May 19, 2026

Market Dynamics Driving Global Phosphate Trade Transformation

The global phosphate fertilizer industry faces unprecedented structural shifts as supply chain vulnerabilities exposed during recent years continue reshaping international trade patterns. China's phosphate export market represents a critical focal point where resource nationalism intersects with agricultural security concerns. Market participants across agricultural value chains must navigate an increasingly complex landscape where traditional supplier relationships no longer provide the stability once taken for granted.

Understanding these evolving dynamics becomes critical as geopolitical tensions intensify competition for strategic mineral resources. Countries worldwide reassess their fertilizer security frameworks while balancing domestic agricultural needs against export revenue opportunities. This transformation extends beyond simple supply and demand mechanics to encompass fundamental questions about resource sovereignty and industrial policy coordination.

Investment implications emerge as traditional market assumptions face testing against new realities. Long-term contracts, inventory strategies, and production capacity planning must account for heightened volatility across multiple risk dimensions simultaneously. Furthermore, the mining industry evolution demonstrates how technological advances reshape traditional resource extraction approaches.

When big ASX news breaks, our subscribers know first

Understanding China's Strategic Phosphate Export Framework

China's phosphate export policy represents a sophisticated approach to resource management that extends beyond simple trade controls. The framework distinguishes between various phosphate products through differential regulatory treatment, creating market segmentation that reflects both domestic priorities and international competitive positioning. This strategic approach parallels broader China export controls strategy seen across critical minerals sectors.

Export Quota Mechanisms and Implementation Strategies

The administrative structure governing China's phosphate exports operates through the Ministry of Commerce (MOFCOM) licensing system, which allocates annual quotas to qualified exporters. This mechanism provides government oversight while allowing individual companies discretion in quota utilization based on market conditions.

Key features of the quota system include:

• Administrative allocation through MOFCOM licensing procedures

• Market-driven execution allowing companies to optimize quota usage

• Annual adjustment mechanisms reflecting domestic supply assessments

• Selective product classification distinguishing finished from intermediate products

The policy framework draws parallels with China's approach to other strategic minerals, including rare earth elements and tungsten, establishing precedent for resource-based export management. Implementation typically involves quarterly reviews of domestic market conditions to assess export capacity availability.

China's export control evolution reflects broader industrial policy coordination emphasising domestic value-added production over raw material exports. This strategic shift prioritises securing sufficient resources for domestic agricultural needs while maintaining influence over global supply chains.

NP and NPS Export Classification Complexities

The regulatory distinction between finished phosphate fertilizers and intermediate compounds creates significant market implications. Nitrogen-Phosphate (NP) and Nitrogen-Phosphate-Sulfur (NPS) products receive different treatment compared to traditional DAP and MAP fertilizers.

Technical specifications driving classification differences:

• NP compounds typically combine ammonium nitrate or urea with phosphate components

• NPS formulations incorporate sulfuric acid or sulfate elements for enhanced nutrient delivery

• Processing stage considerations distinguish inputs for further manufacturing from final agricultural products

• End-use applications determine regulatory categorisation and export licensing requirements

This classification approach allows China to maintain exports of intermediate products while restricting finished fertilizers, preserving some international market presence while prioritising domestic agricultural security. The technical complexity creates opportunities for product reformulation to navigate regulatory requirements.

Market participants must understand these distinctions to develop appropriate sourcing strategies and contract structures. The regulatory framework evolution suggests continued refinement of product classifications based on domestic supply conditions and international market dynamics.

What Drives China's Domestic Phosphate Supply Constraints?

China's phosphate supply situation presents a fundamental resource paradox that underlies current export policy decisions. The country maintains global production leadership while confronting significant resource limitations that threaten long-term sustainability. Additionally, the impact of US‑China trade impacts further complicates strategic resource allocation decisions.

Resource Scarcity vs. Production Dominance Paradox

According to China's phosphate market analysis, China holds approximately 3.7 billion tonnes of phosphate rock reserves, representing roughly 5.2% of global reserves totalling 71 billion tonnes. Despite this relatively modest reserve base, China produces approximately 35-40% of global phosphate output.

Critical reserve-to-production ratio analysis reveals:

| Metric | China | Global Average |

|---|---|---|

| Reserve-to-production ratio | 74 years | 303 years |

| Production intensity | High extraction rate | Moderate extraction rate |

| Reserve depletion risk | Elevated | Lower |

This production intensity creates structural vulnerability as China extracts phosphate at rates significantly exceeding the global average relative to reserve base. The accelerated depletion timeline forces policy makers to balance current economic benefits against future resource security.

Environmental compliance requirements further constrain production capacity. China's Ministry of Ecology and Environment implements progressively stricter standards for phosphate mining operations, particularly in environmentally sensitive areas such as the Yangtze River basin watershed.

Mining capacity faces reduction pressure through environmental permit restrictions and facility closures for non-compliance. Industry consolidation eliminates smaller, less efficient operations while concentrating production among larger companies with better environmental management capabilities.

Competing Industrial Demand Pressures

Traditional agricultural demand for phosphate fertilizers now competes with emerging technology sectors requiring phosphorus-based materials. The lithium iron phosphate (LFP) battery sector represents the most significant new demand source, though the competition occurs through indirect supply chain interactions.

LFP battery sector impact analysis:

• Industrial phosphoric acid production diverts sulfuric acid feedstock from fertilizer manufacturing

• Battery-grade phosphate compounds require higher purity specifications than agricultural applications

• Processing facility capacity allocation must balance between traditional and emerging market demands

• Technology sector demand typically offers premium pricing compared to commodity fertilizer applications

According to International Energy Agency analysis, global LFP battery production reached approximately 2.5-3.0 million MWh capacity in 2024. This translates to roughly 30,000-54,000 tonnes of phosphorus demand annually, representing a relatively small but rapidly growing consumption segment.

Investment Insight: The competition between traditional agricultural and emerging technology applications creates bifurcated market dynamics where premium applications can bid resources away from commodity uses during supply constraint periods.

Energy storage demand projections suggest continued growth in phosphate consumption for non-agricultural applications. This trend reinforces domestic resource conservation priorities while creating opportunities for value-added processing operations.

How Production Cost Inflation Impacts Export Decisions

Cost structure dynamics significantly influence China's phosphate export economics, with sulfuric acid input costs representing a critical variable in production viability assessments. However, these costs must be evaluated alongside tariff-driven market impacts affecting international competitiveness.

Sulfur Price Volatility as a Critical Variable

Sulfuric acid requirements for phosphoric acid production create direct linkage between sulfur market conditions and phosphate fertilizer manufacturing economics. The wet phosphoric acid process demands approximately 0.8-0.9 tonnes of concentrated sulfuric acid per tonne of phosphate rock processed.

Production cost structure breakdown:

| Cost Component | Share of Total Production Cost | Market Sensitivity |

|---|---|---|

| Raw materials (phosphate rock, ammonia) | 40-50% | High |

| Sulfuric acid inputs | 25-35% | Very High |

| Labour and overhead | 10-15% | Low |

| Energy and utilities | 5-10% | Moderate |

| Transportation | 3-5% | Regional variation |

According to U.S. Geological Survey data and market assessments, sulfur prices experienced modest increases of approximately 5-15% year-over-year through 2024-2025, though regional variations and supply disruptions created periodic volatility spikes.

Key sulfur supply factors affecting Chinese producers:

• Reduced Russian sulfur availability due to geopolitical disruptions (from 13 million tonnes to approximately 10-11 million tonnes annually)

• Canadian oil sands processing adjustments affecting sulfur byproduct recovery

• Environmental regulations increasing global sulfur recovery requirements

• Competition from industrial applications beyond fertilizer production

Industry Consolidation Effects on Supply Chain

China's phosphate industry undergoes significant structural transformation as environmental compliance requirements eliminate smaller, less efficient operations. Major producers including Yunnan Yuntianhua and Chuanheng Group pursue vertical integration strategies to secure raw material supplies and optimise production costs.

Consolidation impacts include:

• Capacity rationalisation eliminating an estimated 36-46 million tonnes of inefficient production over 3-4 years

• Vertical integration reducing dependence on external raw material suppliers

• Technology upgrading improving environmental performance and production efficiency

• Market concentration among leading producers with better regulatory compliance capabilities

The consolidation process creates operational efficiencies while reducing overall production flexibility. Fewer, larger operations provide more predictable output but potentially less responsiveness to short-term market opportunities.

Environmental compliance costs represent a permanent structural change rather than cyclical expense variation. Companies must maintain higher operating standards regardless of market conditions, creating floor-level cost increases that affect export competitiveness.

Which Regional Markets Face the Greatest Supply Disruption?

China's export restrictions create differential impacts across global markets based on historical trade relationships and alternative supply source availability. In particular, agricultural regions that relied heavily on Chinese phosphate imports now face significant supply security challenges.

Trade Flow Redistribution Analysis

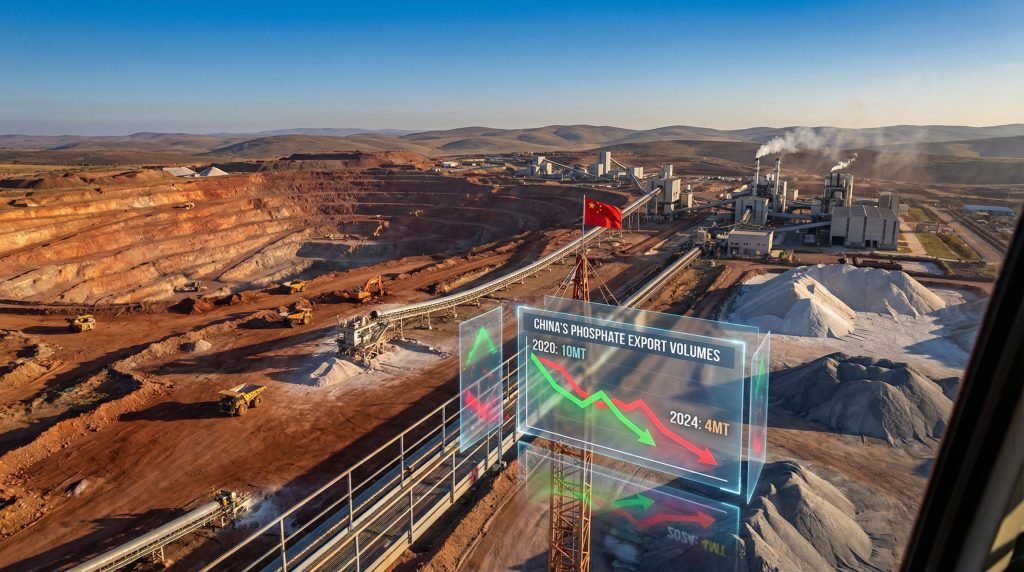

UN Comtrade data reveals the magnitude of Chinese phosphate export reductions and their implications for global supply chains. Historical export patterns show dramatic decline from peak levels.

Chinese Phosphate Fertiliser Export Trends:

| Year | Export Volume (Million Tonnes) | Policy Context |

|---|---|---|

| 2019 | 9.7 | Normal operations |

| 2020 | 8.2 | Pandemic-affected |

| 2021 | 4.8 | Initial restrictions |

| 2022 | 2.1 | Quota tightening |

| 2023 | 1.8 | Sustained controls |

The reduction from 9.7 million tonnes to under 2 million tonnes represents a supply gap requiring redistribution among alternative global suppliers. This reallocation creates strain on remaining production capacity while elevating price levels across importing regions.

Most affected regional markets include:

• Southeast Asia – High historical dependence on Chinese DAP and MAP supplies

• South America – Seasonal import timing conflicts with reduced Chinese availability

• Indian subcontinent – Large-scale agricultural demand competing for limited alternative supplies

• East Africa – Transportation cost disadvantages from alternative supplier locations

Price Discovery Mechanisms in Constrained Markets

Supply constraints create structural changes in global phosphate pricing dynamics as traditional benchmarks adjust to reduced Chinese participation. Regional price premiums develop based on transportation economics and alternative supplier capacity limitations.

Alternative suppliers including Morocco, Russia, and Saudi Arabia operate at or near maximum sustainable capacity, limiting ability to absorb displaced Chinese volumes fully. This creates persistent supply gaps that elevate global price levels, with implications for fertilizer price volatility affecting farmers worldwide.

Market tightness indicators:

• Extended contract lead times for DAP and MAP procurement

• Regional price premium expansion beyond historical transportation differentials

• Inventory accumulation strategies among importing countries

• Increased bilateral government-to-government supply agreements

The constrained supply environment forces importing countries to develop more diversified sourcing strategies while accepting higher procurement costs and reduced supply flexibility.

When Will China Resume Normal Phosphate Export Operations?

China's export resumption timeline depends on multiple interconnected factors including domestic supply security, international market conditions, and policy objective achievement. Furthermore, companies seeking alternative funding sources must consider various capital raising methods to finance supply chain adjustments.

Policy Timeline Projections and Triggers

Export policy adjustments typically follow seasonal agricultural cycles and domestic fertilizer demand patterns. Historical precedents suggest export suspensions during January-May periods coinciding with domestic spring fertilizer application seasons.

Potential resumption scenarios include:

• Optimistic timeline: Partial resumption by late 2026 following domestic supply security achievement

• Conservative projection: Sustained restrictions through 2027 pending resource management targets

• Risk factors: Extended environmental compliance requirements or emerging demand sectors

Policy reversal triggers likely include combination of domestic supply surplus conditions, international diplomatic considerations, and producer economic pressures. The government maintains flexibility to adjust export quotas based on changing circumstances.

Market Condition Dependencies

Several market variables influence export policy decision-making:

Critical factors for policy adjustment:

• Sulfur price normalisation reducing production cost pressures

• Domestic fertilizer demand seasonal patterns and inventory levels

• Strategic reserve accumulation targets for resource security

• International relationship considerations and trade diplomacy

Export resumption likely occurs gradually through quota increases rather than immediate return to historical volumes. This approach allows policy makers to test market conditions while maintaining domestic supply security priorities.

Disclaimer: Export policy projections involve significant uncertainty as decisions depend on complex political, economic, and environmental factors subject to rapid change.

The next major ASX story will hit our subscribers first

How Are Global Competitors Responding to China's Market Exit?

Alternative phosphate producers pursue capacity expansion strategies while confronting technical and economic constraints limiting rapid supply increase capability. These developments reshape competitive dynamics across the global phosphate industry.

Alternative Producer Capacity Expansion

Global phosphate production concentration among a limited number of countries creates supply chain vulnerabilities when major producers implement export restrictions. Alternative suppliers face varying capacity expansion potential.

Major Alternative Supplier Analysis:

| Producer Region | Current Capacity Status | Expansion Timeline | Market Share Potential |

|---|---|---|---|

| Morocco | Gradual capacity increases | 2022-2026 | Partial gap filling |

| Russia | Operating at maximum capacity | Stable through 2027 | Limited expansion |

| Saudi Arabia | Full capacity utilisation | New capacity 2027-2028 | Future competition |

| Jordan | Moderate expansion capability | 2025-2027 | Regional supply focus |

Morocco's OCP Group represents the largest alternative supplier with ongoing capacity expansion projects. However, production increases occur gradually due to technical complexity and infrastructure requirements for phosphate processing facilities.

Russian producers including PhosAgro operate at maximum sustainable capacity with limited expansion potential due to international sanctions affecting technology access and financing capabilities.

Saudi Arabian development through Ma'aden joint ventures offers future capacity additions but requires several years for project completion and production ramp-up.

Supply Chain Adaptation Strategies

Importing countries and agricultural companies implement various approaches to manage supply disruption risks:

Adaptation strategies include:

• Long-term contract restructuring with alternative suppliers to secure volume commitments

• Regional sourcing diversification reducing dependence on single supplier countries

• Inventory management adjustments maintaining higher strategic reserves

• Product substitution exploring alternative fertilizer formulations and nutrient delivery systems

• Domestic production development where geological conditions support phosphate mining

Bilateral government agreements become increasingly important as state-to-state relationships provide supply security unavailable through purely commercial arrangements. Countries pursue diplomatic initiatives to secure fertilizer supplies for food security purposes.

Investment flows redirect toward alternative supplier regions as market participants seek to develop additional production capacity outside traditional dominant suppliers.

What Are the Investment Implications for Global Phosphate Markets?

The structural changes in global phosphate trade create significant investment opportunities and risks across the value chain. China's phosphate export market transformation forces investors to reassess traditional sector assumptions and identify emerging opportunities.

Capacity Investment Requirements

The supply gap created by reduced Chinese exports requires substantial capital investment in alternative production regions. Industry analysis suggests $15-20 billion in new capacity investment needed to fully replace Chinese export volumes.

Investment priority areas:

• Mine development in Morocco, Saudi Arabia, and other phosphate-rich regions

• Processing facility construction for DAP and MAP production

• Infrastructure development including ports, railways, and utilities

• Technology transfer for advanced phosphate processing techniques

Capital expenditure requirements typically range $800-1,200 per tonne of annual DAP production capacity, depending on location and technological sophistication. Project development timelines extend 4-6 years from initial investment to commercial production.

Financing challenges include:

• Long payback periods requiring patient capital sources

• Commodity price volatility affecting project economics

• Environmental and social approval processes

• Technology access restrictions in some jurisdictions

Market Structure Evolution

The phosphate industry experiences fundamental restructuring as market share redistributes among global producers. Traditional dominance patterns face permanent adjustment as new production capacity develops.

Structural changes include:

• Concentration risk reduction through diversified supplier base development

• Regional self-sufficiency initiatives where geological resources permit

• Strategic partnership formation between producers and consumers

• Vertical integration trends securing supply chain control

Investment opportunities emerge in:

• Companies with undeveloped phosphate reserves outside China

• Logistics and transportation infrastructure serving alternative suppliers

• Technology providers for phosphate processing efficiency improvements

• Agricultural input companies developing China-independent supply chains

Investment Warning: Phosphate market investments involve significant geological, regulatory, and commodity price risks requiring thorough due diligence and risk management strategies.

Strategic Outlook for Global Phosphate Trade

Long-term phosphate market evolution depends on multiple interconnected trends including environmental regulation, technology advancement, and geopolitical developments. The transformation of China's phosphate export market represents just one component of broader structural changes reshaping global fertilizer trade.

Scenario Planning for Market Recovery

Three primary scenarios emerge for China's phosphate export market participation:

Scenario 1: Gradual Resumption (Probability: 40%)

- Partial export resumption by 2026-2027

- Quota-based system maintaining domestic priority

- Limited return to historical export volumes

Scenario 2: Prolonged Restrictions (Probability: 45%)

- Sustained export limitations through 2028

- Permanent market share loss to alternative suppliers

- Focus on domestic market and value-added products

Scenario 3: Full Market Re-entry (Probability: 15%)

- Complete policy reversal following resource security achievement

- Competitive re-entry against established alternative suppliers

- Market share recovery challenges due to supply chain diversification

Long-term Structural Changes

Several trends suggest permanent alterations to global phosphate trade patterns:

Structural transformation factors:

• Resource nationalism prioritising domestic food security over export revenue

• Environmental constraints limiting production capacity expansion

• Technology diversification creating alternative nutrient delivery systems

• Regional production development reducing dependence on traditional exporters

Supply chain resilience becomes a strategic priority as agricultural systems require reliable fertilizer access for food security. Countries develop domestic production capabilities where possible or establish diversified import relationships to reduce concentration risks.

Innovation opportunities emerge in phosphate recovery technologies, precision fertilizer application, and nutrient cycling systems that reduce overall phosphorus demand while maintaining agricultural productivity.

The global phosphate market transitions from a China-dominated system toward a more distributed production landscape with higher costs but improved supply security for importing regions. This transformation requires significant capital investment and time for full implementation.

This analysis is based on publicly available data and industry research. Projections involve inherent uncertainty due to complex political, economic, and environmental factors. Investors should conduct independent due diligence and consider professional advice before making investment decisions.

Looking to Capitalise on China's Phosphate Export Disruption?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, including phosphate and fertiliser-related opportunities that could benefit from global supply chain shifts. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, then begin your 30-day free trial today to position yourself ahead of the market.