June 16, 2026

The Investment Logic Behind a World Reshaped by Energy Insecurity

Energy systems do not transform overnight. They shift gradually, shaped by decades of accumulated capital decisions, policy frameworks, and technological momentum. But occasionally, a single geopolitical rupture compresses that timeline dramatically, forcing a wholesale reassessment of where money flows, why it flows there, and how quickly it must arrive. The Middle East conflict and global energy investment patterns are living proof of this phenomenon, playing out in real time.

The effective closure of the Strait of Hormuz, a waterway through which roughly a fifth of global oil and liquefied natural gas has historically transited, has delivered a supply shock of genuinely historic proportions. Unlike the Russia-Ukraine energy crisis of 2022, which primarily disrupted pipeline gas flows into Europe, this disruption strikes at a physical chokepoint that serves as a common artery for energy exports reaching Asia, Europe, and beyond simultaneously.

The implications are not simply a matter of higher spot prices. They represent a structural rewiring of investment priorities that could rival the realignment triggered by the oil shocks of the 1970s. The geopolitical mining landscape is being reshaped in ways that extend well beyond any single commodity or region.

The International Energy Agency's World Energy Investment 2026 report, released in May 2026, provides the most comprehensive quantitative mapping of how these forces are reshaping capital allocation across the global energy system. The findings are striking in both scale and direction.

When big ASX news breaks, our subscribers know first

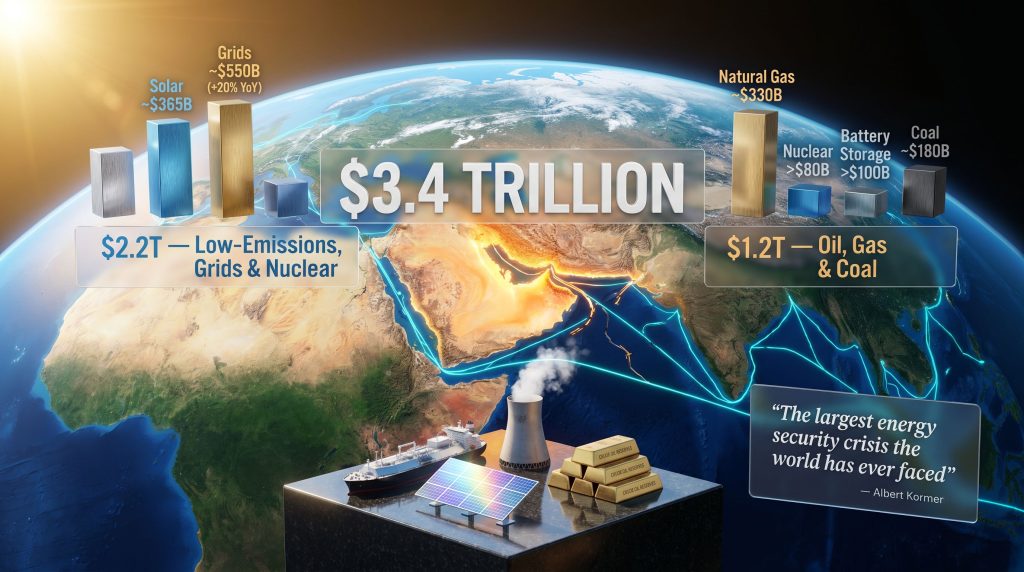

$3.4 Trillion and the Architecture of a Security-First Investment Era

Global energy investment is projected to reach $3.4 trillion in 2026, a figure that represents a slight increase year-on-year but conceals a profound reordering of priorities beneath the headline number. The split between clean and fossil fuel investment tells the deeper story.

Approximately $2.2 trillion is directed toward grids, storage, low-emissions fuels, nuclear, renewables, efficiency, and electrification. Around $1.2 trillion flows toward oil, natural gas, and coal combined. That ratio, with low-emissions and electricity-system investment outpacing fossil fuels by nearly two-to-one, reflects something more durable than climate policy momentum. It reflects the logic of energy security itself.

Global Energy Investment Breakdown for 2026

| Investment Category | 2026 Projected Spend | Primary Driver |

|---|---|---|

| Total Global Energy Investment | $3.4 trillion | Geopolitical security + electrification |

| Low-emissions, grids, storage, nuclear, efficiency | $2.2 trillion | Domestic energy security pivot |

| Oil, gas, and coal combined | $1.2 trillion | Fossil fuel baseline + LNG surge |

| Electricity supply and infrastructure | ~$1.6 trillion | Grid modernisation + AI demand |

| Electricity incl. end-use electrification | ~$2.0 trillion | Full system electrification push |

| Electricity grids alone | ~$550 billion (+20% YoY) | Resilience and capacity expansion |

| Renewable power | ~$665 billion | Domestic resource diversification |

| Solar energy | ~$365 billion | Cost competitiveness + scalability |

| Natural gas investment | ~$330 billion (decade high) | LNG export project wave |

| Nuclear power | >$80 billion | Energy reliability resurgence |

| Coal investment | ~$180 billion (highest since 2012) | Asian security buffer strategy |

| Battery storage | >$100 billion | Grid flexibility and storage demand |

| Oil investment | <$500 billion (3rd consecutive decline) | Risk aversion + strategic pivot |

| Energy efficiency | ~$350 billion | Demand-side policy expansion |

Low-emissions sources now account for more than 70% of total power generation investment globally. This is not a cyclical fluctuation driven by a single policy cycle. It is a structural reorientation being reinforced by successive geopolitical crises, each one demonstrating the strategic vulnerability of import-dependent energy systems.

The current energy disruption is arriving just four years after the Russia-Ukraine crisis reshaped European energy strategy. Two consecutive supply shocks within half a decade are compressing investment decision timelines and creating a fundamentally more risk-conscious capital allocation environment across importing nations.

Why Oil Investment Is Falling Even as Prices Rise

One of the most counterintuitive findings in the 2026 investment data concerns oil. Despite elevated prices driven by the Strait of Hormuz disruption, oil investment is expected to fall below $500 billion in 2026, marking the third consecutive annual decline. This defies the traditional logic of commodity markets, where price signals are supposed to unlock capital.

Furthermore, the IEA's analysis of Middle East energy impacts highlights how four structural constraints are suppressing the upstream spending response:

-

Price uncertainty: Investors remain unconvinced the current price spike is durable enough to justify committing capital to long-cycle projects that may take five to ten years to reach production.

-

Long project lead times: Even where investment appetite exists, the timeline between final investment decision and first production severely limits any near-term supply response.

-

Supply chain bottlenecks: Equipment manufacturing capacity, specialised workforce availability, and materials procurement are all constrained after years of underinvestment.

-

Offshore rig market tightening: Rig availability in key deepwater basins has become increasingly limited, creating a physical ceiling on drilling activity regardless of project economics.

The Middle East stands as a partial exception, where some upstream spending responses are occurring closer to existing infrastructure. Elsewhere, particularly in deepwater and frontier basins, the appetite for long-cycle fossil fuel commitments has fundamentally shifted. Capital that might previously have flowed into multi-decade oil projects is being evaluated against a different risk matrix, one that now includes stranded asset risk, energy transition timelines, and geopolitical exposure alongside traditional project economics.

Natural Gas Reaches a Decade High: The LNG Beneficiary Effect

While oil investment contracts, natural gas tells a different story. Investment in natural gas is projected to reach $330 billion in 2026, the highest level in approximately ten years. The driver is a wave of new LNG export projects concentrated primarily in the United States and Qatar. The LNG supply outlook for the coming years reflects this surge in project activity and long-term contract commitments.

The strategic logic is straightforward. Countries that previously relied on Strait of Hormuz transit flows for gas imports are now actively seeking alternative supply sources accessible via different maritime routes. Long-term LNG supply contracts, which provide the revenue certainty needed to underpin multi-billion-dollar liquefaction terminal financing, are being signed at an accelerated pace.

The tension within this gas investment surge is significant. For importing nations in Asia and Europe, long-term LNG contracts represent security of supply but also exposure to decades of fossil fuel dependence. For project developers, the investment case is compelling in the short term but carries long-term carbon pathway risk as decarbonisation commitments harden. This dual-role dilemma, gas as both bridge solution and potential long-term liability, is one of the defining tensions shaping energy finance in 2026.

Renewables, Nuclear, and the Domestic Resource Imperative

Solar Leads the Renewable Charge

Renewable power investment is expected to reach approximately $665 billion in 2026, with solar commanding a dominant $365 billion of that total. Solar's ascendancy is not accidental. Among all low-emissions technologies, solar offers the most scalable, fastest-deploying, and increasingly cost-competitive pathway to domestic energy production. For governments confronting import dependency, solar has been repositioned as a strategic security asset, and renewable energy solutions are increasingly being integrated across industrial sectors as well.

Annual growth in renewable investment has moderated following several years of rapid expansion, but the underlying trajectory remains firmly upward. The moderation reflects a maturing investment cycle rather than any reversal of direction.

Nuclear's Broad-Based Revival

Nuclear investment is exceeding $80 billion annually, with close to 80 gigawatts of new nuclear capacity under construction across 15 countries. The geographic spread of that construction pipeline is particularly significant. Nuclear's resurgence is not confined to a handful of historically dominant markets. It reflects a broad-based reassessment of baseload generation reliability as a strategic asset in an era of heightened supply risk.

Nuclear offers what renewables cannot yet fully replicate at scale: dispatchable, weather-independent power generation with zero fuel import exposure. In a post-Hormuz investment environment, those characteristics carry substantial strategic premium.

Coal's Controversial Return

The most politically uncomfortable data point in the 2026 investment picture is coal. Investment is set to reach approximately $180 billion, the highest level since 2012. China accounts for nearly 70% of global coal supply spending, and several Asian nations are actively considering extending the operational life of existing coal-fired power plants as a near-term energy security measure.

The simultaneous acceleration of both renewable and coal investment illustrates the defining contradiction of crisis-driven energy policy. Short-term security imperatives and long-term decarbonisation commitments are being pursued in parallel rather than in sequence, with no guarantee that the short-term decisions will not create infrastructure lock-in that complicates the longer-term agenda.

Electricity Infrastructure: The $550 Billion Backbone of the New Energy System

Grids as Strategic Infrastructure

The single most important infrastructure investment category in 2026 is electricity grids. Spending is projected to approach $550 billion, representing growth of nearly 20% year-on-year. This figure reflects the dual demand created by renewable integration requirements on one side and the electrification of transport, heating, and industrial processes on the other.

Grid investment functions as a hedge against fossil fuel supply disruptions in a way that no individual generation technology can match. A more capable, interconnected grid reduces system vulnerability by enabling flexibility across generation sources and geography. Crucially, grid infrastructure also enables the full value of renewable and storage investment to be realised.

Battery Storage Crosses the $100 Billion Threshold

Battery storage investment exceeding $100 billion marks a genuine threshold moment for the sector. This scale of investment unlocks higher renewable penetration rates by addressing intermittency and enables energy systems to manage supply disruptions without defaulting to fossil fuel backup. The crossing of the $100 billion level reflects not just technology cost reductions but a fundamental shift in how energy planners view storage as a core system component rather than an optional enhancement.

AI, Data Centres, and the New Electricity Demand Frontier

An emerging and often underestimated driver of electricity investment is the rapid expansion of artificial intelligence infrastructure and data centre capacity. This trend is particularly pronounced in the United States, where orders for new gas-fired power plants reached a 25-year high in 2025, with data centre electricity demand playing a central role in that surge.

The concentration of turbine demand in the United States and the Middle East is creating supply constraints that limit availability for other regions seeking to expand gas-fired generation capacity. This turbine market tightness adds a new dimension to energy security planning, one that was not a significant factor in previous investment cycles.

The next major ASX story will hit our subscribers first

Financing Conditions and the Emerging Market Vulnerability Gap

How Conflict Drives Up the Cost of Capital

The Middle East conflict and global energy investment dynamics extend well beyond direct project economics into the financing environment itself. Conflict-driven financial market volatility is slowing investment decision timelines and pushing up long-term financing costs across capital-intensive energy technologies. The IEEFA's research on crisis impacts underscores how deeply these financing pressures are affecting capital allocation decisions worldwide.

The impact of rising financing costs is not evenly distributed. Emerging and developing economies already face financing costs materially higher than those in advanced economies, creating a compounding disadvantage. These nations simultaneously face higher energy import costs due to the supply disruption and elevated financing costs that make clean energy investment more expensive precisely when it is most strategically urgent.

This dual vulnerability represents one of the most serious equity dimensions of the current crisis. The regions most exposed to supply shock impacts are also the regions least able to finance their way out through accelerated domestic investment.

Regional Exposure: Who Faces the Sharpest Investment Disruptions

Asia sits at the epicentre of supply shock vulnerability. Nations heavily dependent on Strait of Hormuz transit flows are experiencing the most acute combination of import cost pressures and strategic anxiety. The investment response in Asia is multifaceted: accelerating domestic renewable deployment, extending coal plant operational lifetimes, and pursuing alternative LNG supply agreements simultaneously.

Middle Eastern producers face a paradox. Elevated global prices theoretically improve export revenues, but infrastructure damage and transit disruptions constrain the ability to capitalise fully. Reconstruction investment and the development of alternative export infrastructure, including new pipelines and transit routes that bypass the Hormuz chokepoint, are becoming priority capital allocations.

Europe is navigating its second consecutive geopolitical energy crisis within five years. The lessons of the 2022 Russia-Ukraine shock, which drove a rapid acceleration of renewables deployment and strategic gas storage investment, are informing a more robust response to the current disruption. European investment strategy is now being shaped by an explicit acknowledgment that consecutive supply shocks require structural rather than cyclical responses.

Africa and Latin America face asymmetric impacts. Energy-exporting nations may benefit from elevated price environments, while energy-importing nations confront intensified affordability challenges and increased difficulty accessing international energy financing.

Energy Efficiency: The Most Undervalued Investment in the Portfolio

With approximately $350 billion invested globally in energy efficiency each year, and around 20 countries announcing new efficiency policies directly in response to the current crisis, demand-side investment is receiving renewed attention. The strategic logic is compelling: efficiency investment reduces exposure to supply-side shocks without requiring new supply infrastructure, making it simultaneously a cost management, security, and climate tool.

Despite this, significant policy coverage gaps remain. Furthermore, the energy transition in mining and heavy industry sectors demonstrates how efficiency gains can be pursued even within the most energy-intensive operations. Closing the remaining policy gaps represents a high-return opportunity that is frequently underweighted in crisis response frameworks.

Long-Term Scenarios: Three Investment Pathways Beyond 2026

Scenario A: Prolonged Disruption Accelerates Structural Transition

If the Strait of Hormuz disruption extends well beyond 2026, the investment trajectory points toward an accelerated clean energy transition. Renewable deployment timelines compress, nuclear construction pipelines expand, and grid investment intensifies. Fossil fuel investment trajectories face a structural break as long-cycle projects struggle to justify capital commitment against an increasingly uncertain demand outlook.

Scenario B: Rapid De-escalation Creates a Rebound Dilemma

A rapid geopolitical resolution presents a different challenge. Does the security-first investment pivot prove durable, or does it reverse as price pressures ease? The risk of stranded assets in both fossil fuel infrastructure built to serve crisis-level prices and clean energy infrastructure premised on sustained security premium is non-trivial. Investment decisions made under crisis conditions may not be fully rational from a long-cycle perspective.

Scenario C: Fragmentation and Regional Energy Autarky

A third pathway involves the progressive fragmentation of global energy trade into regional blocs, each prioritising energy self-sufficiency over integrated market participation. This scenario accelerates domestic investment across all categories but reduces global capital allocation efficiency and may slow the pace of technology transfer and cost reduction that has driven renewable investment growth. In addition, the critical minerals demand surge associated with this scenario would place extraordinary pressure on global supply chains already under strain.

Frequently Asked Questions

How much is the world investing in energy in 2026?

Global energy investment is projected to reach $3.4 trillion in 2026 according to the IEA's World Energy Investment 2026 report. Of that total, approximately $2.2 trillion is directed toward low-emissions technologies, grids, storage, and nuclear, while roughly $1.2 trillion flows to fossil fuels.

Why is oil investment declining despite high prices?

Four structural constraints are suppressing upstream oil spending: uncertainty over whether the current price spike is durable, long project lead times that prevent rapid capital deployment, supply chain bottlenecks, and tightening offshore rig markets. These factors are collectively preventing elevated prices from translating into proportional upstream investment growth.

Which energy sources are benefiting most from the Middle East conflict?

- Natural gas and LNG are the primary beneficiaries, with investment reaching a decade high of $330 billion.

- Solar commands $365 billion of a $665 billion renewable investment total.

- Nuclear is seeing a broad-based global resurgence exceeding $80 billion annually.

- Electricity grids and battery storage are the backbone infrastructure beneficiaries.

- Coal is a secondary short-term beneficiary, particularly in Asia, reaching $180 billion.

How does the Middle East conflict affect energy financing in developing countries?

Emerging economies face a dual vulnerability: higher energy import costs from supply disruption, compounded by elevated financing costs that make domestic clean energy investment more expensive. This creates a compounding disadvantage that risks rationing clean energy capital away from the regions most urgently in need of energy infrastructure investment.

What role is AI playing in the 2026 energy investment outlook?

Data centre and AI infrastructure expansion is driving a surge in electricity demand, particularly in the United States, where orders for new gas-fired power plants reached a 25-year high in 2025. The concentrated turbine demand from the US and Middle East is creating supply constraints that limit gas-fired capacity deployment in other regions.

The New Investment Architecture: What It Means Going Forward

The pattern emerging from the 2026 investment data is not a temporary crisis response. It is the early signature of a durable structural shift in how the world finances, builds, and operates its energy systems. The Middle East conflict and global energy investment trajectories are now inextricably linked in ways that will shape capital allocation decisions for years to come.

The investment hierarchy is now clearly ordered: electricity infrastructure first, then renewables and nuclear, then gas, then efficiency, with oil declining and coal rising as a short-term regional anomaly. That hierarchy is being driven by a security-first paradigm that has displaced the cost-and-climate framework that governed investment logic through most of the previous decade.

Three indicators deserve close monitoring as this investment cycle unfolds:

- Strait of Hormuz transit status and the pace at which alternative export routes become operationally viable.

- LNG project final investment decisions and whether long-term contract commitments sustain the current gas investment momentum.

- Emerging market financing cost trajectories and whether international capital markets develop mechanisms to close the equity gap that currently disadvantages developing economies.

The investment decisions being made between 2026 and 2030 will determine whether the global energy system emerges from this period with genuine structural resilience or with a patchwork of short-term fixes that defer deeper challenges. The scale of capital being deployed is not in question. What remains uncertain is whether it will be allocated with sufficient foresight to build a system that can withstand the next disruption, not just respond to the current one.

This article draws on data and analysis from the International Energy Agency's World Energy Investment 2026 report. Projections and scenario analyses represent forward-looking assessments subject to geopolitical, macroeconomic, and technological uncertainty. Nothing in this article constitutes financial or investment advice.

Want to Know Which ASX Discoveries Are Emerging From the Energy Transition Surge?

With $3.4 trillion reshaping global energy investment priorities, the ripple effects on critical mineral exploration and ASX-listed resource companies are profound. Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries tied to the commodities driving this new energy architecture — from battery metals to nuclear inputs — so subscribers can act ahead of the broader market. Explore historic examples of what major discoveries can deliver and begin a 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.