August 1, 2026

The rare earth elements sector has emerged as a critical component of modern supply chains, with critical minerals energy transition demands accelerating globally. Lynas Rare Earths stock analysis reveals a company uniquely positioned at the intersection of geopolitical necessity and technological innovation. Understanding investment opportunities requires examining how supply chain vulnerabilities create systematic risks that extend far beyond traditional commodity cycles.

Understanding Lynas' Market Position in the Global Rare Earths Landscape

The rare earth elements sector operates within a unique supply-demand paradigm where processing capabilities matter more than mining capacity. Furthermore, China's dominance in rare earth processing reaches approximately 85-90% of global separated rare earth oxide production, according to U.S. Geological Survey data. This concentration creates strategic vulnerabilities for Western technology manufacturers, defense contractors, and clean energy developers.

The Non-China Supply Chain Advantage

Lynas operates across two primary processing jurisdictions, providing comprehensive separation capabilities that compete directly with Chinese processors. The Mt Weld facility in Western Australia extracts rare earth ore containing approximately 50% REO content, while the Kalgoorlie processing plant separates mixed rare earth oxides into individual elements.

Additionally, the company's Malaysian facility in Kuantan processes both light and heavy rare earth elements. The strategic value extends beyond simple supply diversification, as Western governments increasingly mandate non-Chinese sourcing for defense applications. Consequently, this creates premium pricing opportunities for qualified suppliers, with the U.S. Department of Energy's 2022 strategy document explicitly identifying rare earth supply chain resilience as essential to national security objectives.

Moreover, the development of strategic minerals reserve initiatives across multiple jurisdictions supports sustained demand for non-Chinese supply sources. The critical minerals executive order framework further emphasises the strategic importance of diversified supply chains.

Critical Materials for the Energy Transition

NdPr (Neodymium-Praseodymium) represents the highest-value component of Lynas' production portfolio, commanding current prices of US$111 per kilogram compared to the H1 FY26 average of US$74. This 50% price appreciation reflects genuine supply-demand tightening rather than speculative activity.

Electric vehicle applications drive substantial NdPr demand growth. Each EV motor requires 0.5-2 kilograms of permanent magnet material containing high concentrations of neodymium and praseodymium. With global EV sales reaching 14 million units in 2024 and projected to exceed 20 million by 2030, annual NdPr demand from automotive applications alone approaches 28,000 tonnes at current penetration rates.

Wind energy applications create additional demand pressure. Direct-drive wind turbines utilise 200-600 kilograms of permanent magnet material per 5-10 MW installation. Global wind capacity additions of approximately 75 GW annually translate into substantial rare earth consumption, particularly for offshore installations where permanent magnet generators offer superior reliability.

Heavy rare earth production provides Lynas with access to premium markets. Dysprosium and terbium command 3-5x pricing premiums versus light rare earths due to supply scarcity and critical applications in high-performance magnets. Current dysprosium oxide pricing approximates US$200-250 per kilogram, while terbium oxide reaches US$800-1,000 per kilogram.

When big ASX news breaks, our subscribers know first

How Strong Are Lynas' Latest Financial Results?

Financial performance analysis reveals Lynas executing on multiple growth vectors simultaneously while managing operational challenges that temporarily impacted earnings delivery. The company's financial transformation demonstrates the impact of mining industry evolution on traditional resource companies.

Revenue Growth Analysis

| Metric | H1 FY25 | H1 FY26 | Change | Growth Rate |

|---|---|---|---|---|

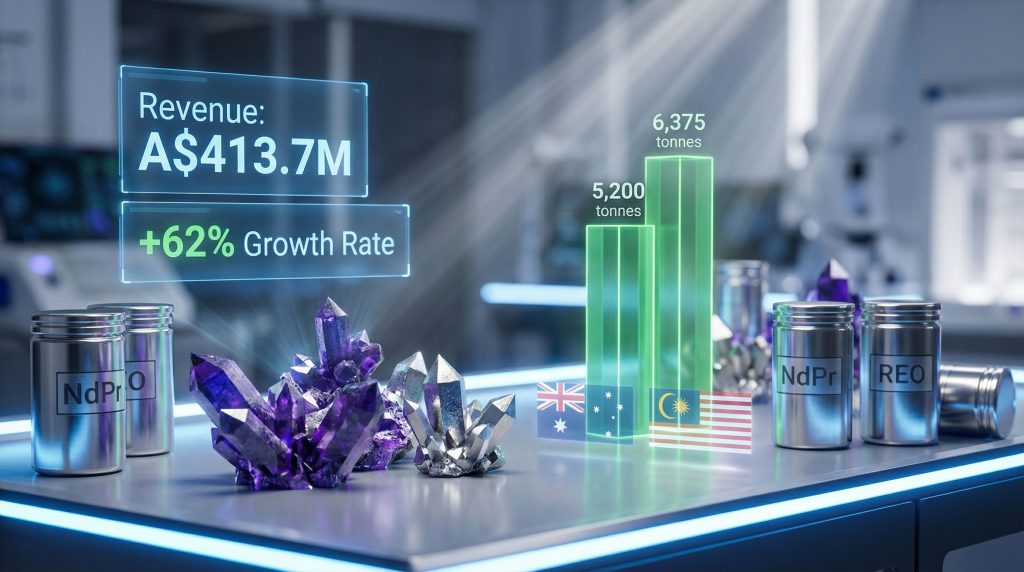

| Revenue | A$254.3M | A$413.7M | +A$159.4M | +62.7% |

| Net Profit | A$5.9M | A$80.2M | +A$74.3M | +1,259% |

| REO Production | ~5,200 tonnes | 6,375 tonnes | +1,175 tonnes | +22.6% |

| Cash Position | Not disclosed | A$1.03B | – | Post-equity raise |

The revenue expansion reflects both volume growth and pricing improvements. REO production increased 23% year-over-year to 6,375 tonnes, while average realised prices benefited from NdPr appreciation and heavy rare earth revenue contribution. Heavy rare earths contributed an estimated 25-30% of H1 FY26 revenue, representing the first full half-year of consistent production from the Malaysian facility.

Earnings quality assessment reveals margin expansion driven primarily by pricing rather than operational leverage. Gross margins approximated 48-52% during H1 FY26, supported by premium pricing for non-Chinese supply and higher-value product mix including dysprosium and terbium sales.

Production Capacity Expansion Impact

The Mt Weld mine expansion commissioning during H1 FY26 increased processing capacity from approximately 3,500 tonnes to 5,000+ tonnes REO annually. This expansion utilised modernised mill infrastructure designed to increase throughput per tonne of ore processed while reducing unit costs.

However, operational disruptions at the Kalgoorlie processing plant created temporary headwinds. Power supply issues in November 2025 caused production downtime and elevated processing costs, contributing an estimated A$8-12 million in unplanned expenses. The facility requires 20-25 MW continuous power load, highlighting infrastructure dependencies that management is addressing through solar and battery backup solutions.

The Malaysian heavy rare earth facility achieved full operational status during the reporting period. Current capacity reaches approximately 1,500-2,000 tonnes dysprosium oxide equivalent annually, with expansion potential to 3,000+ tonnes by FY28. Product mix includes dysprosium (60%), terbium (20%), and other heavy rare earths (20%).

What Are the Key Investment Risks and Opportunities?

Investment analysis requires balancing exceptional growth prospects against operational execution risks and commodity price volatility inherent in rare earth markets. Furthermore, understanding the broader implications of US-China trade war impact on global supply chains becomes increasingly important for Lynas rare earths stock analysis.

Price Volatility and Market Dynamics

Rare earth pricing exhibits cyclical patterns driven by Chinese policy decisions, technology adoption rates, and strategic stockpiling activities. Historical NdPr pricing ranged from US$40-50 per kilogram during 2020-2022, demonstrating the potential for significant price corrections.

Nevertheless, current pricing dynamics differ from historical cycles. Government strategic stockpiling initiatives across the U.S., EU, and Australia create sustained demand floors. Technology companies increasingly prioritise supply chain security over cost optimisation, supporting premium pricing for Western suppliers.

Long-term demand projections support structural price appreciation. The International Energy Agency forecasts 20-25% compound annual growth in rare earth demand through 2030, driven by electric vehicle adoption and renewable energy deployment. Supply additions outside China remain limited, supporting sustained price premiums.

Operational and Execution Risks

Leadership transition represents a near-term uncertainty factor. CEO Amanda Lacaze's retirement after 12 years of leadership creates succession planning challenges, though management continuity appears well-structured with her remaining through June 2026 to support the handover process.

Infrastructure dependencies pose ongoing operational risks. The Kalgoorlie power supply disruptions demonstrate vulnerability to grid reliability issues. Management's evaluation of solar and battery backup solutions indicates proactive risk management, though implementation timelines and capital requirements remain unclear.

Additionally, regulatory environment complexity spans multiple jurisdictions. The Malaysian facility operates under specific licensing conditions, while Australian operations face evolving environmental compliance requirements. Tailings management and water usage optimisation represent ongoing operational priorities requiring continuous capital investment.

How Do Analysts Value Lynas Stock?

Valuation analysis reveals significant dispersion in price targets reflecting uncertainty around rare earth price sustainability and operational execution capabilities. The latest analysis from Australian Resources and Investment highlights the company's remarkable transformation during this commodity cycle.

Consensus Forecasts and Price Targets

| Forecast Category | Consensus Estimate | Growth vs FY25 |

|---|---|---|

| Revenue | A$1.08-1.1B | +94-98% |

| EPS | A$0.32 | +3,100% |

| REO Production | 16,100 tonnes | +53% |

| EBITDA Margin | ~44% | Expansion |

Earnings per share projections reflect substantial leverage to rare earth pricing and production scaling. The consensus EPS estimate of A$0.32 implies an annualised run-rate based on H1 FY26 performance, though this assumes sustained pricing levels and operational stability.

Revenue forecasts incorporate full-year contribution from heavy rare earth sales and capacity expansion benefits. The projected 94-98% revenue growth appears achievable given current pricing trends and production scaling timeline, though execution risks remain significant.

Valuation Multiples and Peer Comparison

Current valuation metrics reflect growth premium pricing with inherent volatility risks:

- Price-to-Sales ratio: 26.68x versus sector average of 9.23x

- Forward Price-to-Earnings: Approximately 40x based on FY26 estimates

- Enterprise Value to EBITDA: Premium multiples reflecting scarcity value

DCF intrinsic value estimates range around A$16.12 per share, suggesting current trading levels near fair value assuming base-case scenarios for rare earth pricing and production scaling. However, sensitivity analysis reveals significant valuation ranges depending on price assumptions and operational execution.

What Strategic Factors Drive Long-term Value?

Long-term investment thesis centres on sustained demand growth for separated rare earth elements combined with limited supply additions outside Chinese control. As Stocks Down Under research indicates, profit improvements don't always translate immediately into share price appreciation due to market volatility concerns.

Geopolitical Supply Chain Positioning

Western government initiatives increasingly prioritise rare earth supply chain security through policy frameworks and funding mechanisms. The U.S. CHIPS and Science Act includes provisions for critical minerals supply chain development, while EU Strategic Autonomy initiatives target reduced dependence on Chinese rare earth imports.

Trade tensions and export control policies create additional tailwinds for non-Chinese suppliers. China has demonstrated willingness to restrict rare earth exports during geopolitical disputes, most notably during 2010-2015 when export quotas drove significant price appreciation.

Consequently, strategic partnership opportunities with technology companies provide revenue stability and expansion potential. Long-term off-take agreements with automotive and renewable energy manufacturers offer protection against price volatility while securing market access during capacity expansion phases.

Technology and Market Evolution

Electric vehicle market penetration continues accelerating across major automotive markets. Tesla, General Motors, and European manufacturers increasingly commit to permanent magnet motor designs for performance and efficiency advantages, creating sustained NdPr demand growth.

Wind energy expansion, particularly offshore installations, drives heavy rare earth consumption. Offshore wind projects utilise direct-drive generators requiring substantial quantities of dysprosium and terbium for high-performance magnet applications.

In addition, technology substitution risks remain limited in the medium term. While research continues on rare earth-free motor designs and ferrite magnet alternatives, current penetration remains below 15% of EV motor applications. Performance compromises and cost considerations limit adoption rates for substitution technologies.

Investment Decision Framework for Lynas

Investment analysis requires scenario-based evaluation given the multiple variables affecting rare earth market dynamics and operational execution. Moreover, conducting thorough Lynas rare earths stock analysis involves understanding both upside potential and downside protection mechanisms.

Bull Case Scenario Analysis

Sustained high rare earth pricing driven by supply-demand imbalances creates exceptional profitability scenarios. NdPr pricing maintenance above US$100 per kilogram combined with successful capacity scaling to 16,100 tonnes annually could generate substantial cash flow growth.

Key bull case drivers include:

- Accelerated EV adoption exceeding current market projections

- Government stockpiling programs creating sustained demand floors

- Chinese export restrictions limiting competitive supply availability

- Successful operational scaling without significant execution challenges

Premium valuation multiples could expand further if Lynas demonstrates consistent operational performance and market share gains in Western supply chains.

Bear Case Risk Assessment

Rare earth price normalisation represents the primary downside risk. Historical pricing patterns suggest potential corrections to US$60-70 per kilogram for NdPr if supply additions or demand moderation occurs.

Bear case risk factors include:

- New supply sources reducing scarcity premiums for non-Chinese production

- Execution challenges in capacity expansion projects affecting production targets

- Technology substitution accelerating adoption of rare earth-free alternatives

- Regulatory compliance issues creating operational disruptions or cost increases

Current valuation multiples provide limited downside protection during commodity price corrections, requiring strong conviction in long-term demand fundamentals.

The next major ASX story will hit our subscribers first

Key Catalysts and Monitoring Points

Investment timing requires careful monitoring of operational milestones and market developments that could significantly impact valuation. Furthermore, understanding the broader context of Lynas rare earths stock analysis involves tracking both company-specific and sector-wide developments.

Near-term Performance Indicators

The Q3 FY26 production report, expected in April 2025, represents the most significant near-term catalyst. Demonstration of operational stability at Kalgoorlie following power supply resolution could remove the primary cloud over operational execution.

Key monitoring points include:

- Production volume consistency across all facilities

- NdPr pricing trends and contract negotiation outcomes

- CEO succession planning and leadership transition execution

- Cash deployment strategy for expansion projects and potential acquisitions

Long-term Strategic Milestones

The "Towards 2030" strategic plan implementation provides a framework for evaluating long-term value creation potential. Successfully achieving 16,100 tonnes annual capacity while maintaining cost competitiveness represents a critical validation of the growth thesis.

Strategic milestone tracking includes:

- Heavy rare earth production scaling to full facility capacity

- Market share evolution in Western technology supply chains

- Potential downstream processing investments in magnet manufacturing

- Strategic partnership development with major automotive and renewable energy companies

Investment Thesis Summary: Lynas represents unique exposure to rare earth supply chain security trends with demonstrated operational momentum, though elevated valuation multiples require sustained pricing premiums and flawless execution of capacity expansion plans to justify current market pricing.

Disclaimer: This analysis contains forward-looking statements and projections that involve inherent risks and uncertainties. Rare earth commodity prices exhibit significant volatility, and operational execution risks could materially impact financial performance. Investors should conduct independent research and consider their risk tolerance before making investment decisions.

Ready to Capitalise on the Next Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring how major finds like those from De Grey Mining and WA1 Resources created exceptional market opportunities. Begin your 14-day free trial today to position yourself ahead of the market and secure your competitive advantage in the evolving critical minerals landscape.