May 12, 2026

The Strait of Hormuz at Breaking Point: What the Oil Price Surge Above $100 Really Signals

Every major oil price shock in modern history has shared a common thread: supply disruption at a chokepoint that the global economy assumed would remain open. The 1973 Arab oil embargo, the 1979 Iranian Revolution, and the 1990 Gulf War each exposed how profoundly dependent modern industrial civilisation is on the uninterrupted flow of crude through a small number of critical maritime passages. What is unfolding in 2026 around the Strait of Hormuz represents not merely a repetition of this historical pattern, but a qualitative escalation in its severity, duration, and geopolitical complexity.

Understanding why oil prices rise on US-Iran talks and Strait of Hormuz supply worries requires looking well beyond the daily price tick. The deeper architecture of global energy logistics, OPEC's market influence, and the competing strategic interests of the United States, Iran, China, and Gulf producers has created a supply shock with few modern precedents.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz: Why This 33-Kilometre Passage Controls Global Energy Security

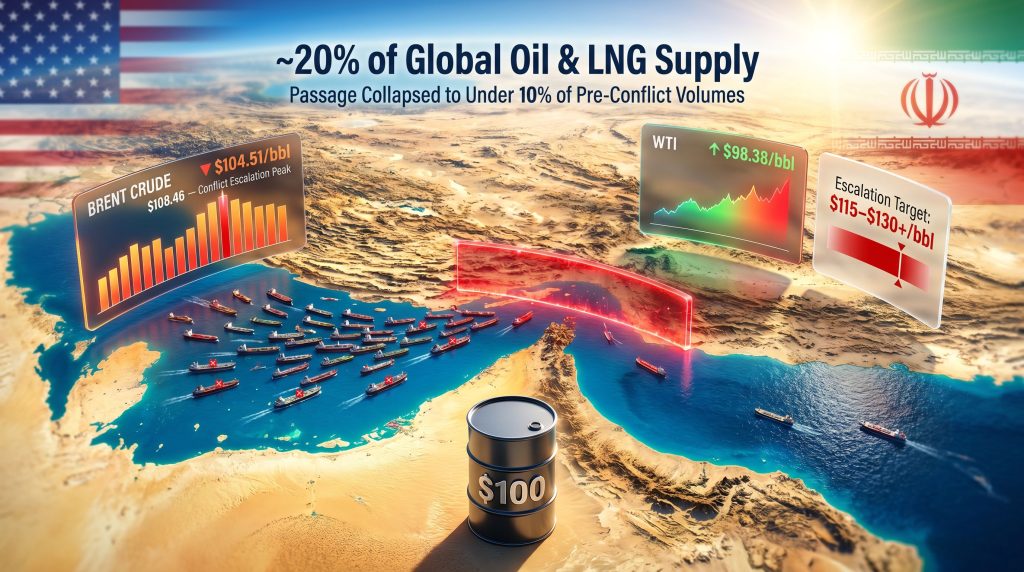

The Strait of Hormuz connects the Persian Gulf to the Gulf of Oman, forming a narrow maritime bottleneck through which approximately one fifth of the world's combined oil and liquefied natural gas supply transits on any given day. That single statistic understates the corridor's true strategic weight. At full pre-conflict throughput, the strait handled tens of millions of barrels of seaborne crude per day, along with enormous volumes of LNG destined primarily for Asian markets in Japan, South Korea, China, and India.

What makes this chokepoint categorically different from other points of supply vulnerability is its near-irreplaceability. Unlike a pipeline rupture that can often be bypassed through alternative infrastructure within days or weeks, a sustained maritime corridor disruption creates a structural rerouting problem that no single policy intervention can rapidly solve. Furthermore, the consequences for global LNG supply are particularly severe given the region's central role in liquefaction exports.

Why No Alternative Route Can Absorb the Volume

The options available to producers seeking to bypass the Strait are limited in both capacity and speed of deployment:

- The East-West Pipeline running across Saudi Arabia can carry crude toward the Red Sea, but its throughput capacity represents only a fraction of normal Hormuz volumes and was not designed to serve as a full replacement corridor

- Rerouting tankers around the Cape of Good Hope adds approximately two to three weeks of additional transit time per voyage, compressing refiner margins and increasing the effective cost of delivered crude regardless of the headline benchmark price

- Suez Canal transit offers a partial alternative for some Atlantic Basin flows but introduces its own bottleneck constraints and cannot serve the full range of Asian destination terminals

- LNG rerouting faces particularly acute constraints, as liquefied natural gas vessels operate under long-term offtake contracts tied to specific regasification terminals, meaning supply cannot simply be redirected without contractual and logistical consequences

"When the Strait of Hormuz is effectively closed or severely restricted, the global oil market does not simply adjust through price signals alone. It enters a structural supply deficit that no single policy lever can immediately resolve, and the duration of that deficit becomes the primary variable determining macroeconomic damage."

Three Compounding Factors Driving Oil Prices Above $100 Per Barrel

The current price environment above $100 per barrel for Brent crude is not the product of a single supply shock. It reflects the simultaneous compression of three distinct risk layers, each reinforcing the others.

Layer One: Active Conflict and Collapsed Diplomatic Architecture

The US-Iran military conflict, which escalated sharply from February 2026, has fundamentally repriced the geopolitical risk premium embedded in crude benchmarks. A conditional two-week ceasefire arranged through Pakistan-mediated negotiations collapsed without resolution, with both parties citing irreconcilable differences across multiple negotiating dimensions.

Iran's formal demands include the complete removal of the US naval blockade of its ports, full resumption of Iranian crude export flows, financial compensation for wartime infrastructure damage, and explicit recognition of Iranian sovereignty claims over navigation rights within the Strait of Hormuz. US President Donald Trump publicly described the ceasefire as being in critical condition, a characterisation that markets interpreted as confirmation that a near-term diplomatic resolution remains structurally distant rather than merely delayed.

Layer Two: Naval Escalation and Physical Flow Collapse

The imposition of a US Navy blockade of the Strait following the ceasefire breakdown triggered an immediate single-day price spike of more than 7%, with Brent briefly reaching $108.46 per barrel and WTI touching $96.85 during that session. According to Reuters reporting on the fragile US-Iran talks, as of May 12, 2026, Brent crude futures were trading at $104.51 per barrel, representing a gain of approximately 2.8% over the preceding session, while WTI stood at $98.38 per barrel with a comparable gain.

Ship-tracking data confirms that physical crude movements through the corridor remain severely curtailed, with producers forced to curtail export schedules rather than allow unsellable inventory to accumulate at loading terminals. The market is not pricing in a theoretical risk of disruption. It is pricing in a disruption that has already occurred and shows no imminent sign of resolution. In addition, the crude price volatility seen across recent sessions underscores just how reactive benchmarks have become to each diplomatic development.

Layer Three: OPEC Production at a 26-Year Low

A Reuters survey of OPEC production confirmed that collective cartel output in April 2026 fell to its lowest level in over two decades, driven directly by war-related export disruptions across member states whose crude must transit the Strait to reach global markets. Saudi Aramco's chief executive, Amin Nasser, warned that disruptions to oil export flows through the Strait may delay any meaningful return to market stability until 2027, with the estimated volume impact running at approximately 100 million barrels of oil per week in lost or curtailed export capacity.

| Benchmark | Price (May 12, 2026) | Session Gain | Prior Session Peak |

|---|---|---|---|

| Brent Crude Futures | $104.51/bbl | +2.8% | $108.46/bbl |

| WTI Crude Futures | $98.38/bbl | +2.8% | $96.85/bbl |

The SPR Release and Sanctions: Washington's Dual-Track Response

Faced with a sustained supply shock, the Trump administration activated two distinct policy instruments simultaneously, each carrying its own set of limitations and geopolitical signals.

The Strategic Petroleum Reserve Deployment

The administration authorised a loan of 53.3 million barrels from the US Strategic Petroleum Reserve as a market stabilisation measure. Ship-tracking data confirmed that the first SPR crude shipment is en route to Turkey, making it the first such delivery to a Mediterranean destination under this release programme.

The critical context that market participants must understand is the scale mismatch between the SPR release and the underlying supply deficit. At the estimated rate of approximately 100 million barrels of weekly disruption attributed to Hormuz export curtailments, the entire 53.3 million barrel SPR release represents less than a single week of lost throughput. This positions the release as a confidence signal and a short-duration pressure valve rather than a structural solution to the supply deficit.

Sanctions and the China Dimension

Washington simultaneously imposed fresh sanctions on three individuals and nine companies, including entities based in Hong Kong, the United Arab Emirates, and Oman, for allegedly facilitating Iranian crude shipments to China. The timing of these sanctions, occurring just days before a planned summit between President Trump and Chinese President Xi Jinping, introduces a significant diplomatic complexity that markets are beginning to price into broader risk assessments.

The United States is simultaneously seeking Chinese diplomatic leverage over Iran while targeting Chinese-linked entities involved in Iranian oil trade. This creates a structural tension in US foreign policy that complicates the diplomatic pathway toward Hormuz normalisation. Furthermore, The Star reports that Morgan Stanley described the oil market as being in a race against time on the Hormuz situation, highlighting the urgency being felt across financial institutions. Additionally, reporting from the Wall Street Journal indicated that the UAE conducted military strikes on Iranian infrastructure, including an early April attack targeting a refinery on Iran's Lavan Island, with the UAE not having publicly acknowledged those strikes at the time of reporting.

According to Tim Waterer, chief market analyst at KCM Trade, oil prices are expected to remain anchored above the $100 threshold for as long as Strait of Hormuz physical flows remain restricted and US-Iran negotiations remain unresolved. A credible diplomatic breakthrough could trigger a sharp downward correction of $8-12 per barrel, while any renewed escalation or blockade intensification would likely propel Brent toward $115 or higher.

Three Scenario Pathways for Oil Prices Through the Second Half of 2026

The trajectory of crude prices from this point is not linear. It branches across three structurally distinct scenarios, each with identifiable probability weightings and observable trigger conditions. Consequently, the oil price rally dynamics from earlier in 2025 now look comparatively modest against the scale of what is currently unfolding.

Scenario A: Diplomatic Breakthrough

A comprehensive peace framework encompassing blockade removal, Iranian export resumption, and nuclear oversight provisions would unlock rapid supply normalisation. Market analysis suggests an $8-12 per barrel immediate correction upon credible deal confirmation, with Brent potentially retracing toward the $88-95 range within 30-60 days. OPEC would likely respond with measured production increases to prevent an oversupply-driven price collapse from undermining member-state revenues.

The primary trigger to monitor is the outcome of the Trump-Xi summit and whether Chinese diplomatic influence can bridge the core negotiating gaps between Washington and Tehran.

Scenario B: Prolonged Stalemate (Base Case)

This scenario, assessed as the most probable outcome given current negotiating dynamics, involves continued talks without resolution and Strait flows remaining suppressed but not further restricted. Under these conditions:

- Brent holds in the $100-110 per barrel range through the third quarter of 2026

- US SPR releases and modest OPEC output adjustments provide marginal relief without resolving the underlying structural deficit

- Consumer-facing energy inflation intensifies in energy-importing economies, with upstream cost pressures beginning to flow through to broader goods and services pricing

- Saudi crude exports to China, already projected to reach record lows in June 2026 according to industry sources, continue to compress as exporters struggle to route volumes through alternative corridors

Scenario C: Escalation and Intensification

Renewed naval confrontations, Iranian attacks on Gulf energy infrastructure, or a formal expansion of the blockade to additional shipping lanes would propel Brent toward $115-130 or higher per barrel. However, this scenario carries the additional risk of triggering coordinated International Energy Agency reserve releases and accelerating demand destruction in price-sensitive emerging market economies. The broader trade war impact on oil markets would amplify these pressures significantly under such conditions.

| Scenario | Brent Range | Assessed Probability | Primary Resolution Trigger |

|---|---|---|---|

| A: Diplomatic Breakthrough | $88-96/bbl | Low to Moderate | Verified Hormuz reopening and nuclear framework |

| B: Prolonged Stalemate | $100-110/bbl | High (Base Case) | Sustained restricted flows, no escalation |

| C: Escalation Intensification | $115-130+/bbl | Moderate | Infrastructure attacks or blockade expansion |

The Aramco Paradox and OPEC's Internal Fractures

One of the less-examined dimensions of the current supply shock is the paradox it creates for Gulf energy producers. Saudi Aramco reported a 25% jump in first-quarter 2026 profit, beating analyst estimates, driven by elevated crude prices even as export volumes face Hormuz-related constraints. This revenue windfall at elevated price levels simultaneously complicates calls for emergency production increases, since pushing more volume into markets that cannot easily absorb it through restricted shipping lanes would simply accumulate unsellable inventory at loading terminals.

The OPEC architecture is also being tested in ways that extend beyond production discipline. Member states whose export routes run exclusively through the Strait face revenue shortfalls and export schedule curtailments that are reshaping their relative positions within the cartel. Members with alternative pipeline access or Atlantic Basin production exposure gain competitive advantage in the current environment, introducing new fault lines into OPEC's internal cohesion.

The next major ASX story will hit our subscribers first

What Commodity Market Participants Should Monitor

For those tracking the oil prices rise on US-Iran talks and Strait of Hormuz supply worries, the following indicators represent the most actionable signals for near-term price direction:

Near-Term Signals (0-30 Days)

- Strait of Hormuz vessel passage data from ship-tracking services: any measurable increase in tanker transits would signal de-escalation ahead of formal announcements

- Language shifts in official US-Iran diplomatic communiques, particularly any movement away from publicly declared positions on blockade removal and sovereignty

- Outcomes from the Trump-Xi summit, specifically whether China formally commits to active mediation on Iranian nuclear and export terms

- Additional SPR shipment authorisations beyond the Turkey delivery, which would indicate escalating supply concern at the policy level

Medium-Term Signals (30-90 Days)

- Any OPEC extraordinary session convocation, which would confirm that member-state revenue pressures are overriding existing production discipline frameworks

- IEA coordinated reserve release authorisation, signalling that the supply shock has reached systemic proportions requiring multilateral intervention

- Shifts in Iranian nuclear negotiating posture, which would materially alter the diplomatic trajectory and market risk premium

- Public acknowledgment or further escalation in UAE-Iran tensions following reported military strikes on Iranian territory

Frequently Asked Questions

Why Are Oil Prices Rising Above $100 Per Barrel in 2026?

Three compounding factors are driving the price surge: the ongoing US-Iran military conflict, severe restriction of shipping through the Strait of Hormuz, and OPEC production falling to a 26-year low as a direct consequence of export disruptions across member states reliant on that corridor.

What Would a US-Iran Peace Deal Mean for Crude Prices?

A credible and comprehensive agreement that included verified reopening of the Strait and resumption of Iranian crude exports could trigger an immediate price correction of $8-12 per barrel, potentially pulling Brent back toward the $88-96 range within 30-60 days of confirmation.

Can the US Strategic Petroleum Reserve Fix the Supply Shortage?

The 53.3 million barrel SPR release authorised by the Trump administration functions as a short-duration pressure valve rather than a structural solution. At estimated disruption volumes of approximately 100 million barrels per week in lost Hormuz throughput, the release represents less than one week of equivalent supply compensation.

Why Is OPEC Production at a 26-Year Low?

Member states relying on Strait of Hormuz export routes have been forced to curtail shipments due to the near-closure of the corridor. This has pushed collective OPEC output to its lowest level since the late 1990s, compounding the supply shock from reduced Iranian crude exports under the US naval blockade.

How High Could Prices Go If the Conflict Escalates?

Market analysis indicates that significant escalation — such as confirmed attacks on Gulf energy infrastructure or expansion of the naval blockade — could propel Brent crude toward $115-130 per barrel or above, potentially triggering coordinated international reserve releases and accelerating demand destruction across price-sensitive economies.

Disclaimer: This article contains forward-looking scenario analysis and market projections based on publicly reported information as of May 2026. Commodity price forecasts are inherently speculative and subject to rapid change based on geopolitical, macroeconomic, and supply chain developments. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research and consult qualified financial professionals before making investment decisions.

Want to Profit From the Next Major Commodity Discovery Before the Broader Market Catches On?

While geopolitical shocks like the Strait of Hormuz crisis reshape global energy markets, significant mineral discoveries on the ASX can deliver transformative returns entirely independent of oil price movements — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment those discoveries are announced, turning complex geological data into clear, actionable opportunities for investors at every experience level. Explore how historic ASX discoveries have generated exceptional returns on Discovery Alert's dedicated discoveries page, then begin your 14-day free trial to position yourself ahead of the market.