August 1, 2026

The Hidden Revenue Engine Reshaping South Africa's PGM Sector

Few dynamics in resource extraction are as consequential as the moment a waste stream becomes a profit centre. For decades, chrome concentrate recovered during platinum group metal mining in South Africa was treated largely as an operational footnote, a mineral fraction separated from UG2 reef ore and sold at marginal value. That characterisation no longer holds. Across the Bushveld Igneous Complex, chrome has undergone a quiet reclassification, one driven not by geology but by the brutal arithmetic of PGM basket price compression.

The Northam Platinum chrome production surge recorded in FY2026 is the clearest evidence yet that this reclassification is now shaping operational strategy at the mine planning level, not merely the marketing department.

When big ASX news breaks, our subscribers know first

Understanding the UG2 Reef: Why Chrome and PGMs Are Inseparable

To understand why the Northam Platinum chrome production surge carries such strategic weight, it is necessary to start underground. The Bushveld Igneous Complex, which underlies much of South Africa's North West, Limpopo, and Mpumalanga provinces, contains two principal platinum-bearing ore horizons: the Merensky Reef and the Upper Group 2, or UG2, reef.

The UG2 is a chromitite layer, meaning it is composed predominantly of chromite minerals interlocked with PGM-bearing sulphide phases. Crucially, UG2 ore carries substantially higher chrome content than Merensky Reef ore, with chromite typically constituting between 60% and 90% of the UG2 reef by mass in certain horizons. When UG2 ore is processed through a concentrator, chrome concentrate is a natural and unavoidable output alongside the PGM-rich fraction.

This geological reality creates a structural dual-commodity opportunity that most PGM miners have historically under-optimised. The Northam Platinum chrome production surge in FY2026 reflects a deliberate shift toward maximising both commodity streams simultaneously. Furthermore, supply constraints in the PGM market have made this dual-stream approach even more commercially compelling for producers with UG2 exposure.

Key geological and processing characteristics of UG2 mining worth understanding:

- UG2 reef widths typically range from 0.5 to 2 metres, requiring precision mechanised mining methods to minimise dilution

- Chrome recovery from UG2 concentrators depends heavily on milling intensity and spiral concentrator circuit design

- Over-milling UG2 ore can liberate chrome particles too finely for effective recovery, meaning circuit calibration directly affects chrome yield

- Higher chrome recovery rates do not automatically degrade PGM recoveries, but the two circuits must be carefully balanced

Northam's incremental upgrades to its concentrator circuits across multiple operations improved chrome recovery rates in FY2026, compounding the volume gains generated at the asset level.

Eland Platinum: The Operational Transformation Behind the Numbers

What drove Eland's exceptional output growth?

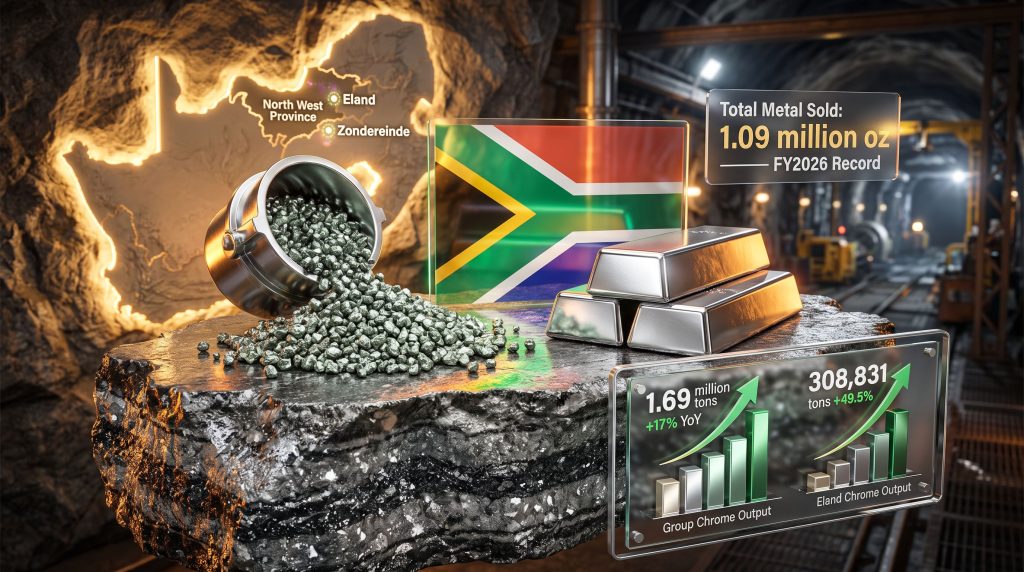

The scale of the Northam Platinum chrome production surge becomes most visible at the Eland mine in the North West Province. Eland delivered a 49.5% increase in chrome output, reaching 308,831 tons in FY2026. This single asset was the primary driver of group-wide chrome output reaching 1.69 million tons, a 17% year-on-year increase from the prior year's 1.44 million tons. Confidence in Northam climbs as Eland upgrade pays off, according to Business Day, reflecting broader market recognition of the asset's transformation.

Three distinct operational interventions produced this outcome:

| Operational Change | Detail | Production Effect |

|---|---|---|

| Workforce scale-up | Crews expanded from approximately 25 to 50 personnel | Higher stope throughput per shift cycle |

| Ventilation system overhaul | Airflow reorganised to enable simultaneous multi-blast mining | Faster face advance rates across active panels |

| Inter-asset ore management | Surplus ore from Zondereinde's at-capacity concentrator redirected to Eland | Additional feed volume without new capital commitment |

The third lever is particularly instructive from an operational management perspective. When Zondereinde, Northam's oldest and most established mine, reached concentrator capacity during the year, surplus ore that would otherwise have created a processing bottleneck was redirected to Eland's circuit. This opportunistic redeployment generated incremental chrome output at Eland without requiring any greenfield capital expenditure.

This type of inter-asset ore management is rarely discussed in mainstream mining commentary but represents a sophisticated form of capital-light production optimisation that materially improves group-level economics.

The momentum had already been building. In the first half of FY2026, covering the six months to December 31, 2025, Eland's chrome output grew 19.6%, contributing to a group H1 chrome increase of 14.8% to 822,759 tons. Looking further back, Eland's H1 FY2025 chrome concentrate production surged 113.1% to 115,387 tons against the prior comparable period, signalling that the ramp-up trajectory at this asset has been sustained and accelerating.

PGM Price Pressure and Why Chrome Diversification Matters Now

The timing of the Northam Platinum chrome production surge is not coincidental. The PGM basket price declined approximately 40% from a peak of roughly $2,900 per ounce in January 2026, creating a revenue environment that has forced producers to examine every available income stream with renewed discipline. Consequently, the commodity price impact on producer margins has made chrome diversification not merely attractive but strategically essential.

The mechanism behind this correction is important for investors to understand correctly. The primary driver has not been a collapse in industrial demand for platinum or palladium. It has been a withdrawal of financial investment:

- Platinum ETF holdings fell by approximately 574,000 ounces from their January 2026 peak

- Nymex futures holdings declined by approximately 288,000 ounces from peak levels

- CME positioning in palladium has returned to a net short configuration

This distinction between financial market positioning and physical supply-demand fundamentals is critical. When ETF investors liquidate platinum holdings, they create real selling pressure in spot and futures markets without any corresponding change in industrial consumption patterns. The result is a price correction that does not necessarily reflect the underlying supply-demand balance. Understanding the broader platinum and palladium market dynamics is therefore essential context for interpreting Northam's strategic response.

HSBC analyst James Steel has forecast a platinum supply-demand deficit of approximately 531,000 ounces for 2026, and anticipates a price recovery despite having revised his average annual price estimate downward. Steel similarly projects palladium supply-demand deficits to widen moderately through 2026 and into 2027, even as futures markets maintain a net short posture. (Source: MiningMX, July 2026)

The divergence between physical market deficits and financial market net-short positioning is a classic setup that commodity market historians will recognise. It tends to resolve when physical tightness forces short-covering, but the timing is notoriously difficult to predict.

FY2026 Production Record in Full Context

The chrome surge occurred alongside a broader operational milestone for the group. FY2026 represented Northam's strongest production year to date across multiple metrics. Northam hits new PGM output record while chrome surges, as reported by MiningMX, confirming the scale of the group's operational achievement.

| Production Metric | FY2026 Result | Year-on-Year Change |

|---|---|---|

| Own-mine equivalent refined PGM output | 938,754 oz | +4.4% |

| Third-party metal purchased | 158,138 oz | +24.4% (record) |

| Total metal sold | 1.09 million oz | +8.0% (record) |

| Group chrome output | 1.69 million tons | +17.0% |

| Eland chrome output | 308,831 tons | +49.5% |

The 24.4% surge in third-party metal purchases to a record 158,138 ounces deserves attention. Northam's active participation in concentrate purchasing markets allows it to process third-party ore through its refining infrastructure, effectively monetising spare smelting and refining capacity. This is a relatively underappreciated revenue mechanism that amplifies the group's total metal sold figure beyond what its own mining operations alone could deliver.

Northam crossed the one million ounce PGM production milestone in FY2025, a long-stated strategic target. FY2026 extended that achievement to a record 1.09 million ounces of total metal sold, demonstrating that the milestone was not a one-off outcome but the beginning of a new operational baseline.

The Chrome Export Policy Question: Regulatory Risk Without Certainty

Any analysis of the Northam Platinum chrome production surge must engage with the regulatory shadow hanging over South Africa's chrome export sector. The Department of Mineral and Petroleum Resources has floated proposals to cap raw chrome ore and concentrate exports as part of a broader industrial beneficiation policy. The underlying objective is to drive more chrome into domestic ferrochrome smelting rather than exporting the raw material for processing elsewhere.

South Africa is already the world's largest producer of chrome ore, contributing roughly 45% of global supply. In addition, South Africa's ferroalloys sector plays a critical role in determining how regulatory changes of this nature would ripple through downstream processing and export revenues. The proposed policy reflects a recurring tension in South African industrial strategy between commodity export revenues and downstream value addition.

However, the regulatory situation requires careful framing:

- As of the FY2026 reporting period, the export cap remains a policy proposal and has not been gazetted as binding regulation

- The DMPR has explicitly characterised the measure as a proposal rather than a firm undertaking

- South Africa has a documented history of beneficiation proposals undergoing significant modification or delay before implementation

- The South32-Alcoa transaction and related policy discussions have exposed ongoing tensions within government between beneficiation ideology and investment attractiveness

| Regulatory Scenario | Near-Term Probability | Potential Impact on Chrome Producers |

|---|---|---|

| Export cap enacted as proposed | Moderate | Revenue reduction; possible ferrochrome investment requirement |

| Policy revised or implementation delayed | High | Status quo revenue profile maintained |

| Full domestic beneficiation mandate imposed | Low (near-term) | Structural cost increase; margin compression unless ferrochrome pricing compensates |

Investors should treat this as a watch item requiring monitoring, not an imminent operational threat. The key signal to track is a formal gazette notice from the DMPR, which would mark the transition from policy discussion to regulatory implementation.

The next major ASX story will hit our subscribers first

Supply Contraction, Lead Times, and the Medium-Term Thesis

Why do supply lead times create an asymmetric investment setup?

One of the less widely appreciated structural features of the global PGM market is the extraordinary length of time required to bring new primary supply into production. A greenfield platinum mine in South Africa typically requires eight to twelve years from initial resource definition through to steady-state production, incorporating feasibility studies, environmental authorisation, shaft sinking, underground development, and plant construction.

This lead time dynamic means that the supply response to any sustained period of higher prices is structurally delayed. Conversely, periods of price weakness, like the current correction, actively suppress the capital allocation decisions that would be needed to maintain future supply. The result is a ratchet effect: price weakness today reduces the pipeline of new supply available three to ten years from now.

Northam's own production guidance for the next two financial years points toward higher tonnages and improved grades as capital projects across its portfolio reach completion. Combined with a group-level view that primary PGM supply will continue declining well into the next decade, the operational growth trajectory is positioned to benefit disproportionately from any medium-term price recovery. (Source: MiningMX, July 2026)

Global primary PGM and chrome supply is broadly expected to keep contracting, as no major new mining projects are approaching production readiness in any jurisdiction at scale sufficient to offset depletion at existing operations. Furthermore, the broader trend of mining industry consolidation is reshaping which producers are positioned to capitalise when price recovery eventually arrives.

What This Means for Investors Watching the PGM Sector

Synthesising the operational, geological, and market dynamics above into an investor framework produces several distinct observations:

-

Chrome is now a structural revenue buffer, not an incidental byproduct. Producers with growing UG2 exposure and optimised chrome recovery circuits carry a form of operational hedging that pure-play PGM producers do not.

-

The ETF-driven price correction has created a wedge between financial market sentiment and physical market fundamentals. Historically, such wedges close in the direction of the physical balance, though timing is uncertain and further downside from financial market positioning cannot be ruled out in the near term.

-

Third-party metal purchasing at scale represents an under-followed growth lever. Northam's record 158,138 ounces of purchased metal in FY2026 reflects refining infrastructure utilisation that generates returns without proportional increases in mining capital expenditure.

-

Regulatory risk on chrome exports is real but not imminent, and experienced South African mining investors will recognise that the distance between a DMPR proposal and enacted regulation is frequently substantial in both time and final form.

-

Supply lead times create an asymmetric medium-term setup where current price weakness, if sustained, ensures the next supply cycle is smaller rather than larger, setting the conditions for a deficit-driven recovery.

Disclaimer: This article contains forward-looking analysis, analyst forecasts, and scenario assessments that involve inherent uncertainty. Nothing in this article constitutes financial advice. Investors should conduct independent due diligence and consider their own risk tolerance before making investment decisions relating to PGM sector equities or commodity exposures.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly converting complex geological and commodity data into actionable investment insights — explore historic discoveries and their exceptional returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.