June 22, 2026

The Underground Pivot Reshaping Canada's Copper Future

The global mining industry is quietly undergoing one of its most consequential technical transitions in decades. As the world's richest open-pit copper deposits approach the limits of economic extraction, major producers are descending underground, deploying mass-mining technologies that were once considered too capital-intensive for widespread adoption. Block caving, long reserved for exceptional geological circumstances, is rapidly becoming the preferred tool for unlocking the next generation of large-scale copper supply. Nowhere is this shift more tangible right now than in northwest British Columbia, where the Newmont Red Chris underground expansion approval has just cleared a major regulatory threshold, positioning one of Canada's most significant mineral endowments for transformation.

When big ASX news breaks, our subscribers know first

From Surface to Depth: Understanding the Block Cave Decision at Red Chris

Why Block Caving Makes Geological Sense Here

Block caving is fundamentally different from conventional open-pit mining in nearly every operational dimension. Rather than progressively removing overburden to access ore from above, block caving undercuts a large ore body from below, allowing gravity to do much of the work. As the undercut expands, the ore mass above it fractures and collapses into draw points, where it is collected and hauled to surface processing facilities.

For a deposit like Red Chris, this approach aligns closely with the ore body's physical geometry. Copper-gold porphyry systems of this scale typically extend thousands of metres vertically, meaning the ore that can be economically accessed via open pit represents only a fraction of the total mineral endowment. Continuing to deepen an open pit eventually crosses a threshold where the stripping ratio, the volume of waste rock removed per tonne of ore extracted, makes surface mining economically prohibitive. At Red Chris, that crossover point is approaching, and the underground transition is the logical response.

The deposit's known mineral inventory underscores just how much value remains below current pit limits:

| Attribute | Detail |

|---|---|

| Location | Golden Triangle, British Columbia, Canada |

| Primary Commodities | Copper, Gold |

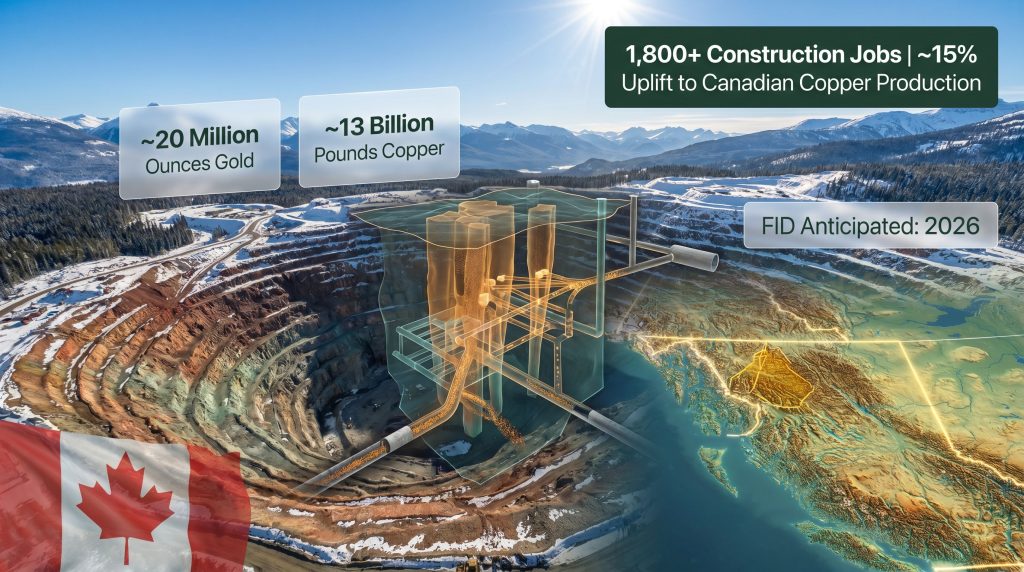

| Estimated Gold Resource | ~20 million ounces (measured, indicated and inferred) |

| Estimated Copper Resource | ~13 billion pounds (measured, indicated and inferred) |

| Projected Mine Life Extension | To the mid-2040s |

| Operator | Newmont (NYSE: NEM, TSX: NGT) |

| Joint Venture Partner | Imperial Metals (TSX: III), 30% stake |

| Deposit Classification | Copper-gold porphyry |

Importantly, Newmont has noted publicly that the initially permitted underground phase represents just the first stage of what could be a much longer mine life. The deposit's geometry and scale suggest meaningful exploration and development potential beyond what is currently being evaluated in the definitive feasibility study (DFS), meaning the permitted phase could be the foundation of a much larger long-term operation rather than its entirety.

The Operational Transition: Continuity and Complexity

Shifting from open-pit to underground is not a simple handover. During the early underground development phase, open-pit operations typically continue in parallel, providing production continuity while underground infrastructure, declines, ventilation systems, ore handling networks, and draw point construction proceeds. This blended production period is critical for maintaining cash flow and avoiding the kind of output gaps that can significantly affect a miner's near-term financial performance.

The complexity of managing both operational modes simultaneously adds to the capital requirements and project management demands, but for a deposit of Red Chris's scale, it is considered the most commercially rational path to unlocking the deeper ore.

What the Regulatory Approvals Actually Unlock

A Two-Part Approval Structure

The Newmont Red Chris underground expansion approval comprised two distinct but interdependent regulatory instruments. The first was an amended Environmental Assessment Certificate (EAC), the foundational document governing the project's environmental obligations and authorising the change in mining method. The original EAC was issued specifically for open-pit operations, meaning any transition to underground block caving required a formal amendment, effectively a re-evaluation of the project under BC's mining claims framework.

The second instrument was an amended Mines Act permit, which governs the operational, safety, and engineering conditions under which underground development can proceed. Together, these two approvals form the legal basis for construction and operational activities associated with the block cave transition. Neither approval alone would have been sufficient to unlock development, which is why both were required concurrently.

The Tahltan Nation's Role: Beyond Consultation

Perhaps the most structurally significant aspect of this approval process is how it was achieved. The amended EAC was secured through a consent-based process with the Tahltan Nation, the Indigenous group whose traditional territory encompasses the Red Chris project area in northwest British Columbia.

This distinction matters considerably in the context of Canadian resource law. Standard regulatory processes require that project proponents fulfil a duty-to-consult obligation with affected Indigenous groups, but that obligation does not inherently require consent. A consent-based framework goes further, embedding Indigenous decision-making authority into the approval pathway itself.

The Red Chris approval demonstrates that when Indigenous economic partnership is treated as a foundational project element rather than a late-stage compliance requirement, it can become a driver of regulatory efficiency rather than a source of delay.

The economic dimensions of the Tahltan partnership extend beyond the approval process. The framework is structured to deliver ongoing economic benefits to Tahltan communities, including employment, contracting opportunities, and revenue-sharing arrangements over the project's operational life. This model of substantive economic partnership, rather than procedural consultation, is increasingly being referenced as a template for resource project development across Canada.

Key Industry Insight: The Red Chris block cave project represents the sixth major BC mine or mine extension to receive regulatory clearance within an 18-month period, according to the Mining Association of British Columbia. The industry body has publicly called on the provincial government to build on this momentum by further accelerating permitting timelines to strengthen Canada's competitive position in critical mineral supply chains.

Newmont's Capital Allocation Framework and the Path to FID

Stage-Gating: How Major Miners Manage Risk at Scale

Understanding where the Newmont Red Chris underground expansion approval sits within Newmont's broader decision-making architecture requires familiarity with stage-gating, a structured capital allocation methodology used extensively across the major mining sector.

In stage-gating, a project progresses through defined phases, each separated by a decision gate where management and the board evaluate technical, regulatory, financial, and commercial parameters before committing further capital. This approach prevents premature capital deployment into projects that have not yet de-risked sufficiently to justify large financial commitments.

The Red Chris block cave project's stage-gate milestones can be summarised as follows:

-

Regulatory approval secured (completed, June 2026): amended EAC and Mines Act permit received, clearing the critical environmental and operational compliance gate.

-

Definitive Feasibility Study completion (in progress): the DFS will establish the detailed capital cost estimate, production schedule, processing throughput, infrastructure specifications, and economic model underpinning the Final Investment Decision.

-

Final Investment Decision (FID) (anticipated late 2026): board-level sanctioning of full project capital commitment, contingent on DFS outcomes meeting Newmont's return thresholds.

-

Engineering, procurement, and construction management (EPCM) mobilisation: engagement of specialist contractors to commence detailed engineering and procurement of long-lead items.

-

Underground development commencement: initial portal development, decline construction, and establishment of early-stage underground infrastructure.

-

Phased production ramp-up: transition from open-pit to blended production, progressing toward full underground block cave operation.

What the DFS Will Determine and Why It Matters

The definitive feasibility study is the document upon which Newmont's board will base its FID. Its outputs carry substantial weight for investors and analysts tracking the project's economic viability. Key parameters the DFS will establish include:

-

Total capital expenditure (capex): several billion Canadian dollars are expected, with the precise figure dependent on underground infrastructure scope, processing plant modifications, and regional construction cost benchmarks.

-

Mine throughput and production rates: how many tonnes of ore per day the block cave will process, and the resulting annual copper and gold output.

-

Operating cost structure: the per-tonne cost profile of underground operations, which in a mature block cave is typically lower than open-pit mining at equivalent scales.

-

Economic sensitivity analysis: how project NPV and internal rate of return respond to copper and gold price fluctuations, capital cost overruns, and throughput variations.

Investors should note that DFS outcomes are not guaranteed to confirm project advancement. If capital cost estimates exceed Newmont's internal hurdle rates under conservative commodity price assumptions, the company retains the option to defer or restructure the project scope. This is a material risk that should be factored into any assessment of project probability.

Economic Scale and Regional Impact

What the Numbers Reveal About Red Chris's Significance

The economic footprint of the Newmont Red Chris underground expansion is substantial enough to have meaningful effects at the national level, not merely regional:

| Economic Metric | Projected Figure |

|---|---|

| Construction Phase Jobs | 1,800+ direct positions |

| Peak Operating Jobs | ~1,500 sustained roles |

| Operating Employment Duration | At least through 2040 |

| Capital Investment Scale | Several billion dollars (CAD) |

| Impact on Canadian Copper Output | ~15% increase in national production |

A 15% uplift to Canada's total copper production from a single project is a striking figure. It reflects both the scale of the Red Chris ore body and the relatively concentrated nature of Canada's current copper production base. For context, the copper supply crunch tied to electric vehicle manufacturing, grid infrastructure buildout, and renewable energy deployment continues to point toward structural supply deficits emerging later this decade, making large new supply additions increasingly strategically significant.

Northwest BC as an Emerging Mining District

The regional significance of the Red Chris approval cannot be assessed in isolation. Northwest British Columbia is progressively assembling the infrastructure and institutional frameworks that define a world-class mining district. Furthermore, when compared to the largest copper mines globally, Red Chris's ore body stands as a genuinely significant resource.

-

Clean hydroelectric power: access to BC Hydro's grid, including the Northwest Transmission Line, provides a competitive advantage in both operating cost and carbon intensity relative to diesel-dependent remote operations.

-

Port connectivity: the region's access to tidewater supports concentrate export logistics at competitive cost.

-

Mineral endowment density: the Golden Triangle hosts multiple world-class deposits across copper, gold, and silver, with Red Chris representing one of the largest undeveloped porphyry systems in the Americas.

-

Indigenous economic partnership maturity: the Tahltan Nation's sophisticated engagement with resource development has established a framework that attracts capital rather than creating uncertainty.

Newmont's commitment to northwest BC was substantially deepened by its US$17 billion acquisition of Newcrest in 2023, which brought both Red Chris and the Brucejack gold mine into its portfolio. The company has publicly indicated its intention to maintain a lengthy operational presence in the region, treating it as a core geographic pillar of its long-term production strategy rather than a transitional asset.

Block Caving's Broader Role in Copper Supply Strategy

The Technical Case for Underground Mass Mining

Globally, the mining industry faces a structural problem. The most accessible, highest-grade open-pit copper deposits are progressively depleting, while average ore grades at existing operations continue to decline. According to data tracked by industry analysts, average copper ore grades at major producing mines have fallen by roughly 25-30% over the past two decades, forcing miners to process substantially more material to produce the same volume of copper.

Block caving offers a partial solution to this challenge. By enabling the economic extraction of large, lower-grade ore bodies that cannot support open-pit economics at depth, block caving expands the universe of mineable copper resources. The technology's key financial characteristic is its cost structure: while upfront capital requirements are significant, typically running into the billions of dollars for a project of Red Chris's scale, the resulting operating cost per tonne is among the lowest of any hard rock mining method once the cave is established and draw points are producing at full capacity.

Operational Risks Specific to Block Caving

Block caving is not without its own technical challenges, and investors and observers evaluating the Red Chris block cave project should be aware of the key risk categories:

-

Subsidence management: as the cave propagates upward through the ore body, surface subsidence above the cave zone must be carefully managed, particularly regarding environmental monitoring obligations and infrastructure exclusion zones.

-

Draw point scheduling: the sequencing of draw point activation and ore extraction rates is critical to cave propagation, fragmentation management, and dilution control. Poor draw control can result in increased waste rock contamination of the ore stream, degrading mill feed grades.

-

Geotechnical risk: the rock mass conditions at Red Chris will be characterised in detail during the DFS phase. Underground stress conditions, structural geology, and groundwater management all influence the design and performance of the cave.

-

Ramp-up duration: block caves have typically long ramp-up periods before reaching steady-state production. It is not uncommon for major block cave operations to take three to five years after initial undercutting to reach full production capacity, a timeline that must be reflected in investor expectations about production profiles.

Disclaimer: All forward-looking projections and economic figures referenced in this article are based on publicly disclosed company announcements and industry estimates. They involve assumptions that may not prove accurate. Investors should conduct independent due diligence and seek professional financial advice before making investment decisions related to any mining company or project.

The next major ASX story will hit our subscribers first

BC's Permitting Environment: Momentum or Milestone?

Six Approvals in 18 Months: What It Signals

The Mining Association of British Columbia's observation that Red Chris represents the sixth major mine or mine extension permitted in the province within 18 months carries analytical weight beyond the individual project. It suggests a directional shift in BC's regulatory processing efficiency, though the structural drivers of that shift warrant careful evaluation.

British Columbia has historically been viewed within the global mining investment community as a jurisdiction with a robust regulatory framework but sometimes extended timelines for project advancement. The concentration of approvals in recent months reflects several converging factors:

-

Refinements to the Environmental Assessment process that have improved predictability of timelines without reducing scrutiny of environmental obligations.

-

The maturation of First Nations economic partnership models, which has reduced the adversarial dynamics that previously extended consultation timelines.

-

A provincial economic development agenda that recognises mining's role in funding public services through tax and royalty revenues.

Premier David Eby's public framing of the Red Chris approval emphasised that partnership agreements with First Nations and regulatory predictability are what create the conditions for major private-sector capital investment. The fiscal logic underlying this position is straightforward: projects of Red Chris's scale generate substantial royalty, corporate tax, and payroll tax revenues that directly support provincial program spending.

The Competitive Context: Canada vs. Global Mining Jurisdictions

Canada competes for a globally mobile pool of mining capital investment with jurisdictions across Latin America, Africa, and Australia. The Mining Association of British Columbia's call for further permitting acceleration reflects an awareness that, while recent momentum is encouraging, BC's competitiveness relative to peers with faster approval pathways remains a live issue.

For projects requiring the scale of capital that Red Chris demands, investment decisions are sensitive to jurisdictional risk perceptions. Every additional year of regulatory uncertainty represents a meaningful cost of capital impact. Consequently, the ability to demonstrate that consent-based Indigenous engagement and environmental rigour can coexist with efficient timelines is therefore both a commercial and a reputational asset for the province. Investors exploring copper investment strategies will find BC's improving regulatory environment an increasingly relevant factor in project-level risk assessments.

The Road Ahead: What Happens Before Construction Begins

Key Milestones and Risk Factors

With the Newmont Red Chris underground expansion approval secured, the critical path to construction is now defined primarily by the DFS completion and FID timing. The key variables that will determine whether and when construction commences include:

-

Copper and gold price trajectories: both commodities directly influence project NPV. Sustained weakness in either could compress returns below Newmont's internal approval thresholds.

-

Capital cost inflation: the construction materials and skilled labour markets in British Columbia and across Canada have experienced significant cost pressure in recent years. The DFS will need to reflect current cost benchmarks accurately.

-

Board-level capital prioritisation: Newmont manages a large global portfolio of development projects. The Red Chris block cave will compete for capital allocation against other opportunities, and its relative ranking within that portfolio influences FID timing.

-

Ongoing environmental monitoring: the amended EAC carries conditions that must be satisfied through the development phase. Compliance with these conditions is a prerequisite for maintaining the approvals in good standing.

For those tracking the project's progress, the completion of the definitive feasibility study and the subsequent FID, anticipated in late 2026, will be the defining events determining whether the Newmont Red Chris underground expansion moves from approved concept to funded construction. In addition, the broader implications for the copper supply crunch mean this project's advancement will be closely watched by analysts, investors, and policymakers well beyond British Columbia's borders.

Want to Be First When the Next Major Copper Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly cutting through complex geological data to surface actionable opportunities in copper and beyond — so begin your 14-day free trial today and explore how historic mineral discoveries have generated substantial returns for investors who positioned early.