July 22, 2026

The Strategic Imperative for Nuclear Fuel Autonomy

Global energy markets face unprecedented disruption as traditional nuclear fuel supply chains confront geopolitical tensions and resource competition. The complexity of nuclear fuel production creates multiple vulnerability points that extend far beyond simple commodity trading. Understanding how nations achieve the U.S. nuclear fuel independence requires examining the intricate web of mining, conversion, enrichment, and recycling technologies that form the backbone of civilian nuclear power generation.

Furthermore, nuclear fuel independence represents more than energy security; it encompasses technological sovereignty, economic resilience, and strategic defence capabilities. Countries operating significant nuclear reactor fleets must navigate the challenge of securing uranium supplies, conversion services, and enrichment capacity whilst managing long-term fuel cycle economics and environmental considerations.

Current Global Vulnerability Metrics:

- Global uranium production concentration: Top five countries control 85% of output

- Conversion facility bottlenecks: Only five major plants worldwide

- Enrichment capacity distribution: Russia controls 44% of global capability

- Advanced reactor fuel gap: Minimal HALEU production outside of research facilities

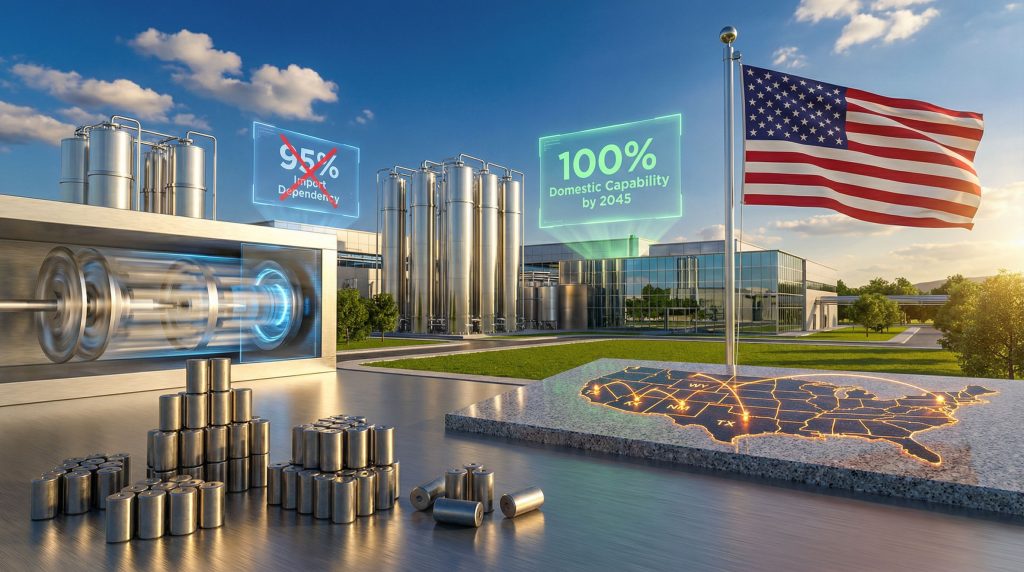

The United States operates 93 commercial nuclear reactors generating approximately 20% of domestic electricity, yet imports over 90% of required uranium whilst maintaining insufficient enrichment infrastructure. This dependency creates cascading risks across multiple supply chain segments, from raw material procurement through final fuel assembly manufacturing.

When big ASX news breaks, our subscribers know first

What Are the Core Components of Nuclear Fuel Independence?

Mining and Extraction Infrastructure

Nuclear fuel independence begins with domestic uranium extraction capabilities spanning diverse geological formations and extraction methodologies. The technical complexity of uranium mining varies significantly based on ore grade, geological characteristics, and environmental considerations, requiring specialised knowledge of hydrogeology, radiological safety, and metallurgical processing.

Current U.S. Production Landscape:

Burke Hollow facility in South Texas commenced operations in April 2026, representing the largest in-situ recovery project initiated in over a decade. The 20,000-acre site contains an estimated 6.15 million pounds of U3O8, utilising advanced U.S. ISR technology to extract uranium from sandstone aquifers at depths of 400-800 feet below surface.

Wyoming's uranium belt contains multiple ISR facilities under various stages of development, with identified resources exceeding 350,000 tons of U3O8. The region's geology features roll-front uranium deposits formed by ancient groundwater flow, creating concentrated ore zones suitable for solution mining techniques.

New Mexico's Grants Mineral Belt historically produced 280 million pounds of U3O8 between 1950 and 2002, demonstrating the region's substantial uranium endowment. Current estimates indicate remaining resources of approximately 150,000 tons, though extraction would require conventional mining methods due to higher ore grades averaging 0.15-0.25% U3O8.

Technical Extraction Methods Comparison:

| Method | Capital Requirements | Environmental Footprint | Production Timeline | Operating Costs |

|---|---|---|---|---|

| In-Situ Recovery | $20-40 million | Minimal surface impact | 18-24 months | $25-35/lb U3O8 |

| Conventional Mining | $100-300 million | Significant surface disruption | 5-7 years | $30-50/lb U3O8 |

| Solution Mining | $40-60 million | Controlled environmental impact | 24-36 months | $30-40/lb U3O8 |

In-situ recovery technology offers significant advantages for uranium extraction in sedimentary formations, utilising controlled chemical leaching to dissolve uranium from host rock without large-scale excavation. The process involves injecting oxygenated groundwater with dissolved carbon dioxide into uranium-bearing aquifers, creating oxidising conditions that mobilise uranium into solution for recovery at production wells.

ISR Technical Process Details:

- Wellfield development: Injection and recovery well pairs spaced 50-100 feet apart

- Leaching solution: Oxygenated water with pH adjustment using CO2 or weak acids

- Recovery rates: 60-80% uranium extraction from ore zones

- Aquifer restoration: Post-mining groundwater cleanup to baseline conditions

- Operational lifespan: 10-20 years depending on resource size and grade

Conversion and Enrichment Capacity

Nuclear fuel independence requires comprehensive conversion infrastructure to transform uranium oxide concentrates into uranium hexafluoride gas, the feedstock for enrichment operations. Conversion represents a critical chokepoint in the fuel cycle, with limited global capacity concentrated among few facilities worldwide.

Current U.S. Infrastructure Gaps:

The United States lacks operational uranium conversion capacity, creating complete dependency on foreign suppliers for UF6 production. Global conversion capacity totals approximately 150,000 tons U3O8 equivalent annually, with Russia controlling roughly 60,000 tons through Rosatom facilities.

France operates significant conversion capacity through Orano facilities, whilst China has expanded domestic capability to support reactor construction programmes. Canada maintains conversion operations primarily for export markets, though capacity remains limited relative to global demand growth projections.

U.S. Enrichment Operations:

Urenco USA operates the nation's sole commercial enrichment facility in Eunice, New Mexico, producing approximately 2.8 million separative work units (SWU) annually. The facility employs gas centrifuge technology to increase U-235 concentration from natural levels (0.7%) to reactor-grade specifications (3-5%).

Current U.S. enrichment capacity addresses roughly 25-30% of domestic reactor requirements, necessitating substantial imports to meet operational demand. Advanced reactor development creates additional demand for high-assay low-enriched uranium (HALEU) enriched to 5-20% U-235, requiring specialised centrifuge configurations not widely available.

Planned Infrastructure Expansion:

- 2026-2028: Groundbreaking on new enrichment facilities targeting 4-6 million SWU capacity

- 2029-2031: Commercial conversion plant operations beginning

- 2032-2035: HALEU production capabilities for advanced reactor fuel

- 2036-2040: Complete fuel cycle independence achievement

How Do Legislative and Policy Frameworks Support Independence Goals?

The Prohibiting Russian Uranium Imports Act

Legislative action targeting Russian uranium imports fundamentally restructures U.S. nuclear fuel procurement, creating market incentives for domestic infrastructure development whilst managing transition periods for existing reactor operations. This initiative directly addresses the Russian uranium ban impact on supply chains.

Implementation Structure:

The legislation effective August 2024 prohibits new Russian uranium purchases whilst providing waiver authority through 2028 for existing contractual obligations. This approach balances immediate strategic objectives with practical recognition of supply chain transition requirements.

Economic impact analysis indicates the prohibition affects approximately $1 billion in annual uranium imports, creating domestic market opportunity equivalent to 15,000-20,000 tons of U3O8 annually. Waivers remain available for reactor operators demonstrating supply security concerns, though approval requires comprehensive justification.

Strategic reserve provisions authorise government stockpiling of domestically-produced uranium, creating market floor pricing for U.S. mining operations whilst establishing emergency supply buffers. Reserve targets encompass 90-day reactor operating requirements, totalling approximately 6,000-8,000 tons of enriched uranium product.

Nuclear Fuel Security Act of 2023

Comprehensive federal investment authorisation addresses multiple fuel cycle segments through direct funding, loan guarantees, and procurement commitments extending through 2035.

Investment Allocation Framework:

- Uranium mining revival: $2.7 billion federal commitment supporting 8-12 new mining operations

- Enrichment infrastructure: $3.4 billion facility development targeting 8-10 million SWU capacity

- Conversion capability: $1.8 billion investment in domestic UF6 production

- Research and development: $800 million advanced fuel cycle technology programmes

Procurement Guarantee Structure:

The Department of Energy commits to purchasing domestically-produced uranium at market-competitive pricing, providing investment certainty for private capital deployment. Long-term contracts spanning 15-20 years justify infrastructure development costs whilst ensuring government supply security.

Procurement volumes target 25% of government reactor requirements initially, escalating to 75% by 2035. Price mechanisms incorporate market indexing with minimum floor pricing to protect producer economics during commodity cycle downturns.

What Role Does Spent Fuel Recycling Play in Independence Strategy?

Resource Utilisation Optimisation

Nuclear fuel recycling transforms waste management challenges into strategic resource opportunities, potentially extending uranium supplies by decades whilst reducing repository requirements. Advanced recycling technologies offer 95% resource recovery efficiency compared to current once-through fuel cycles, addressing nuclear waste disposal safety concerns.

Current Waste Stream Analysis:

Accumulated spent fuel totalling approximately 90,000 metric tons contains substantial recoverable resources including 85% of original uranium content and weapons-usable plutonium suitable for mixed-oxide fuel production. Recycling implementation could eliminate uranium mining requirements for 25-30 years whilst supporting existing reactor operations.

The current storage approach treats spent fuel as waste requiring permanent disposal, ignoring significant economic value in recoverable materials. International experience demonstrates recycling feasibility, with France achieving 96% resource recovery through aqueous reprocessing operations.

Advanced Recycling Technology Pathways:

| Technology | Uranium Recovery | Plutonium Separation | Capital Investment | Implementation Timeline |

|---|---|---|---|---|

| Pyroprocessing | 95% efficiency | Partial recovery | $15-20 billion | 15-20 years |

| Aqueous Methods | 99% separation | Complete recovery | $10-15 billion | 10-15 years |

| Advanced Aqueous | 99% efficiency | Selective separation | $12-18 billion | 12-18 years |

Pyroprocessing technology utilises high-temperature electrochemical methods to separate uranium and transuranics from fission products, offering proliferation-resistant characteristics whilst achieving excellent recovery rates. The process operates at 500°C in molten salt electrolytes, avoiding aqueous chemistry concerns.

Economic and Strategic Benefits

Recycling implementation generates multiple value streams including recovered uranium worth $15-20 per pound, plutonium suitable for reactor fuel, and significant reduction in waste disposal requirements. Economic analysis indicates recycling operations achieve profitability at uranium prices exceeding $80-100 per pound.

Strategic Resource Extension:

Recycling extends domestic uranium resources by factor of 50-100 compared to once-through fuel cycles, effectively eliminating import dependency for uranium supplies. Combined with domestic mining expansion, recycling creates surplus capacity for potential export markets whilst supporting allied fuel security.

Repository requirements decrease by 85-90% through recycling implementation, reducing disposal costs whilst extending Yucca Mountain capacity indefinitely. High-level waste volume reduction simplifies transportation logistics and community acceptance for nuclear expansion.

How Do Geopolitical Factors Influence Independence Strategies?

Russia's Market Dominance and Weaponisation

Russian control over global uranium markets extends beyond production to encompass conversion services, enrichment capacity, and technology transfer. Rosatom's integrated approach creates systematic dependencies that restrict Western strategic autonomy in nuclear fuel cycles, contributing to uranium market volatility.

Global Market Control Mechanisms:

Russia maintains 44% of global enrichment capacity through advanced centrifuge technology, whilst controlling significant conversion capability and establishing long-term contracts with major uranium producers in Kazakhstan and Uzbekistan. This vertical integration creates multiple leverage points for market manipulation.

Export restrictions implemented in 2024 demonstrate Russian willingness to weaponise energy supplies, affecting approximately 15-20% of global nuclear fuel trade. Strategic partnerships with China and India provide alternative markets, reducing Western leverage in bilateral negotiations.

Resource Weaponisation Examples:

- 2024 uranium export limitations targeting NATO allies

- Kazakhstan production agreements favouring Russian purchasers

- Technology transfer restrictions for Western enrichment projects

- Joint ventures with Chinese nuclear companies expanding market presence

Allied Cooperation Through Sapporo 5 Initiative

Multilateral coordination among democratic allies creates alternative supply chain structures reducing dependency on authoritarian regimes. The Sapporo 5 framework encompasses resource sharing, technology development, and coordinated investment strategies.

Participating Nations Contributions:

Canada provides reliable uranium supplies through established mining operations in Saskatchewan, contributing approximately 15% of global production. Long-term supply agreements with allied nations create predictable revenue streams supporting continued exploration and development.

Australia offers substantial uranium resources through existing mining operations and undeveloped deposits, though political considerations limit expansion potential. Regulatory frameworks require careful navigation to maximise resource access whilst addressing environmental concerns.

France contributes enrichment capacity and recycling technology through Orano operations, whilst the United Kingdom provides advanced fuel cycle expertise and research capabilities. Japan offers advanced reactor technology and HALEU development programmes supporting next-generation nuclear deployment.

Strategic Resource Sharing Framework:

- Coordinated uranium procurement reducing market competition among allies

- Technology transfer agreements accelerating capability development

- Joint facility development sharing capital costs and technical risks

- Emergency supply protocols ensuring continuous reactor operations

What Are the Economic Implications of Nuclear Fuel Independence?

Investment Requirements and Returns

Nuclear fuel independence requires substantial capital deployment across multiple industry segments, with total investment estimates ranging from $15-25 billion over the next decade. Investment returns depend on successful market capture, cost competitiveness, and political sustainability of support programmes, particularly given U.S. uranium disruption concerns.

Sector Investment Breakdown:

Mining infrastructure requires $4-6 billion in capital deployment supporting 8-12 new uranium extraction facilities. ISR technology reduces capital intensity compared to conventional mining whilst offering faster project timelines and improved environmental profiles.

Conversion and enrichment facilities demand $8-12 billion investment for establishing comprehensive fuel cycle capability. Facility construction timelines span 6-10 years requiring sustained political support through multiple election cycles.

Economic Impact Analysis:

Job creation potential ranges from 50,000-75,000 direct positions across mining, conversion, and enrichment operations. Indirect employment effects multiply total job impact by factor of 2-3 through supporting industries and regional economic development.

Rural community revitalisation occurs primarily in uranium-rich regions including Wyoming, New Mexico, and South Texas. Mining operations provide high-paying technical positions whilst generating substantial tax revenue for local governments.

Market Price Stabilisation Effects:

Domestic production capability reduces exposure to volatile international uranium markets, providing price stability for reactor operators through long-term contract mechanisms. Strategic reserve operations offer additional price buffering during supply disruptions.

Import substitution retains $1.2-1.5 billion annually within domestic economy, supporting continued infrastructure investment and technology development. Export potential emerges once domestic demand satisfaction allows surplus capacity utilisation.

Competitive Positioning

Global nuclear fuel markets undergo fundamental restructuring as major consumers develop domestic capabilities. Competition intensifies among established suppliers facing reduced market access whilst new entrants seek market penetration.

Market Share Transformation:

Current U.S. position as net importer transitions toward balanced domestic supply by 2030-2032, with potential export capability emerging by 2035-2040. Market share objectives target 25-30% of global enrichment capacity and 15-20% of conversion services.

Technology advantages in advanced reactor fuel provide competitive differentiation, as HALEU demand grows with small modular reactor deployment. U.S. facilities could capture majority market share for specialised fuel products serving next-generation reactors.

Strategic Timeline Objectives:

- 2025-2028: Import dependency reduction to 50-60% of total requirements

- 2029-2035: Domestic supply coverage reaching 75-85% of reactor needs

- 2036-2040: Export market participation with surplus capacity

- 2041-2050: Technology leadership in advanced fuel cycle services

The next major ASX story will hit our subscribers first

How Do Advanced Reactor Technologies Drive Independence Requirements?

Next-Generation Fuel Specifications

Advanced nuclear reactor designs require specialised fuel formulations exceeding current commercial production capabilities. High-assay low-enriched uranium (HALEU) enriched to 5-20% U-235 enables compact reactor designs whilst maintaining proliferation-resistant characteristics.

HALEU Production Challenges:

Current U.S. HALEU production capability remains minimal, limited to small quantities from research reactor operations and historical stockpiles from downblended weapons material. Commercial-scale production requires specialised centrifuge configurations and enhanced security protocols.

Market projections indicate HALEU demand reaching 40-60 metric tons annually by 2030, expanding to 200-300 tons by 2040 as small modular reactors achieve commercial deployment. Current global production capacity totals less than 10 tons annually, creating substantial supply-demand imbalance.

Technical Production Requirements:

HALEU enrichment demands modified centrifuge cascades capable of achieving higher U-235 concentrations whilst maintaining cost competitiveness. Enhanced security measures protect against proliferation risks associated with weapons-usable enrichment levels.

Quality control specifications exceed current commercial standards, requiring advanced analytical capabilities and material certification programmes. Transportation protocols incorporate enhanced physical security and specialised containers designed for higher-enriched materials.

Innovation and Technology Development

Advanced reactor deployment drives innovation across multiple fuel cycle technologies, creating opportunities for U.S. technology leadership whilst addressing proliferation concerns and waste management challenges.

Research and Development Priorities:

Accident-tolerant fuel development incorporates advanced cladding materials and fuel compositions designed to withstand severe accident conditions. Silicon carbide and other ceramic materials offer enhanced performance during loss-of-coolant accidents.

Thorium fuel cycles provide alternative resource pathways reducing uranium dependency whilst offering proliferation-resistant characteristics. Molten salt reactor technologies enable thorium utilisation though requiring different fuel cycle infrastructure.

Digital Monitoring and Control:

Advanced fuel performance monitoring utilises real-time sensors and data analytics to optimise reactor operations whilst extending fuel lifetime. Digital twin technology enables predictive maintenance and performance optimisation.

Machine learning applications improve fuel design and manufacturing processes whilst reducing quality control costs. Automated inspection systems enhance safety whilst reducing human exposure to radiation.

What Timeline and Milestones Define the Independence Pathway?

Short-Term Objectives (2025-2028)

Immediate priorities focus on establishing foundation infrastructure whilst maintaining existing reactor operations during the transition from Russian imports. Political sustainability requires demonstrable progress within current presidential term.

Critical Near-Term Milestones:

Russian import phase-out completion by 2028 eliminates approximately $400-500 million in annual uranium purchases whilst requiring alternative supply arrangements. Waiver authority provides flexibility for reactor operators facing supply constraints.

Mining capacity expansion targets 3-5 new ISR facilities achieving initial production by 2027-2028. Burke Hollow and Wyoming operations provide operational experience supporting subsequent facility development and regulatory approval processes.

Enrichment infrastructure groundbreaking on major facilities establishes momentum for comprehensive fuel cycle development. Site selection, regulatory approval, and construction initiation demonstrate political commitment to long-term objectives.

Workforce Development Programmes:

Technical training programmes target 10,000+ workers across mining, conversion, and enrichment operations. Community college partnerships provide specialised education whilst university research programmes develop advanced technologies.

Regulatory workforce expansion addresses licensing bottlenecks whilst maintaining safety standards. Nuclear Regulatory Commission staffing increases support accelerated facility approval processes without compromising oversight quality.

Medium-Term Goals (2029-2035)

Infrastructure maturation phase achieves substantial progress toward the U.S. nuclear fuel independence whilst establishing technological leadership in advanced fuel cycles. Market dynamics shift as domestic capability displaces imports.

Production Capability Targets:

Domestic uranium production reaches 15,000-20,000 tons U3O8 annually, covering 75-85% of reactor requirements through expanded ISR operations and potential conventional mining restart. Production costs achieve competitiveness with international suppliers.

Conversion capacity begins operations providing 30,000-40,000 tons annual UF6 production capability. Technology transfer from allied partners accelerates facility development whilst maintaining operational independence.

HALEU Production Scale-Up:

Commercial HALEU production achieves 50-75 tons annual capacity supporting initial small modular reactor deployment. Enhanced security infrastructure protects against proliferation risks whilst enabling commercial operations.

Advanced reactor demonstration projects validate fuel performance whilst establishing supply chain relationships. Technology export potential emerges as U.S. companies capture intellectual property advantages in next-generation nuclear systems.

Long-Term Vision (2036-2045)

Strategic independence achievement encompasses complete fuel cycle autonomy with surplus capacity for allied support and technology export. U.S. nuclear industry regains global leadership position across multiple technology segments.

Independence Metrics Achievement:

Complete supply chain autonomy provides 100% domestic capability across mining, conversion, enrichment, and fuel fabrication. Strategic reserves maintain 180-day emergency supplies whilst supporting market stability during disruptions.

Export market participation utilises surplus capacity supporting allied fuel security whilst generating revenue supporting continued infrastructure investment. Technology licensing creates additional revenue streams from intellectual property development.

Allied Cooperation Framework:

Regional supply security encompasses North American fuel cycle integration with Canadian uranium resources and Mexican reactor market development. European partnerships provide technology transfer whilst accessing larger uranium reserves.

Advanced reactor technology export supports global nuclear expansion whilst maintaining U.S. technological leadership. Fuel cycle services generate substantial export revenue whilst supporting international non-proliferation objectives.

How Do Environmental and Safety Considerations Shape Independence Strategies?

Sustainable Mining Practices

Environmental protection standards significantly influence uranium extraction methodologies and facility siting decisions. In-situ recovery technology offers substantial advantages over conventional mining approaches regarding surface disruption and long-term environmental impact.

ISR Environmental Advantages:

In-situ recovery operations minimise surface footprint whilst utilising natural geological containment for processing operations. Groundwater protection protocols ensure aquifer restoration to baseline conditions following resource extraction completion.

Wildlife habitat preservation maintains ecosystem integrity through minimal surface infrastructure requirements. Traditional mining operations require extensive surface facilities including waste rock storage and tailings management systems.

Regulatory Compliance Framework:

Nuclear Regulatory Commission oversight encompasses comprehensive safety standards including radiological protection, environmental monitoring, and emergency response capabilities. Licensing processes require detailed environmental impact assessments and community consultation programmes.

Environmental Protection Agency coordination ensures water and air quality protection whilst maintaining operational efficiency. State regulatory integration addresses local environmental concerns through cooperative oversight mechanisms.

Waste Management Integration

Comprehensive fuel cycle planning addresses waste streams throughout uranium processing, conversion, enrichment, and reactor operations. Integrated waste management strategies minimise environmental impact whilst optimising resource utilisation efficiency.

Fuel Cycle Waste Categories:

Mining waste includes processing solutions and low-level contaminated materials requiring controlled disposal in licensed facilities. ISR operations generate minimal solid waste compared to conventional mining approaches.

Conversion and enrichment operations produce depleted uranium requiring long-term storage pending potential future utilisation. Facility decommissioning creates additional waste streams demanding specialised handling and disposal protocols.

Long-Term Storage Solutions:

Interim storage facilities provide temporary accommodation for spent fuel pending recycling implementation or permanent disposal. Dry cask storage technology offers proven safety performance whilst maintaining retrievability for future processing.

Repository development for high-level waste disposal continues through Yucca Mountain licensing whilst exploring alternative sites and disposal technologies. International cooperation provides technical expertise whilst sharing disposal costs among allied nations.

The path toward the U.S. nuclear fuel independence represents a comprehensive transformation spanning multiple decades and requiring sustained political commitment across changing administrations. Success depends on coordinated investment, technological innovation, and international cooperation whilst maintaining environmental protection and safety standards. As global nuclear energy experiences renewed growth, establishing domestic fuel cycle capability becomes increasingly critical for energy security, economic competitiveness, and strategic autonomy.

The nuclear industry faces significant challenges in developing comprehensive fuel cycle infrastructure, whilst recent developments suggest renewed government commitment to achieving independence goals. Furthermore, the transition requires balancing immediate supply security needs with long-term strategic objectives, ensuring reactor operations continue without interruption during infrastructure development phases.

This analysis incorporates data from multiple government sources, industry reports, and technical assessments. Readers should verify current market conditions and policy developments when making investment or business decisions related to nuclear fuel markets.

Looking to capitalise on the uranium boom?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant uranium discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, then begin your 14-day free trial today to position yourself ahead of the market.