June 23, 2026

The Capital Architecture Problem at the Heart of Global Minerals Supply

The global mining industry is confronting a financing paradox that no single institution, government, or private equity house can resolve alone. The sheer volume of capital required to bring the next generation of critical minerals projects into production has outpaced every conventional funding mechanism available. Commercial banks have systematically retreated from pre-revenue project lending over the past decade, tightening credit conditions that already excluded most junior and mid-tier developers.

Meanwhile, sovereign balance sheets across the world's largest economies are stretched by post-pandemic debt loads, limiting the appetite for direct government investment in speculative mining ventures. The critical minerals demand surge in recent years has only deepened this mismatch between available capital and financing need.

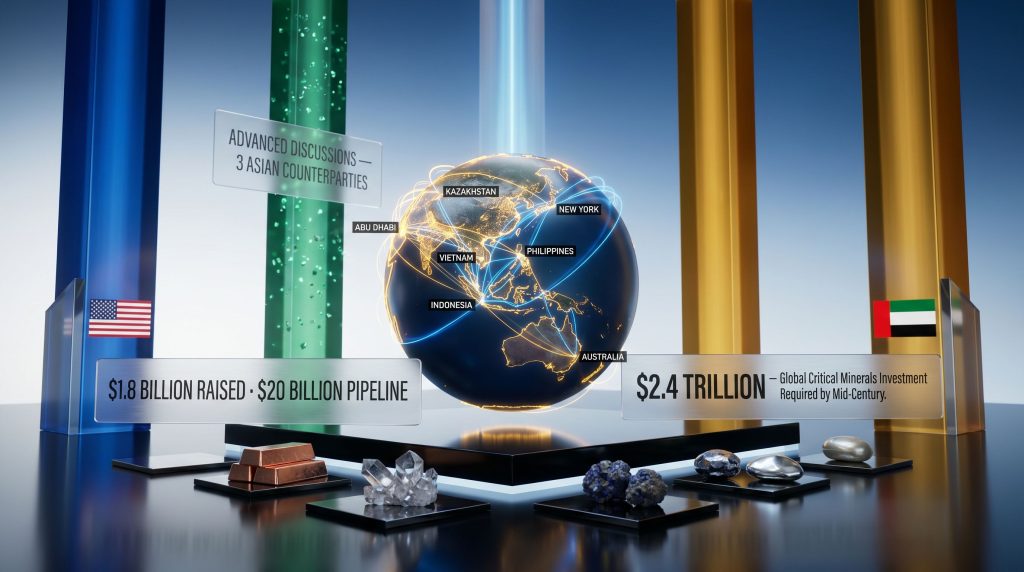

The arithmetic is sobering. Meeting projected demand for copper, lithium, rare earth elements, and battery metals through to mid-century will require an estimated $2.4 trillion in cumulative investment, with a minimum of $800 billion needed within the next 15 years simply to bring a sufficient pipeline of projects to production-ready status. Against this backdrop, blended public-private consortium models have emerged as the architecture most capable of mobilising capital at the required scale. Among the most ambitious of these structures is the Orion Critical Mineral Consortium, more commonly referred to as Orion CMC.

Understanding why Orion CMC is now pursuing Orion CMC Asian partnerships in critical minerals with such urgency requires stepping back from the deal-by-deal narrative and examining the structural logic of the consortium's three-pillar investment thesis.

When big ASX news breaks, our subscribers know first

How Orion CMC's Three-Pillar Framework Is Being Built

Orion CMC is a blended public-private investment vehicle led by Orion Resource Partners, a New York-headquartered mining-focused private equity firm. The consortium was designed from inception with a multi-regional capital structure intended to draw institutional money from three geographically and politically distinct sources. Understanding the role of resource capital in mining is essential context for appreciating why this structure was chosen.

The first two pillars are already operational. The U.S. leg is anchored by the U.S. International Development Finance Corporation (DFC), the American government's development finance arm, which co-invests alongside Orion Resource Partners' private equity capital. The Middle Eastern pillar is represented by ADQ, Abu Dhabi's sovereign wealth fund, which brings long-horizon mandate capital and Gulf institutional credibility to the consortium's dealmaking.

Together, these two pillars supported the $1.8 billion raised by Orion CMC in 2025, establishing the consortium as a credible and scaled alternative to Chinese state-backed investors in emerging market minerals jurisdictions.

| Capital Pillar | Partner | Type of Capital |

|---|---|---|

| U.S. institutional | DFC + Orion Resource Partners | Development finance + private equity |

| Middle Eastern sovereign | ADQ (Abu Dhabi) | Sovereign wealth, long-horizon mandate |

| Asian (target) | Sovereign funds, OEMs, agencies | Strategic co-investment (in negotiation) |

| Total raised (2025) | Combined | $1.8 billion |

| Pipeline target | Global | $20 billion |

The third pillar, targeting Asian institutional capital, remains the consortium's most urgent strategic priority as of mid-2026. Orion CMC is currently in advanced discussions with three separate Asian counterparties, spanning potential sovereign wealth fund partners, government development agencies, and original equipment manufacturers (OEMs) with direct downstream exposure to electric vehicles, energy storage systems, and defence electronics.

The significance of this expansion should not be understated. The consortium's previously stated investment target was $5 billion. The current pipeline ambition of $20 billion represents a fourfold scaling of that original scope, a figure that can only be credibly pursued with Asian institutional capital firmly embedded in the ownership structure.

Why Asian Institutional Capital Is Strategically Irreplaceable

Asian institutional investors are not simply an additional source of capital volume. They represent a qualitatively distinct category of co-investor that combines two characteristics rarely found together in Western financing markets: demand-side exposure to the very minerals being financed, and long-duration capital mandates that align with the 10-to-20-year development timelines typical of major mining projects.

Asian sovereign wealth funds and OEMs often have procurement exposure to the same commodities they would be financing, creating an alignment of incentive that purely financial investors cannot replicate.

OEM participation is particularly compelling from a supply chain architecture standpoint. Japanese, South Korean, and Taiwanese manufacturers of electric vehicles, consumer electronics, and industrial components represent potential anchor offtake partners as well as equity co-investors. Their involvement would transform Orion CMC Asian partnerships in critical minerals from a financing intermediary into a more vertically integrated supply chain vehicle, with capital providers and end-product manufacturers sharing exposure to upstream mineral production.

The complexity of closing these partnerships, however, is considerable. Asian institutional mandates frequently require domestic content frameworks, bilateral government-level coordination, and long internal approval cycles that extend well beyond the timelines typical in U.S. or Gulf institutional dealmaking. This structural friction explains why, despite being categorised as advanced-stage discussions, none of the three prospective Asian partnerships had been publicly confirmed as of June 2026.

Southeast Asia's Multi-Billion-Dollar Minerals Pipeline

Where Is the Regional Investment Concentrated?

The geographic focus of Orion CMC's Asian investment thesis maps closely onto the region's existing development-stage project pipeline. Southeast Asia, in particular, has emerged as one of the most active corridors for critical minerals project development globally.

John Dorian, a portfolio manager at Orion Resource Partners focused on Asian opportunities, has publicly identified the breadth of the regional opportunity set, noting the concentration of multi-billion-dollar projects across Indonesia, Vietnam, the Philippines, and Australia (Mining Weekly, June 2026).

| Country | Estimated Major Projects | Primary Commodities |

|---|---|---|

| Indonesia | ~5 major projects | Nickel, copper, cobalt |

| Vietnam | ~2 major projects | Rare earths, bauxite |

| Philippines | Several projects | Nickel, copper, chromite |

| Australia | Multiple projects | Lithium, copper, rare earths |

Indonesia's position at the top of this list reflects both the scale of its nickel endowment and the structural complexity of investing there. The country has progressively tightened its ore export restrictions since 2020, forcing international capital to engage with downstream processing investment rather than raw ore extraction. This policy environment creates challenges for purely extractive investment models, but also opportunities for consortium structures like Orion CMC that can offer development finance alongside downstream processing capital.

Vietnam's rare earth sector represents a less widely analysed opportunity within Western critical minerals strategy. The country holds some of the world's largest rare earth reserves, yet extraction and processing capacity remains dramatically underdeveloped relative to geological endowment. Furthermore, Western-aligned capital that can navigate Vietnam's complex foreign investment approvals and environmental permitting frameworks is in short supply, creating a potential first-mover advantage for early institutional entrants.

Central Asia: The Underappreciated Minerals Corridor

Why Kazakhstan and Uzbekistan Matter

Beyond Southeast Asia, Orion CMC's assessed opportunity universe extends into Central Asia, with Kazakhstan and Uzbekistan identified as priority markets. This geographic angle receives far less coverage in mainstream critical minerals discourse than African or South American jurisdictions, yet the fundamentals are compelling.

Kazakhstan holds world-class reserves of copper, uranium, and chromite, while Uzbekistan's gold and copper sectors have attracted growing institutional interest following the country's economic liberalisation programme over the past several years. Both nations are actively cultivating relationships with Western institutional investors as a strategic counterbalance to the historically dominant Russian and Chinese presence in their extractive sectors.

The geopolitical positioning of Central Asian nations as Western-aligned supply chain partners is an underappreciated dimension of the critical minerals investment thesis. For a consortium explicitly designed to compete with Chinese state-backed capital, Kazakhstan and Uzbekistan represent high-value relationship targets.

Consequently, the metals mining geopolitics of the region are shifting rapidly, making early-mover positioning increasingly valuable for Western-aligned capital.

The Mid-Tier Developer Thesis: Where Production Growth Actually Lives

One of the more distinctive and commercially important aspects of Orion CMC's strategy is its deliberate focus on mid-sized developers rather than major mining groups. This is not simply a market positioning choice; it reflects a substantive thesis about where the next wave of critical minerals production growth is most likely to originate.

The major diversified mining companies have systematically underinvested in exploration and greenfield development for well over a decade, prioritising shareholder returns through buybacks and dividends over capital-intensive project development. The result is a structural production gap that the majors are not positioned to fill quickly, regardless of commodity price incentive.

According to John Dorian of Orion Resource Partners, the development-stage and mid-tier cohort is where meaningful production growth is concentrated, precisely because this is the segment that the majors have vacated (Mining Weekly, June 2026). However, the evolving relationship between majors and juniors in copper does suggest that some collaborative structures are beginning to emerge across the sector.

This thesis carries important implications for how investors should think about the critical minerals supply chain:

- Mid-tier developers typically operate with higher geological risk but also higher potential upside relative to development capital deployed

- They are systematically underserved by major mining company M&A, meaning they cannot rely on strategic acquirer interest to validate project economics

- They require patient, specialised capital that understands pre-revenue project risk, which is precisely the niche that Orion CMC's blended structure is designed to fill

- Their long development timelines (often 7 to 15 years from discovery to first production) demand capital partners with mandates that extend well beyond typical private equity fund cycles

The next major ASX story will hit our subscribers first

Demand Drivers Compressing the Investment Timeline

Three distinct structural forces are accelerating the urgency of capital deployment into critical minerals development, each operating on a different part of the demand curve:

- Data centre and hyperscaler expansion is driving exponential growth in copper and rare earth demand, with large-scale AI infrastructure buildouts consuming extraordinary volumes of electrical cabling, cooling systems, and specialised metals

- Continued global urbanisation, particularly across South and Southeast Asia, is sustaining long-term base metals consumption at volumes that existing mine supply cannot satisfy without significant new project development

- Rearmament and munitions replenishment across NATO-aligned and allied nations is creating an accelerating new demand vector for critical minerals that was not a significant factor in pre-2022 supply modelling

The intersection of these three demand forces with the structural capital gap described above creates the fundamental investment case for consortium models like Orion CMC. In addition, the broader importance of critical minerals and energy security is increasingly recognised by governments and institutions worldwide, further reinforcing the urgency of securing new supply chains.

The Competitive Calculus: Orion CMC vs. Chinese Investment Models

Orion CMC explicitly positions itself as an alternative financing partner to Chinese investors and state-backed trading houses in emerging market mineral jurisdictions. This competitive framing is commercially important but also carries strategic complexity.

Chinese investment vehicles have historically moved faster, accepted lower returns, tolerated higher political risk, and offered host country financing packages that blend infrastructure development with resource access. Matching this model with Western institutional capital, which carries fiduciary return requirements and ESG compliance obligations, is genuinely difficult.

Where the Orion CMC model can differentiate itself is through:

- Blended public-private capital that can accept concessional returns on the DFC tranche, allowing the overall consortium to price competitively against Chinese state financing

- Western regulatory and ESG credibility, which is increasingly valued by host country governments seeking to diversify their financing relationships

- OEM co-investment, which provides downstream market access guarantees that pure financial investors cannot offer

- Multi-regional institutional backing, which signals long-term commitment beyond a single government's strategic priorities

A Continental Pipeline With Global Ambitions

Orion CMC's assessed investment universe spans multiple continents, reflecting its ambition to build a genuinely diversified Western-aligned critical minerals supply chain. The proposed acquisition of a strategic stake in Glencore's DRC assets is one high-profile example of the consortium's appetite for transformative, large-scale transactions.

| Region | Key Countries |

|---|---|

| Southeast Asia | Indonesia, Vietnam, Philippines |

| Central Asia | Kazakhstan, Uzbekistan |

| Australasia | Australia |

| Africa | DRC/Zambia Copper Belt, Morocco, Namibia, Mali |

| South America | Brazil, Argentina, Chile |

Successfully closing three Asian institutional partnerships would represent a pivotal inflection point for this global ambition. It would not only expand the capital base available to mid-tier developers across these regions, but also signal that Asian institutional investors are willing to anchor their minerals investment mandates to Western-aligned supply chain structures, rather than defaulting to Chinese-led vehicles.

That signal, if it materialises, would carry consequences well beyond Orion CMC's own portfolio. It would reshape the competitive financing landscape across the Global South at precisely the moment when the race to secure the next generation of Orion CMC Asian partnerships in critical minerals supply is intensifying most rapidly.

Disclaimer: This article contains forward-looking statements and references to projected investment figures, demand forecasts, and strategic timelines. These are subject to significant uncertainty and should not be construed as financial advice. Readers should conduct independent due diligence before making any investment decisions related to companies, projects, or sectors discussed herein.

Want to Spot the Next Major Critical Minerals Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across copper, lithium, rare earths, and more — instantly transforming complex mineral data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the next wave of critical minerals opportunity.