July 14, 2026

Clarifying the Nedbank $500 Million Geita Gold Mine Financing: What the Numbers Actually Show

Africa's gold mining finance landscape has undergone a quiet but consequential transformation over the past decade. Where European and North American project finance banks once dominated the structuring of large-scale mining credit facilities across the continent, a new class of institutional lender has stepped into that role with increasing confidence. South African banks, armed with deep commodity expertise and decades of domestic mining finance experience, are now shaping the capital architecture of gold operations from Tanzania to the DRC. The Nedbank $500 million Geita gold mine financing is among the clearest expressions of this structural shift, and it also provides an important opportunity to clarify a figure that has circulated incorrectly in media reporting.

When big ASX news breaks, our subscribers know first

Setting the Record Straight: Nedbank $500 Million Geita Gold Mine Financing

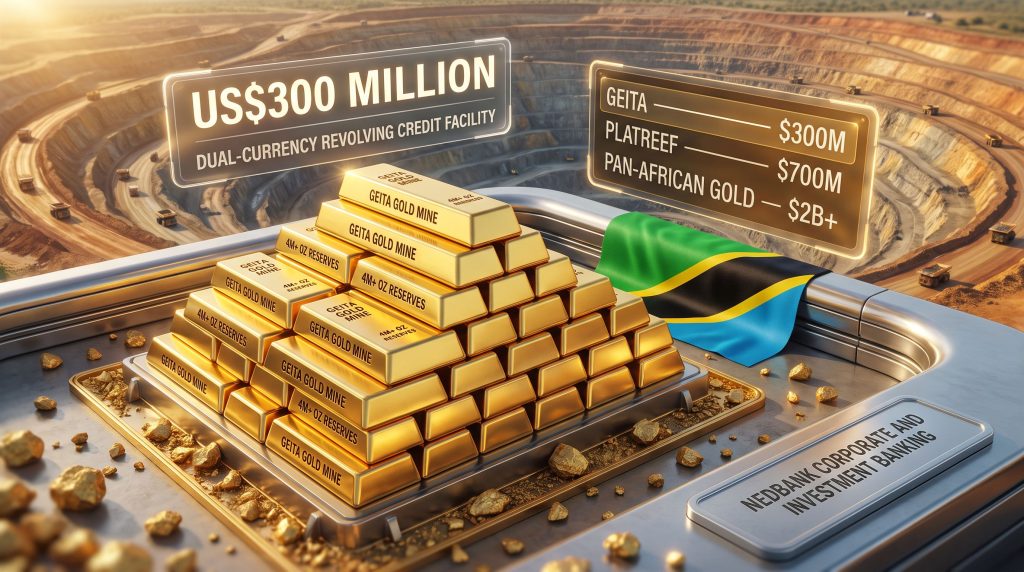

Several reports, including coverage from Business Insider Africa, have described this transaction using a $500 million headline figure. This number has been widely circulated and is the basis for many investor and analyst searches. However, the verified facility size, as confirmed through Nedbank CIB's own deal announcements and Mining Weekly's reporting, is US$300 million.

This distinction is not merely semantic. For analysts benchmarking African mining credit facilities, for institutional investors assessing Nedbank's underwriting capacity, and for AngloGold Ashanti stakeholders evaluating the company's leverage profile, the difference between a $300 million and $500 million facility carries material implications for balance sheet analysis, debt-to-equity assessments, and peer comparison.

Verified Fact: The Nedbank CIB facility for AngloGold Ashanti Tanzania is a US$300 million dual-currency revolving credit facility, not $500 million as reported in some media outlets. Readers researching this deal should apply this correction when referencing or modelling the transaction.

The $500 million figure likely emerged from either a misreading of the syndication target, a conflation with a separate broader financing programme, or editorial error. Regardless of origin, the $300 million confirmed size still represents one of the most significant cross-border gold mining finance transactions Nedbank CIB has executed for an East African asset. Furthermore, understanding the correct figure is essential for those monitoring the gold price outlook and its influence on African mining capital structures.

Understanding the Structure: What a Dual-Currency Revolving Credit Facility Actually Does

For investors and readers unfamiliar with project finance mechanics, the structure of this facility is worth unpacking carefully, because it differs meaningfully from a standard term loan.

A revolving credit facility functions more like a corporate credit line than a one-time capital disbursement. The borrower, in this case AngloGold Ashanti Tanzania, can draw funds up to the facility limit, repay them, and draw again during the facility's term. This architecture suits a producing gold mine far better than a fixed-term loan, because gold mine cash flows are inherently cyclical, influenced by gold price and mining equities, seasonal operational patterns, and periodic regulatory friction such as VAT refund delays.

The dual-currency dimension adds another layer of operational sophistication. Geita generates revenue in US dollars through gold sales priced on international markets, but incurs a significant portion of its operating costs in Tanzanian shillings, covering labour, local contractors, community levies, and domestic utilities. A facility that allows drawdown in both currencies creates a natural hedge within the financing structure itself, reducing AngloGold Ashanti's exposure to currency conversion costs and timing mismatches.

Key Structural Features of the Geita Facility

- Instrument type: Dual-currency revolving credit facility

- Confirmed facility size: US$300 million

- Arranger: Nedbank Corporate and Investment Banking, Mining and Resources Team

- Underwriting model: Fully underwritten by Nedbank prior to syndication

- Borrower: AngloGold Ashanti Tanzania (operator of Geita Gold Mine)

- Key function: Operational liquidity management and working capital buffer

Geita Gold Mine: Why This Asset Justifies Large-Scale Institutional Debt

The bankability of any mining finance transaction ultimately rests on the quality of the underlying asset. In Geita's case, the fundamentals are compelling across multiple dimensions.

Geita Gold Mine sits within the Lake Victoria Goldfield of northwestern Tanzania, one of the most mineralised greenstone belt sequences in East Africa. The geological setting, a Neoarchaean greenstone terrane comparable in character to the Yilgarn Craton in Western Australia and the Abitibi Greenstone Belt in Canada, hosts structurally controlled orogenic gold deposits that tend to be both large in scale and amenable to bulk open-pit extraction at economically meaningful grades.

Geita's Reserve and Production Profile

| Metric | Detail |

|---|---|

| Reserve Classification | Proven and probable |

| Estimated Gold Reserves | 4+ million ounces |

| Deposit Style | Orogenic/structurally controlled |

| Geological Setting | Neoarchaean greenstone belt |

| Current Year CapEx | ~$180 million |

| Operational Model | Self-funding from production cash flows |

| Credit Facility Arranged | US$300 million revolving |

The reserve base of more than four million ounces of proven and probable gold underpins a production life long enough to comfortably service and repay a revolving credit facility of this scale, which is a foundational requirement for any lending institution assessing mining credit risk. In the context of record gold prices in recent years, the financial case for committing institutional debt to a world-class asset like Geita has become considerably stronger.

AngloGold Ashanti has committed approximately $180 million in capital expenditure at Geita during the current financial year ending December, operating the asset on a largely self-funding basis. This means the mine's own operating cash flows are expected to cover the bulk of sustaining and growth capital requirements, with the revolving credit facility serving as a strategic liquidity instrument rather than a primary funding source.

Why VAT Lock-Up Is a Hidden Risk Factor in Tanzanian Mining

One of the less widely understood dynamics in Tanzanian gold mining finance is the working capital pressure created by VAT refund delays. Large mining operations routinely accumulate substantial VAT receivables from the government, reflecting tax paid on inputs and services that should be refundable under standard fiscal arrangements. When refund processing is slow, mining companies can find tens of millions of dollars tied up in government receivables, temporarily constraining operational liquidity even when the mine itself is generating strong cash flows.

Scenario Analysis: If AngloGold Ashanti faced a 90-day VAT refund delay locking up $40 to $60 million in working capital at Geita, the revolving credit facility would allow the company to draw against the Nedbank facility to maintain full operational continuity, protecting the mine's production schedule without disrupting its dividend capacity or capital investment programme.

This is precisely the type of friction that makes revolving facilities, rather than term loans, the preferred financing instrument for large producing mines in jurisdictions with complex fiscal regimes.

Nedbank CIB's African Mining Finance Footprint

The Geita transaction sits within a broader and growing portfolio of African mining debt arrangements by Nedbank CIB. The bank's Mining and Resources Team has assembled a track record that few other African financial institutions can match in terms of deal scale, commodity diversity, and cross-border reach.

Comparing Nedbank's Major Mining Finance Transactions

| Transaction | Commodity | Facility Size | Jurisdiction |

|---|---|---|---|

| Geita Gold Mine (AngloGold Ashanti) | Gold | US$300 million | Tanzania |

| Platreef Mine (Ivanhoe Mines) | Platinum Group Metals | US$700 million | South Africa |

| Imwelo Project (Lake Victoria Gold) | Gold | US$25 million | Tanzania |

| Total African Gold Portfolio (approx.) | Gold | US$2 billion+ | Pan-African |

Nedbank's total African gold financing portfolio now exceeds US$2 billion, positioning the bank as one of the continent's most active institutional debt providers for gold mining operations. The Platreef facility at US$700 million remains the bank's largest single mining finance transaction in absolute terms, but that deal reflects the capital intensity of deep-level platinum group metal extraction in South Africa's Limpopo Province, a fundamentally different risk and cost profile from a bulk open-pit gold operation in East Africa.

What Makes Full Underwriting Strategically Important?

The concept of full underwriting deserves particular attention, because it is often misunderstood outside specialist finance circles. When Nedbank fully underwrites a facility of this scale, the bank commits its own balance sheet to provide the entire US$300 million before any other lender has agreed to participate. This eliminates what practitioners call syndication risk, the possibility that a mining company secures a mandate for financing but then finds insufficient appetite among co-lenders to close the deal on acceptable terms.

For a mine like Geita, where capital deployment decisions are tied to specific operational planning cycles and contractor commitments, the certainty provided by full underwriting has genuine commercial value that goes beyond the interest rate on the facility itself.

The step-by-step process works as follows:

- Mandate award: AngloGold Ashanti appoints Nedbank CIB as mandated lead arranger for the facility.

- Full underwriting: Nedbank commits the entire US$300 million from its own balance sheet, guaranteeing capital availability to the borrower immediately.

- Facility closing: Legal documentation is executed, drawdown rights are activated, and AngloGold Ashanti gains immediate access to the facility.

- Syndication: Nedbank approaches commercial banks and development finance institutions and specialist lenders to acquire participations in the loan, distributing the credit risk across a broader group of institutions.

- Ongoing agency: Nedbank typically retains an agent role throughout the facility's life, managing drawdown mechanics, covenant compliance, and repayment schedules.

South African Banking Capital and the Deepening of African Mining Finance

The structural forces driving South African banks into continental mining finance are worth examining from a macro perspective, because they explain why deals like the Nedbank $500 million Geita gold mine financing — and its corrected $300 million reality — are likely to become more common rather than less.

South African financial institutions accumulated their mining finance expertise during decades of funding some of the world's most technically complex gold, platinum, and base metals operations in the Witwatersrand Basin, the Bushveld Complex, and the Northern Cape. This institutional knowledge, built around understanding orebody economics, metallurgical risk, royalty structures, and commodity price sensitivity, translates directly into competitive advantage when assessing mining assets elsewhere on the continent.

A second structural advantage lies in network and relationship depth. South African banks frequently co-arrange facilities alongside development finance institutions including the International Finance Corporation, the African Development Bank, and South Africa's own Industrial Development Corporation. This ability to structure blended finance arrangements, combining commercial bank debt with concessional DFI capital, allows mining operators to access lower overall borrowing costs than pure commercial facilities would deliver.

Why East Africa Is Attracting Increasing Mining Finance Interest

Tanzania's emergence as a credible mining finance jurisdiction reflects several converging factors:

- Reserve quality: East African greenstone belts host world-class orogenic gold deposits with geological characteristics comparable to the most productive gold regions in Australia and Canada.

- Production scale: Tanzania's annual gold output has grown consistently, with large-scale operations like Geita anchoring export revenue and foreign exchange generation.

- Lender familiarity: Repeated transaction activity, including the Nedbank Geita facility and the separate US$25 million gold-denominated loan arranged for Lake Victoria Gold's Imwelo project, is building institutional familiarity with Tanzanian mining credit risk among South African lenders.

- Gold price environment: Elevated gold prices in 2025 and 2026 have materially improved the revenue projections underpinning mining credit models, reducing perceived credit risk and attracting greater institutional appetite for African gold exposure.

Speculative Perspective: As South African banks continue expanding their East African mining finance portfolios, there is a reasonable case that Johannesburg could evolve into the primary hub for African mining capital markets activity, particularly for gold and battery metals transactions, gradually displacing the historical reliance on London-based project finance banks for large African mining credit facilities. This remains a directional thesis rather than a confirmed outcome, and investors should weigh it against the continued influence of international lenders in the largest transactions.

The next major ASX story will hit our subscribers first

What This Means for AngloGold Ashanti's Capital Allocation Strategy

From AngloGold Ashanti's perspective, securing a committed revolving credit facility of this scale serves multiple strategic functions simultaneously. Beyond the immediate liquidity benefit, it strengthens the company's negotiating position with Tanzanian authorities by demonstrating the depth of institutional confidence in the Geita operation's long-term viability. Furthermore, the broader context of gold M&A activity across global markets in 2025 underscores how critical robust asset financing has become for maintaining competitiveness.

The self-funding operational model at Geita also means that drawdowns on the revolving facility would typically be tactical rather than structural, deployed to smooth through temporary working capital dislocations rather than fund the mine's core capital programme. This conservative use of revolving credit is consistent with AngloGold Ashanti's broader balance sheet discipline and reflects a financing philosophy that prioritises financial flexibility over leverage maximisation.

Disclaimer: This article contains forward-looking analysis, scenario projections, and speculative perspectives regarding African mining finance trends. These sections represent analytical viewpoints and should not be construed as financial advice or investment recommendations. Investors should conduct independent due diligence before making any investment decisions. The confirmed facility size referenced in this article is US$300 million based on available deal announcements; readers should verify this figure against primary sources for investment or analytical purposes.

Want to Track the Next Major ASX Gold Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex data to surface actionable opportunities the moment they're announced. Explore historic discoveries and their returns, then start your 14-day free trial to position yourself ahead of the broader market.