July 28, 2026

Africa's Battery Materials Moment: Why One Law Could Reshape the Global Graphite Trade

The global race to secure battery-grade minerals has fundamentally altered the negotiating position of resource-rich developing nations. For decades, African governments watched enormous volumes of raw materials flow offshore while the majority of economic value was captured by downstream processors, manufacturers, and technology companies in Asia and Europe. That dynamic is shifting, and Mozambique's newly enacted mining legislation represents one of the clearest expressions yet of how African resource sovereigns are repositioning themselves within the clean energy supply chain.

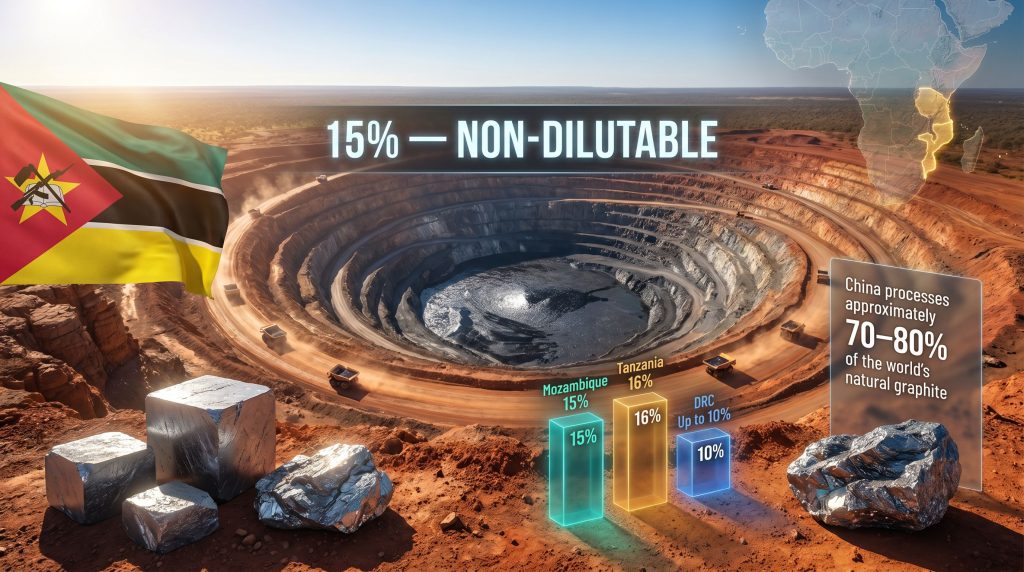

Mozambique's Parliament approved the new mining law in May 2026, with President Daniel Chapo signing it into effect on June 3, 2026. The legislation introduces a mandatory 15% free-carried and non-dilutable equity stake held by the state through the National Mining Company (ENM) across all mining projects at every stage of the value chain. It simultaneously prohibits the export of unprocessed or semi-processed minerals unless covered by a specific ministerial authorisation linked to approved local processing plans. Understanding what the Mozambique mining 15% state stake rule means, who it affects, and what it signals for global battery supply chains requires unpacking both the mechanics of the legislation and the broader context in which it was designed.

When big ASX news breaks, our subscribers know first

What the Mozambique Mining 15% State Stake Rule Actually Requires

The core architecture of the new legislation rests on three interlocking mechanisms: mandatory state equity, export restrictions on raw minerals, and a local development revenue allocation. Each component carries distinct implications for foreign operators.

| Provision | Detail |

|---|---|

| Mandatory State Equity | 15% minimum, free-carried and non-dilutable |

| State Vehicle | National Mining Company (ENM) |

| Scope | All mining projects, any stage of the value chain |

| Raw Mineral Export Ban | Prohibited without specific ministerial authorisation |

| Authorisation Condition | Must be based on approved plans to eventually process locally |

| Local Development Fund | 10% of mining revenues directed to local development |

| Artisanal Mining | Designated zones established under new licensing terms |

| Parliamentary Approval | Passed May 2026; signed by President Daniel Chapo, June 3, 2026 |

What "Free-Carried and Non-Dilutable" Means in Practice

The phrase free-carried means the ENM acquires its 15% stake without contributing capital toward project development costs. The entire financial burden of exploration, feasibility, construction, and commissioning falls on the remaining equity holders, who collectively bear 100% of the capital expenditure while owning only 85% of the asset.

Non-dilutable takes this a step further. It means that future capital raises, rights issues, or debt-to-equity conversions cannot reduce ENM's ownership below 15%. In project financing structures that rely on equity dilution to manage staged capital deployment, this creates a structural constraint that must be factored into deal architecture from the outset.

The combination of free-carried and non-dilutable provisions effectively increases the per-unit cost of ownership for private investors, compressing returns before operational revenues have been generated.

Does the Law Apply to Existing Operations?

One of the most consequential questions the legislation leaves unanswered is whether its provisions apply retroactively to mines already operating under long-term stability agreements. According to Reuters reporting from June 4, 2026, it was not immediately clear whether existing operations would be captured by the new rules, and Mozambique's Mines Ministry was not available to provide clarification at the time of publication.

This ambiguity is not a minor technical detail. Mozambique's largest mining operations, including Syrah Resources' Balama graphite complex and Gemfields' Montepuez ruby mine, operate under negotiated development agreements that were structured under the prior legislative framework. Whether these agreements provide legal insulation from the new requirements, or whether ENM will seek to renegotiate equity positions, will be among the first legal battles to watch as implementation unfolds.

How Mozambique's Law Compares Across the African Mining Landscape

Mozambique's Mozambique mining 15% state stake rule does not exist in isolation. It is part of a discernible continental pattern in which resource-holding governments are asserting greater control over mineral wealth, particularly those minerals identified as critical minerals demand in the global energy transition.

| Country | Mandatory State Equity | Export Restrictions | Key Commodity |

|---|---|---|---|

| Mozambique | 15% (free-carried, non-dilutable) | Raw mineral export ban with ministerial exemptions | Graphite, coal, rubies |

| Zimbabwe | Varies by sector | Full ban on all raw minerals and lithium concentrates | Lithium |

| Democratic Republic of Congo | Up to 10% (royalty-based model) | Cobalt processing requirements | Cobalt, copper |

| Tanzania | 16% free-carried interest | Local beneficiation mandated | Gold, tanzanite |

| Zambia | Negotiated case-by-case | Processing incentives, no hard ban | Copper |

The Pan-African Resource Nationalism Pattern

Zimbabwe's ban on exports of all raw minerals and lithium concentrates established a significant regional precedent, demonstrating that outright export prohibitions were a credible policy tool rather than an empty political gesture. The Congo cobalt export ban similarly demonstrated how African producers could leverage resource control to reshape global commodity dynamics. Furthermore, the DRC, as the world's leading cobalt producer and a major copper supplier, has moved toward requiring greater in-country processing as a condition of export licensing.

What differentiates Mozambique's approach is the structural emphasis on permanent, non-dilutable equity rather than royalty escalation or windfall profit taxes. This model more closely resembles Tanzania's framework, where the government holds a 16% free-carried interest, than the DRC's royalty-centric system. The permanence of the equity stake means Mozambique's government participates in long-term asset appreciation, not just production-phase revenue, which changes the risk-reward calculus for the state significantly.

Resource nationalism in this context is better understood as resource industrialisation policy. The goal is not simply to capture more revenue from existing operations but to redirect mineral flows toward domestic value creation.

Mozambique's Mining Assets and Why They Matter Globally

The Graphite Dimension: A Tier-One Producer in a Critical Material

According to the United States Geological Survey, Mozambique ranks as the world's third-largest graphite producer, sitting behind China and Madagascar in global output. This ranking carries strategic weight that far exceeds Mozambique's size or economic profile, because natural graphite serves as the primary anode material in lithium-ion batteries powering electric vehicles and grid-scale energy storage. Indeed, the global graphite shortage affecting battery supply chains makes Mozambique's reserves all the more strategically significant.

The Balama graphite operation in northern Mozambique, operated by Syrah Resources, hosts one of the largest graphite deposits on earth. What makes Balama particularly significant from a supply chain perspective is the quality of its output. Mozambican graphite deposits are predominantly high-purity large-flake graphite, which commands premium pricing in battery-grade applications compared to lower-grade amorphous graphite found elsewhere.

Large-flake graphite undergoes a purification and spheronisation process to produce spherical graphite, the actual anode material used in battery cells, and higher starting purity reduces processing costs and improves final product quality.

Montepuez: The World's Largest Ruby Mine

Northern Mozambique is also home to the Montepuez ruby mine, owned by Gemfields and recognised as the largest ruby-producing operation in the world. While rubies occupy a different market segment to battery materials, Montepuez represents a high-value asset directly exposed to the new legislation's equity and export provisions. Coloured gemstone exports from Mozambique generate significant foreign exchange earnings, and the application of local processing requirements to rough ruby exports could substantially alter trade flows to cutting and polishing centres in India, Thailand, and Sri Lanka.

Coal: The Legacy Asset Question

Mozambique's northern Tete Province contains significant thermal and coking coal deposits that were previously developed by Rio Tinto and Brazil's Vale before both companies exited amid challenging market conditions. While coal sits outside the battery materials narrative, these assets represent the historical foundation of Mozambique's mining sector and remain relevant to any assessment of how the new law interacts with legacy infrastructure, existing workforce structures, and regional economic development obligations.

The Local Processing Mandate and Its Economic Logic

Why Raw Exports Leave Value on the Table

The prohibition on exporting unprocessed or semi-processed minerals reflects a straightforward economic argument: raw material extraction captures only a fraction of the total value generated across a mineral supply chain. In the graphite sector specifically, mining and basic concentration typically represents the lowest-margin stage of production. The higher-value stages, including purification to battery-grade specifications, spheronisation, and coating, occur almost entirely in China, which processes an estimated 70–80% of the world's natural graphite into battery-grade anode material.

From Mozambique's perspective, this processing concentration means that Chinese manufacturers have historically captured the majority of economic value derived from Mozambican graphite, whilst Mozambique retained only mining royalties, basic employment income, and export taxes. The China battery supply chain dominance is precisely the dynamic the new law attempts to disrupt by requiring that any export exemptions be tied to credible plans for eventual domestic processing.

Infrastructure Realities and the Implementation Gap

The local processing ambition faces substantial practical constraints:

- Mozambique's electricity infrastructure is underdeveloped, with significant portions of the population lacking reliable grid access, a challenge for energy-intensive mineral processing

- Road and rail connectivity to the northern mining provinces where graphite and ruby assets are concentrated remains limited

- A domestic industrial workforce capable of operating advanced mineral processing facilities does not yet exist at scale

- Access to processing chemicals, reagents, and technical equipment requires reliable import supply chains

These constraints explain why the legislation incorporates a ministerial exemption mechanism rather than imposing an immediate and unconditional export ban. The exemption pathway, conditioned on approved local processing plans, creates a transitional bridge whilst the infrastructure foundations for in-country processing are established.

The exemption mechanism is not a loophole. It is an acknowledgement that resource industrialisation is a decade-long project, not a policy switch. The question for investors is who bears the cost of building the bridge.

The 10% Local Development Fund

Beyond equity and processing requirements, the legislation allocates 10% of mining revenues to a local development fund. For international operators, this represents an additional fiscal obligation layered on top of existing royalty and tax frameworks. Mozambique's proposed mining reforms, which were widely covered ahead of the law's passage, signalled these provisions were coming, yet the specific percentage and governance structure of the fund will significantly influence how it is perceived by investors.

What the 15% Rule Means for Foreign Mining Investment

Modelling the Impact on Project Returns

To illustrate the financial mechanics of the free-carried equity provision, consider a hypothetical mid-tier graphite development with the following characteristics:

- Total capital cost: $400 million

- Pre-law projected IRR: 18%

- ENM equity stake: 15% (free-carried, non-dilutable)

- Private investor equity: 85%

Under this structure:

- The private investor group bears 100% of the $400 million capital requirement while owning only 85% of the asset

- The effective capital cost per percentage point of private ownership increases by approximately 17.6% relative to a structure without state participation

- Revenue sharing from production is split 85/15 between private investors and ENM

- Future capital raises cannot dilute ENM below 15%, limiting equity financing flexibility

- Project IRR for private investors compresses depending on the royalty, tax, and development fund obligations layered above the equity structure

This scenario illustrates why grandfathering clarity will be among the most urgent questions for existing project operators and why new project proponents will need to build ENM equity costs into feasibility models from day one.

The Non-Dilutability Constraint on Project Finance

Non-dilutability creates a particular challenge in project finance structures that rely on equity dilution as a risk management mechanism. In staged development models, early-phase investors often accept dilution as later-phase capital is raised, with dilution protections negotiated as a commercial matter. ENM's statutory immunity from dilution means that all dilution from future capital rounds falls entirely on private equity holders, increasing their sensitivity to development cost overruns and removing a common financing flexibility tool.

The next major ASX story will hit our subscribers first

Existing Operations, Long-Term Agreements, and Regulatory Ambiguity

The most immediate risk for the mining sector is not the law itself but the uncertainty surrounding its application. Mozambique's major mining operations operate under development agreements negotiated with the government over many years, often containing stabilisation clauses that are intended to protect investors from subsequent legislative changes. Whether these clauses provide effective protection against the new equity and processing requirements is a question that will ultimately be resolved through legal interpretation and, potentially, government-to-company negotiation.

Several scenarios are plausible:

- Full grandfathering: Existing operations are explicitly exempted until their current agreements expire

- Negotiated transition: The government invites existing operators to renegotiate agreements to incorporate ENM participation over a defined transition period

- Immediate application: The law is applied to all operations regardless of existing agreements, triggering potential arbitration claims

The Mines Ministry's silence at the time of the law's announcement suggests that implementation guidance is still being developed, which is itself informative. Regulatory ambiguity of this nature typically depresses new investment commitments until clarity is achieved, as capital allocators require legal certainty before committing to long-horizon projects.

Global Supply Chain Implications: Graphite, Batteries, and the China Variable

Why Mozambique's Policy Matters Beyond Its Borders

The global battery supply chain's dependence on Chinese graphite processing creates a structural vulnerability that policymakers in the United States, Europe, Japan, and South Korea have been attempting to address through supply chain diversification strategies. Mozambique's Balama deposit has been identified as one of the most viable non-Chinese sources of natural graphite at meaningful scale, making it a strategically important asset for the battery raw materials market as manufacturers seek to reduce exposure to Chinese processing capacity.

China processes approximately 70–80% of the world's natural graphite into battery-grade anode material. Any policy change that redirects Mozambican graphite toward mandatory domestic processing, rather than export to established refining hubs, has direct implications for the timeline and cost of supply chain diversification efforts by non-Chinese battery manufacturers.

The Processing Mandate's Redirection Risk

If Mozambique's local processing mandate is enforced without adequate exemptions, graphite from Balama could face export delays or redirected trade flows while domestic processing infrastructure is developed. In the near to medium term, this could tighten global supply of unprocessed flake graphite, potentially benefiting producers in other jurisdictions including Madagascar, Canada, and Tanzania.

However, the ministerial exemption mechanism suggests that a complete disruption of graphite export flows is unlikely in the short term. More probable is a gradual renegotiation of offtake agreements to incorporate local processing commitments, with exemptions providing a bridge period. Furthermore, Mozambique's move to tighten mining rules signals a long-term policy direction that battery manufacturers dependent on Mozambican graphite supply will need to incorporate into their supply planning.

Frequently Asked Questions: Mozambique Mining Law and the 15% State Stake Rule

What is the Mozambique mining 15% state stake rule?

It is a legislative provision within Mozambique's new mining law, signed by President Daniel Chapo in June 2026, requiring the state to hold a minimum 15% equity stake in all mining projects through the National Mining Company. The stake is free-carried, meaning the state contributes no capital, and non-dilutable, meaning it cannot be reduced by future equity raises.

Which government body holds the state's equity stake?

The National Mining Company, known by its Portuguese acronym ENM, is the designated vehicle through which the Mozambican state holds its mandatory participation in mining projects.

Does the new mining law ban all mineral exports from Mozambique?

No. The law prohibits the export of unprocessed or semi-processed minerals as a default position, but provides for ministerial authorisation of exports where the applicant has approved plans to eventually process minerals domestically. It is an export restriction with a conditional exemption mechanism, not an absolute ban.

Will existing mining projects be required to comply with the 15% rule?

This remains unclear. Mozambique's Mines Ministry had not provided guidance on the application of the new law to existing operations covered by long-term development agreements at the time of the law's signing.

What percentage of mining revenues must go to local development under the new law?

The legislation requires that 10% of mining revenues be directed to a local development fund.

How does Mozambique's mining law compare to Zimbabwe's mineral export ban?

Zimbabwe implemented a comprehensive ban on exports of all raw minerals and lithium concentrates, covering all unprocessed materials without an exemption mechanism. Mozambique's approach is more graduated, prohibiting raw mineral exports as a default but allowing ministerial exemptions conditioned on local processing commitments.

Key Takeaways: What the Mozambique Mining Law Signals for the Decade Ahead

Resource Sovereignty as Industrial Strategy

The most important analytical framing for Mozambique's new legislation is not resource nationalism in its traditional extractive sense, but resource industrialisation as a deliberate development strategy. The combination of mandatory state equity, processing requirements, and local development funding reflects a coherent policy logic: capture equity upside, redirect mineral value toward domestic processing, and ensure communities near mining operations receive a defined share of economic benefits.

The Investment Calculus Has Changed, Not Collapsed

Mozambique retains world-class mineral assets, particularly in graphite, that will remain strategically relevant regardless of policy changes. Tier-one deposits attract capital even under more demanding regulatory frameworks, as the global battery materials supply chain cannot simply bypass one of the world's largest and highest-quality graphite provinces. What changes is the return profile, the financing structure, and the legal risk premium that investors must incorporate into project economics.

What to Monitor as Implementation Proceeds

Investors, operators, and supply chain strategists should track the following developments closely:

- Official guidance from the Mines Ministry on the application of the law to existing operations

- ENM's institutional capacity to fulfil its role as a meaningful equity partner across multiple projects simultaneously

- The pace and terms of ministerial exemptions granted for graphite and other mineral exports

- Legal challenges or arbitration proceedings initiated by existing operators under stabilisation clause provisions

- Infrastructure investment announcements linked to domestic mineral processing ambitions

- The response of Syrah Resources and Gemfields, as the operators of Mozambique's highest-profile mining assets, to the new legislative framework

The trajectory of Mozambique's mining sector over the next decade will be shaped less by the existence of the Mozambique mining 15% state stake rule itself and more by the quality of its implementation, the credibility of ENM as an institutional partner, and the government's ability to balance sovereign resource ambitions with the investment conditions necessary to develop world-scale mineral deposits. Those three variables remain, for now, an open question.

This article contains forward-looking analysis and scenario modelling based on publicly available information. It does not constitute financial or investment advice. Readers should conduct independent due diligence before making any investment decisions related to companies or projects operating in Mozambique or the broader battery materials sector.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including graphite and other critical battery materials — instantly translating complex data into actionable investment insights for traders and long-term investors alike. Explore historic discoveries and their extraordinary returns on Discovery Alert's dedicated discoveries page, or begin your 14-day free trial today to position yourself ahead of the market.