July 24, 2026

Strategic nuclear fuel independence represents one of the most fundamental shifts in global energy security dynamics since the establishment of international uranium markets. The nuclear fuel cycle operates through multiple interdependent stages, with enrichment facilities serving as critical bottlenecks that determine whether extracted uranium can transform into reactor-ready fuel. Understanding these supply chain dynamics becomes essential for investors and policymakers navigating an energy landscape where geopolitical tensions increasingly influence resource allocation decisions. Furthermore, the recent Russian uranium import ban impact has accelerated the need for uranium enrichment infrastructure investment across Western allied nations.

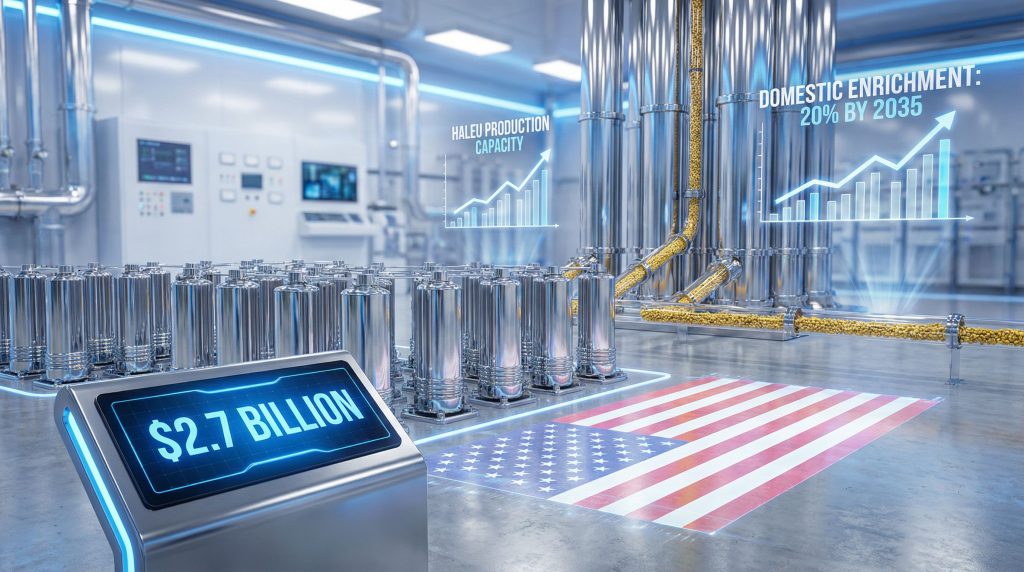

Understanding America's $2.7 Billion Nuclear Infrastructure Transformation

Nuclear fuel supply chains require sophisticated midstream processing capabilities that convert raw uranium ore into enriched fuel suitable for power generation. The United States Department of Energy allocated $2.7 billion across specialised enrichment infrastructure projects, fundamentally restructuring how Western nations access nuclear fuel supplies.

American Centrifuge Operating, operating as a Centrus Energy subsidiary, secured $900 million specifically for High-Assay Low-Enriched Uranium (HALEU) production development. This advanced fuel type contains uranium-235 enriched between 5% and 20%, compared to conventional reactor fuel enriched at 3-5% levels. HALEU enables next-generation Small Modular Reactors that cannot operate using standard fuel compositions.

General Matter, backed by technology entrepreneur Peter Thiel, received $900 million for advanced enrichment technology development. This investment targets innovative processing methodologies that could revolutionise uranium enrichment efficiency and reduce operational costs compared to traditional centrifuge systems.

Orano Federal Services obtained $900 million for expanding low-enriched uranium production capacity. This funding addresses conventional reactor fuel requirements for America's existing nuclear fleet while establishing redundant supply sources independent of foreign enrichment services. Additionally, comprehensive energy security strategies have become paramount in reducing reliance on potentially adversarial suppliers.

Global Laser Enrichment, partially owned by Canadian uranium company Cameco, received $28 million for next-generation laser isotope separation technology advancement. This represents cutting-edge enrichment methodology with potential efficiency advantages over centrifuge-based systems.

Investment Timeline and Implementation Strategy:

- 2026-2027: Infrastructure construction initiation and regulatory approval processes

- 2028-2029: Initial production capacity deployment and testing phases

- 2030: Target achievement of full domestic enrichment capability

- 2035: Projected 20% share of global enrichment capacity

The compressed development timeline reflects strategic urgency surrounding supply chain independence objectives. Traditional nuclear facility construction typically requires longer development periods, suggesting accelerated regulatory pathways and streamlined approval processes for these critical infrastructure projects.

When big ASX news breaks, our subscribers know first

The Strategic Importance of Uranium Enrichment Infrastructure Investment

Uranium enrichment represents the critical transformation point where extracted ore becomes usable nuclear fuel. Without enrichment facilities, mined uranium remains economically valueless for power generation purposes, creating fundamental supply chain constraints that have historically limited Western nuclear energy expansion capabilities.

Russia currently controls approximately 40% of global uranium enrichment capacity, establishing dominant market positioning that creates strategic vulnerabilities for Western energy security. China operates 15% of worldwide enrichment facilities, while the European Union maintains 25% through the Urenco consortium. Prior to this infrastructure investment, the United States lacked significant domestic enrichment capabilities and relied extensively on foreign processing services.

Current Global Enrichment Market Structure:

| Provider | Market Share | Technology Focus | Strategic Orientation |

|---|---|---|---|

| Russia (Rosatom) | 40% | Advanced centrifuge systems | State-backed expansion |

| European Union (Urenco) | 25% | Gas centrifuge technology | Commercial partnerships |

| China (CNNC) | 15% | Domestic capacity focus | Belt and Road integration |

| United States | Target: 20% by 2035 | HALEU specialisation | Allied cooperation framework |

The enrichment process involves converting uranium ore into uranium hexafluoride gas, processing it through sophisticated centrifuge or laser systems to concentrate uranium-235 isotopes, and reconverting enriched material into fuel assemblies suitable for reactor loading. Each processing stage requires specialised technical expertise, certified facilities, and rigorous quality control procedures that represent significant barriers to entry for new market participants.

HALEU Production Monopoly Concerns

Russia maintains virtual monopoly control over High-Assay Low-Enriched Uranium commercial production, creating critical supply dependencies for advanced reactor development programmes. Most next-generation Small Modular Reactor designs cannot operate using conventional fuel and require HALEU for safe, efficient operation. This monopoly positioning has effectively constrained Western advanced reactor deployment timelines and limited strategic energy independence options.

Secretary of Energy Chris Wright emphasised that the awards demonstrate administration commitment to "restoring secure domestic nuclear fuel supply chains capable of producing nuclear fuels needed to power current reactors and advanced reactors of tomorrow." This positioning establishes enrichment infrastructure as foundational national security infrastructure rather than commercial energy development.

Supply Chain Integration Benefits:

Domestic enrichment capability creates guaranteed local customers for American and allied uranium mining operations. Companies like Cameco and Energy Fuels gain access to committed processing services, enabling integrated supply chain planning and reduced market volatility exposure. This structural change transforms uranium mining from commodity price dependency to contractual relationship stability.

The establishment provides 10-year contract frameworks that deliver long-term price signals, reducing capital allocation uncertainty for mining project development. Junior mining companies benefit from enhanced financing opportunities when government investment supports downstream infrastructure that creates assured demand for their extracted products. Moreover, understanding uranium market volatility becomes crucial for strategic investment decisions.

Market Transformation Scenarios and Strategic Implications

Nuclear fuel market restructuring could follow multiple development pathways depending on implementation success, geopolitical developments, and technological advancement rates. Each scenario presents distinct investment opportunities and risk profiles for market participants across the uranium supply chain.

Scenario 1: Rapid Market Rebalancing (2026-2030)

Successful infrastructure deployment within projected timelines creates immediate market rebalancing effects. Russian enrichment market share declines from current 40% dominance toward 25% as Western alternatives become operational. Uranium spot prices stabilise within $75-95 per pound ranges as supply security reduces price volatility premiums.

Advanced reactor deployment accelerates significantly once HALEU supply constraints are eliminated. Small Modular Reactor commercialisation timelines compress from current decade-plus projections toward 5-7 year development cycles. This acceleration creates substantial uranium demand increases that benefit mining operations across Western allied nations.

Western mining companies secure long-term supply contracts with domestic enrichment facilities, providing revenue certainty that enables major capital expenditure programmes for mine expansion and new project development. Investment capital flows toward uranium extraction operations increase substantially as downstream processing guarantees reduce market risk perceptions.

Scenario 2: Gradual Transition with Supply Disruptions (2026-2032)

Technical delays in enrichment facility construction extend full implementation timelines toward 2032. Skilled workforce shortages in nuclear engineering disciplines create bottlenecks that slow facility commissioning and operational ramp-up phases. Regulatory approval processes for advanced enrichment technologies require additional safety assessments and environmental compliance reviews.

Geopolitical tensions affecting international uranium trade create periodic supply disruptions that generate price volatility spikes. Emergency uranium stockpile releases provide temporary market stability during transition periods, while enhanced reliance on allied enrichment facilities maintains fuel supply continuity for existing reactor operations.

Strategic Response Mechanisms:

- Accelerated nuclear technician training programmes address workforce constraints

- Temporary processing agreements with Canadian and European facilities provide interim capacity

- Enhanced physical security protocols protect domestic enrichment infrastructure

- Strategic petroleum reserve-style uranium stockpiles buffer supply disruption impacts

Scenario 3: Competitive Global Restructuring (2026-2035)

Multiple Western nations develop domestic enrichment capabilities following American infrastructure development success. Technology transfer agreements between NATO allies create standardised enrichment systems that enable interoperability and shared technical expertise. Regional nuclear fuel trading blocs emerge with processing capacity sharing arrangements.

Advanced reactor standardisation across Western alliance countries reduces fuel specification complexity and enables economies of scale in HALEU production. Export opportunities for American enrichment services develop as allied nations require advanced fuel supplies for their Small Modular Reactor deployment programmes.

This scenario creates the most favourable outcomes for American uranium enrichment infrastructure investment, establishing long-term competitive positioning in global nuclear fuel markets while reducing strategic dependencies on potentially adversarial suppliers.

Investment Impact Analysis and Market Winners

Infrastructure development creates multiple beneficiary categories across the nuclear fuel supply chain, from direct service providers to upstream mining operations and supporting technology companies. Understanding these impact patterns enables strategic investment positioning for both immediate opportunities and long-term market evolution.

Primary Infrastructure Beneficiaries

American Centrifuge Operating gains first-mover advantages in HALEU production, positioning Centrus Energy as a leading supplier for advanced reactor fuel requirements. The $900 million investment provides substantial competitive moats against potential new entrants and establishes technical expertise that extends beyond domestic markets toward export opportunities.

General Matter's $900 million technology development funding positions Peter Thiel's investment group at the forefront of next-generation enrichment innovation. Advanced processing technologies could revolutionise industry cost structures and efficiency metrics, creating intellectual property assets with global licensing potential.

Orano Federal Services expands conventional fuel production capacity that serves America's existing nuclear fleet while building operational expertise for potential international expansion. The $900 million investment strengthens market positioning for long-term utility service contracts and government fuel supply agreements.

Upstream Mining Sector Benefits

Domestic uranium mining operations gain guaranteed customer access through long-term processing contracts that eliminate previous supply chain bottlenecks. Companies operating American extraction facilities benefit from reduced transportation costs, simplified regulatory oversight, and enhanced security protocols for nuclear material handling. In fact, US uranium production insights reveal significant opportunities for domestic mining companies.

Key Mining Company Positioning:

- Cameco: Maintains dual exposure through uranium mining operations and Global Laser Enrichment technology investment

- Energy Fuels: Benefits from guaranteed domestic processing access for American-extracted uranium

- Paladin Resources: Continues operating the Langer Heinrich Mine in Namibia as major independent uranium producer serving global markets

Project financing opportunities improve substantially for junior mining companies when downstream processing infrastructure provides assured demand signals. Capital markets demonstrate increased willingness to fund uranium exploration and development projects when government investment reduces midstream processing risks.

Technology and Engineering Sector Opportunities

Centrifuge technology development contracts create opportunities for specialised engineering firms with nuclear industry experience. Facility construction and maintenance agreements provide multi-year revenue streams for companies capable of meeting stringent nuclear facility requirements.

Advanced materials research receives increased funding for uranium hexafluoride handling systems, specialised centrifuge components, and radiation-resistant facility construction materials. Cybersecurity and operational technology integration projects become critical for protecting enrichment infrastructure from potential foreign interference.

Regional Economic Development Impacts

High-skilled job creation in rural communities hosting enrichment facilities provides substantial local economic benefits. Nuclear engineering positions typically offer wages significantly above regional averages and require extensive training programmes that benefit local educational institutions.

Infrastructure development supporting enrichment facilities includes specialised transportation systems, enhanced electrical grid capacity, and emergency response capabilities that benefit multiple local industries beyond nuclear operations.

Global Supply Chain Reconfiguration and Strategic Alliances

American uranium enrichment infrastructure investment catalyses broader Western alliance coordination for nuclear fuel supply chain independence. This reconfiguration extends beyond bilateral arrangements toward multilateral frameworks that enhance collective energy security while reducing dependencies on potentially adversarial suppliers.

Western Nuclear Fuel Alliance Development

Canada-US coordination integrates uranium mining operations with enrichment processing through streamlined regulatory frameworks and joint infrastructure planning. Australian uranium export partnerships expand to include long-term supply contracts specifically designed to support domestic American enrichment capacity requirements.

European Union technology sharing agreements enable advanced centrifuge and laser enrichment expertise transfer while maintaining competitive positioning for European companies. Japan-US collaboration focuses on advanced reactor fuel development that requires specialised HALEU compositions not available through conventional enrichment processes.

Shifting Global Trade Relationships

Russian enrichment services face systematic exclusion from Western markets as import restriction legislation takes effect by 2028. This creates substantial supply gaps that domestic American capacity explicitly targets for replacement, fundamentally altering global market dynamics and pricing structures.

Kazakhstan uranium exports require redirection toward Asian markets as Western enrichment independence reduces demand for raw uranium requiring foreign processing. African uranium producers must identify new processing partnerships to access Western reactor fuel markets previously served through Russian enrichment services.

Central Asian uranium-producing nations face strategic decisions regarding domestic enrichment capability development versus continued reliance on Russian processing services for their extracted uranium resources.

Transportation and Logistics Optimisation

Domestic supply chain advantages include reduced shipping costs and delivery timeframes for uranium concentrate transportation from mining operations to enrichment facilities. Enhanced security protocols for nuclear material transport benefit from simplified oversight when materials remain within American regulatory jurisdiction throughout the supply chain.

Emergency response capabilities for supply disruptions improve significantly when enrichment facilities, transportation routes, and storage facilities operate under unified command and control structures. This integration reduces response times and coordination complexity during potential crisis situations.

Advanced Reactor Market Implications and HALEU Demand Projections

High-Assay Low-Enriched Uranium availability represents the critical enabler for Small Modular Reactor commercialisation and advanced reactor technology deployment. Current HALEU supply constraints have effectively limited Western advanced reactor development timelines, making uranium enrichment infrastructure investment essential for next-generation nuclear technology advancement.

Small Modular Reactor Market Development

Over 50 SMR projects are planned across North America by 2035, requiring specialised fuel compositions unavailable through conventional enrichment processes. Industrial applications requiring specialised HALEU formulations include high-temperature process heat, hydrogen production, and remote community power generation where traditional reactor designs prove impractical.

Military applications for compact reactor systems require HALEU fuel with extended operational cycles and enhanced safety characteristics. These defence-related requirements create additional demand streams beyond commercial power generation applications.

HALEU Demand Growth Projections

| Year | Projected HALEU Demand (tonnes) | Primary Market Applications | Supply Security Level |

|---|---|---|---|

| 2028 | 15-20 | Demonstration reactor projects | Critical dependency |

| 2030 | 40-60 | Initial commercial SMR deployment | Transition phase |

| 2035 | 150-200 | Widespread SMR commercialisation | Supply independence |

| 2040 | 300-400 | Advanced reactor fleet maturity | Export capability |

Export market opportunities emerge as allied nations require HALEU supplies for their advanced reactor programmes. Canada, United Kingdom, and European Union countries pursuing SMR development create potential customer bases for American HALEU production beyond domestic requirements.

Technology standardisation across Western alliance SMR programmes enables economies of scale in HALEU production while reducing fuel specification complexity. This standardisation approach reduces per-unit production costs and improves supply chain efficiency compared to custom fuel requirements for individual reactor designs. Furthermore, the World Nuclear Association's comprehensive guide to uranium enrichment provides essential technical understanding for investors evaluating this sector.

The next major ASX story will hit our subscribers first

Risk Assessment and Mitigation Framework

Uranium enrichment infrastructure development faces multiple risk categories that require comprehensive mitigation strategies for successful implementation. Technical, regulatory, market, and geopolitical risk factors could significantly impact project timelines, costs, and ultimate success metrics.

Technical Implementation Risks

Centrifuge reliability and maintenance requirements present ongoing operational challenges that affect facility availability and production consistency. Uranium hexafluoride handling requires specialised safety protocols and environmental compliance systems that add complexity and operational costs to enrichment processes.

Quality control for reactor-grade fuel specifications demands precise technical standards that must meet Nuclear Regulatory Commission requirements and international safety protocols. Equipment failure scenarios could disrupt production schedules and affect long-term supply contract fulfilment obligations.

Mitigation Strategies for Technical Risks:

- International technology licensing agreements provide access to proven enrichment methodologies

- Comprehensive operator training programmes ensure skilled workforce availability

- Redundant safety systems and emergency procedures minimise operational disruption risks

- Regular third-party audits and quality assessments maintain compliance standards

Market and Financial Risk Factors

Nuclear plant retirement schedules could reduce conventional uranium demand and affect project economics if advanced reactor deployment lags behind projections. Competition from renewable energy sources might limit nuclear capacity expansion and reduce long-term fuel demand growth expectations.

Uranium price volatility affects upstream mining operations and could impact integrated supply chain economics if long-term contracts fail to provide adequate price stability mechanisms. Construction cost overruns represent significant financial risks for enrichment facility development projects.

Financial Protection Mechanisms:

Government loan guarantees reduce private investor risk exposure while enabling project financing at favourable interest rates. Long-term purchase agreements with utilities provide revenue certainty that supports debt service requirements and investor return expectations.

Strategic reserve accumulation during periods of excess production capacity provides market stability buffers and enables emergency supply response capabilities. Export market development creates alternative revenue streams that reduce dependence on domestic demand fluctuations.

Regulatory and Compliance Challenges

Nuclear Regulatory Commission oversight requires comprehensive environmental impact assessments, security clearance requirements for facility personnel, and regular inspection protocols that add operational complexity and compliance costs.

International Atomic Energy Agency safeguards agreements mandate monitoring and reporting requirements that ensure non-proliferation treaty compliance while adding administrative overhead to facility operations. Additionally, nuclear waste disposal safety considerations become increasingly important as enrichment activities expand.

Geopolitical Risk Considerations

Potential foreign interference with enrichment infrastructure represents national security concerns that require enhanced physical and cybersecurity protection measures. International trade disputes could affect uranium supply access and create material shortages for enrichment operations.

Allied nation policy changes regarding nuclear energy development could impact export market opportunities and reduce projected demand for American enrichment services. Economic sanctions affecting uranium trade could create supply disruption scenarios requiring emergency response protocols.

Future Market Projections and Strategic Investment Opportunities

Nuclear fuel market evolution extends beyond immediate infrastructure development toward comprehensive industry transformation that creates multiple investment categories and strategic positioning opportunities. Long-term market dynamics favour integrated supply chain control and advanced technology development across the uranium enrichment sector.

Infrastructure Investment Categories

Direct enrichment facility investment provides exposure to fundamental supply chain control while generating long-term contracted revenue streams. Uranium conversion and fuel fabrication capabilities represent complementary infrastructure that enhances supply chain integration and reduces external dependencies.

Transportation and storage infrastructure development becomes increasingly valuable as domestic nuclear fuel volumes expand. Specialised rail transportation systems, secure storage facilities, and handling equipment create essential supporting infrastructure with long asset lifecycles and stable revenue characteristics.

Research and development investment targets next-generation enrichment technologies that could revolutionise industry cost structures and efficiency metrics. Laser isotope separation, advanced centrifuge designs, and automated processing systems represent technological frontiers with substantial competitive advantage potential.

Indirect Market Opportunities

Specialised engineering and construction services for nuclear facility development require unique expertise and security clearances that create significant barriers to entry. Companies with proven nuclear construction capabilities benefit from limited competition and premium pricing for specialised services.

Nuclear-grade materials and components manufacturing serves growing demand for specialised equipment, radiation-resistant materials, and precision-engineered components required for enrichment facility operations. These manufacturing opportunities often involve long-term supply contracts with attractive margin structures.

Cybersecurity and operational technology solutions become increasingly critical as enrichment infrastructure faces potential foreign interference and sophisticated cyber threats. Companies specialising in nuclear facility security benefit from government contracts and ongoing service requirements.

Advanced Technology Development Investment

Laser enrichment technology development represents potentially transformative advancement with superior efficiency characteristics compared to traditional centrifuge systems. Early investment in laser enrichment intellectual property could provide substantial long-term competitive advantages as technology matures.

Artificial intelligence applications for enrichment process optimisation, predictive maintenance, and quality control systems create operational efficiency improvements and cost reduction opportunities. Companies developing AI solutions specifically for nuclear applications benefit from specialised market knowledge requirements.

Advanced materials research for centrifuge components, uranium hexafluoride handling systems, and radiation-resistant facility construction materials addresses critical technical requirements while building valuable intellectual property portfolios.

Export Market Development Strategies

Allied nation partnerships for enrichment technology transfer create revenue opportunities beyond domestic facility construction. Licensing agreements for proven American enrichment technologies provide ongoing royalty income while supporting Western alliance energy security objectives.

HALEU export services to countries developing Small Modular Reactor programmes represent high-value market opportunities with limited global competition. American enrichment facilities could serve as Western alliance fuel suppliers for advanced reactor deployment across multiple countries.

Technical consulting and facility management services for international enrichment projects leverage American expertise while generating service revenue streams independent of commodity price fluctuations in uranium markets. According to ProActive Investors, recent uranium enrichment commitments have significantly boosted investor confidence in the nuclear sector.

The $2.7 billion uranium enrichment infrastructure investment represents more than facility construction funding. This strategic initiative fundamentally restructures global nuclear fuel supply chains while positioning America as a leading supplier of advanced reactor fuels essential for next-generation nuclear technology deployment. Success metrics extend beyond domestic energy security toward comprehensive market leadership in the expanding global nuclear renaissance.

Looking for Opportunities in Australia's Dynamic Mining Sector?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across Australian markets, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 30-day free trial today and secure your market-leading advantage in the evolving energy transition landscape.