May 12, 2026

When Geopolitics Rewrites the Trading Playbook

In financial markets, the most powerful signals are rarely found in earnings reports or central bank minutes alone. Sometimes they emerge from the trading floor itself, encoded in a handful of letters that capture a collective conviction about where the world is heading. The acronym has become one of Wall Street's most efficient tools for transmitting complex macro bets across desks, platforms, and asset classes at speed. When a new one takes hold, it is worth paying close attention to the thesis underneath it.

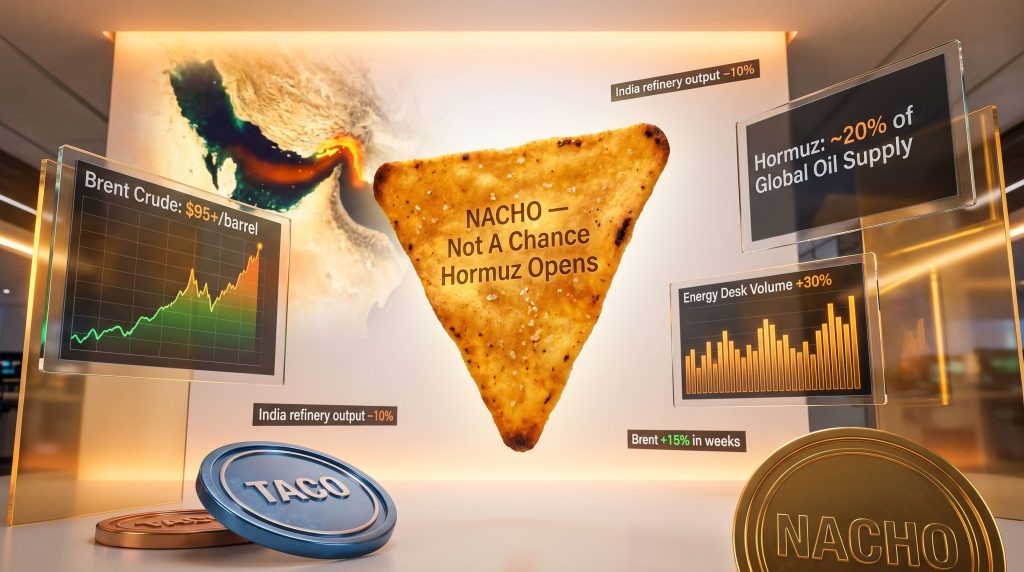

The latest to grip global markets is the NACHO Wall Street acronym, a phrase that encodes a deeply pessimistic reading of Middle East geopolitics and its consequences for energy prices worldwide.

When big ASX news breaks, our subscribers know first

What the NACHO Wall Street Acronym Actually Means

NACHO stands for "Not A Chance Hormuz Opens", a trader-coined phrase that crystallised into a market narrative after Bloomberg energy columnist Javier Blas shared it on social media in late April 2026, attributing the term to an unnamed trader. The phrase is deceptively simple but carries an enormous amount of macro freight within it.

At its core, the NACHO thesis rests on a single structural assumption: that the Strait of Hormuz, one of the world's most critical energy chokepoints, will remain effectively blocked for a prolonged and uncertain period, sustaining elevated global oil prices across multiple asset classes.

The geopolitical backdrop is as significant as the acronym itself. Following the conclusion of US military operations against Iran, known as Operation Epic Fury, which launched in February 2026, US Secretary of State Marco Rubio confirmed the military action had formally concluded. However, the downstream consequences have proven far stickier than the operation itself. The strait remains functionally blocked, a fragile ceasefire is holding only in the loosest sense, and markets have yet to price in any credible pathway toward full de-escalation.

The NACHO thesis is not merely a commentary on oil prices. It is a directional bet on geopolitical irreversibility, the idea that the forces now shaping the Hormuz situation cannot be reversed by a single press conference or diplomatic handshake.

The Strait of Hormuz carries approximately 20% of the world's total oil supply through a narrow maritime corridor between Iran and Oman. When that corridor is disrupted, the transmission into global energy markets is immediate and severe. Brent crude has risen more than 15% since the blockade intensified, pushing above $95 per barrel, while Indian refineries have already moved to cut output by approximately 10% in response to constrained supply availability. Furthermore, the broader crude oil price trends emerging from this disruption are reshaping energy investment strategies globally.

From TACO to NACHO: Understanding the Strategic Inversion

To understand why the NACHO trade matters, it is essential to first understand the framework it replaced.

TACO, standing for "Trump Always Chickens Out", was born during the height of the US tariff cycle and became one of the defining macro trades of its era. The underlying logic was straightforward: buy the dip when aggressive tariff announcements were made, then sell into the rally when the inevitable reversal materialised. The strategy exploited the predictable gap between presidential rhetoric and policy follow-through, and it proved profitable across multiple cycles as the pattern repeated. In addition, understanding the broader US-China trade war impacts helps contextualise how the TACO framework developed in the first place.

TACO was, fundamentally, a bet on political predictability. It assumed that domestic political incentives would always win out over escalatory rhetoric, and that a single decision-maker, the US President, held the primary variable in the trade.

NACHO represents something structurally different, and far more complex.

| Dimension | TACO Trade | NACHO Trade |

|---|---|---|

| Core Assumption | Policy reversal is likely | Gridlock is the base case |

| Primary Asset Focus | Equities, tariff-sensitive sectors | Energy futures, oil volatility |

| Trade Direction | Buy dips, fade threats | Long energy, buy volatility |

| Risk Driver | US domestic policy decisions | Middle East geopolitical stalemate |

| Time Horizon | Short-term (days to weeks) | Medium-term (weeks to months) |

| Key Variable | Presidential decision-making | Third-party geopolitical actors |

| Sentiment Tone | Cynical optimism | Structural pessimism |

The critical difference is the introduction of third-party geopolitical actors whose behaviour is not governed by US domestic political incentives. Iran, regional proxies, and the broader constellation of Persian Gulf stakeholders operate on entirely different decision-making calculus than a US administration facing re-election pressures or domestic economic feedback loops. The TACO playbook had no mechanism for pricing this kind of risk, and that is precisely where it broke down.

The Strait of Hormuz: Why This Chokepoint Drives Global Markets

Understanding why the NACHO trade has generated such rapid institutional adoption requires appreciating just how structurally irreplaceable the Strait of Hormuz is within global energy logistics.

The strait is a narrow waterway, roughly 33 kilometres wide at its narrowest navigable point, through which tankers carry crude oil from Saudi Arabia, the UAE, Kuwait, Iraq, and Iran to markets across Asia and Europe. There is no easy substitute for this route at the volumes the global economy currently demands.

Key facts about the Hormuz chokepoint:

- Approximately 20% of all globally traded oil transits through the strait

- It is the primary export corridor for Gulf Cooperation Council (GCC) nations

- Alternative routes such as the East-West Pipeline across Saudi Arabia have limited spare capacity relative to total Hormuz flows

- Tanker rerouting around the Cape of Good Hope adds significant time and cost penalties to delivery timelines

- Strategic petroleum reserves in consuming nations are finite buffers, not structural replacements for lost supply

The combination of these factors means that even a partial or functional blockade, rather than a complete closure, can sustain meaningful supply-side pressure on global oil prices for extended periods. Markets are not pricing a scenario where Hormuz closes completely. They are pricing a scenario where uncertainty persists and supply flows remain materially reduced from pre-crisis levels. Consequently, geopolitical risk in mining and broader commodity sectors is also rising in tandem with energy market instability.

Second-Order Consequences Spreading Across Asset Classes

The NACHO Wall Street acronym may have originated on energy trading desks, but its implications are radiating across a much broader universe of assets and economic variables.

How Is Inflation Being Affected?

Sustained crude prices above $95 per barrel represent a meaningful cost-push inflationary shock for energy-importing economies. Central banks in Europe and across Asia face a particularly difficult policy environment: rising energy-driven inflation without the demand-side growth that would normally justify rate increases. This stagflationary dynamic complicates monetary policy transmission and reduces room for rate-cutting cycles that markets had previously anticipated.

Emerging Market Currency Pressure

Nations that import the majority of their energy needs and hold limited foreign exchange reserves face compounding currency stress. A combination of higher import bills denominated in US dollars and reduced export competitiveness from elevated manufacturing input costs creates dual pressure on current account balances.

Shipping and Supply Chain Disruption

Higher energy costs feed directly into shipping rates, which remain one of the primary transmission mechanisms for commodity price shocks across global supply chains. Agricultural commodity prices are particularly sensitive given the fuel intensity of modern food production and logistics. However, the full extent of these disruptions will depend on how long the Hormuz situation persists.

Energy Equity Outperformance

Energy desk trading volumes reportedly rose approximately 30% following the widespread adoption of the NACHO narrative, reflecting both directional positioning and increased hedging activity from corporates exposed to energy price volatility. Integrated energy majors and upstream producers have become focal points for capital rotation away from sectors with high energy input cost sensitivity. For investors assessing broader exposure, the relationship between tariffs and investment markets adds another layer of complexity to portfolio positioning in this environment.

Energy markets do not price what is happening today. They price expectations about supply and demand several months forward. The NACHO trade is effectively a bet that forward expectations will remain elevated, not just spot prices.

The Trump-Xi Summit as a Potential Turning Point

One variable the NACHO thesis must account for is the scheduled meeting between US President Donald Trump and Chinese President Xi Jinping in Beijing. China occupies a unique position in the Hormuz equation: as one of the world's largest importers of Persian Gulf crude, Beijing has significant and direct economic incentive to push for de-escalation that restores supply flows.

However, the relationship between Chinese diplomatic pressure and Iranian decision-making is complex and historically inconsistent. China's leverage over Iran exists, but the translation of that leverage into specific operational outcomes in the Strait of Hormuz is far from guaranteed or predictable.

Markets appear to be pricing the summit as a low-probability catalyst for rapid NACHO thesis invalidation. That assessment could change if the meeting produces concrete diplomatic commitments with verifiable timelines, but until evidence emerges to the contrary, the base case remains one of continued gridlock.

The next major ASX story will hit our subscribers first

How Traders Are Positioning Around the NACHO Framework

The NACHO Wall Street acronym is not merely a rhetorical device. It is translating into concrete portfolio positioning across multiple asset classes, as reported by MarketWatch in its analysis of the emerging trade thesis.

Primary Energy Positioning:

- Long positions in Brent crude futures and related derivatives

- Increased allocation to crude oil options, particularly call spreads pricing further upside

- Reduced exposure to airlines, petrochemical manufacturers, and energy-intensive industrials

- Rotation into upstream exploration and production equities with high leverage to crude price

Cross-Asset Implications:

- Safe-haven flows into gold and US Treasuries reflecting elevated geopolitical uncertainty premium, with gold as a safe haven attracting particularly strong institutional interest

- Currency positioning favouring exporters of energy commodities over importers

- Potential interest in Middle East sovereign-linked assets benefiting from elevated oil revenues

- Underweighting of emerging market fixed income in nations with high energy import dependence

The speed of adoption is notable. From Javier Blas sharing the phrase on social media in late April 2026 to measurable institutional positioning shifts within weeks represents a compression of the typical narrative adoption cycle, suggesting strong underlying conviction rather than pure momentum chasing.

Is the NACHO Trade a Reliable Signal or a Meme-Driven Distortion?

This question sits at the centre of any serious evaluation of the NACHO Wall Street acronym and its utility as a framework for portfolio decision-making.

Arguments Supporting NACHO as a Legitimate Macro Signal

- The underlying thesis is grounded in observable and documented facts: the strait remains blocked, the ceasefire is fragile, and de-escalation timelines are genuinely unclear

- Oil price responses have been material, not merely psychological, with Brent above $95 per barrel reflecting actual supply-demand adjustment

- Historical precedent from Middle East chokepoint disruptions, including the 1973 Arab oil embargo and Persian Gulf tanker wars of the late 1980s, demonstrates that supply disruptions can sustain elevated energy prices for months to quarters, not days

- Institutional positioning data, rather than purely retail sentiment, appears to be driving the volume increases observed on energy trading desks

Arguments for Caution Around the NACHO Framework

- Acronym-based narratives can become self-reinforcing feedback loops, with positioning itself amplifying price moves beyond what fundamental supply-demand analysis would justify

- A single credible diplomatic breakthrough, particularly from a Trump-Xi summit outcome, could rapidly compress the geopolitical risk premium priced into crude markets

- The NACHO thesis assumes gridlock as the base case, but geopolitical situations of this nature have historically resolved faster than consensus expected, as well as slower

- Crowded trades unwind violently when the consensus is wrong, and the NACHO trade shows signs of becoming crowded within a relatively short adoption window

Traders who anchor too deeply to a single macro narrative acronym face asymmetric risk. The trade works until it does not, and when the thesis breaks, the exit is rarely orderly.

Narrative Economics and the Modern Market Signal

The rise of the NACHO Wall Street acronym reflects something broader about how contemporary financial markets process and price complex information. Shared narrative shorthand has always played a role in market consensus formation, but social media has dramatically accelerated the speed at which a single trader's phrase can achieve institutional resonance.

What was once a process measured in weeks, the gradual diffusion of a trading idea through research notes, conference calls, and floor conversations, now occurs within hours. This compression creates both opportunity and risk. Early movers in a narrative can position ahead of broader institutional adoption and benefit from the resulting flows, but late adopters risk entering a trade at peak crowding precisely when reversal risk is highest. As CNBC notes, the transition from TACO to NACHO represents a meaningful shift in how traders are approaching geopolitical risk in energy markets.

The most durable lesson from both TACO and NACHO is not the acronym itself but the underlying analytical framework it represents. Furthermore, savvy investors will always look past the shorthand to ask whether the geopolitical, policy, or economic conditions genuinely support the thesis, and at what point those conditions are likely to change.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instrument. All market data, price references, and trading volume figures cited are drawn from publicly available reporting and are subject to change. Readers should conduct their own independent research and consult qualified financial advisers before making investment decisions. Geopolitical situations referenced in this article are inherently uncertain, and forward-looking statements or scenario projections carry no guarantee of accuracy or completeness.

Want to Stay Ahead of the Next Major Market-Moving Discovery?

While geopolitical narratives like NACHO reshape energy and commodity markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity data into actionable insights for both short-term traders and long-term investors. Explore why major mineral discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to secure a market-leading edge before the broader market catches on.