August 4, 2026

When Scarcity Is No Longer Enough: The Forces Reshaping Africa's Diamond Industry

For most of the twentieth century, the natural diamond market operated on a deceptively simple premise: control supply tightly enough, and prices will hold. That logic built fortunes, sustained African economies, and underpinned one of the most effective marketing narratives in consumer history. However, the architecture supporting that model is fracturing in ways that no amount of supply discipline can fully address. The Petra Diamonds Finsch mine business rescue, announced in late May 2026, is among the most concrete expressions of that fracture yet seen at the operational level.

Understanding why this matters requires looking beyond the specifics of one mine's finances. The Finsch situation reflects a collision between structural demand shifts, technological disruption, currency pressures, and geological reality — forces that are reshaping who wins and who loses across the entire natural diamond value chain.

When big ASX news breaks, our subscribers know first

What Business Rescue Actually Means Under South African Law

Before examining the commercial dynamics driving Petra's decision, it is worth understanding what the formal mechanism of business rescue entails, because it is frequently mischaracterised in financial commentary.

Business rescue is a structured legal process defined under Chapter 6 of South Africa's Companies Act 71 of 2008. Its defining feature is that it is explicitly not liquidation. The objective is rehabilitation: to give a financially distressed company a supervised opportunity to restructure its affairs, business, property, debt, and equity in a manner that maximises the likelihood of the company continuing in existence, or at minimum, achieving a better outcome for creditors than immediate dissolution would provide.

How the Process Works in Practice

Once business rescue proceedings commence, several significant legal consequences take effect:

- An independent business rescue practitioner is appointed, assuming substantial authority over the company's strategic and operational decisions.

- A temporary moratorium is placed on all legal proceedings against the company, meaning creditors cannot independently enforce debt obligations during the rescue period.

- Employees retain their existing contracts and employment rights, though the practitioner may initiate restructuring processes including retrenchments under applicable labour law.

- Creditors must engage through the practitioner rather than pursuing independent legal remedies.

- The practitioner has authority to renegotiate, suspend, or in some cases cancel existing contracts where doing so serves the rescue plan.

The moratorium is a critical tool. It buys the company time to develop and implement a credible restructuring plan without the disruptive pressure of simultaneous creditor litigation. However, it is important to understand that business rescue does not guarantee survival. Outcomes span the full range from genuine operational recovery to structured wind-down that simply produces better creditor recoveries than a chaotic liquidation would.

Comparing Business Rescue to Global Equivalents

South Africa's framework shares conceptual DNA with Chapter 11 bankruptcy protection in the United States and voluntary administration in Australia, but differs in important respects. The South African model places particular emphasis on workforce protection and community obligations, which is especially relevant in a mining context where a single operation may represent the dominant employer across an entire region. The Finsch mine, located near Lime Acres in the Northern Cape, operates in exactly that kind of environment.

The Financial Anatomy of the Finsch Mine Crisis

Operational Profile and Revenue Significance

Finsch has been in continuous operation since 1967, making it one of South Africa's longest-running diamond production assets. Located in the Northern Cape province, the mine has historically ranked among Petra's most important revenue contributors, accounting for approximately 34% of the company's total group revenue in fiscal year 2025. At the time of the business rescue announcement, the mine employed approximately 1,700 employees and contractors, with broader economic dependencies extending well beyond that direct headcount into the surrounding regional economy.

The Geological Trap: Small Stones, Big Problems

Here is where the geological dimension becomes critically important to understanding why Finsch has become financially untenable while other operations remain viable. More than 90% of Finsch's rough diamond output consists of stones weighing two carats or less. This is not a recent operational failure — it reflects the fundamental geological character of the Finsch kimberlite pipe.

Kimberlite pipes, the volcanic rock formations that transport diamonds from deep within the earth's mantle to the surface, vary enormously in the size distribution and quality of the diamonds they contain. Finsch's pipe is characterised by high volume but small average stone sizes. In a market environment where commercial-grade small stones were priced well, this geological profile was commercially acceptable. In the current market, it has become a structural liability.

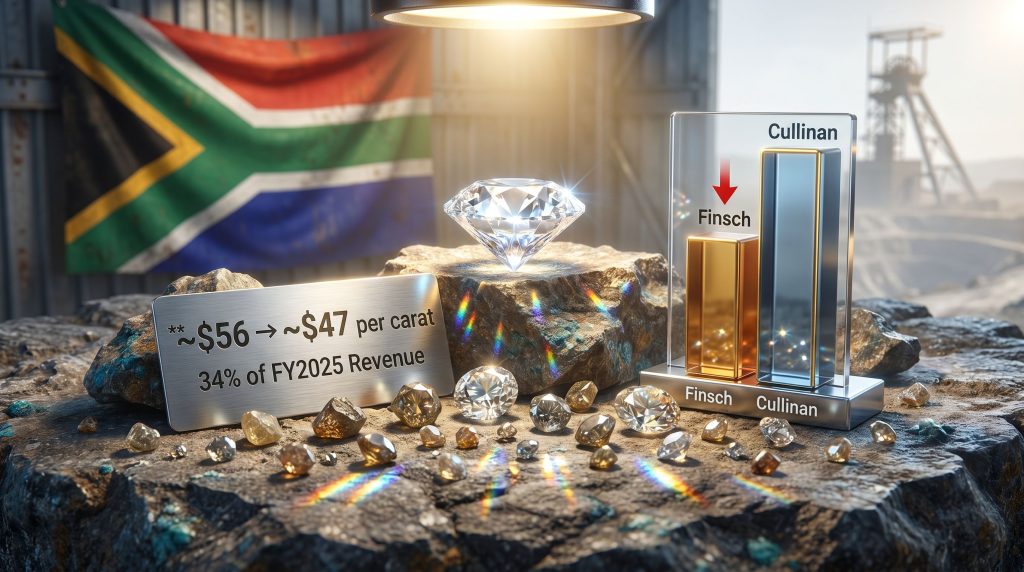

The pricing data illustrates the damage precisely:

| Metric | Previous Quarter | April to May 2026 | Change |

|---|---|---|---|

| Finsch average realised price (per carat) | ~$56 | ~$47 | 16% decline |

| Cullinan average realised price (per carat) | ~$109 | ~$81 | 26% decline |

| Finsch revenue contribution to group | 34% of FY2025 revenue | Under review | Guidance suspended |

Even Cullinan, which produces far higher-value stones, experienced a 26% decline in average realised prices between quarters. For Finsch, the combination of lower base prices and steeper percentage declines at the commercial-grade end of the market has pushed the operation past the point of financial sustainability.

The Currency Compounding Effect

A factor that receives less attention than it deserves is the role of rand strength in amplifying losses. Petra's diamond sales are denominated in US dollars, as is standard across the global rough diamond trade. When the South African rand strengthens against the dollar, every dollar of revenue converts into fewer rand, while mining costs — wages, electricity, consumables, contractors — remain rand-denominated. This currency mismatch functions as an invisible tax on margins, and its effect has compounded the impact of falling dollar prices.

For South African mining operations already operating on compressed margins, sustained rand strength can be the factor that pushes a marginal operation into genuine distress. Finsch appears to be a textbook case of that dynamic, and it is worth noting that similar commodity price pressures have been weighing on producers across multiple sectors.

Is the Finsch Collapse a Symptom of a Broken Diamond Market?

The Lab-Grown Diamond Disruption: Deeper Than It Appears

The narrative around lab-grown diamonds often focuses on price competition, but the more profound disruption is structural. Natural diamonds derived their pricing power from a combination of genuine physical scarcity and carefully cultivated consumer perception of that scarcity. Lab-grown diamonds — chemically and physically identical to mined stones but produced in controlled industrial environments — eliminate both dimensions simultaneously.

Production volumes of lab-grown diamonds are scalable in ways that geological kimberlite deposits simply are not. Entry costs for lab-grown production have declined sharply over the past decade, and the price gap between lab-grown and natural diamonds in commercial categories has widened dramatically in Western consumer markets, particularly in the United States.

The penetration is most acute in the commercial-grade segment: smaller, lower-clarity, lower-colour stones where the consumer's primary motivation is aesthetic rather than provenance. This is precisely the category that dominates Finsch's output. Premium, rare, large natural stones retain a meaningful identity distinction from lab-grown alternatives in the minds of high-net-worth buyers. A one-carat commercial-grade stone does not.

The diamond industry's historic pricing architecture was built on controlled supply and cultivated scarcity. Lab-grown production removes both constraints simultaneously, and that removal is permanent, not cyclical.

China's Demand Slowdown: A Structural or Cyclical Problem?

China has historically functioned as one of two anchor demand markets for global diamond consumption, alongside the United States. The prolonged contraction in China's domestic property sector has had a cascading effect on discretionary luxury spending, with jewellery demand among the categories most affected. Chinese consumer confidence has remained subdued, and bid volumes from Chinese tender buyers at rough diamond auctions have weakened measurably.

The critical question for the industry is whether this represents a cyclical trough or a more durable shift in Chinese luxury consumption patterns. If Chinese consumers increasingly equate diamond jewellery with speculative asset value — closely linked to property wealth — a sustained property sector depression could produce a generational shift in sentiment rather than a recoverable cyclical dip.

De Beers and the Limits of Supply-Side Management

De Beers, the world's largest diamond producer, has implemented multiple rounds of production cuts and supply reductions over the past two years. Furthermore, inventory accumulation across the diamond pipeline has persisted despite these measures. The Petra Diamonds Finsch mine business rescue announcement is arguably the clearest signal yet that supply-side management alone cannot restore pricing floors for producers whose output is concentrated in commercial-grade categories.

The market is bifurcating: rare, premium natural diamonds are holding value with greater resilience, while smaller commercial-grade inventory continues to accumulate without clearing. This trend is observable across global diamond producers who are increasingly being forced to reassess their operational strategies.

Petra's Strategic Pivot: Cullinan as the Survival Bet

The Type IIa Diamond Advantage: A Geological Primer

Cullinan's strategic value lies in a geological distinction that most commentary on the diamond industry fails to explain clearly. Diamonds are classified into types based on their nitrogen content and structural characteristics. Type Ia diamonds, which represent the vast majority of natural diamonds, contain nitrogen atoms clustered in pairs or larger aggregates within the crystal lattice. Type IIa diamonds contain no measurable nitrogen impurities whatsoever, making them the most chemically pure form of diamond that exists.

This chemical purity has two commercially significant consequences:

- Optical clarity: Type IIa diamonds tend to exhibit exceptional transparency and light performance, producing the visual qualities most prized by premium jewellery buyers and auction houses.

- Rarity: Type IIa diamonds represent roughly 1 to 2% of all gem-quality diamonds mined globally. This genuine geological scarcity is not manufacturable in lab-grown production at equivalent quality levels.

The Cullinan pipe has historically produced some of the world's most significant Type IIa stones, including numerous gems that now form part of the British Crown Jewels. This provenance and ongoing geological potential gives Cullinan a premium market positioning that is genuinely differentiated from lab-grown competition.

Petra is actively increasing mining activity in higher-value geological zones within the Cullinan orebody, redeploying both capital and skilled workers from Finsch to maximise output from this premium segment. In this respect, the restructuring mirrors broader mining industry consolidation trends seen across the sector, where operators are shedding marginal assets to concentrate resources on their highest-value operations.

The Strategic Logic and Its Risks

If Cullinan's premium output sustains average realisations above $80 to $90 per carat, Petra may generate sufficient cash flow to service obligations while the Finsch rescue process proceeds. However, Cullinan's own April to May 2026 average realised price of approximately $81 per carat sits uncomfortably close to that threshold, leaving limited margin for further deterioration.

The leadership restructuring that accompanied the Finsch announcement adds further complexity. The departure of long-serving executive Juan Kemp at the end of May 2026 leaves CEO Vivek Gadodia as sole executive leader at precisely the moment when the company is navigating its most challenging operational period. Petra has suspended all financial guidance previously issued through 2030 and is developing a new business plan expected later in 2026.

What the Finsch Rescue Means for Workers and Mining Communities

Scale of Workforce Exposure

Petra employs more than 4,000 people across its South African operations. The approximately 1,700 employees and contractors directly associated with Finsch represent a significant proportion of that total. Formal consultation with employees and labour unions has commenced under the requirements of South African labour law, specifically the framework established under Section 189 of the Labour Relations Act, which governs large-scale retrenchment processes and entitles affected workers to structured consultation, defined notice periods, and severance entitlements.

Petra has not publicly disclosed the precise number of anticipated job losses, but given the scale of the operational suspension at Finsch, the number is likely to be material. Reporting from CNBC Africa confirms that job cuts are being implemented across the group alongside the formal rescue proceedings.

Regional Economic Dependencies

The Lime Acres area of the Northern Cape, where Finsch is situated, has limited alternative employment opportunities of comparable scale. Mining wages and contractor spending form a substantial portion of local economic circulation. Historical precedent from other South African mining closures and restructurings suggests that regional economic contraction following large mine closures can persist for years, affecting supplier businesses, transport operators, service providers, and housing markets well beyond the directly employed workforce.

The next major ASX story will hit our subscribers first

How This Fits Into Africa's Wider Diamond Sector Crisis

The Petra Diamonds Finsch mine business rescue does not occur in isolation. It is one data point in a broader pattern of distress affecting diamond-dependent economies across southern Africa. Indeed, geopolitical mining risks and shifting trade dynamics are compounding the sector-specific pressures already facing producers in the region.

| Country | Diamond Sector Significance | Key Risk Exposure |

|---|---|---|

| South Africa | Major producer; multiple active mines | Employment, export revenue, rand dynamics |

| Botswana | Diamonds represent approximately 70 to 80% of export earnings | Sovereign revenue, credit rating pressure |

| Namibia | Significant offshore and onshore production | Foreign investment confidence, fiscal receipts |

Botswana's sovereign credit rating was downgraded by S&P, a development that reflects how diamond sector revenue pressure has migrated from corporate balance sheets to national fiscal accounts. For these economies, diamond industry distress is not simply a mining finance issue — it carries direct implications for government spending capacity, social programmes, and economic stability.

Cyclical Correction or Structural Realignment?

This is arguably the most consequential question facing the industry. Previous diamond market downturns, including those following the 2008 global financial crisis, were fundamentally demand recessions — temporary demand reductions from which the market eventually recovered as consumer confidence returned. The current downturn contains that cyclical dimension but also embeds a structural component that did not exist in previous cycles: permanent, scalable lab-grown substitution in the commercial-grade segment.

Producers of large, rare, high-quality stones with genuine geological differentiation are better positioned to survive the structural shift. High-volume commercial-grade miners concentrated in smaller stones face a market where their competitive positioning is deteriorating in ways that supply discipline cannot reverse. Consequently, policy responses across producer nations — including beneficiation requirements, royalty adjustments, and discussions around state support mechanisms — are being evaluated, though these operate at the margin of a market undergoing fundamental repricing.

Moreover, comparisons with major mining operations in other commodities suggest that the path to viability increasingly demands a combination of asset quality, geological differentiation, and financial resilience rather than volume alone.

Frequently Asked Questions: Petra Diamonds Finsch Mine Business Rescue

What does business rescue mean for the Finsch mine?

Business rescue is a formal legal process under South Africa's Companies Act that places the mine under the supervision of an independent practitioner, with a moratorium on creditor enforcement, while a restructuring plan is developed. It aims to rehabilitate the operation or achieve a better outcome for stakeholders than immediate liquidation would provide.

How many jobs are at risk?

Approximately 1,700 employees and contractors work directly at Finsch. Petra has not disclosed the precise number of anticipated retrenchments, but formal consultation with unions and employees is underway under South African labour law requirements.

Why are diamond prices falling so sharply?

Several forces are converging: rapid growth of lab-grown diamonds in commercial jewellery markets, sustained demand weakness from China following its property sector contraction, global economic uncertainty dampening luxury spending, and rand strength compressing rand-equivalent revenues from dollar-denominated sales.

What makes Cullinan different from Finsch geologically?

Cullinan produces a significant proportion of Type IIa diamonds, the rarest and most chemically pure diamond classification, representing approximately 1 to 2% of all gem-quality diamonds mined globally. Finsch's geological profile produces predominantly smaller commercial-grade stones, the category facing the most severe and sustained price pressure.

What happens to Finsch's creditors during business rescue?

A legal moratorium prevents creditors from taking independent enforcement action against the mine during the rescue period. All creditor engagements are routed through the appointed business rescue practitioner, who has authority to renegotiate or restructure obligations as part of the rescue plan.

Will Petra Diamonds survive the current crisis?

Petra has suspended financial guidance through 2030 and is developing a revised business plan. The company's strategy centres on concentrating resources at Cullinan while the Finsch rescue process proceeds. Survival depends substantially on whether Cullinan can maintain average realised prices above operational cost thresholds and whether broader market conditions stabilise. This represents forward-looking analysis and is not a guarantee of any particular outcome.

Key Takeaways: What the Finsch Rescue Signals for the Diamond Industry

The Petra Diamonds Finsch mine business rescue is not a self-contained corporate event. It is a symptomatic expression of forces that are reshaping the natural diamond industry at a foundational level:

- Commercial-grade small-stone producers face the greatest structural viability risk as lab-grown substitution deepens in their core market segment.

- The bifurcation between premium rare diamonds (particularly Type IIa stones) and mass-market commercial inventory is accelerating and is likely permanent.

- Supply-side management by major producers has proven insufficient to defend pricing floors in commercial categories when demand destruction has a structural rather than purely cyclical cause.

- African economies with high diamond export dependency face compounding fiscal, employment, and sovereign credit risks that extend well beyond individual corporate restructurings.

- The geological profile of a mine is no longer merely a technical detail — in the current market environment, it is the primary determinant of medium-term viability.

- Investor and policymaker frameworks built on historical diamond market assumptions require fundamental revision to remain relevant.

Readers seeking additional market context can explore related coverage via Mining.com's reporting on the Finsch closure. This article contains forward-looking analysis and market observations that involve uncertainty. Nothing in this article constitutes financial advice, and readers should conduct their own independent research before making investment decisions.

Want To Stay Ahead of Major Mineral Discoveries Before the Broader Market Reacts?

While the diamond sector navigates structural headwinds, opportunities in other mineral discoveries continue to emerge on the ASX — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant discoveries are announced, turning complex geological and market data into actionable insights for both traders and long-term investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position yourself ahead of the market.