August 6, 2026

When Paper Markets Ignore Physical Reality: The Oil Futures Disconnect Explained

There is a concept in behavioural finance known as the "optimism bias" — the systematic tendency of market participants to assign lower probabilities to adverse outcomes than the underlying data actually supports. In commodity markets, this bias tends to be self-reinforcing: the more loudly official sources signal resolution, the more aggressively speculative traders discount the physical evidence building in the opposite direction. That tension is now playing out in real time across the global oil market, and the stakes could not be higher.

The critical question facing energy investors in mid-2026 is not whether the Hormuz supply shock is real. The physical crude market has already delivered an unambiguous verdict on that. The more important question is why oil futures remain complacent about the supply shock and what happens when the gap between paper market pricing and physical market reality finally collapses.

When big ASX news breaks, our subscribers know first

The Physical-Futures Divide: A Market Sending Two Different Signals Simultaneously

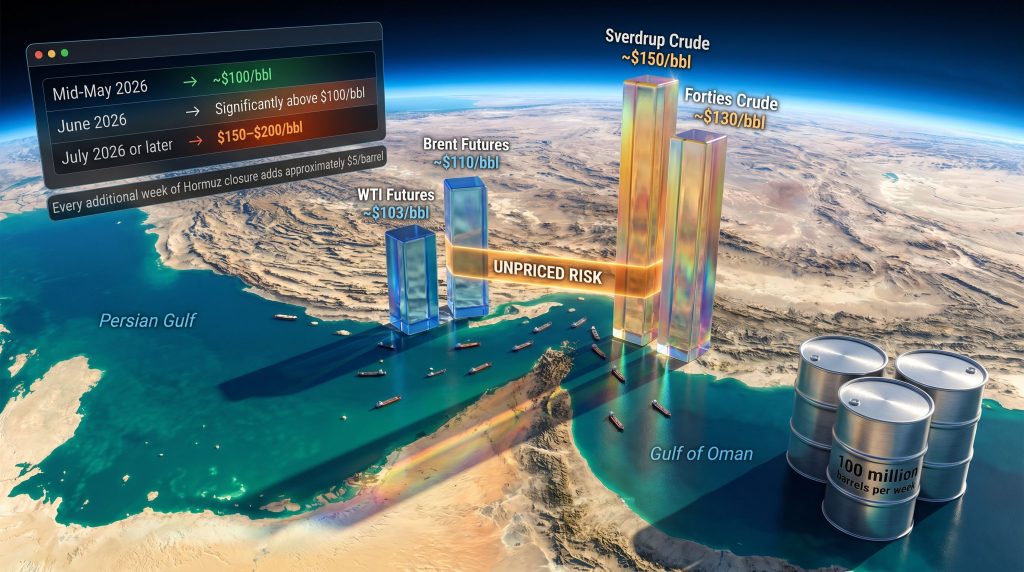

At the heart of the current oil market dysfunction lies an extraordinary pricing divergence between futures contracts and actual physical cargo transactions. Brent and WTI crude futures have risen meaningfully since the conflict began in late February 2026, but they remain dramatically cheaper than the real-world cost of securing a barrel of crude that does not require transit through the Strait of Hormuz.

The following table illustrates the scale of this divergence as of early May 2026:

| Crude Grade / Benchmark | Recent Physical Price | Futures-Equivalent Price | Estimated Premium |

|---|---|---|---|

| Forties Crude (NW Europe) | ~$130/bbl | ~$100–$110/bbl | ~$20–$30/bbl |

| Troll Crude (Norway) | ~$130/bbl | ~$100–$110/bbl | ~$20–$30/bbl |

| Sverdrup Crude (Norway) | ~$150/bbl (April) | ~$100–$110/bbl | ~$40–$50/bbl |

| Angola Cabinda | ~$130/bbl | ~$100–$110/bbl | ~$20–$30/bbl |

| Brent Futures (current) | — | ~$110/bbl | Baseline |

| WTI Futures (current) | — | ~$103/bbl | Baseline |

These are not marginal discrepancies. A $40–$50 per barrel premium for Norwegian Sverdrup crude represents a fundamental market signal: buyers with genuine delivery requirements are paying enormous sums to access supply that bypasses the Gulf entirely. The futures market, meanwhile, continues trading as though diplomatic resolution is imminent.

This condition is what commodity analysts describe as futures complacency — a state in which paper market pricing systematically lags physical market reality, creating conditions that historically precede sharp, disorderly repricing events.

The Behavioral Roots of the Disconnect

Understanding why oil futures complacent about supply shock conditions persist requires looking beyond supply-demand arithmetic and into the psychology of speculative market participants. Three cognitive biases are operating simultaneously:

-

Anchoring bias — speculative traders remain psychologically tethered to the pre-conflict Brent price range of roughly $70–$80 per barrel, treating any price significantly above that level as "already elevated" and therefore resistant to further upside.

-

Recency bias — the 2022–2024 period was characterised by relatively abundant supply and effective OPEC+ production management, creating a reference frame in which disruptions were temporary and self-correcting. Traders are applying that mental model to a structurally different situation.

-

Optimism heuristic — repeated signals from Washington suggesting imminent ceasefire agreements have created a persistent anchor point around resolution expectations, systematically suppressing futures price discovery. Helima Croft, Head of Global Commodity Strategy at RBC Capital Markets, noted in a late April 2026 strategy note that official messaging successfully capped front-month prices for approximately eight weeks by repeatedly implying the conflict was approaching resolution.

The result is a market in which physical participants — refiners, national oil companies, and end-users with genuine delivery obligations — are pricing crude at dramatically different levels than macro funds and algorithmic traders responding to geopolitical headlines.

"Physical crude markets are the true reflection of what is actually happening at and around the Strait of Hormuz, while futures pricing incorporates expectations, narrative, and hope in roughly equal measure to supply fundamentals." — Tamas Varga, PVM Oil Associates, as reported by Reuters, May 2026

The Strait of Hormuz: Why This Chokepoint Has No Practical Substitute

The Strait of Hormuz handles approximately 20–21% of total global oil trade — a figure that understates its true systemic importance. Unlike other chokepoints, the Strait has no credible alternative routing infrastructure capable of compensating for its closure at scale.

Since the conflict began in late February 2026, roughly 10–15% of global oil flows have been choked off, representing one of the most severe involuntary supply disruptions in the history of the modern oil market. Furthermore, the pre-conflict inventory buffer — built during a period when analysts were forecasting a 2026 oversupply — provided initial cushioning, but that buffer is now being consumed at a rate of approximately 100 million barrels per week, according to analysis from SEB Bank commodity strategists Bjarne Schieldrop and Ole R. Hvalbye.

Goldman Sachs has assessed that global oil inventories have fallen to their lowest level in eight years — a structural deterioration that makes the system increasingly brittle against any additional demand pressure. Analysts at OilPrice.com have warned that this degree of complacency in oil futures markets carries significant systemic risk.

Why Even a Full Reopening Would Not Quickly Normalise the Market

A critical and widely underappreciated dimension of this supply shock is the recovery timeline. Even in the scenario where the Strait of Hormuz reopened unconditionally today, the normalisation of supply flows would be neither immediate nor straightforward. The pathway to restored production would involve:

- Months required to restore normal shipping logistics and cargo scheduling through the Strait

- Additional months needed for Gulf producers to restart shut-in wells, with timelines depending heavily on reservoir pressure management during the extended shut-in period

- Up to five years to repair the physical damage inflicted on upstream oil production assets, downstream processing infrastructure, and LNG production and export facilities

This asymmetry between the speed of disruption and the speed of recovery is one of the most important factors the futures market appears to be systematically underweighting. Markets are pricing the resolution of the conflict; however, they are not adequately pricing the reconstruction of the supply chain that follows it.

The Inventory Depletion Clock and the Summer Demand Convergence

SEB Bank's scenario framework translates the weekly inventory draw rate into concrete price trajectories, providing one of the clearest quantitative frameworks available for assessing the range of outcomes:

| Reopening Scenario | Implied Rest-of-Year Brent Price | Market Characterisation |

|---|---|---|

| Mid-May 2026 | ~$100/bbl | Manageable — tight but functional |

| June 2026 | Significantly above $100/bbl | Uncomfortable territory |

| July 2026 or later | $150–$200/bbl range | Full-blown supply crisis |

| 8+ additional weeks of closure | $150–$200/bbl | Cumulative supply loss exceeds 1.5 billion barrels |

Source: SEB Bank commodity strategy, Bjarne Schieldrop and Ole R. Hvalbye, May 2026

The July scenario is particularly alarming because it does not simply imply a higher price — it implies a market in which consumption must physically contract to align with available supply. That is not a price spike; it is a structural rationing event.

Compounding this dynamic is the seasonal calendar. Peak summer demand is approaching precisely as inventories are hitting multi-year lows. The convergence of these two forces — accelerating demand and depleting supply buffers — is the central risk that speculative positioning in the futures market continues to discount. In addition, the trade war's impact on energy markets has further complicated the picture for traders attempting to model demand trajectories.

"According to SEB Bank's commodity analysts, each additional week of Hormuz closure beyond May 1 theoretically adds approximately $5 per barrel to the rest-of-year average Brent price, as global inventories draw at roughly 100 million barrels per week."

Strategic Petroleum Reserve releases coordinated through the IEA can provide partial and temporary relief, but the structural ceiling on this intervention is well understood: strategic reserves represent a bridging mechanism operable across roughly a 60–90 day drawdown window at maximum rates, not a substitute for sustained production capacity.

Why Global Supply Alternatives Cannot Close the Gap

A common but flawed assumption in current market commentary is that alternative producers can meaningfully compensate for Gulf supply losses. The arithmetic of replacement does not support this view:

| Potential Offset Source | Theoretical Capacity | Practical Limitation |

|---|---|---|

| U.S. Shale (Permian Basin) | ~500,000–800,000 bpd incremental | Infrastructure constraints and 6–12 month lead times |

| Russia | Partially constrained by sanctions and dark fleet capacity | Geopolitical ceiling on accessible markets |

| West Africa (Nigeria, Angola) | Limited spare capacity; already trading at premiums | Insufficient cargo volumes at scale |

| Canada (Trans Mountain pipeline) | ~590,000 bpd additional capacity | Pacific routing, not a direct Gulf replacement |

| IEA Strategic Reserves | 60–90 day drawdown window | Finite and non-renewable in the short term |

The logistical reality compounding the supply arithmetic is that non-Middle Eastern crude now travels longer routes, consuming additional shipping time and effectively reducing the real-world barrels available per unit of time. Japan and South Korea have been deepening bilateral oil procurement arrangements directly in response to Hormuz supply insecurity — a structural shift in Asian energy purchasing patterns that will have lasting consequences for regional pricing.

ADNOC has announced plans to double its Hormuz-bypass export pipeline capacity, but this expansion is not scheduled for completion until 2027 — providing no relief for the current crisis window. Furthermore, OPEC's influence on global supply coordination has been visibly weakened by the UAE's exit, signalling fracturing cohesion among Gulf producers at precisely the moment when a coordinated response would be most valuable.

The Macro Transmission Risk: From Energy Shock to Economic Crisis

The downstream economic consequences of a sustained oil shock above $100 per barrel are already becoming visible in real-world data. India's wholesale inflation reached a 3.5-year high as fuel costs surged by approximately 25%, prompting the government to raise fuel prices twice within a single week — an unprecedented pace of adjustment reflecting the acute pressure on downstream consumers.

U.S. consumers have absorbed an estimated $45 billion in higher energy costs since the conflict began, while the Middle East oil crisis has generated an estimated $25 billion in broader global business disruption costs. These are early-stage figures; the cumulative cost trajectory accelerates materially as the disruption extends.

The inflation transmission pathway follows a well-documented sequence:

- Crude oil prices rise at the wellhead level

- Refined product costs increase across gasoline, diesel, and jet fuel

- Transport and logistics costs increase throughout supply chains

- Consumer prices rise across goods categories with significant transport cost exposure

- Wage pressure builds as workers seek compensation for higher living costs

- Central banks face a choice between fighting inflation and supporting growth

This is precisely the dilemma now confronting the new Federal Reserve chair, who faces simultaneous pressure from oil-driven inflation and growth headwinds at a moment when monetary policy flexibility is already constrained. Consequently, gold's role as a safe-haven asset has grown considerably as investors seek protection from these compounding macro risks. PIMCO has observed that oil shocks become economically meaningful not at the moment of initial price spike, but when they persist — forcing central banks into exactly this kind of structurally difficult policy position.

The next major ASX story will hit our subscribers first

Three Scenarios: What a Repricing Event Would Actually Look Like

Scenario A — Diplomatic Resolution by June 2026

Brent converges toward the $95–$105 per barrel range, inventory rebuilding begins in Q3 2026, and the inflation impact, while elevated, remains manageable. Futures markets reprice in an orderly fashion as physical premiums compress.

Scenario B — Prolonged Stalemate Through July and August 2026

Brent moves toward $130–$150 per barrel. Demand destruction begins in price-sensitive Asian economies. Central banks in import-dependent nations are forced to hold rates higher for longer, and equity markets begin repricing growth expectations downward across sectors with significant energy cost exposure.

Scenario C — Full Crisis Escalation Into Q3 and Q4 2026

Brent tests the $150–$200 per barrel range. Cumulative supply losses exceed 1.5 billion barrels. Global consumption must involuntarily align with physical availability — a rationing scenario rather than a price discovery event. Stagflationary macro conditions emerge across import-dependent economies, with recession risk elevated in the most exposed markets.

The critical insight from this scenario framework is that Scenario C is not a tail risk to be discounted at low probability. It is the base case outcome if the Strait of Hormuz remains closed through July 2026 — and five days into May, the ceasefire was deteriorating rather than consolidating. For a broader view of where crude oil prices are heading amid this volatility, the structural forces at play extend well beyond the current conflict window. The Lowy Institute has also highlighted that complacency in oil markets could ignite a broader global crisis if left unaddressed.

Key Takeaways for Investors Navigating the Hormuz Supply Shock

The evidence from both physical crude markets and macroeconomic data points consistently in one direction. Investors and market participants should consider the following framework:

-

The futures market is pricing hope; the physical market is pricing reality. The gap between these two represents unpriced risk that has historically resolved through rapid, disorderly repricing.

-

Every additional week of Hormuz closure adds approximately $5 per barrel to the rest-of-year Brent average, according to SEB Bank's scenario modelling — a compounding dynamic with non-linear consequences as inventory buffers approach depletion.

-

Peak summer demand is arriving precisely as inventories hit multi-year lows. The convergence of these two forces is the central risk the futures market appears to be systematically discounting.

-

Recovery timelines are asymmetric and lengthy. Even a full resolution today would require months to normalise flows and potentially years to restore upstream production capacity damaged during the conflict.

-

The $150–$200 per barrel scenario is the base case, not a tail risk, if the disruption persists through July 2026, based on the inventory draw rate and the cumulative supply loss trajectory.

-

Three cognitive biases — anchoring, recency, and optimism — are measurable and systematic forces suppressing futures prices below their fundamental equilibrium. Recognising these biases is the first step to positioning ahead of the repricing event rather than being caught in it.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. All price scenarios, forecasts, and analyst assessments referenced herein involve inherent uncertainty and should not be relied upon as predictions of future market outcomes. Readers should conduct their own due diligence and consult qualified financial advisers before making any investment decisions.

Want to Stay Ahead of the Next Major Commodity Repricing Event?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity data into actionable investment insights — ensuring subscribers are positioned ahead of the broader market rather than reacting after the fact. Explore Discovery Alert's discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to secure a market-leading advantage.