July 17, 2026

The Industrial Logic of Lime: Why Zambia's Copperbelt Revival Starts With Calcium Oxide

Across Africa's mineral-rich corridors, the most consequential industrial investments are rarely the ones that generate the loudest headlines. While copper cathode prices and lithium supply chains attract global investor attention, the unglamorous upstream inputs that make metal processing possible operate largely beneath the radar. Lime is one such input, and its scarcity on the Zambian Copperbelt over the past several years has quietly undermined the operational efficiency of one of the world's most strategically important copper-producing regions.

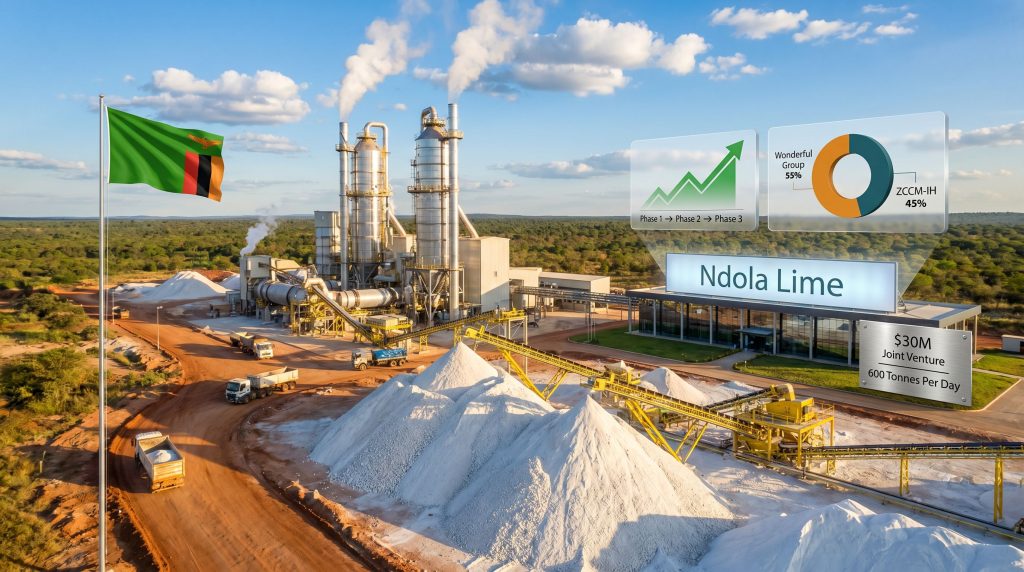

The announcement that the ZCCM-IH Wonderful Group Ndola lime production facility represents far more than the restoration of a dormant industrial asset, with a $30 million commitment to revive operations. It signals a deliberate shift in how Zambia's state-owned investment arm approaches portfolio management, how Chinese industrial capital is engaging with African resource economies, and how the Copperbelt's next phase of industrial development will be structured. For investors and industry observers tracking Zambia's copper ambitions, understanding this joint venture requires unpacking both the chemistry of copper processing and the economics of state-owned asset revival.

When big ASX news breaks, our subscribers know first

Why Lime Is Non-Negotiable in Copper Processing

Lime's role in metallurgical processing is one of the most underappreciated dynamics in the mining value chain. In copper ore flotation circuits, quicklime serves as a pH regulator, maintaining the alkaline conditions necessary for selective mineral separation. Without consistent, high-quality lime supply, flotation performance degrades, recovery rates fall, and the cost-per-tonne of refined copper rises materially. Furthermore, the copper price growth drivers that are reshaping global markets make reliable domestic reagent supply increasingly critical for competitive processing operations.

There are two primary lime products used across Zambia's industrial base, each serving distinct functions:

- Quicklime (calcium oxide): Produced by calcining limestone at high temperatures, quicklime is the primary reagent used in copper ore flotation and hydrometallurgical processing. Its reactivity and particle size distribution directly influence process efficiency.

- Hydrated lime (calcium hydroxide): Produced by adding water to quicklime, hydrated lime is used in wastewater treatment at mine sites and in soil stabilisation for construction projects.

- Agricultural lime (ground limestone): Finely crushed calcium carbonate applied to acidic soils to raise pH, improving crop yields across Zambia's agricultural regions where soil acidity is a persistent productivity constraint.

- Limestone aggregate: Used as a construction material and as a precursor to cement manufacturing, limestone aggregate underpins infrastructure development across the Copperbelt.

The collapse of the Ndola facility in 2018 did not merely inconvenience Zambian copper producers. It removed the primary domestic source of a reagent that cannot simply be substituted. Importing lime introduces significant logistical costs, foreign exchange exposure, and supply reliability risks that compound operational challenges for mining operations already navigating volatile commodity prices.

The absence of a reliable domestic lime supplier forces copper producers to either pay import premiums or accept inconsistent reagent quality, both of which erode the economic competitiveness of Zambia's copper sector at precisely the moment global demand is accelerating.

Understanding the ZCCM-IH and Wonderful Group Joint Venture

Deal Structure and Ownership Breakdown

The joint venture between ZCCM-IH and Wonderful Group of Companies establishes a co-investment framework that balances state oversight with private-sector operational capability. The structure reflects lessons learned from both the original facility's failure and from comparable industrial revival projects across sub-Saharan Africa. Mining joint ventures and asset sales of this nature are increasingly common as state entities seek capable partners to unlock dormant industrial value.

| Parameter | Detail |

|---|---|

| Total Investment | $30 million USD |

| JV Vehicle | Ndola Lime |

| ZCCM-IH Equity Stake | 45% |

| Wonderful Group Equity Stake | 55% |

| Site Production History | Continuous since 1931 |

| Previous Operating Entity | Limestone Resources Limited / Ndola Lime Company |

| Insolvency Event | 2018 |

| Phase 1 Target Capacity | 600 tonnes per day |

The 55/45 ownership split is strategically significant. By retaining a 45% equity stake, ZCCM-IH preserves meaningful participation in the facility's future earnings and maintains governance influence over operational decisions, particularly those with national supply chain implications. Simultaneously, the majority position held by Wonderful Group ensures that the operating partner has sufficient decision-making authority to drive the efficiency and speed necessary for commercial success.

Who Are the Joint Venture Partners?

ZCCM Investment Holdings functions as Zambia's primary state-owned vehicle for mineral and energy sector investments. Unlike a purely extractive state mining company, ZCCM-IH operates as an active portfolio manager, holding stakes across a range of industrial and resource assets while seeking to catalyse private investment into dormant or underperforming operations. The organisation's evolving mandate has shifted it from passive shareholder to industrial architect, a transition this joint venture explicitly embodies.

Wonderful Group of Companies enters the Zambian market as the majority partner and operational lead, bringing capital, modern industrial technology, and management expertise accumulated through its broader industrial activities. For a Chinese industrial conglomerate, the Zambian lime and cement market represents both a commercial opportunity and a strategic foothold in one of Africa's most important copper-producing jurisdictions. CEO Huang Yaochi's position, as conveyed through the joint venture announcement, framed the investment as a long-term industrial commitment to Zambia's economic development rather than a short-term capital deployment.

How the Final Terms Evolved From Earlier Reports

Earlier market intelligence had suggested a potential transaction valued at approximately $25 million for a 55% acquisition by Wonderful Group. The finalised structure reflects a $30 million co-investment framework, representing an expanded scope that implies both partners increased their commitment from initial expectations.

This evolution in deal terms is meaningful: it suggests that due diligence revealed either greater opportunity than initially assessed, a broader scope for Phase 2 and Phase 3 development, or both. Investors tracking ZCCM-IH's portfolio strategy should note that the revised terms signal genuine conviction from the private-sector partner about the facility's commercial potential.

A 95-Year Industrial Legacy: The History of Ndola Lime

Few industrial assets on the African continent can claim a continuous operating history stretching back to 1931. The Ndola lime production site predates Zambian independence, the modern copper industry's global expansion, and the contemporary energy transition that is now reshaping demand for copper and associated processing inputs.

The facility's timeline maps directly onto the Copperbelt's industrial arc:

- 1931: Lime production commences at Ndola, establishing what would become one of the Copperbelt's foundational industrial operations under the banner of the Ndola Lime Company.

- Post-independence decades: The facility continues supplying lime to Zambia's copper mines, construction sector, and agricultural producers, operating as a critical upstream enabler of the country's primary export industry.

- ZCCM-IH era: The entity transitions from the Ndola Lime Company to Limestone Resources Limited under 100% ZCCM-IH ownership, reflecting the broader restructuring of Zambia's state mining portfolio.

- 2018: Sustained operational difficulties culminate in the insolvency of the plant owner, halting production and creating the supply vacuum that persisted for nearly a decade.

- 2026: ZCCM-IH and Wonderful Group announce the $30 million JV, marking the facility's entry into what ZCCM-IH describes as its next industrial chapter.

The Ndola lime facility is not merely a legacy asset requiring rescue. It is a 95-year-old industrial institution whose revival carries both economic and symbolic weight for the Copperbelt's identity as a world-class mining and processing hub.

The 2018 insolvency deserves closer examination as an industrial case study. Lime production facilities are capital-intensive operations with high fixed costs related to energy consumption, kiln maintenance, and quarrying. When demand fluctuates or operating costs escalate beyond revenue, the economics of lime production can deteriorate rapidly, particularly for older facilities with aging infrastructure requiring continuous reinvestment.

The Three-Phase Expansion Plan: How $30 Million Gets Deployed

The phased approach to restoring and expanding the ZCCM-IH Wonderful Group Ndola lime production facility reflects sound industrial planning principles. Rather than committing the full capital envelope to a fixed configuration, the JV partners have structured the investment to allow market signals and operational performance to guide subsequent phases. This creates optionality, reduces execution risk, and ensures capital is deployed in line with demonstrated demand.

Phase 1: Restoring Industrial-Scale Lime Production

The foundational investment involves constructing and commissioning a new lime production plant with a capacity of 600 tonnes per day. This figure is not arbitrary. At 600 t/d, the facility would operate at industrial scale sufficient to serve multiple copper mining operations simultaneously while also supplying construction and agricultural lime markets.

Assuming continuous operation, a 600 t/d plant generates approximately 219,000 tonnes of lime annually, a volume capable of displacing a meaningful share of Zambia's current import dependency for this input. Phase 1's primary objectives are:

- Installing modern lime kiln technology to replace the insolvent facility's outdated infrastructure

- Establishing consistent product quality and particle size specifications that meet copper processing requirements

- Re-anchoring domestic lime supply on the Copperbelt to reduce import dependency

- Demonstrating operational performance as the foundation for Phase 2 investment decisions

Phase 2: Expanding the Product Range

Within 12 months of Phase 1 commissioning, the JV partners will deliver either a cement processing plant or a second lime production line. This binary decision point is one of the most analytically interesting aspects of the investment structure.

| Phase 2 Option | Strategic Logic | Market Served |

|---|---|---|

| Cement processing plant | Diversifies revenue, leverages limestone resource, addresses construction material shortages | Construction, infrastructure, urbanisation |

| Second lime production plant | Deepens position in core market, meets growing mining sector demand | Copper mining, agriculture, industrial processing |

The cement option would transform the facility from a single-product operation into an integrated mineral processing platform, significantly broadening its revenue base and reducing exposure to copper sector cyclicality. Consequently, the second lime plant option doubles down on the facility's core competency and directly serves the growing copper production ambitions underpinning Zambia's economic development strategy.

Phase 3: Market-Driven Scalability

The third phase deliberately avoids prescribing a fixed investment outcome, instead conditioning further expansion on market conditions prevailing at the time of Phase 2 completion. This approach positions the Ndola facility as a scalable industrial platform rather than a static capacity addition.

| Phase | Primary Deliverable | Timeline |

|---|---|---|

| Phase 1 | 600 t/d lime production plant | Initial construction and commissioning |

| Phase 2 | Cement plant or second lime production line | Within 12 months of Phase 1 commissioning |

| Phase 3 | Further capacity expansion | Contingent on market conditions at Phase 2 completion |

What Technology Modernisation Actually Means for Lime Production

The commitment to installing state-of-the-art plant and technology is more than marketing language. For lime production specifically, technological generation matters enormously for both economics and product quality. Modern rotary or shaft lime kilns differ fundamentally from legacy equipment in several dimensions:

- Energy efficiency: Contemporary lime kilns achieve significantly lower fuel consumption per tonne of output compared to equipment from the mid-twentieth century. In an energy-constrained environment like Zambia, lower energy intensity per unit of production directly improves the facility's cost competitiveness.

- Product consistency: Modern process control systems allow operators to maintain tighter temperature profiles through the calcination zone, producing lime with more consistent reactivity levels. For copper flotation circuits, this consistency translates directly into more predictable reagent performance and better mineral recovery.

- Emissions performance: Legacy lime kilns typically produce higher particulate emissions and are more difficult to bring into compliance with contemporary environmental standards. Modern kiln designs incorporate improved dust collection and gas handling systems that reduce the facility's environmental footprint.

- Automation and yield optimisation: Digital process monitoring enables real-time adjustment of feed rates, fuel inputs, and cooling parameters, reducing both over-burning and under-burning of limestone, both of which degrade product quality.

The next major ASX story will hit our subscribers first

Economic and Industrial Implications for Zambia

Copperbelt Supply Chain Integrity

The eight-year gap created by the 2018 insolvency forced Zambian mining operations and construction firms into unfavourable positions: sourcing lime from alternative domestic suppliers with constrained capacity, or importing at a cost premium that erodes operational margins. In addition, the broader copper market trends emerging globally make this supply chain vulnerability increasingly costly to sustain.

Restoring 600 t/d of domestic lime production addresses this vulnerability at its source. The operational and financial implications for copper producers are direct:

- Elimination of import freight costs and associated foreign exchange outflows

- Reduced supply chain lead times compared to imported material

- Greater pricing stability through domestic supply relationships

- Improved operational planning certainty for flotation circuit reagent scheduling

Ndola's Industrial Renewal Narrative

The ZCCM-IH Wonderful Group Ndola lime production facility joint venture carries significance beyond its direct operational outputs. Ndola, as the Copperbelt's commercial centre, has experienced the broader economic pressures associated with the decline of legacy industrial infrastructure. The revival of a 95-year-old industrial institution sends a signal to other potential investors that Zambia's state investment holding company is willing and capable of structuring credible public-private partnerships to revitalise dormant assets.

The multiplier effects of restoring industrial operations at this scale include:

- Direct employment in plant operations, maintenance, and quarrying activities

- Demand for ancillary services including logistics, engineering, and consumables supply

- Stimulation of local procurement networks that support the facility's operating requirements

- Skills development through technology transfer from Wonderful Group's operational expertise

Agricultural Sector Benefits

Agricultural lime is a critical input for Zambian smallholder and commercial farmers managing soil acidity across the country's agricultural zones. Soil pH directly affects nutrient availability, and acidic soils can dramatically reduce crop yields regardless of fertiliser application. The restoration of domestic agricultural lime production therefore supports food security objectives that extend well beyond the mining sector's immediate interests. This also complements Zambia copper production growth ambitions by stabilising the broader economic environment in which mining operations function.

ZCCM-IH's Portfolio Management Model: A Potential Template

From Passive Investor to Active Industrial Architect

ZCCM-IH's approach to the Ndola lime revival illustrates a portfolio management philosophy that diverges significantly from the conventional state mining entity model. Rather than attempting to fund and operate the facility directly, ZCCM-IH has structured a transaction that brings in a capable private partner with the capital, technology, and operational track record to execute the industrial revival.

The ZCCM-IH CEO's characterisation of this transaction as active portfolio management in practice points to an institutional posture that prioritises value creation through partnership over direct operational control. The 45% retained equity stake ensures ZCCM-IH participates in the facility's long-term earnings without absorbing the full operational risk and capital burden of the revival.

Comparing Approaches to State Industrial Asset Management

| Dimension | ZCCM-IH Model | Conventional State Entity Model |

|---|---|---|

| Investment approach | Active JV structuring with capable private partner | Passive equity holding or direct state operation |

| Technology sourcing | Partner-led modernisation with knowledge transfer | State-funded procurement, often delayed |

| Capital risk allocation | Shared across JV structure | Concentrated on state balance sheet |

| Operational responsibility | Partner-managed with state governance oversight | State-managed, often with operational constraints |

| Scale of ambition | Phased expansion with market-driven growth | Fixed capacity, limited growth orientation |

The structural logic of retaining 45% while allowing the majority partner to lead operations reflects a sophisticated understanding of where value is created in industrial asset revival. Furthermore, this transaction model, if it delivers the intended operational and financial outcomes, could establish a replicable framework for other dormant assets within ZCCM-IH's portfolio. Details of the venture's structure are outlined by ZCCM-IH, providing useful context for analysts tracking the organisation's evolving portfolio strategy. This could attract additional international industrial partners to Zambia's broader reindustrialisation agenda, particularly as the global copper supply forecast points to sustained demand growth through the decade ahead.

FAQs: ZCCM-IH, Wonderful Group, and the Ndola Lime Revival

What is the Ndola Lime production facility?

The Ndola lime production facility is one of Zambia's oldest continuously operating industrial sites, with lime production at the location dating back to 1931. Operating under the names Ndola Lime Company and subsequently Limestone Resources Limited, the facility has historically supplied quicklime, hydrated lime, agricultural lime, and limestone across Zambia's mining, construction, and agricultural sectors. The operator became insolvent in 2018, halting production until the current ZCCM-IH and Wonderful Group joint venture.

What is the total investment in the Ndola Lime revival?

ZCCM-IH and Wonderful Group have committed a combined $30 million to the JV vehicle, Ndola Lime, funding plant construction, technology installation, and phased capacity expansion.

What production capacity will the revived facility achieve?

Phase 1 targets 600 tonnes per day of lime production capacity. Subsequent phases may add either a cement processing plant or a second lime production line, with Phase 3 further expansion subject to market conditions.

What is the ownership split of the Ndola Lime joint venture?

Wonderful Group holds 55% and ZCCM-IH holds 45% of the joint venture vehicle.

Why is lime critical to Zambia's copper mining sector?

Quicklime functions as a pH-regulating reagent in copper ore flotation circuits, maintaining the alkaline conditions necessary for selective mineral separation. Inconsistent or inadequate lime supply directly reduces copper recovery efficiency and increases per-tonne processing costs, making reliable domestic lime availability a genuine operational priority for Zambian copper producers.

What happened to the original Ndola Lime Company?

The operator encountered sustained financial and operational difficulties that culminated in insolvency in 2018, halting production and removing the Copperbelt's primary domestic lime supplier from the market for nearly a decade.

Key Takeaways

The ZCCM-IH Wonderful Group Ndola lime production facility joint venture is a transaction that rewards careful analysis beyond its headline figures. Several dimensions stand out as particularly significant for investors, industry observers, and policymakers tracking Zambia's industrial development:

- A $30 million co-investment between ZCCM-IH (45%) and Wonderful Group (55%) marks the most substantial commitment to Zambian lime production in decades, with a phased structure designed to minimise execution risk while preserving expansion optionality.

- The facility's 95-year industrial heritage gives its revival a significance that extends beyond simple capacity restoration, representing a statement about the Copperbelt's industrial continuity and ZCCM-IH's commitment to preserving legacy assets as productive contributors to the national economy.

- A 600 t/d Phase 1 capacity target is commercially meaningful for Zambia's copper sector, with the potential to displace a significant portion of imported lime and stabilise reagent supply chains that have been disrupted since 2018.

- The technology modernisation component is not incidental. Modern kiln technology, process automation, and improved product consistency have direct implications for copper recovery performance and environmental compliance across the Copperbelt's processing operations.

- The transaction structure illustrates a replicable portfolio management model for ZCCM-IH, potentially serving as a template for attracting capable private partners to other dormant or underperforming state-held industrial assets across Zambia's mineral economy.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. Forward-looking statements, phased investment timelines, and capacity projections referenced herein are based on publicly available information from the joint venture announcement and are subject to change based on operational, market, and regulatory conditions. Readers should conduct independent due diligence before making any investment decisions related to companies or sectors discussed in this article.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market?

The copper supply chain revival unfolding across Zambia's Copperbelt is a reminder that transformative investment opportunities often begin with the upstream enablers others overlook — and Discovery Alert's proprietary Discovery IQ model is built to surface exactly these kinds of high-potential ASX mineral discoveries the moment they are announced, turning complex data across 30+ commodities into clear, actionable insights. Explore how historic discoveries have delivered extraordinary returns on Discovery Alert's dedicated discoveries page, then begin your 14-day free trial to ensure you are positioned ahead of the market when the next significant announcement lands.