extraction methodologies, removes the overhang that had made long-horizon capital commitments to the Malaysian operations difficult to justify.

This condition is technically achievable. Thorium is a naturally occurring by-product of rare earth processing from monazite-bearing ores, which characterise the Mount Weld deposit that supplies Lynas' Malaysian operations. Establishing a thorium extraction and storage solution by 2031 is a defined engineering challenge with a known solution pathway, rather than an open-ended regulatory risk.

Lynas Share Price Performance

Over the twelve months preceding the announcement of the Lynas Rare Earths Malaysian magnet factory deal, shares in Lynas Rare Earths (ASX: LYC) rose approximately 122%, compared with a gain of approximately 3% for the S&P/ASX 200 Index over the same period. This 119-percentage-point outperformance reflects both favourable rare earth pricing dynamics and growing investor recognition of Lynas' strategic positioning as the most advanced non-Chinese integrated rare earth company globally.

Investment Considerations: What Informed Investors Should Monitor

Key Project Milestones and Catalysts

For investors tracking this deal as a medium-term value driver, the following milestones represent the most important near-term catalysts:

- Groundbreaking and construction commencement at the Kuantan site, which would confirm the transition from announced partnership to active construction.

- Commissioning timeline for the initial production phase of the 3,000 tpa facility.

- Ramp-up trajectory to nameplate capacity, which will determine the timing of downstream revenue contribution.

- Heavy rare earth production commencement from the separate RM500 million dysprosium/terbium investment, targeted for 2025 to 2026.

- Customer offtake announcements from automotive, wind energy, or electronics manufacturers securing supply from the Kuantan facility.

Scenario Analysis

Factors that could accelerate project outcomes:

- EV adoption rates exceeding current projections, pulling forward critical minerals demand ahead of the facility's ramp-up schedule

- Further Chinese export restrictions on rare earth materials or processing technology, increasing the market premium for non-Chinese magnet supply

- Additional strategic partnerships or supply agreements announced alongside the JS Link deal

Factors that could create headwinds:

- Construction delays or cost overruns at the Kuantan site, given the complexity of commissioning a precision manufacturing facility

- Rare earth price volatility, particularly for NdPr, compressing margins on the exclusive supply arrangement

- Technical challenges in meeting the heavy rare earth production timeline, which could limit the range of magnet grades Lynas can supply to JS Link

The three-year escrow applied to Lynas' A$50 million equity stake in JS Link effectively locks in this investment through approximately 2028 to 2029, which aligns with the expected window for the facility to reach meaningful production levels. Investors should treat this as a medium-horizon capital commitment with a defined timeframe, rather than a near-term earnings catalyst.

The next major ASX story will hit our subscribers first

Malaysia's Emerging Role as a Critical Minerals Manufacturing Hub

Competitive Positioning Against Alternative Jurisdictions

Malaysia's candidacy as a rare earth and magnet manufacturing hub rests on a combination of existing infrastructure, geographic proximity to Asian end markets, and an established rare earth processing track record that no other non-Chinese jurisdiction currently matches at equivalent scale. Furthermore, its energy transition security credentials are strengthened by the confirmed land acquisition and operational licence clarity already in place.

| Factor | Malaysia (Kuantan) | Alternative Western Jurisdictions |

|---|---|---|

| Existing rare earth processing infrastructure | Operational (LAMP facility) | Limited or pre-development |

| Proximity to Asian EV/electronics manufacturers | High | Low to medium |

| Land acquisition status for JS Link facility | Confirmed | Not applicable |

| Rare earth operating licence clarity | 10-year extension confirmed | Variable |

| Established manufacturing workforce | Present | Developing |

| Co-location with NdFeB magnet facility | Confirmed (JS Link) | Not yet achieved |

The Korea-Malaysia Manufacturing Corridor

The dual-country operational footprint of JS Link, spanning South Korea and Malaysia, creates a manufacturing corridor with natural synergies. South Korea's dominance in EV battery production and consumer electronics generates substantial domestic demand for high-performance magnets. Serving this demand from a co-located Malaysian production facility, supplied with non-Chinese rare earths, is an arrangement that aligns well with South Korea's own stated objectives around supply chain diversification.

This Korea-Malaysia axis could become a template for other non-Chinese magnet manufacturing partnerships, particularly as Japanese and European automotive manufacturers also seek to reduce their exposure to Chinese magnet supply. The Malaysian magnet plant development, moreover, reflects broader regional ambitions to position Southeast Asia as a credible hub within the global rare earth geopolitics landscape, as explored in assessments of rare earth geopolitics more broadly.

FAQ: Lynas Rare Earths Malaysian Magnet Factory Deal

What is the Lynas Rare Earths Malaysian magnet factory deal?

Lynas Rare Earths has entered a long-term partnership with South Korean company JS Link to construct a 3,000-tonne-per-annum NdFeB sintered magnet manufacturing facility in Kuantan, Malaysia. The total project investment is approximately A$142 million, with Lynas contributing A$50 million for an approximately 4.58% equity stake in JS Link. Lynas will exclusively supply rare earth materials to JS Link's Korean and Malaysian facilities until January 2038.

Where will the factory be located and why does it matter?

The factory will be built in Kuantan, Pahang, directly adjacent to Lynas' existing LAMP processing facility. This co-location eliminates the cross-border material transfer step that has historically routed processed rare earth materials through Chinese manufacturing before reaching end users.

What products will the factory make?

The facility will produce NdFeB sintered permanent magnets for use in electric vehicle motors, wind turbines, consumer electronics, and defence applications, targeting customers in South Korea, Malaysia, and broader Asian and Western markets.

What is the significance of dysprosium and terbium to this project?

High-performance NdFeB magnets for EV and industrial applications require heavy rare earth additions, specifically dysprosium and terbium, to maintain magnetic performance at elevated temperatures. Lynas is separately investing approximately RM500 million to establish domestic heavy rare earth production in Malaysia, targeting delivery by 2025 to 2026, which would give it the capacity to supply the full input spectrum for premium magnet grades.

How has the Lynas share price performed?

Over the twelve months preceding the announcement, Lynas Rare Earths (ASX: LYC) shares rose approximately 122%, substantially outperforming the S&P/ASX 200 Index, which gained approximately 3% over the same period.

This article contains general information only and does not constitute financial advice. Investments in ASX-listed securities carry risk, including the potential for capital loss. Past share price performance is not indicative of future returns. Forecasts, timelines, and production targets discussed in this article are subject to change based on construction progress, market conditions, and regulatory developments. Readers should seek independent financial advice before making investment decisions.

Want To Identify the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex mineral data into actionable insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.