May 13, 2026

When a Strait Becomes a Siege: Understanding the Energy Crisis Reshaping Global Markets

Few concepts in geopolitics carry as much practical weight as the idea of a chokepoint. Unlike borders, armies, or sanctions, a physical bottleneck in maritime trade needs no diplomatic declaration to reshape the global economy. It simply closes, and within hours, the consequences ripple outward across continents. The world is now living through the most consequential test of this principle in modern history, as the oil prices Iran ceasefire Strait of Hormuz crisis enters its third month with no clear resolution in sight.

What began as a military confrontation has evolved into a slow-motion supply emergency, one that is simultaneously driving crude benchmarks above levels not seen in years, stoking inflation across advanced economies, and forcing central banks into increasingly uncomfortable positions. Understanding how this crisis works, what the data actually says, and where it might lead requires moving beyond the daily price ticker and examining the structural forces at play.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz: A 33-Kilometre Fault Line in Global Energy

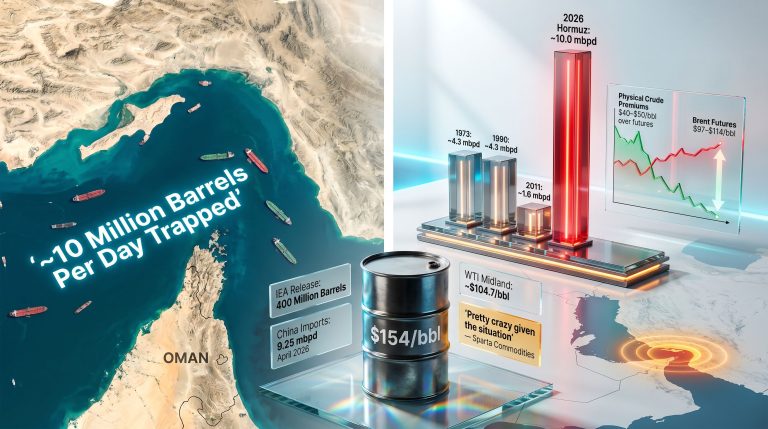

The Strait of Hormuz connects the Persian Gulf to the broader Arabian Sea, forming the only maritime exit route for the petroleum-rich nations that line the Gulf's shores. At its narrowest navigable point, the waterway spans roughly 33 kilometres, yet through this relatively modest corridor flows approximately one-fifth of the world's combined oil and liquefied natural gas supply on any given day, according to ETEnergyWorld (May 13, 2026).

The arithmetic of this dependency is striking. No other single piece of ocean real estate carries this much economic consequence. The Panama Canal, the Suez Canal, and the Malacca Strait each carry significant trade volumes, but none approach the petroleum concentration of the Hormuz corridor. When Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar export crude, it exits almost exclusively through this passage.

"The Strait of Hormuz is not merely a shipping lane. It is the physical mechanism through which global oil prices are set. When it closes, benchmark pricing decouples from demand fundamentals entirely and becomes hostage to the timeline of geopolitical resolution."

Historical precedent offers some guidance, though imperfect parallels. During the Tanker War of the 1980s, partial disruptions to Gulf shipping triggered regional price spikes as traders priced in supply uncertainty. What is occurring now, however, represents a qualitatively different scenario: not partial disruption, but effective closure sustained over months, affecting both crude oil and LNG flows simultaneously. Furthermore, the geopolitical oil price trends driving this crisis have been building for some time, making the current situation the culmination of longer-term tensions.

From Strikes to Standoff: The Timeline of the 2026 Conflict

The sequence of events that led to the current crisis unfolded rapidly. In late February 2026, US and Israeli forces conducted coordinated military strikes against Iranian targets. Tehran's response was swift and strategically calculated: the effective sealing of the Strait of Hormuz, cutting off the primary export artery for Gulf petroleum producers.

Since that point, both Brent crude and WTI have traded largely at or above the $100 per barrel threshold, a level that carries both economic and psychological significance for global markets. As of May 13, 2026, Brent crude futures were priced at $106.95 per barrel, while WTI stood at $101.52 per barrel, according to Reuters reporting on oil prices cited by ETEnergyWorld.

On Tuesday, May 12, prices had climbed more than 3% in a single session as investor confidence in a durable ceasefire weakened further, reducing the probability that Strait transit would resume in the near term. The following day saw a modest pullback of less than 1% as traders took profit ahead of diplomatic developments, illustrating just how sensitive crude prices have become to any signal, however incremental, about ceasefire progress.

The Ceasefire's Fragile Architecture

The ceasefire that briefly offered markets some relief has proven structurally unstable. President Donald Trump publicly characterised it as being on life support after Iran rejected a proposed peace framework as inadequate to its core interests. Direct naval exchanges between US and Iranian forces occurred as recently as early May 2026, underlining the gap between a nominal ceasefire and actual de-escalation.

The complexity of Iran's negotiating position adds another layer of difficulty. Tehran's strategic leverage rests on two interlocking pillars: physical control over Strait access and its nuclear programme as a diplomatic instrument. Any resolution framework that addresses only the military dimension while leaving the nuclear question unresolved is unlikely to produce durable Strait reopening, meaning the diplomatic challenge is significantly more complex than a conventional military ceasefire.

Quantifying the Supply Shock: What the Numbers Reveal

The scale of the supply disruption is without modern precedent. Eurasia Group, in analysis cited by Reuters and ETEnergyWorld, assessed that cumulative supply losses from the Strait closure had already exceeded 1 billion barrels as of mid-May 2026. That figure represents a supply removal from global markets that no strategic reserve drawdown programme can fully compensate for.

| Metric | Estimated Figure (May 2026) |

|---|---|

| Brent crude (May 13, 2026) | $106.95/barrel |

| WTI crude (May 13, 2026) | $101.52/barrel |

| Approximate price appreciation vs. pre-war baseline | ~52-53% |

| Cumulative supply loss since conflict began | Over 1 billion barrels |

| Duration of Strait closure (mid-May 2026) | 70+ days |

| US crude inventory drawdown streak | 4 consecutive weeks |

The pre-conflict baseline for Brent was approximately $70 per barrel, meaning the market has absorbed a price increase of roughly 52-53% from that starting point. At an inflation-adjusted level, prices above $100 per barrel carry significant economic weight, particularly for energy-import-dependent economies.

The US government has deployed releases from the Strategic Petroleum Reserve (SPR) in an attempt to moderate domestic supply tightness. However, given that cumulative Hormuz losses are estimated in the billions of barrels, reserve releases represent a partial buffer rather than a structural solution.

Why Inventory Data Has Become a Market Signal

One of the more technically important developments within the crisis has been the sustained pattern of US crude inventories drawing down. According to American Petroleum Institute data cited by ETEnergyWorld, US crude oil inventories fell for a fourth consecutive week as of mid-May 2026, with distillate stockpiles (including diesel and heating oil) also declining.

"Four consecutive weekly inventory drawdowns, occurring simultaneously with active SPR releases, indicate that physical demand is absorbing available supply faster than reserve programmes can compensate. This is a structurally bullish signal that supports a sustained price floor above $100 per barrel in the near term."

The US Energy Information Administration's official weekly figures were expected to confirm the same trend, consistent with Reuters poll forecasts. For market participants, consecutive inventory drawdowns function as a real-time referendum on the balance between physical supply and demand, providing a data anchor that sentiment-driven price moves eventually have to return to.

Three Scenarios for Oil Prices: What the Iran Ceasefire Resolution Could Mean

Eurasia Group's assessment that oil prices are likely to remain above $80 per barrel for the remainder of 2026 even with partial diplomatic progress establishes a credible price floor. However, the ceiling and trajectory from current levels depend heavily on how the following scenarios resolve.

Scenario 1: Durable Ceasefire and Strait Reopening

- Brent crude could retrace toward the $80-$85 per barrel range within 60-90 days of confirmed reopening

- Inventory rebuilding would require 3-6 months, maintaining prices above pre-war levels throughout the process

- Inflationary relief would be gradual rather than immediate, with fuel prices lagging crude benchmarks by several weeks

Scenario 2: Prolonged Stalemate (Current Trajectory)

- Prices remain anchored above $100 per barrel through Q3 2026

- Inflationary pressure intensifies across energy-importing economies

- Central banks face increasingly difficult trade-offs between rate policy and recession prevention

Scenario 3: Full Conflict Escalation

- Brent could approach the $130-$150 per barrel range in a worst-case military escalation scenario

- Global recession risk would increase materially, though demand destruction would eventually impose a natural ceiling on prices

- IEA coordinated emergency releases and coordinated allied SPR drawdowns would become the primary market stabilisation tools

The Inflation Transmission: From Oil Prices to Consumer Prices

Higher crude prices do not stay contained within oil markets. They transmit outward through the economy via transportation costs, manufacturing inputs, agricultural production, and retail energy pricing. This transmission mechanism is well understood by economists but often underestimated by consumers experiencing it in real time.

The data from April 2026 confirmed that this process is well underway. US consumer prices rose sharply for a second consecutive month, producing the largest annual inflation increase in nearly three years, according to ETEnergyWorld. That figure arrived at a particularly difficult moment, when the Federal Reserve was already navigating a complex post-pandemic policy environment.

Capital Economics summarised the broader picture in a client note cited by Reuters: while real consumer spending across advanced economies had not yet contracted in response to the price shock, meaningful deterioration in consumer sentiment and hiring intentions suggested that economic stress was accumulating beneath the surface numbers. Consequently, the market volatility reset playing out across financial assets reflects these deepening structural anxieties.

Federal Reserve Policy: Caught Between Inflation and Slowdown

The Federal Reserve now faces a dilemma that monetary policy tools are poorly suited to resolve. Market expectations have shifted decisively toward the Fed holding interest rates unchanged for an extended period, potentially through late 2026, as policymakers weigh the risks on both sides.

The structural problem is this: energy-driven inflation is fundamentally different from the demand-pull variety that interest rate policy is designed to suppress. The Fed cannot resolve an oil supply shock by raising borrowing costs. What rate hikes can do is reduce business investment, cool credit demand, and slow economic activity, creating secondary GDP drag at precisely the moment when households are already absorbing higher fuel and food costs.

"Energy-driven inflation creates a genuine monetary policy trap. Raising rates to fight energy-price inflation risks accelerating an economic slowdown caused by the same energy prices. Holding rates steady allows inflation to embed further into expectations. Neither path is clean, making this an unusually difficult environment for central bank communication."

The next major ASX story will hit our subscribers first

Regional Fallout: Who Pays the Highest Price?

The economic burden of sustained $100+ crude prices is distributed unevenly across the global economy. Nations with high oil import dependency, limited domestic production, and weaker fiscal buffers face disproportionate strain.

| Region | Primary Impact Channel | Key Indicator |

|---|---|---|

| United States | Fuel cost surge, consumer inflation | Gasoline prices rising sharply from pre-conflict baseline |

| India | High import dependency, current account pressure | Estimated daily losses of approximately $120 million |

| Global LNG importers | Spot price volatility, energy security exposure | ~20% of global LNG also transits Hormuz |

| European Union | Secondary supply tightness, transition policy pressure | Accelerated urgency for renewable energy deployment |

India's exposure warrants particular attention. As one of the world's largest oil importers, the country absorbs the full impact of both higher crude prices and the Hormuz disruption's effect on LNG availability. The daily economic cost to India's oil-dependent import economy has been estimated at roughly ₹1,000 crore (approximately $120 million) per day, a sustained drain on foreign exchange reserves and a complicating factor for the Reserve Bank of India's monetary management.

Within the United States, average gasoline prices have climbed sharply since the conflict began. The Trump administration has signalled openness to suspending the 18-cent federal gasoline tax as a consumer relief measure, though critics note that such a move addresses the symptom rather than the structural supply deficit. The fiscal cost of full suspension would run to approximately $500 million per week in foregone federal revenue. Several states, including Georgia, Indiana, and Utah, have already moved independently to suspend state-level fuel taxes.

Beijing's Role: Can the Trump-Xi Summit Shift the Calculus?

China occupies a uniquely complex position in this crisis. As the dominant buyer of Iranian crude oil, Beijing maintains deep commercial ties with Tehran that give it indirect influence over Iran's strategic calculus, an influence that no other external actor fully replicates.

President Trump stated publicly that he does not believe he needs China's assistance to resolve the Iran conflict, a characterisation that ETEnergyWorld (May 13, 2026) reported ahead of Trump's scheduled meeting with President Xi Jinping in Beijing. Whether this reflects a genuine negotiating stance or deliberate signalling designed to extract concessions from Beijing is a question analysts continue to debate.

The structural reality is more nuanced than Trump's public posture suggests. China has no formal security relationship with Iran and cannot compel Tehran's compliance through military or diplomatic command. Its leverage is economic and reputational: Beijing could signal to Tehran that continued Strait closure threatens Chinese commercial interests in ways that would complicate the bilateral relationship.

Even a constructive joint statement from the Trump-Xi summit calling for Strait reopening would carry significant market weight, potentially triggering a 3-5% downward correction in crude prices as geopolitical risk premiums partially unwound. Markets have become extraordinarily sensitive to diplomatic signals in this environment, meaning that even a modest positive development could produce outsized price responses. The broader oil price impact of US-China trade tensions adds yet another dimension to this already complex dynamic.

The Long-Term Structural Consequences for Energy Security

Beyond the immediate price dynamics, the oil prices Iran ceasefire Strait of Hormuz crisis is accelerating a structural reassessment of global energy security architecture. The vulnerability of concentrating so much of the world's petroleum trade through a single 33-kilometre passage has been understood theoretically for decades. The current crisis is converting that theoretical vulnerability into lived economic reality.

Policy and investment responses are likely to intensify across several fronts:

- Strategic reserve expansion across IEA member nations to improve buffer capacity against future supply shocks

- Alternative pipeline infrastructure development, including routes that bypass Gulf transit corridors

- Renewable energy and storage deployment as a long-term demand-side hedge against fossil fuel supply disruptions — indeed, renewable energy solutions are increasingly seen as a structural answer to the energy security challenge

- LNG terminal diversification to reduce Asian import dependency on Gulf-sourced liquefied natural gas

None of these responses will meaningfully affect the current crisis. Infrastructure takes years to develop, and strategic reserves are finite. However, the political and commercial momentum generated by this crisis is likely to outlast the conflict itself, reshaping energy investment priorities across the 2030s.

What Markets Will Watch in the Coming Weeks

For investors and market participants tracking the oil prices Iran ceasefire Strait of Hormuz situation, the following indicators carry the most forward-looking signal value:

- Ceasefire negotiation developments — any credible diplomatic breakthrough remains the single most powerful downward price catalyst available

- Weekly EIA inventory data — continued drawdowns will reinforce the $100+ price floor and validate the supply-tightness thesis

- Trump-Xi summit outcomes — diplomatic signals from Beijing could shift market risk premiums significantly in either direction

- Iranian naval activity in the Strait — any further direct military exchanges would likely push Brent toward the $110-$115 range

The Eurasia Group's projection that prices will remain above $80 per barrel through the end of 2026 even with partial diplomatic progress establishes the lower boundary of realistic expectations. The upper boundary remains defined by the pace of conflict escalation and the credibility of whatever ceasefire framework eventually emerges.

Furthermore, as CNBC's coverage of oil markets has highlighted, trader sentiment continues to swing on each new diplomatic development, reinforcing just how uncertain the path forward remains.

What is clear is that the Strait of Hormuz has proven once again that geography is not neutral. In a global economy built on the assumption of frictionless energy flows, a 33-kilometre waterway holds the power to reshape inflation, interest rate policy, regional economies, and geopolitical alignments simultaneously. The world is learning this lesson in real time, and at considerable cost.

This article draws on reporting from ETEnergyWorld (May 13, 2026), citing Reuters, Eurasia Group, and Capital Economics. Forward-looking price scenarios and economic projections represent analytical frameworks based on available data and should not be construed as investment advice. All forecasts involve significant uncertainty given the rapidly evolving geopolitical situation.

Want to Stay Ahead of the Next Major Resource Discovery Amid Market Volatility?

While geopolitical shocks like the Strait of Hormuz crisis reshape commodity markets overnight, Discovery Alert's proprietary Discovery IQ model continuously scans ASX announcements in real time, instantly identifying significant mineral discoveries and translating complex data into actionable investment insights — explore historic discovery returns on Discovery Alert's discoveries page and begin your 14-day free trial to secure a market-leading edge before the broader market catches on.