June 30, 2026

The Geology of Strategic Advantage: Why Heavy Rare Earth Deposits Demand a Different Lens

Most investors approaching the rare earth sector reach instinctively for a single screening metric: total rare earth oxide grade. It is a natural impulse, borrowed from the logic of gold and base metal investing, where higher grade almost universally signals higher value. But in rare earths, this instinct can lead to a fundamental misreading of which deposits actually matter strategically and which are merely abundant in elements with limited industrial application.

The distinction between light rare earth elements and heavy rare earth elements is not a matter of marketing terminology. It reflects a genuine divide in industrial criticality, processing complexity, and geopolitical scarcity. Dysprosium and terbium, the two most commercially significant heavy rare earths, are essential additives in neodymium-iron-boron permanent magnets. Without them, the thermal stability of those magnets degrades sharply, making them unsuitable for the high-temperature operating environments of electric vehicle drive motors and direct-drive wind turbines. There is no commercially viable substitute for these elements in high-performance magnet applications at scale.

Understanding this context is the essential prerequisite for understanding why the granting of a 25-year exploitation concession over the Norra Kärr deposit in southern Sweden carries significance well beyond a single company's permitting milestone. The Norra Karr mining lease Sweden represents one of the most consequential permitting decisions in European critical mineral development in recent years.

When big ASX news breaks, our subscribers know first

What Makes Norra Kärr Geologically Distinct From Other Rare Earth Deposits

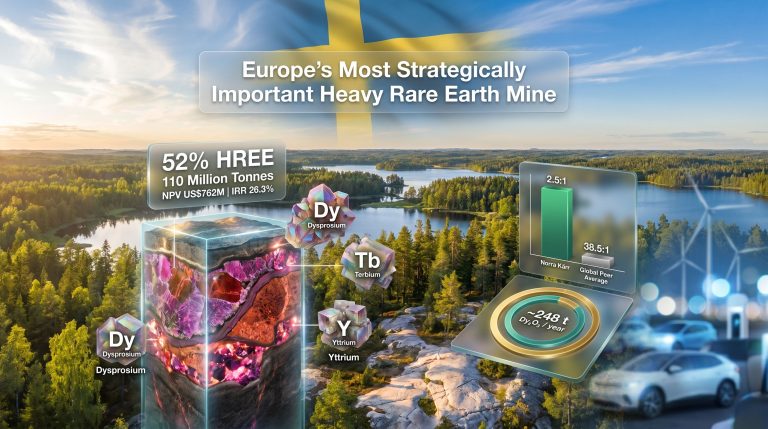

The Norra Kärr deposit is hosted within a body of eudialyte-group mineralisation in Jönköping County, southern Sweden. Eudialyte is a sodium zirconium silicate mineral that, in certain geological settings, incorporates elevated concentrations of heavy rare earth elements into its crystal structure. This is the key to Norra Kärr's anomalous HREE profile.

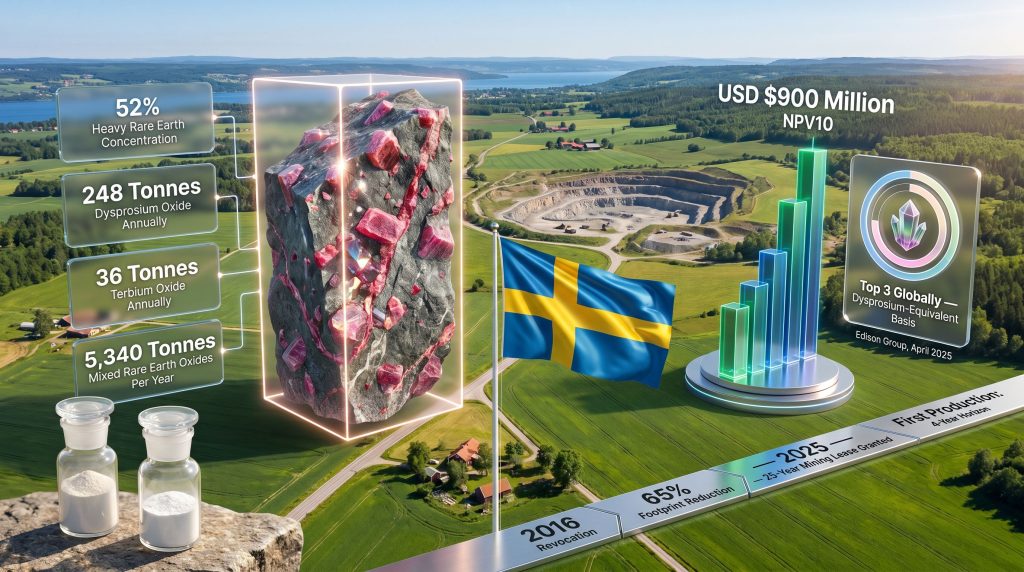

Where a conventional rare earth deposit, including many of the largest deposits in China's Bayan Obo complex and many Australian and Canadian projects, derives the overwhelming majority of its rare earth content from light elements such as lanthanum, cerium, praseodymium, and neodymium, Norra Kärr presents an inverted profile. Approximately 52% of the deposit's total rare earth content is concentrated in heavy rare earth elements, with the balance comprising light rare earths and mid-rare earths.

When ranked on a dysprosium-equivalent basis, which recalculates total rare earth content by weighting each element according to its relative market value and strategic importance rather than its raw abundance, Norra Kärr positions among the top three deposits globally. This is a calculation that standard TREO grade comparisons entirely obscure. A deposit with 8% TREO but 50% HREE concentration can be dramatically more valuable than a deposit with 12% TREO but only 5% HREE content, yet the latter will consistently attract more initial investor attention because the headline grade is higher.

Prior feasibility modelling indicates that a producing Norra Kärr operation could generate:

- Approximately 5,340 tonnes of mixed rare earth oxides per year

- 248 tonnes of dysprosium oxide annually

- 36 tonnes of terbium oxide annually

- A production life of 26 years

These output figures place the project in a category of global strategic relevance, not merely regional interest. For context, global dysprosium supply is extremely concentrated, with the overwhelming majority originating from Chinese ionic clay deposits and primary mining operations in China's Jiangxi and Fujian provinces. Detailed rare earth supply chains analysis confirms just how structurally exposed Western manufacturers remain to this concentration risk.

The operational model at Norra Kärr is also materially simpler than conventional underground rare earth mining. The deposit lends itself to quarry-style extraction, involving surface excavation, crushing, grinding, and on-site mineral separation to produce a heavy rare earth-rich concentrate. This concentrate would then be transported to a separate downstream hydrometallurgical facility for further processing. The absence of deep underground infrastructure significantly constrains the environmental footprint of the operation.

The 25-Year Exploitation Concession: Legal Meaning and Regulatory Context

What the Concession Actually Grants

Under Swedish mining law, an exploitation concession is a fundamentally different instrument from an exploration licence. An exploration licence permits geological investigation and sampling but confers no right to extract mineralisation commercially. An exploitation concession, by contrast, grants the legal right to mine the deposit itself. It is the foundational instrument upon which all subsequent permitting, financing, and commercial agreements must be built.

The 25-year exploitation concession granted to Leading Edge Materials through its Swedish subsidiary, Greenna Mineral AB, represents the culmination of more than 15 years of continuous technical development spanning geological, geotechnical, metallurgical, hydrogeological, and environmental disciplines. The concession was granted following formal assessment by the county administrative boards, a recommendation from the Swedish Mining Inspectorate (Bergsstaten), and a final decision by the Swedish government.

A Regulatory Journey Spanning Two Decades

The path to this concession was not linear. The project encountered a significant reversal in 2016 when an earlier concession application was overturned on environmental and land-use grounds. Rather than abandoning the project, the development team undertook a comprehensive redesign that reduced the operational surface footprint by 65% and reconfigured the extraction methodology to align with a quarrying rather than conventional open-pit or underground mining model.

This redesign was not merely cosmetic. It produced a fundamentally different project with a materially reduced environmental impact profile, and it is this revised project that successfully completed the regulatory assessment process in 2025.

| Milestone | Detail |

|---|---|

| Project geological inception | Early 2000s surveys |

| 2016 concession revocation | Original application overturned on environmental grounds |

| Project redesign completed | Operational footprint reduced by 65%; quarry model adopted |

| Mining Inspectorate endorsement | Formal recommendation supporting strategic importance |

| Swedish government concession grant | 25-year exploitation concession issued |

| Immediate share price response | Approximately 28% uplift post-announcement |

From Permitting Story to Investable Asset: The De-Risking Effect on Commercial Negotiations

Why the Absence of a Mining Lease Was a Commercial Ceiling

There is a specific dynamic in mining project development that is often underappreciated by generalist investors: permitting milestones are not merely administrative checkboxes. They are the prerequisites for an entirely different quality of commercial conversation. Without a mining lease, any discussion with potential offtake partners, lenders, or strategic investors carries an implicit asterisk.

The project may be geologically important, technically well-developed, and strategically irreplaceable, but it remains contingent on a decision outside the company's control. Prior to the concession grant, Leading Edge Materials could position Norra Kärr as one of Europe's most strategically significant heavy rare earth assets at industry forums. However, the absence of the mining lease created an immediate perception of risk in any downstream conversation, regardless of the project's geological merits.

The moment that framing shifted from a project awaiting a government decision to a permitted, 25-year-concession-backed asset, the nature of every commercial discussion changed. This is particularly significant for downstream offtake negotiations, where companies manufacturing permanent magnets, electric vehicle motors, and wind turbine generators face their own supply chain security imperatives. A mining lease is typically the minimum permitting threshold that gives downstream counterparties the confidence to progress toward binding offtake terms.

Independent Valuation: What the Numbers Suggest

Independent research completed in April 2025 produced a risk-adjusted NPV10 valuation of approximately USD $900 million on a 50% risk-weighted basis. This figure represents a significant recalibration from the 2015 Pre-Feasibility Study, and the most important driver of that revision is not a change in the project's geology — it is a structural shift in rare earth pricing.

The emergence of a bifurcated global pricing structure for dysprosium and terbium is among the most consequential market developments in the rare earth industry over the past two years. China's rare earth strategy of applying export restrictions on heavy rare earth elements has created a divergence between Chinese domestic prices and ex-China market prices. Furthermore, for years, original equipment manufacturers were effectively required to price non-Chinese rare earth supply against the Chinese domestic benchmark — a benchmark that reflected a heavily subsidised and state-managed supply chain. That pricing discipline has now broken down.

OEM manufacturers seeking dysprosium and terbium supply outside China are demonstrating willingness to pay prices that reflect actual market availability rather than Chinese domestic benchmarks, fundamentally altering the economics of non-Chinese HREE projects.

This pricing bifurcation is not merely cyclical. It reflects a structural reconfiguration of global rare earth markets driven by geopolitical friction and deliberate supply chain policy by multiple nation-states. Projects like Norra Kärr that were previously evaluated against an artificially suppressed Chinese pricing floor are now being reassessed against a fundamentally different commercial reality.

It is important to note that the April 2025 independent valuation was completed before the formal mining lease grant, meaning the 50% risk weighting applied to the NPV calculation does not yet reflect the de-risking effect of the concession itself. The updated Pre-Feasibility Study, currently in progress, will incorporate revised pricing assumptions, updated capital and operating cost estimates, and the confirmed project design.

Norra Kärr vs. Typical Light REE Projects: A Comparison

| Metric | Norra Kärr | Typical Light REE Deposit |

|---|---|---|

| HREE as % of Total REE | ~52% | Less than 10% |

| Dysprosium-equivalent global ranking | Top 3 globally | Not applicable |

| Operational model | Quarry plus mineral separation | Variable |

| Jurisdiction | Sweden (EU member state) | Variable |

| Concession status (2025) | 25-year mining lease granted | Variable |

| Modelled annual dysprosium oxide output | ~248 tonnes | Minimal |

The Development Roadmap: Environmental Permitting, PFS, and the Path to Production

Environmental Permitting: The Next Regulatory Hurdle

The exploitation concession is a necessary but not sufficient condition for production. A separate environmental permit application must be prepared and submitted, addressing the specific operational activities, land use interactions, water management, and potential environmental impacts associated with the quarrying and mineral separation operations.

The preparation of that application is estimated to require between 6 and 9 months of baseline data collection and technical documentation. Critically, this environmental permitting process can be run in parallel with the ongoing Pre-Feasibility Study update, compressing the overall development timeline rather than sequencing these workstreams consecutively.

Sweden's regulatory framework is also evolving in ways that may benefit project timelines. The Swedish government has initiated a reform process aimed at consolidating environmental permitting under a single authority with the specialist competence to assess mining and mineral processing applications efficiently. This structural reform, while still in progress, reflects a policy orientation toward improving the speed and predictability of the permitting process for economically significant projects.

The quarry-based operational model at Norra Kärr is relevant here. Because the on-site activities are limited to excavation, crushing, grinding, and mineral separation, the environmental impact profile is comparatively constrained relative to underground mining operations or projects involving on-site hydrometallurgical processing. Downstream processing will be conducted at a separate, purpose-selected industrial facility, with permitting for that activity expected to benefit from existing industrial zoning and regulatory familiarity with analogous process chemistries.

Four-Year Production Horizon: Key Development Milestones

- 2025 (H2): Environmental permit application preparation commences; PFS update progresses in parallel; offtake partner negotiations advance following concession grant

- 2026: Environmental permit application submitted to relevant authority; updated PFS completed; strategic project designation application under EU Critical Raw Materials Act under consideration

- 2027: Environmental permit decision anticipated; project financing discussions with institutional lenders commence; binding offtake agreements targeted

- 2028-2029: Construction and commissioning; first production targeted within four-year horizon from concession grant

The four-year timeline to production is ambitious but not without precedent in comparable jurisdiction-safe, well-documented mining projects. Its achievability is contingent on concurrent progress across environmental permitting, PFS completion, offtake agreements, and project financing, with each workstream reinforcing the others in terms of investor and institutional confidence. The rare earth processing challenges inherent in eudialyte mineralisation, however, remain a technical variable that the updated PFS will need to address in detail.

The Geopolitical Backdrop: Why China's Export Restrictions Are Restructuring HREE Markets

A Two-Tier Pricing World

China's dominance in rare earth processing is not a recent development. It has been built over three to four decades of deliberate state-directed investment in mining, separation, alloying, and magnet manufacturing capacity. What has changed materially in recent years is China's willingness to use that dominance as an active instrument of trade and geopolitical policy.

Export restrictions targeting dysprosium, terbium, and other critical heavy rare earth elements have created the bifurcated pricing structure described above, but their effect goes beyond pricing. They have fundamentally altered the risk calculus of every OEM that depends on these materials. Supply security has moved from a procurement consideration to a boardroom strategic priority. The willingness to pay a premium for permitted, jurisdiction-safe, non-Chinese supply has increased accordingly.

For the Norra Karr mining lease Sweden project, situated within the European Union and capable of producing dysprosium and terbium at industrial scale, this geopolitical context represents a structural commercial tailwind rather than a transient pricing cycle.

US Capital Is Moving Faster Than European Capital

One of the more striking dynamics in the current rare earth investment landscape is the pace differential between American and European capital deployment. US-backed entities are actively acquiring European rare earth supply chain infrastructure at a rate that has caught many European policymakers off-guard.

Energy Fuels' acquisition of VAC (Vacuumschmelze), a German advanced magnet alloy manufacturer, for approximately USD $1.9 billion represents one of the largest recent transactions in rare earth supply chain consolidation. USA Rare Earth's acquisition of Less Common Metals in the UK and its stake in a French separation facility represents another vector of American capital entering European rare earth infrastructure.

The paradox is stark: American strategic capital is securing European rare earth processing and alloying capacity at considerable speed, while European public financing institutions have generally required projects to reach prefeasibility-level documentation before committing risk capital. The European Investment Bank, for instance, requires feasibility-level technical documentation as a threshold condition for capital deployment, creating a structural funding gap for projects in the development phase that precedes that documentation.

The MP Materials precedent, where US government equity participation catalysed subsequent private bank lending at scale, represents a capital formation model that Europe has not yet replicated in the rare earth sector.

France represents a partial exception, with state-affiliated investment vehicles demonstrating more proactive participation in critical mineral supply chain development. However, at the EU level, the gap between policy ambition and actual risk capital availability for junior mining projects developing strategically important assets remains acute. In this context, European critical raw materials policy is struggling to bridge the divide between legislative ambition and practical capital deployment.

The next major ASX story will hit our subscribers first

EU Strategic Project Designation: Potential Benefits and Realistic Expectations

What the CRMA Strategic Project Framework Offers

The EU Critical Raw Materials Act, which entered into force in 2024, establishes a strategic project designation framework intended to accelerate the development of domestically significant mineral projects. The two primary benefits associated with designation are expedited permitting timelines and facilitated access to public capital instruments.

Projects applying for strategic status are assessed against criteria including their contribution to EU supply chain resilience, their technical viability, and their permitting progress. The granting of a 25-year mining lease materially strengthens any application by demonstrating that the project has cleared the most significant legal threshold in its development pathway. Furthermore, among Europe's strategic metals projects, Norra Kärr stands out for its combination of geological distinctiveness and advanced permitting status.

However, it is important to apply a degree of analytical realism to the strategic project framework. Early-designation projects have not universally experienced the expedited permitting or capital access benefits that the framework promised at inception. The framework's practical effectiveness is still being established, and the gap between policy intent and operational delivery remains a genuine variable.

The Three-Part De-Risking Stack

For Norra Kärr, the most powerful near-term value catalyst is likely the assembly of a three-part de-risking combination:

- Mining lease (now granted): establishes legal right to extract

- Binding offtake agreement: demonstrates commercial demand and provides revenue visibility for lenders

- Completed Pre-Feasibility Study: provides the technical documentation required by institutional financing sources

Each element of this stack reinforces the others. A binding offtake agreement becomes significantly easier to negotiate from a position of having a 25-year mining lease. A completed PFS with revised pricing assumptions reflecting the current ex-China market environment provides lenders with the documentation they require. Strategic project designation, if pursued, adds a further layer of institutional credibility to the combination.

Key Questions Investors Are Asking About Norra Kärr

What does the mining lease actually change commercially?

Before the concession grant, commercial discussions with potential offtake partners operated under a structural constraint: every conversation about securing dysprosium and terbium supply was implicitly conditional on a government decision that had not yet been made. That constraint has been removed. The project can now be presented to downstream counterparties as a permitted, 25-year-concession-backed asset with defined production parameters, which is a categorically different commercial proposition.

Why does the HREE concentration matter so much?

Standard rare earth project screening using TREO grade systematically undervalues deposits like Norra Kärr because it aggregates elements of vastly different strategic and commercial significance into a single number. Lanthanum and cerium, which are abundant and relatively low-value, can dominate a high-TREO figure while contributing little to a project's commercial viability. Dysprosium and terbium, present in small absolute quantities but commanding significant market premiums and carrying irreplaceable functional roles in permanent magnets, can be decisive to a project's economic and strategic value even at modest absolute grades. The dysprosium-equivalent ranking methodology corrects for this distortion.

What are the primary risks to the four-year production timeline?

The timeline depends on several concurrent workstreams each progressing without significant delay. Environmental permitting timelines in Sweden are subject to regulatory process considerations outside the company's direct control, though the simplified operational model and the ongoing Swedish government reform of environmental permitting administration are both factors that work in the project's favour. Capital availability for the construction phase remains the most structurally uncertain variable, given the broader gap between European policy ambition and practical risk capital deployment for junior mining projects.

The Investment Case in Context: What Norra Kärr Represents at This Stage of Development

The transition from permitting story to investable asset is a well-understood concept in mining investment, but it is rarely as cleanly delineated as it is in the Norra Karr mining lease Sweden case. The 25-year exploitation concession does not merely reduce one risk item on a project checklist. It fundamentally changes the nature of the asset being offered to investors, lenders, and commercial counterparties.

Several converging factors give this particular milestone unusual weight:

- The structural shift in ex-China heavy rare earth pricing has materially improved project economics relative to the 2015 baseline assumptions

- Chinese export restrictions on dysprosium and terbium have elevated the strategic premium attached to permitted, jurisdiction-safe HREE supply

- US capital is actively deploying into European rare earth infrastructure, suggesting that strategic investor interest in EU-jurisdiction HREE assets is building from multiple geographic directions

- The Swedish government's permitting reform agenda and its recognition of rare earth supply security as a policy priority provide a constructive regulatory environment for the next development phase

- The deposit's top-three global ranking on a dysprosium-equivalent basis is a geological characteristic that is not replicable through exploration investment in most other jurisdictions

Investor note: All forward-looking statements, production timelines, valuation estimates, and commercial projections discussed in this article involve uncertainty and should not be construed as financial advice. Independent financial and technical advice should be sought before making any investment decision. The NPV estimates referenced are based on assumptions that may change materially as updated feasibility work is completed.

What the Norra Karr mining lease Sweden ultimately represents at this moment in its development history is a rare convergence: a geologically irreplaceable asset, in a politically stable and mining-friendly jurisdiction, that has cleared the most significant legal milestone in its path to production, at precisely the moment when the strategic and commercial case for European heavy rare earth supply has never been stronger. Consequently, this alignment of geological quality, regulatory progress, and geopolitical tailwinds may not be replicated elsewhere in the European critical mineral landscape for some considerable time.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential opportunities across critical minerals and rare earths — turning complex data into clear, actionable insights for investors at every level. Explore how historic mineral discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to secure your market-leading advantage.