June 25, 2026

The Structural Forces Reshaping Global Mining Investment Dynamics

Industrial transformation rarely announces itself through traditional economic indicators. While financial markets obsess over quarterly earnings cycles and central bank policies, deeper structural shifts often emerge from the intersection of technological advancement, resource scarcity, and geopolitical realignment. The contemporary mining sector exemplifies this phenomenon, where artificial intelligence infrastructure demands, energy transition mandates, and supply chain vulnerabilities have converged to create investment dynamics fundamentally different from historical commodity cycles. This mining stocks supercycle represents a fundamental departure from traditional market patterns.

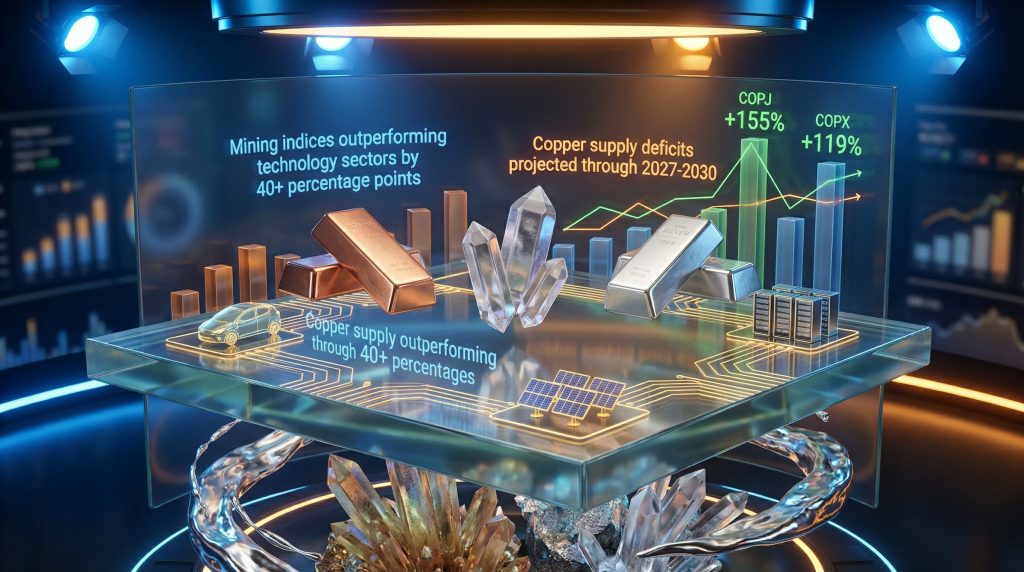

The mathematics underlying this transformation reveal a market in genuine structural transition rather than typical cyclical expansion. European institutional investors have established a net 26% overweight position in mining equities—the highest allocation in four years—while the MSCI Metals and Mining Index delivered a 90% gain since early 2025. These figures reflect recognition that mining investments now function as direct exposure to technological transformation themes rather than traditional defensive commodity positioning.

When big ASX news breaks, our subscribers know first

Understanding the New Mining Supercycle Framework

Contemporary mining investment cycles operate through mechanisms distinct from historical precedents. Traditional supercycles emerged from single-region infrastructure booms—typically Chinese urbanisation driving iron ore price trends through predictable economic expansion phases. Current dynamics reflect multiple simultaneous demand drivers creating sustained rather than episodic consumption patterns.

Technology Infrastructure Requirements:

- AI data centers requiring massive copper wiring and cooling systems

- Electric vehicle charging networks demanding copper-intensive infrastructure

- Grid modernisation projects supporting renewable energy integration

- 5G telecommunications networks increasing silver and copper consumption

The supply response limitations create persistent market tightness. Bloomberg Intelligence analysis indicates copper markets remaining in deficit through 2026, with supply shortfalls potentially worsening from 2025 levels. Unlike previous cycles where high prices incentivised rapid production increases, contemporary mining faces structural constraints from permitting delays, geological challenges, and geopolitical supply chain diversification requirements.

Critical Performance Metrics:

| Sector | 2025 Performance | Primary Drivers | Supply Constraints |

|---|---|---|---|

| Copper | +50% YoY | AI infrastructure, EV charging | 17+ year development cycles |

| Mining Index (MSCI) | +90% YoY | Broad metals demand surge | Permitting bottlenecks |

| European Overweighting | 26% net position | Institutional repositioning | Limited pure-play exposure |

The institutional positioning data reveals strategic rather than tactical allocation decisions. Furthermore, ai transforming drilling blasting mining demonstrates how technology is revolutionising traditional extraction methods. At 26% net overweight, European fund managers maintain substantial conviction despite remaining well below the 38% net overweight held during 2008 peaks, suggesting potential for continued allocation expansion as supply constraints become more apparent.

What Defines a Commodity Supercycle in the Modern Economy?

Modern supercycles differ structurally from historical patterns through demand diversification and correlation breakdown with traditional economic indicators. Research strategist analysis indicates that commodities such as copper and aluminium have become less correlated to economic cycles, transforming from short-term trades dependent on economic growth rates into structural investments driven by technological adoption curves.

Fundamental Cycle Characteristics:

Duration and Scope: Contemporary cycles extend beyond traditional 15-20 year timeframes due to technology adoption requiring decades of infrastructure deployment. Unlike previous cycles driven by single-region industrialisation, current demand emerges from multiple sectors simultaneously—data centres, transportation electrification, renewable energy, and telecommunications infrastructure.

Demand Vector Analysis:

- Artificial Intelligence Infrastructure: Data centre expansion requiring copper-intensive power distribution and cooling systems

- Transportation Electrification: EV adoption creating sustained lithium, nickel, and copper demand

- Grid Modernisation: Renewable energy integration demanding copper for transmission infrastructure

- Industrial Automation: Robotics and manufacturing automation increasing silver and rare earth consumption

The correlation breakdown mechanism operates through technology-driven demand creating consumption patterns independent of business cycle fluctuations. AI data centres require consistent power infrastructure regardless of economic expansion phases, while EV adoption follows government mandate timelines rather than consumer discretionary spending cycles.

"The transition strategies now involve investors purchasing mining assets to gain exposure to AI themes, representing a fundamental shift from defensive commodity positioning to growth-oriented technological investment."

Why Mining Stocks Are Outperforming Traditional Growth Sectors

Valuation analytics reveal a significant disconnect between mining stock performance and traditional valuation metrics. The Stoxx 600 Basic Resources index trades at a forward price-to-book ratio of approximately 0.47, representing a 20% discount to the long-term 0.59 ratio and substantially below prior cycle peaks exceeding 0.7.

This valuation gap persists despite material improvements in strategic relevance for natural resources, creating opportunity for investors willing to position ahead of multiple recognition. However, mercuria betting copper growth strategies highlight institutional confidence in the sector's long-term prospects.

Portfolio Allocation Dynamics:

Inflation Hedge Characteristics: Mining investments provide direct commodity exposure offering protection against monetary policy uncertainty while maintaining equity upside participation.

Thematic Exposure Without Technology Volatility: Investors gain AI and energy transition exposure through mining stocks while avoiding the valuation multiples and competitive risks associated with technology sector positioning.

Geographic Diversification Benefits: Mining assets provide international exposure and currency diversification unavailable through concentrated technology holdings.

Institutional Repositioning Evidence:

The fund manager rush to "buy the dip whenever weak data knocks mining stocks" indicates recognition that cyclical economic concerns should not drive long-term positioning given structural demand tailwinds. This behavioural shift represents acknowledgement that mining stocks now capture growth themes previously associated exclusively with technology sectors.

Major mining companies demonstrate the structural demand thesis through strategic repositioning. While firms like BHP Group and Rio Tinto still derive bulk earnings from iron ore, which faces headwinds from the collapse of China-led demand cycles, companies offering pure exposure to copper command premium valuations reflecting investor preference for concentrated energy transition exposure.

Which Mining Investment Strategies Are Gaining Institutional Favour?

Investment strategy bifurcation reflects different approaches to capturing supercycle opportunities while managing inherent volatility. Analysis of institutional positioning reveals preference patterns based on risk tolerance, thematic conviction, and portfolio construction requirements. In addition, the big pivot critical minerals strategy demonstrates how companies are repositioning for future demand.

Pure-Play Commodity Exposure:

Copper-focused miners benefit from energy transition positioning and AI infrastructure demand convergence. Companies like Freeport-McMoRan and Antofagasta represent the few firms offering pure exposure to copper, making them attractive for investors seeking concentrated thematic positioning. These companies command valuation premiums reflecting scarcity value for direct copper exposure.

Diversified Major Miners:

Broad commodity exposure provides stability and M&A optionality while maintaining participation in structural demand trends. However, iron ore exposure creates sensitivity to Chinese economic performance, potentially limiting upside participation during periods of China-specific weakness.

M&A-Driven Strategy Preferences:

Companies' increasing preference for "buy over build" creates strategic investment opportunities. Anglo American's acquisition of Teck Resources and potential merger discussions between Rio Tinto and Glencore demonstrate major capital deployment toward scale and portfolio optimisation, particularly in copper assets.

The industry's capital-intensive nature drives this trend, but analysis attributes M&A activity specifically to miners' willingness to pursue strategic positioning during supply deficit periods. This backdrop supports higher commodity prices and valuation multiple expansion for companies positioned as acquisition targets.

Risk Management Considerations:

Some investment professionals express caution regarding rally sustainability. When asset prices move in non-linear or parabolic patterns, concerns arise about momentum-driven positioning creating volatility risks. However, fundamental valuation analysis suggests mining stocks remain inexpensive despite recent performance.

"The miners are very inexpensive relative to fundamental improvement, creating opportunities for scale-up positioning during pullbacks whilst maintaining exposure to elevated commodity price environments."

How Supply Chain Disruptions Are Accelerating the Supercycle

Supply constraints operate through multiple mechanisms creating sustained market tightness beyond typical cycle patterns. Mine development faces unprecedented bottlenecks from regulatory, technical, and capital availability challenges that extend project timelines substantially beyond historical norms.

Development Timeline Constraints:

Modern mining projects require average development periods exceeding 15-17 years from discovery to production. Environmental permitting processes have extended project schedules significantly, while capital intensity demands larger financing packages during periods of elevated interest rates. Technical expertise shortages in critical mining regions compound these delays.

Geological Reality Factors:

The discovery rate for world-class mineral deposits has declined substantially over recent decades. Remaining deposits often require extraction from lower-grade ores using more complex and expensive processing technologies. These technical challenges increase both capital requirements and operational complexity.

Strategic Asset Consolidation:

M&A activity reflects recognition that acquisition provides faster access to production than development. Major mining companies increasingly favour purchasing proven reserves rather than funding exploration and development programmes. This preference creates premium valuations for companies controlling tier-one assets in stable jurisdictions.

Geopolitical Supply Chain Considerations:

Western governments' emphasis on supply chain diversification away from dominant producing regions creates additional regional demand. Reshoring initiatives and "friend-shoring" policies increase demand premiums for production from politically stable jurisdictions, supporting sustained elevated pricing.

The next major ASX story will hit our subscribers first

What Are the Primary Risk Factors for Mining Supercycle Investors?

Despite structural demand drivers, mining investments face significant cyclical and technical risks that require careful portfolio management. Understanding these risk factors enables more informed position sizing and timing decisions. For instance, the copper supercycle investment outlook provides crucial insights into long-term market dynamics.

Economic Sensitivity Concerns:

Chinese Economic Exposure: Iron ore demand remains sensitive to Chinese economic performance, affecting diversified miners with substantial iron ore production. Economic slowdown in China creates headwinds for traditional commodity demand even as energy transition metals benefit from structural trends.

Interest Rate Sensitivity: Capital-intensive mining operations face financing cost pressures during periods of elevated interest rates. Higher discount rates also affect the present value calculations for long-duration mining projects.

Currency Fluctuation Risks: International mining operations face revenue and cost exposure to currency movements, particularly in emerging market jurisdictions where many mining assets operate.

Technical and Momentum Risks:

Non-Linear Price Movement Warnings: Rapid price appreciation in both commodities and mining stocks suggests potential speculative activity. Historical precedent indicates that parabolic price movements often precede sharp corrections, requiring careful attention to position sizing and exit strategies.

Correlation Breakdown Risks: While reduced correlation with economic cycles benefits mining stocks during economic uncertainty, this correlation could re-emerge during severe economic downturns, eliminating perceived diversification benefits.

Regulatory and Operational Risks:

Changes in mining taxation, environmental regulations, or permitting requirements can significantly impact project economics. Political instability in key mining jurisdictions creates operational risks for companies with concentrated geographic exposure.

How to Position for Long-Term Supercycle Benefits

Strategic positioning for supercycle participation requires balancing growth potential with risk management whilst maintaining adequate diversification across commodities, geographies, and company types. Furthermore, copper uranium investment opportunities in Australia and Canada present compelling regional exposure options.

Conservative Allocation Approach (20-30% mining exposure):

- Focus on Major Diversified Miners: Companies like BHP and Rio Tinto provide broad commodity exposure with established dividend yields and strong balance sheets

- Emphasise Political Stability: Prioritise operations in mining-friendly jurisdictions with predictable regulatory environments

- Include Precious Metals: Gold and silver provide portfolio insurance characteristics during monetary uncertainty

- Balance Sheet Quality: Emphasise companies with low debt levels and strong cash generation capabilities

Aggressive Growth Strategy (40-50% mining exposure):

- Concentrate on Pure-Play Specialists: Focus on companies offering concentrated exposure to critical metals like copper, lithium, and rare earths

- Include Junior Mining Companies: Accept higher volatility for potential outsized returns from successful exploration and development

- Energy Transition Focus: Emphasise metals directly benefiting from electrification and renewable energy trends

- M&A Positioning: Target companies likely to become acquisition candidates due to strategic asset control

Geographic and Commodity Diversification:

Regional Risk Management:

- Balance exposure across mining-friendly jurisdictions (Canada, Australia, Chile, Botswana)

- Consider currency hedging for international exposure

- Monitor regulatory stability in key operating regions

- Evaluate geopolitical risks affecting supply chains

Commodity Mix Optimisation:

- Combine industrial metals (copper, aluminium) with precious metals (gold, silver)

- Include energy transition materials (lithium, cobalt, rare earths)

- Maintain exposure to uranium for nuclear energy themes

- Consider agricultural commodity exposure for portfolio completion

Future Outlook: Sustainability of the Mining Supercycle

Long-term demand projections support sustained supercycle potential through multiple converging trends that appear likely to persist for decades rather than years. The combination of artificial intelligence expansion, transportation electrification, and renewable energy deployment creates diversified demand vectors unlikely to reverse simultaneously.

2026-2030 Demand Catalysts:

AI Infrastructure Expansion: Goldman Sachs projects gold reaching $5,400 by end-2026—approximately 8% above current levels—reflecting monetary policy and geopolitical concerns. Similar bullish projections exist for copper as AI data centre expansion accelerates globally.

Electric Vehicle Adoption: Government mandates for EV adoption create predictable demand curves for lithium, nickel, and copper regardless of consumer preference changes. These mandates provide demand visibility extending through the 2030s.

Grid Modernisation Requirements: Renewable energy integration requires massive copper infrastructure for transmission and distribution systems. These projects follow regulatory timelines rather than economic cycles. Moreover, analysis from mining stock supercycle prospects reinforces the structural nature of these trends.

Supply Response Limitations:

Despite elevated prices, supply increases face persistent structural constraints. The number of world-class mineral deposits discovered annually has declined significantly, whilst environmental regulations restrict new mine development in many jurisdictions.

Technical Production Challenges:

- Lower-grade ore deposits requiring more complex extraction technologies

- Water scarcity affecting mining operations in key regions

- Skilled labour shortages in critical mining disciplines

- Infrastructure limitations in remote mining locations

Investment Implications:

The upside drivers for commodities appear more powerful and diversified than historical supercycles, supporting portfolio allocation toward mining investments. However, the rapid price appreciation in many metals and mining stocks requires careful position management and attention to valuation sustainability.

Strategic investors positioning for this structural transformation must balance growth opportunities with inherent volatility whilst maintaining appropriate diversification across commodities, geographies, and company types. The mining stocks supercycle represents a fundamental shift driven by technological transformation rather than traditional economic cycles, creating opportunities for investors willing to navigate the complexity of structural change.

The convergence of artificial intelligence infrastructure demands, energy transition requirements, and supply chain constraints has created mining investment dynamics that differ substantially from historical patterns. Success requires understanding these structural forces whilst maintaining discipline around risk management and portfolio construction principles.

Looking to Capitalise on the Mining Supercycle's Next Discovery?

Discovery Alert's proprietary Discovery IQ model identifies significant ASX mineral discoveries in real-time, transforming complex mining announcements into actionable investment opportunities before broader market recognition occurs. With institutional investors establishing record overweight positions in mining equities, understanding which discoveries could deliver exceptional returns has never been more critical for positioning ahead of this structural transformation.