June 27, 2026

The Battery Materials Race Is Rewriting the Rules of African Mining

Across the African continent, a quiet but consequential restructuring of mineral governance is underway. The catalyst is not a commodity boom in the traditional sense, but something more structurally significant: the global electrification of transport and energy storage has transformed a handful of previously undervalued minerals into strategic assets with geopolitical weight. Nations that once accepted standard royalty arrangements and export-oriented extraction models are now rewriting their legislative frameworks to capture a far greater share of the value embedded in their resource endowments.

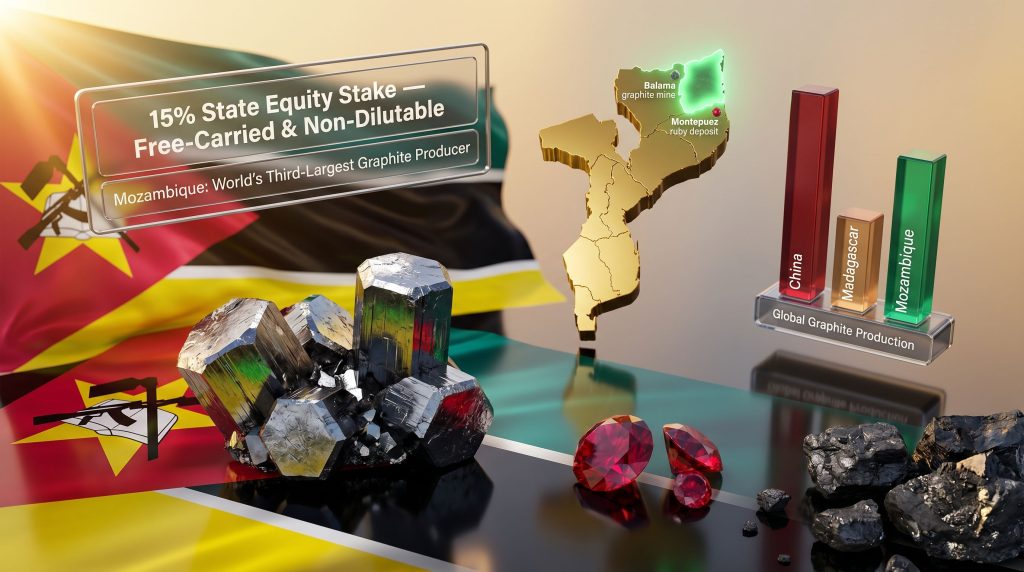

Mozambique's newly enacted mining legislation sits squarely within this continental realignment. Signed into law by President Daniel Chapo following parliamentary approval in May, the legislation introduces mandatory state equity participation in all mining projects and prohibits the export of unprocessed or semi-processed mineral products under standard conditions. For a country ranked as the world's third-largest graphite producer, and one hosting what is widely considered one of the planet's largest graphite deposits, these reforms carry substantial implications for global battery supply chains, foreign investment calculus, and the future of mineral value creation in Sub-Saharan Africa.

Understanding the mechanics of this legislation, its commercial consequences, and its position within a broader wave of African resource nationalism is essential for mining investors, battery material consumers, and policy observers navigating the emerging minerals economy. Furthermore, the critical minerals demand driving these reforms continues to reshape how governments across the continent approach sovereign resource control.

When big ASX news breaks, our subscribers know first

What the Mozambique Mining Law 15% State Stake and Local Processing Mandate Actually Requires

Breaking Down the Equity Participation Provisions

At the core of the new legislation is a requirement that the Mozambican state, acting through the Empresa Nacional de Mineração (ENM), hold a minimum 15% equity stake in every mining project operating within the country. This stake carries two critical structural characteristics that distinguish it from conventional government equity arrangements: it is free-carried and non-dilutable.

Free-carried equity means the state receives its ownership interest without contributing any capital toward project development, construction, or ongoing operations. The financial burden of building and sustaining a mine falls entirely on private investors, while the government participates in profit distributions proportional to its stake once production commences. The non-dilutable provision ensures that ENM's 15% cannot be reduced through any subsequent capital raise, restructuring event, or shareholder dilution mechanism, meaning the government's interest is permanently protected regardless of how the project's ownership evolves over time.

| Provision | Detail |

|---|---|

| Minimum state equity stake | 15% in all mining projects |

| Participation vehicle | National Mining Company (ENM) |

| Equity structure | Free-carried and non-dilutable |

| Applicability across value chain | At any stage of the mining value chain |

| Export restriction | Ban on unprocessed and semi-processed mineral exports |

| Exemption pathway | Ministerial authorization with approved local processing plan |

| Applicability to existing mines | Legally unclear as of enactment |

The government notice describing the law's purpose, dated June 3, framed the reforms as strengthening Mozambique's capacity to manage strategic resources in defence of the national interest, a formulation that signals the ideological orientation driving these changes rather than simply a revenue maximisation objective. This language mirrors similar justifications used by other African governments implementing comparable frameworks, suggesting a coordinated if informal convergence in resource governance philosophy across the continent.

How the Local Processing Mandate Functions

Alongside the equity participation requirement, the legislation introduces a prohibition on the export of minerals in raw or semi-processed form. This measure is arguably as consequential as the state stake requirement because it directly targets where value is created in the mineral supply chain.

Step-by-step: How the export restriction framework operates

-

Default prohibition: All unprocessed and semi-processed mineral exports are prohibited under the new law as a baseline position.

-

Exception mechanism: Mining companies may seek a specific ministerial authorization to export raw or semi-processed material where domestic processing is not yet feasible.

-

Approval condition: Authorization is only granted where the applicant company provides an approved plan committing to eventual in-country processing capacity development.

-

Ongoing compliance: Companies that receive ministerial authorization must demonstrate measurable progress against their processing commitments to maintain export rights.

-

Legacy project ambiguity: The applicability of these export restrictions to existing mines operating under long-term development agreements remains legally unresolved as of the law's enactment.

The processing mandate is designed to push graphite and other minerals further along the value chain before they leave Mozambican territory, capturing the economic activity, employment, and fiscal returns that currently accrue to processing centres in China and other Asian manufacturing hubs. Whether this objective can be achieved in practice depends heavily on attracting the downstream investment that processing infrastructure requires, which creates a circularity challenge: the very conditions that incentivise processing investment may simultaneously deter the upstream mining investment that generates the mineral feed for processors. In addition, broader critical minerals trade dynamics will influence how effectively Mozambique can negotiate terms with downstream processors seeking alternative supply sources.

Does the 15% State Stake Apply to Existing Mining Operations?

The Grandfathering Question and Its Material Consequences

One of the most significant areas of uncertainty surrounding the Mozambique mining law 15% state stake and local processing requirements concerns their application to existing operations. The majority of active mines in Mozambique are covered by long-term development agreements negotiated under previous legislative frameworks. As of the law's enactment, it remains unclear whether ENM will seek to renegotiate these agreements to incorporate the mandatory equity stake, or whether a grandfathering principle will protect legacy arrangements.

Investor Alert: The legal ambiguity surrounding retroactive application of the 15% state participation requirement to existing projects represents a material commercial risk. Companies currently operating under long-term agreements should treat this uncertainty as a live legal exposure requiring active monitoring and counsel.

Key uncertainties for existing operators include:

-

Whether ENM will initiate formal engagement seeking to restructure existing project agreements to introduce the 15% stake

-

Whether major mineral operations, including graphite, coal, and gemstone projects, face transition obligations under implementing regulations not yet issued

-

How the mines ministry will interpret the law's temporal scope when issuing regulatory guidance

-

Whether international investment treaty protections available to foreign investors can shield existing agreements from retroactive adjustment

The mines ministry was not available to clarify these questions at the time of the law's publication. This silence adds to the uncertainty facing operators, who must now make commercial decisions without definitive regulatory guidance. In comparable situations across Africa, the period between legislative enactment and implementing regulation issuance has often been characterised by negotiated transitions rather than immediate enforcement, but this pattern cannot be assumed without confirmation.

How Grandfathering Has Operated in Comparable African Regimes

Tanzania's 2017 mining reforms offer a relevant precedent. When the Tanzanian government introduced a 16% free-carried state equity requirement alongside new royalty and local content obligations, existing projects faced a period of regulatory uncertainty before transition arrangements were clarified through bilateral negotiation between operators and government agencies. The outcome varied by project, with larger operations generally securing longer transition timelines in exchange for voluntary compliance commitments. Mozambique's situation may follow a similar path, though the specific legislative language and the government's reform ambitions will ultimately determine how aggressively ENM pursues restructuring of existing agreements.

Mozambique's Strategic Position in the Global Battery Materials Supply Chain

Why Graphite Makes This Legislation Globally Significant

To appreciate why Mozambique's mining reforms matter beyond the country's borders, it is necessary to understand graphite's role in the battery materials supply chain. Every lithium-ion battery cell used in electric vehicles and grid-scale energy storage contains a graphite anode, which stores and releases lithium ions during charge and discharge cycles. The anode represents one of the largest components by mass in a lithium-ion cell, meaning graphite demand scales directly with battery production volumes.

Global graphite production context (US Geological Survey data):

| Rank | Country | Market Position |

|---|---|---|

| 1 | China | Dominant, approximately 65-70% of global supply |

| 2 | Madagascar | Second-largest producer |

| 3 | Mozambique | Third-largest producer |

China's near-total dominance of graphite processing, estimated at approximately 90% of global processing capacity, creates a structural vulnerability for Western battery manufacturers seeking supply chain diversification. This vulnerability has become a policy priority for the European Union through its Critical Raw Materials Act and for the United States through provisions of the Inflation Reduction Act, both of which emphasise securing diversified sources of graphite and other battery-critical minerals. Consequently, the global graphite shortage narrative has intensified scrutiny of every producing nation's regulatory framework, including Mozambique's newly enacted legislation.

Mozambique hosts the Balama graphite operations in the country's northern region, managed by Syrah Resources and widely recognised as one of the world's largest graphite deposits by reserve size. Balama produces large-flake, high-purity graphite, which commands premium pricing relative to fine-flake material because of its suitability for battery anode applications and other high-specification industrial uses. The distinction between flake sizes is commercially significant: large-flake graphite typically trades at a meaningful premium and is more directly applicable to battery-grade processing pathways, making Balama's output particularly relevant to Western battery supply chain strategies.

Graphite's journey from raw ore to battery-ready material involves multiple processing stages, each of which adds value. Purification to 99.95% carbon purity, spheronisation (shaping graphite particles for optimal packing in anodes), and coating processes together can multiply the value of raw graphite by a factor of several times over. Mozambique's processing mandate is specifically designed to capture some of this value domestically rather than exporting it to Asian processing centres.

Beyond Graphite: Mozambique's Broader Mineral Asset Base

The legislation's impact extends across a diverse mineral portfolio that gives Mozambique multiple dimensions of strategic resource importance.

-

Rubies: The Montepuez deposit in northern Mozambique is recognised as the world's largest ruby mine by production volume, operated by Gemfields. The gemstone sector now falls under the same state participation framework as industrial minerals.

-

Coal: Significant thermal and coking coal deposits in Tete Province were previously associated with major global mining groups including Rio Tinto and Brazil's Vale, with ownership subsequently transitioning to other operators. These legacy investments represent some of the long-term agreement situations most affected by the grandfathering ambiguity.

-

Emerging battery materials: Exploration activity across Mozambique increasingly targets lithium, vanadium, and rare earth elements, suggesting the mineral base underpinning the legislation may expand in strategic significance over coming years.

How Mozambique's Framework Compares to Other African Resource Nationalism Models

Benchmarking State Equity and Processing Requirements Across Sub-Saharan Africa

Mozambique's legislation does not emerge from a policy vacuum. A wave of resource nationalism has reshaped mining governance across Africa over the past decade, with each jurisdiction adopting its own configuration of state equity requirements, export restrictions, and processing mandates.

| Country | Key Mineral | State Equity Requirement | Export Restriction | Processing Mandate |

|---|---|---|---|---|

| Mozambique | Graphite, Coal, Rubies | 15% minimum, free-carried | Yes, unprocessed ban | Yes, local processing required |

| Zimbabwe | Lithium | Varies by project | Yes, raw lithium export ban | Yes |

| DRC | Cobalt, Copper | Gécamines model, varies | Partial | Emerging framework |

| Tanzania | Gold, Tanzanite | 16% free-carried (2017 reforms) | Selective | Selective |

| Ghana | Gold | 10% carried interest via GNPC | No blanket ban | No blanket mandate |

Structurally, Mozambique's framework most closely resembles Tanzania's 2017 reforms in its use of non-dilutable free-carried equity. However, the blanket prohibition on unprocessed mineral exports is more aggressive than most comparable frameworks currently in force, placing Mozambique toward the interventionist end of the African mining governance spectrum. Zimbabwe's ban on raw lithium exports represents a direct parallel in its sector-specific export restriction logic, while the DRC's approach relies more heavily on state enterprise involvement through Gécamines than legislated minimum equity requirements.

Analytical Insight: The convergence of multiple African nations toward similar policy instruments, including free-carried equity and processing mandates, suggests a coordinated, though informal, evolution in continental resource governance philosophy. This pattern is likely to accelerate as battery material demand grows and the strategic leverage of mineral-holding nations increases.

What the 15% Free-Carried Stake Means for Project Economics

Modelling the Financial Impact on Mining Investment Returns

The combined effect of a 15% non-dilutable free-carried equity stake and mandatory local processing requirements materially alters the investment economics for mining projects in Mozambique. Understanding these mechanics is essential for investors assessing existing exposures and evaluating new project opportunities. Furthermore, those tracking the broader battery metals investment landscape will recognise this as part of a wider repricing of risk across African mineral jurisdictions.

Hypothetical scenario: Impact on a mid-scale graphite project

Consider a graphite mining project with:

- Total capital cost: USD 300 million

- Annual revenue at full production: USD 120 million

- Pre-legislation projected equity IRR: 18%

Under the 15% free-carried state stake:

- ENM receives 15% of net project cash flows without contributing capital

- Private investors absorb 100% of the USD 300 million capital requirement

- The effective IRR for private equity investors compresses, with estimates suggesting a reduction of 2-4 percentage points depending on mine life and financing structure

- Local processing requirements add an estimated 20-35% to upfront capital expenditure for beneficiation infrastructure, further increasing the capital burden

Key Takeaway: Projects with high-grade resources, long mine lives, and significant reserve bases are best positioned to absorb these structural cost increases. Marginal deposits that were borderline investable under previous frameworks face a materially more challenging economic case under the new legislation.

Local Processing as Capital Burden and Long-Term Opportunity

While the immediate financial analysis suggests value transfer from private investors to the state, a longer-term perspective reveals that processing mandates can create genuine economic opportunities if correctly structured. Countries that successfully transition from raw material exporters to mineral processors typically capture substantially higher export revenues per tonne, develop domestic industrial capabilities with broader employment multipliers, and reduce their exposure to commodity price volatility at the raw material level.

The challenge for Mozambique lies in creating the conditions, including reliable power supply, skilled labour pools, and logistics infrastructure, that make domestic processing economically viable rather than merely legislatively mandated. In addition, critical minerals recycling trends may ultimately reshape the long-term demand picture for virgin graphite, adding another layer of complexity to processing infrastructure investment decisions.

The next major ASX story will hit our subscribers first

How the 10% Local Development Fund Allocation Works

Revenue Sharing as a Governance Mechanism

The proposed allocation of 10% of mining revenues to a local development fund represents an additional fiscal instrument designed to ensure mineral wealth generates tangible economic benefits at the community and regional levels. This mechanism reflects growing international consensus that mining royalties flowing to central government budgets often fail to translate into improved welfare outcomes for populations adjacent to mine sites.

Local development fund structures, now incorporated into mining codes across multiple African jurisdictions, aim to create a more direct connection between mineral extraction and infrastructure investment, education, healthcare, and economic diversification in host communities. The design and administration of such funds critically determines their effectiveness, with governance frameworks needing to ensure transparency, accountability, and alignment with genuine community priorities rather than becoming conduits for politically directed spending.

What Mining Investors and Operators Should Do Now

Priority Actions Under the New Mozambique Mining Law

Given the combination of confirmed legislative requirements and unresolved implementation uncertainties, companies operating or considering investment in Mozambique face an immediate need for structured legal and commercial assessment.

Checklist: Key actions for mining companies in Mozambique

-

Review all existing project agreements for stability clauses, grandfathering provisions, and international arbitration rights that may provide protection against retroactive application of the 15% stake -

Assess whether current mineral export arrangements require ministerial authorisation under the new processing prohibition framework -

Commission detailed financial modelling of the impact of the free-carried 15% ENM stake on project IRR, NPV, and debt service capacity under multiple production scenarios -

Engage specialist legal counsel to evaluate the availability of bilateral investment treaty protections that might shield existing agreements from renegotiation pressure -

Develop a credible local processing roadmap that can be submitted for ministerial review if export authorisation is required, ensuring the roadmap includes realistic capital, timeline, and technology assessments -

Monitor the mines ministry's issuance of implementing regulations for clarity on transitional arrangements, exemption scope, and ENM's operational mandate

Frequently Asked Questions: Mozambique Mining Law and the 15% State Stake

What is ENM and what role does it play under the new law?

ENM, the Empresa Nacional de Mineração, is Mozambique's National Mining Company and serves as the vehicle through which the state holds its mandatory equity positions in all mining projects. It functions as the institutional mechanism for state participation rather than the government holding equity directly through a ministry or treasury structure.

Is the 15% state stake paid or free-carried?

The stake is explicitly free-carried, meaning ENM receives its equity interest without contributing capital toward project development or operations. Private investors bear the full capital cost while ENM participates in profit distributions.

Does the export ban apply to all minerals or only specific categories?

The prohibition covers unprocessed and semi-processed mineral products broadly, though ministerial authorisation can create exceptions where approved local processing plans are in place. The law does not appear to limit the restriction to specific mineral categories based on available reporting.

How does Mozambique's law affect graphite supply chains for battery manufacturers?

Battery manufacturers and their supply chain partners sourcing Mozambican graphite face potential disruptions if existing export arrangements require renegotiation under the new framework. The processing mandate, if strictly enforced, could require that graphite be upgraded to higher purity or processed into intermediate battery-grade products before export, increasing costs and potentially requiring capital investment in Mozambique-based processing facilities.

Are existing mining operations exempt from the new requirements?

This remains legally unresolved. The law does not explicitly exempt operations covered by long-term development agreements, but the mines ministry has not yet issued implementing regulations clarifying the transitional framework. This ambiguity is a material risk for active operators.

Resource Nationalism, Battery Materials, and the Future of Mozambique's Mining Sector

Balancing Sovereign Control and Investment Attractiveness

The structural tension at the heart of the Mozambique mining law 15% state stake and local processing framework is one familiar to resource-rich developing economies: maximising sovereign control over strategic assets while maintaining the investability that attracts the capital and expertise needed to actually develop those assets. The free-carried, non-dilutable state stake and the local processing prohibition represent a deliberate shift toward the sovereign control end of this spectrum, reflecting a calculation that Mozambique's mineral endowment, particularly its world-class graphite deposits, provides sufficient strategic leverage to sustain investment interest even under more demanding terms.

Whether this calculation proves correct will depend on global demand trajectories for battery materials, the competitiveness of Mozambique's regulatory environment relative to alternative graphite-producing jurisdictions, and the government's capacity to implement the framework with clarity and consistency. Regulatory ambiguity, particularly around legacy agreements and the ministerial authorisation process, poses a near-term risk to investor confidence that could deter exactly the downstream processing investment the legislation is designed to stimulate.

Final Analytical Frame: Mozambique's legislation is not an isolated policy event but part of a continent-wide recalibration of how resource-rich nations engage with foreign mining capital. The 15% free-carried stake and local processing mandate signal a deliberate aspiration to move from raw material exporter to value-chain participant. The success of this transition will ultimately be determined by implementation quality, regulatory transparency, and the government's ability to attract the downstream investment that processing mandates require rather than simply legislating it into existence. Analysts tracking Mozambique's mining law reforms note that the government's resolve will be tested most acutely in its first round of negotiations with major existing operators.

This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. Mining investment involves significant risks including regulatory, operational, and commodity price uncertainties. Readers should conduct their own due diligence and seek qualified professional advice before making investment decisions. Forecasts and hypothetical scenarios presented are illustrative only and should not be relied upon as predictions of actual project performance.

Want to Stay Ahead of the Next Major Mineral Discovery Reshaping Battery Supply Chains?

As African resource nationalism rewrites the rules for graphite, lithium, and other battery materials, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex mineral data into actionable investment insights the moment they hit the market. Explore Discovery Alert's discoveries page to understand how historic mineral finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the next major opportunity.