May 14, 2026

The Strait That Moves Markets: Understanding the Oil Price Surge Behind Fragile US-Iran Diplomacy

Energy markets have always been sensitive barometers of geopolitical instability, but few supply chokepoints carry the concentrated risk of the Strait of Hormuz. This narrow passage between Iran and Oman has historically been the single most consequential waterway in global energy logistics, and right now it sits at the centre of one of the most complex diplomatic standoffs of the modern era. Understanding why oil prices rise on fragile US-Iran talks requires looking beyond the headlines and into the structural mechanics of how conflict, geography, and market psychology interact.

When big ASX news breaks, our subscribers know first

Why Geography Is the Real Wildcard in Global Oil Pricing

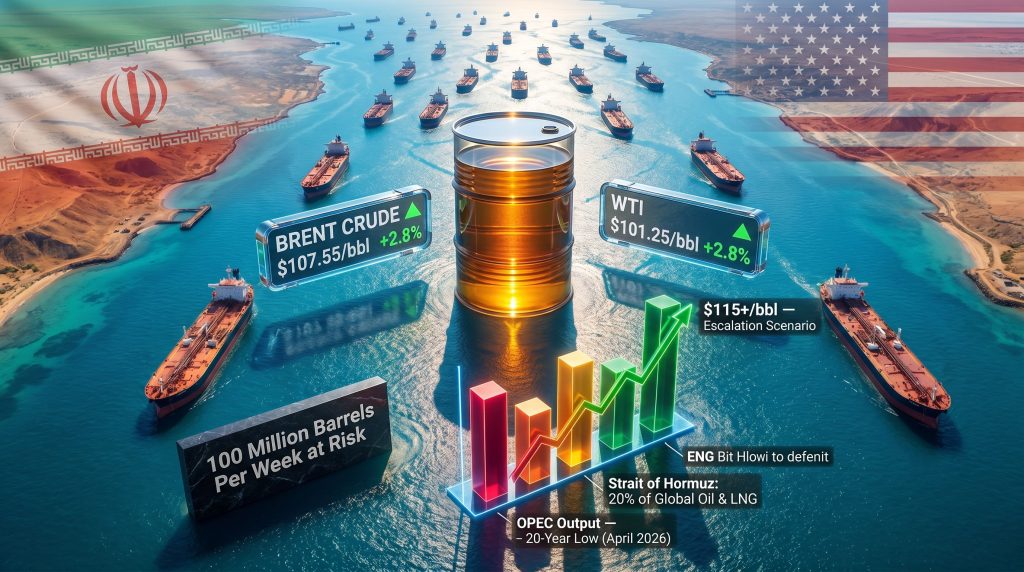

The Strait of Hormuz is not simply a strategic talking point. It is a physical constraint through which approximately one-fifth of the world's oil and liquefied natural gas passes annually, according to reporting by Arab News citing Reuters market data from May 12, 2026. No other single waterway concentrates that volume of energy trade in such a narrow corridor.

When access to this strait is threatened, the market consequences are not theoretical. Producers who rely on Strait transit cannot simply reroute shipments through alternative waterways without absorbing significant cost penalties and facing logistical delays measured in weeks, not days. The result is not merely a price spike driven by sentiment but a genuine physical constraint on export capacity that translates directly into supply shortfalls.

This is why the current diplomatic fragility between Washington and Tehran is generating sustained upward pressure on crude benchmarks, rather than the brief volatility spikes associated with ordinary geopolitical noise. The market is not reacting to rhetoric. It is repricing the probability that Iranian oil supply and Strait transit remain constrained for a structurally longer period than previously anticipated.

Where Crude Prices Stand and What the Numbers Signal

As of May 12, 2026, the crude oil price trends were registering the following levels, as reported by Arab News via Reuters:

| Benchmark | Price (May 12, 2026) | Daily Change | Monday Gain |

|---|---|---|---|

| Brent Crude Futures | $105.07/bbl | +$0.86 (+0.8%) | +2.8% |

| WTI (West Texas Intermediate) | $99.06/bbl | +$0.99 (+1.0%) | +2.8% |

| Brent (escalation scenario) | $115+/bbl | Conditional | Analyst target |

| Brent (peace deal scenario) | -$8 to -$12/bbl correction | Conditional | Analyst estimate |

Source: Arab News / Reuters, May 12, 2026. Analyst scenario targets from KCM Trade and DBS Bank commentary cited in the same report.

The back-to-back gains across Monday and Tuesday are significant in context. A cumulative move of approximately 3.6% over two trading sessions for both Brent and WTI signals that the market is not treating these diplomatic setbacks as temporary noise. Traders are repricing the risk premium upward in a sustained, deliberate fashion.

The Four Demands Preventing a Peace Agreement

The diplomatic stalemate between the United States and Iran is not reducible to a single disagreement. According to statements from President Donald Trump reported by Arab News on May 12, 2026, the ceasefire was characterised as being in a critically fragile state, with multiple unresolved demands preventing agreement:

- Full cessation of hostilities across all active fronts, not a partial or conditional pause

- Removal of the US naval blockade that is currently constraining Iranian maritime access to global trade routes

- Resumption of Iranian oil sales to international markets, including key buyers such as China

- War damage compensation, a demand that Washington has thus far shown no indication of accepting

Each of these demands represents a distinct category of negotiating friction. The compensation demand alone introduces a financial liability question that has historically derailed post-conflict negotiations for years. The blockade removal demand is not merely symbolic; it is the functional prerequisite for Iran to normalise crude exports. Tehran's explicit assertion of sovereignty over the Strait of Hormuz, furthermore, adds a legal and territorial dimension that extends far beyond the immediate military standoff.

The Strait of Hormuz functions simultaneously as Iran's most valuable negotiating asset and the global energy market's most acute vulnerability. As long as its status remains unresolved, a structural supply risk premium is baked into every barrel traded globally.

How Market Analysts Are Framing the Probability Scenarios

What Are the Three Key Market Pathways?

Professional energy market analysts are not simply watching diplomatic news and reacting. They are assigning probability weightings to distinct outcome scenarios and positioning accordingly. The current consensus, based on commentary published in the Arab News Reuters report of May 12, 2026, frames three distinct market pathways:

| Scenario | Trigger Condition | Expected Market Response |

|---|---|---|

| Genuine comprehensive peace deal | Full agreement signed before end of May 2026 | Sharp Brent correction of $8-$12/bbl |

| Prolonged stalemate / no deal by May end | Talks remain fragile without resolution | Upside price risks become structurally embedded |

| Military escalation / renewed blockade | Active confrontation resumes | Brent pushes above $115/bbl |

Source: KCM Trade chief market analyst Tim Waterer and DBS Bank energy sector team lead Suvro Sarkar, as cited in Arab News / Reuters, May 12, 2026.

Suvro Sarkar of DBS Bank identified end of May 2026 as a critical market threshold. If no deal materialises by that point, upside price risks cease to be temporary and become entrenched features of the pricing landscape. This timeline framing is important because it suggests that the market has a defined window within which diplomatic progress must occur before the repricing becomes self-reinforcing.

Tim Waterer of KCM Trade provided the specific price target framework. His analysis indicates that a genuine breakthrough could rapidly unwind the current geopolitical premium, delivering a sharp correction. Conversely, any escalation threatening renewed Strait disruption would rapidly push Brent toward and potentially beyond the $115 per barrel level. Monitoring the US-China oil price impact during this period adds yet another dimension to these projections.

OPEC's Historic Production Collapse: Confirming the Shock Is Real

One of the most significant data points in the current energy market narrative is not a price figure — it is a production figure. A Reuters survey of OPEC output for April 2026 revealed that production fell to its lowest level in more than two decades, as reported by Arab News on May 12, 2026.

This metric carries several important implications:

- Production curtailments are not voluntary policy decisions but physical consequences of being unable to access normal export channels through the Strait of Hormuz

- A 20-plus year production low suggests the intensity of this disruption has exceeded previous notable supply shocks, including the 2011 Libyan civil war and the production pressures of the early 2020s pandemic period

- Export curtailments cannot be reversed instantly even if a peace deal is reached, as supply chains, shipping logistics, and buyer contracts require time to restore

How Significant Is the 2027 Warning?

Saudi Aramco CEO Amin Nasser added the most sobering supply-side assessment to the current debate. According to Arab News reporting on May 12, 2026, Nasser warned that Strait of Hormuz disruptions could delay a return to market stability until 2027, with approximately 100 million barrels of oil per week at risk of being withheld from global markets.

To translate that volume into context: 100 million barrels per week equates to roughly 14.3 million barrels per day of potential supply disruption. Global oil demand currently runs in the range of 100 to 105 million barrels per day. A sustained withdrawal of 14 million barrels per day from accessible supply would represent one of the largest proportional disruptions in the history of modern oil markets.

Furthermore, OPEC's market influence during this period has been significantly constrained precisely because the disruption originates from physical access limitations rather than policy choices. Consequently, the usual levers for managing supply imbalances are less effective than under normal market conditions. Notably, OPEC demand forecasts issued earlier in 2025 did not anticipate a disruption of this scale or duration, underscoring how rapidly conditions have deteriorated.

A 20-year OPEC production low combined with a credible 2027 timeline for market normalisation represents a supply-side shock of a magnitude that most modern energy pricing models have rarely been stress-tested against.

The next major ASX story will hit our subscribers first

US Inventory Dynamics: A Domestic Layer Amplifying Global Pressure

While geopolitical risk dominates the price narrative, domestic US inventory data is quietly adding a second layer of upward pressure. According to a Reuters analyst poll cited in the Arab News report, US crude inventories were forecast to decline by approximately 1.7 million barrels in the week prior to May 12, 2026.

This drawdown is occurring against a backdrop of what Walt Chancellor, energy strategist at Macquarie Group, described as continued strong net waterborne export flows for both crude and refined products expected across the coming weeks.

The interaction between these two factors creates a reinforcing dynamic:

- Falling domestic stockpiles reduce the buffer available to absorb any additional supply disruptions from the Middle East

- Strong export flows indicate robust international demand for US crude, which further constrains domestic availability

- When inventory draws coincide with geopolitical supply risk, the dual pressure tends to be self-amplifying rather than offsetting

This is why oil prices rise on fragile US-Iran talks in a manner that proves more durable than some short-cycle geopolitical spikes. The structural demand backdrop is not soft. US production is meeting strong export demand while domestic inventories simultaneously decline, leaving no obvious domestic supply cushion to absorb a Middle East shock in the near term.

The China Dimension: Sanctions, the Xi Meeting, and a Third Risk Layer

Beyond the immediate Iran negotiations, a secondary geopolitical thread is introducing additional market complexity. Washington imposed sanctions on three individuals and nine companies identified as facilitating Iranian oil shipments to China, according to Arab News reporting from May 12, 2026.

This enforcement action adds a third layer to an already risk-elevated market:

- China has historically been a significant buyer of discounted Iranian crude, providing Tehran with a revenue stream that partially offsets the impact of Western sanctions

- If US pressure successfully curtails Chinese purchases of Iranian crude, Tehran loses a critical income source, potentially hardening its negotiating position and extending the conflict

- If China resists US pressure and continues purchasing Iranian oil, the sanctions signal a broader escalation in the economic dimensions of the standoff, which markets would interpret as an extension of the supply disruption timeline

President Trump's scheduled meeting with Chinese President Xi Jinping on Wednesday, May 13, 2026, was being closely monitored by market participants. According to CNBC, the outcome of that meeting could clarify whether sanctions enforcement represents a meaningful constraint on Iranian export revenues or whether Beijing will find ways to sustain its purchasing arrangements.

The Macro Consequences of Sustained Triple-Digit Crude

Oil prices in the $100 to $115 per barrel range do not stay confined to the energy sector. Their effects propagate through the broader economy in ways that complicate central bank policy, compress corporate margins, and disproportionately burden import-dependent nations.

Key macro channels through which sustained elevated crude prices transmit include:

- Inflation persistence: Higher oil prices feed directly into transportation costs, manufacturing inputs, agricultural production costs, and consumer energy bills, making central bank inflation targets harder to achieve

- Emerging market vulnerability: Nations that import the majority of their energy needs face acute balance-of-payments deterioration when crude remains at current levels, often forcing interest rate responses that compress domestic growth

- Corporate margin pressure: Energy-intensive sectors including aviation, shipping, petrochemicals, and logistics face structurally higher input costs that cannot always be passed through to consumers in competitive markets

- Energy transition acceleration: Sustained high fossil fuel prices historically accelerate capital allocation toward alternative energy infrastructure, though the lag between investment decisions and supply additions is typically measured in years rather than months

| Supply Shock Event | Peak Brent Level (Approx.) | Disruption Duration | Primary Driver |

|---|---|---|---|

| 1973 Arab Oil Embargo | Significant multi-year shock | ~12 months acute phase | OPEC production cuts |

| 1979 Iranian Revolution | Severe output collapse | ~24 months elevated | Iranian supply loss |

| 2022 Russia-Ukraine Conflict | ~$130/bbl | ~6 months | Sanctions and rerouting |

| 2026 US-Iran War (ongoing) | $105-$107/bbl | Ongoing | Strait of Hormuz disruption |

Note: Historical price comparisons are indicative and reflect approximate peak levels. Duration estimates reflect periods of materially elevated pricing, not full market normalisation.

What the End-of-May 2026 Window Really Means for Investors

For investors and market participants assessing crude positioning, the analyst consensus around the end of May 2026 diplomatic threshold deserves careful attention. This is not an arbitrary date. It represents the point at which oil prices rise on fragile US-Iran talks and the current geopolitical risk premium transitions from a temporary, resolution-contingent factor to a structurally embedded feature of oil valuations.

Key variables to monitor as that window approaches include:

- Whether any of the four core negotiating demands — cessation of hostilities, blockade removal, oil sales resumption, and compensation — show signs of movement toward compromise

- Whether the Trump-Xi meeting on May 13 produces clarity on Chinese compliance with Iranian oil sanctions

- Whether US crude inventory data continues to show drawdowns consistent with strong export demand

- Whether Saudi Aramco or other OPEC members provide updated production forecasts that revise the 2027 normalisation timeline in either direction

This article is intended for informational purposes only and does not constitute financial advice. Commodity market prices, diplomatic developments, and geopolitical scenarios can change rapidly. Readers should conduct their own due diligence before making any investment or trading decisions based on the information contained herein.

The current crude market is functioning less as a reflection of underlying supply-and-demand fundamentals and more as a real-time probability model for geopolitical resolution. As long as US-Iran talks remain fragile, OPEC production sits at multi-decade lows, and the Strait of Hormuz remains contested, crude benchmarks will continue pricing in a substantial risk premium. The market is not waiting for diplomats to reach a conclusion. It is continuously updating its assessment of how far away that conclusion is.

Want to Stay Ahead of Commodity Market Shifts Driven by Major Geopolitical Events?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across more than 30 commodities, instantly translating complex market data into actionable investment insights — no matter how volatile the broader energy landscape becomes. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the market.