June 14, 2026

The Hidden Architecture of Gulf Capital Flows

When analysts examine sovereign investment landscapes across the Gulf Cooperation Council, the instinct is often to focus on headline flow numbers and ranking tables. Yet the more revealing story lies beneath the surface: in the structural design of a nation's capital account, the composition of its sectoral exposure, and the asymmetry between what a country attracts and what it deploys abroad. Qatar inward foreign direct investment data for 2025, released in May 2026 through a joint report by the National Planning Council and the Qatar Central Bank, offers precisely this kind of layered insight for those willing to read past the top line.

When big ASX news breaks, our subscribers know first

Why Qatar Has Become a Magnet for Global Capital

The Structural Pillars Behind Investor Confidence

Few economies in the Middle East combine macroeconomic stability, sovereign financial depth, and regulatory openness in the way Qatar has engineered over the past two decades. The country's appeal to foreign capital is not accidental; it is the product of deliberate policy architecture built on three interlocking structural foundations.

The first pillar is hydrocarbon export revenue, which provides Qatar with a consistent and substantial hard currency inflow, insulating its fiscal position from the cyclical pressures that affect less resource-endowed economies. The second is sovereign wealth buffer capacity through the Qatar Investment Authority, which serves as both a stabilisation mechanism and a signal to international investors that the government can manage external shocks without distorting domestic asset markets.

The third pillar, often underappreciated in analyst commentary, is Qatar's net external creditor status, meaning the country holds more foreign assets than it owes abroad. This position is a powerful risk signal for cross-border investors evaluating counterparty exposure.

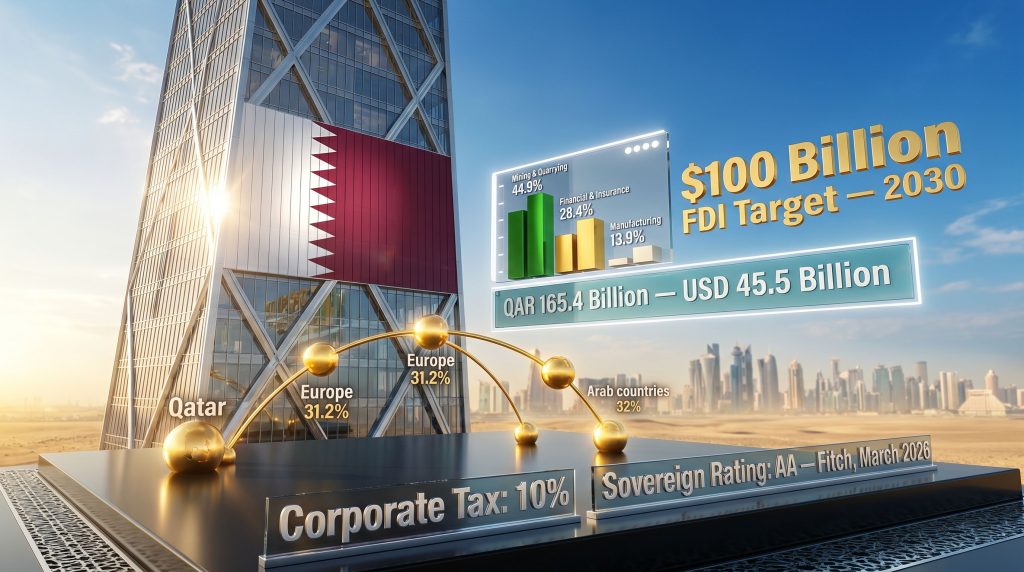

Reinforcing these structural advantages, Fitch Ratings affirmed Qatar's sovereign credit rating at AA with a stable outlook in March 2026, citing the country's robust sovereign balance sheet as a key justification. For international capital allocators using rating-based investment mandates, this affirmation functions as a credibility anchor that keeps Qatar within the investable universe of a broad institutional investor base.

Qatar also eliminates one of the most common friction points for cross-border investors: currency risk. The Qatari riyal has maintained a fixed peg to the US dollar since 1980, currently set at approximately QAR 3.64 per USD. This arrangement means that foreign investors holding Qatar-denominated assets are not exposed to exchange rate volatility when repatriating returns, a meaningful structural advantage over markets where local currency fluctuation erodes investment performance.

Qatar National Vision 2030 and the $100 Billion FDI Target

The policy framework underpinning Qatar's FDI ambitions is Qatar National Vision 2030, a long-range economic transformation agenda targeting a transition from hydrocarbon dependency to a diversified, knowledge-based economic model. Central to this vision is a cumulative inward FDI target of USD 100 billion by 2030.

With inward FDI stock reaching approximately USD 45.5 billion at end-2025, Qatar has covered roughly 45% of its decade-long target with five years remaining. Whether this represents strong progress or a widening gap depends significantly on trajectory assumptions and the pace of policy reform in currently restricted sectors.

A landmark step in this liberalisation journey was the 2018 Foreign Investment Law, which permits 100% foreign ownership across the majority of Qatar's economic sectors. This reform broadened the investable universe considerably, removing ownership barriers that had historically limited foreign participation to joint venture arrangements requiring a local Qatari majority partner.

The 2018 Foreign Investment Law represents the most significant single structural reform in Qatar's FDI liberalisation history, fundamentally changing the risk calculus for international investors evaluating full-ownership business establishment in the country.

What Do the 2025 FDI Numbers Actually Tell Us?

Unpacking Qatar Inward Foreign Direct Investment in Full-Year 2025

The headline figure from Qatar's 2025 FDI survey is an inward FDI stock of QAR 165.4 billion, equivalent to approximately USD 45.5 billion, representing a 2% year-on-year increase from 2024 levels. This data was released in preliminary form by the National Planning Council in collaboration with the Qatar Central Bank and covers the full period from January through December 2025.

Understanding the methodology behind this figure is essential for correct interpretation. The survey drew on responses from approximately 200 private-sector enterprises, supplemented by selected government-owned companies and financial institutions under Qatar Central Bank supervision. Critically, the dataset excludes two categories of capital activity:

- Public-sector investments made directly by government ministries or state entities

- International financial activities conducted by private individuals

This means the QAR 165.4 billion figure represents a partial rather than comprehensive measurement of all foreign capital operating in Qatar. The magnitude of excluded public-sector activity is not specified in the available data, making it difficult to assess the full scale of the country's foreign capital base.

Results from the enterprise survey were then consolidated with Qatar Central Bank data covering monetary financial institutions including banks, insurers, and other regulated entities, creating a two-source composite picture of the country's inward investment position.

The Net FDI Position: Reading Between the Lines

Perhaps the most analytically significant data point in the 2025 report is not the inward figure but the net FDI stock, which reached QAR 44.6 billion by year-end, up from QAR 32.2 billion in 2024. This represents a 39% expansion in the net position, or an absolute increase of QAR 12.4 billion over twelve months.

This net position is driven by outward FDI stock of QAR 210 billion growing at 8.1% year-on-year, substantially outpacing the 2% growth in inward FDI. The resulting asymmetry carries a specific analytical implication: Qatar is deploying capital internationally at a significantly faster rate than it is attracting it domestically.

| Metric | 2025 Value | Year-on-Year Change |

|---|---|---|

| Inward FDI Stock | QAR 165.4bn (USD 45.5bn) | +2% |

| Outward FDI Stock | QAR 210bn | +8.1% |

| Net FDI Stock | QAR 44.6bn | +39% |

| Net FDI Change (Absolute) | +QAR 12.4bn | YoY expansion |

Rather than signalling weakness in Qatar's attractiveness as a destination, this pattern reflects a characteristic of sovereign maturity: a nation with accumulated capital surpluses actively seeking return opportunities across global asset markets while maintaining a stable and well-established inward investment base at home.

Which Sectors Are Capturing Qatar's Inward FDI?

Sector Concentration: Five Industries Account for Over 90% of All Inflows

One of the most striking structural features of Qatar's inward FDI profile is its extreme sectoral concentration. More than 90% of all inward FDI positions are held within just five economic activities, creating a portfolio that is deep in a small number of sectors rather than broad across the economy.

| Sector | Share of Inward FDI |

|---|---|

| Mining and Quarrying | 44.9% |

| Financial and Insurance Activities | 28.4% |

| Manufacturing | 13.9% |

| Professional, Scientific and Technical Activities | 4.1% |

| Information and Communication | 3.0% |

| All Other Sectors | ~5.7% |

This concentration pattern has both strengths and vulnerabilities. On the positive side, it reflects the natural alignment of foreign capital with Qatar's most competitive economic assets: its hydrocarbon infrastructure and its emerging financial services ecosystem. On the risk side, it leaves the inward FDI portfolio heavily exposed to energy price cycles and longer-term global decarbonisation trends, a concern that sits at the heart of broader critical minerals demand conversations shaping global investment priorities in 2025.

Why Hydrocarbons Command 44.9% of Inward FDI

The dominance of mining and quarrying in Qatar's inward FDI stock is a direct consequence of the country's position as one of the world's largest exporters of liquefied natural gas. Qatar's LNG sector operates through long-duration joint venture structures that typically involve major international energy companies holding equity stakes in production and processing infrastructure. These arrangements generate large, persistent FDI stock positions that are unlikely to shift materially in the short term regardless of annual capital flow variations.

The ongoing North Field expansion programme, designed to increase Qatar's LNG export capacity significantly into the mid-2030s, is expected to sustain and potentially increase foreign capital commitments within this sector. Long-term supply agreements and infrastructure co-investment arrangements with international energy majors create structural demand for this category of FDI that extends well beyond current investment cycles.

Financial Services as the Second Pillar at 28.4%

The financial and insurance sector's 28.4% share of inward FDI reflects Qatar's success in positioning itself as a regional financial hub, primarily through the Qatar Financial Centre (QFC). The QFC operates under a common law legal framework modelled on internationally recognised standards, which differentiates it from onshore Qatari commercial law and provides foreign financial institutions with a more familiar regulatory environment.

Sub-sectors driving this FDI category include Islamic finance institutions, conventional banking operations, reinsurance and insurance providers, and asset management firms. The growth of Sharia-compliant financial products across the Gulf and broader Muslim-majority markets creates an ongoing structural demand for Qatar-based financial infrastructure that attracts specialist foreign capital.

Manufacturing and the Diversification Imperative at 13.9%

Manufacturing's 13.9% share represents Qatar's most visible progress in attracting FDI beyond the hydrocarbon sector. Industrial zones at Mesaieed and Ras Laffan serve as the primary geographic destinations for this capital, hosting downstream petrochemical processing, specialty chemical manufacturing, and industrial production facilities that leverage Qatar's feedstock cost advantages.

For the QNV 2030 diversification objective to be met, growing this 13.9% share will be essential. A meaningful reweighting of inward FDI from pure extraction toward value-added manufacturing would represent genuine structural progress rather than simply incremental growth within an existing hydrocarbon framework. This challenge mirrors the critical raw materials transition underway globally, where resource-dependent economies are actively seeking to capture more downstream value.

Where Is Qatar's Outward FDI Going, and Why Does It Matter?

Qatar's Expanding Global Capital Footprint

While Qatar inward foreign direct investment data attracts the most attention in economic reporting, the outward FDI picture reveals equally important strategic dynamics. Outward FDI stock climbed to QAR 210 billion at end-2025, representing an 8.1% increase year-on-year and confirming Qatar's status as one of the most active capital exporters in the Gulf region on a per-capita basis.

Outward FDI Sector Distribution

| Sector | Share of Outward FDI |

|---|---|

| Financial and Insurance Activities | 34.0% |

| Mining and Quarrying | 27.8% |

| Information and Communication | 11.5% |

| Accommodation and Food Services | 9.6% |

| Arts, Entertainment and Recreation | 6.9% |

| All Other Sectors | ~10.2% |

The divergence between inward and outward sector profiles is analytically instructive. Inward FDI is concentrated in extractive industries (44.9% mining), while outward FDI is led by financial services (34.0%). This suggests Qatar's international capital deployment through sovereign and institutional vehicles is increasingly oriented toward financial and service-sector assets abroad, even as the domestic economy continues attracting foreign capital primarily through its resource sector.

Geographic Concentration of Qatar's Global Investments

More than 60% of Qatar's outward investment stock is directed toward two geographic blocs: Arab countries at 32% and Europe at 31.2%. This dual concentration reflects two distinct strategic logics operating simultaneously. Furthermore, Europe's strategic metals push and broader investment diversification ambitions make the continent an increasingly natural destination for Gulf sovereign capital.

The Arab regional allocation at 32% reflects Gulf economic interdependence and regional integration priorities, with capital flowing toward neighbouring economies through both bilateral investment and broader GCC financial market participation. The European allocation at 31.2%, primarily associated with Qatar Investment Authority holdings in real estate, listed equities, and infrastructure assets, reflects a long-standing strategy of diversifying sovereign wealth into stable, developed-market assets with deep liquidity.

The remaining approximately 37% of outward FDI is distributed across Asia, the Americas, Africa, and other regions, with specific geographic breakdowns not disclosed in the currently available data.

The Regulatory Architecture Governing Qatar Inward FDI

A Legal Framework Built for Openness, With Defined Boundaries

Qatar's FDI regulatory environment has undergone substantial liberalisation over the past decade, though important restrictions remain in place across specific sectors. Understanding the full legal landscape is essential for investors evaluating entry strategies and ownership structures.

The key legislative instruments governing foreign investment include:

- 2018 Foreign Investment Law: the cornerstone of Qatar's liberalisation agenda, permitting 100% foreign ownership across the majority of economic sectors

- Law 1/2019: applies a 49% cap on foreign ownership in banking, insurance, and commercial agency activities unless explicit Cabinet-level approval is secured

- Qatar Stock Exchange listings: many listed companies have raised individual foreign ownership ceilings to 49% of issued share capital

- Telecommunications sector: remains predominantly under state-enterprise control, limiting private foreign capital entry

This architecture creates a two-tier system: broad openness across most commercial and professional sectors, combined with carefully maintained restrictions in systemically sensitive industries where state oversight is considered a strategic priority.

Tax Competitiveness as a Capital Attraction Lever

Qatar's tax environment is among the most internationally competitive of any significant economy. A 10% corporate income tax rate applies to most foreign business operations, while no personal income tax is levied on individuals. This combination is particularly attractive for expatriate executives, high-net-worth individuals, and international companies seeking to establish regional headquarters.

A growing network of double taxation avoidance treaties further reduces withholding tax friction on cross-border profit repatriation, reducing the effective tax burden on international investors holding Qatari-based operations.

Comparing Qatar's Regulatory Environment to Gulf Peers

| Indicator | Qatar | UAE | Saudi Arabia |

|---|---|---|---|

| Max Foreign Ownership (General) | 100% | 100% | 100% |

| Max Foreign Ownership (Banking) | 49% | Varies | 49% |

| Corporate Tax Rate | 10% | 9% | 20% |

| Sovereign Credit Rating (Fitch) | AA Stable | AA- Stable | A+ Stable |

| Inward FDI Stock (2025, approx.) | USD 45.5bn | N/A | USD 280bn |

Note: Regulatory frameworks and tax rates are subject to change. Investors should seek independent legal and tax advice before making investment decisions.

The next major ASX story will hit our subscribers first

Who Is Investing in Qatar? Geographic Sources of Inward FDI

The Three Primary Investor Origin Blocs

Qatar's inward FDI base draws predominantly from three geographic clusters, each with distinct sectoral preferences and investment motivations:

-

European Union (~30% of total inward FDI stock): The largest single origin bloc, with European capital concentrated in financial services, energy joint ventures, and professional services operations. Long-standing bilateral trade relationships and QFC common law alignment create institutional familiarity that lowers entry barriers.

-

United States (~24% of total inward FDI stock): US investment is heavily concentrated in the hydrocarbon sector, particularly through equity participation in LNG production and export infrastructure. Financial services representation is also significant, with major US banks maintaining regional operations in Qatar.

-

Asia (~7% of total inward FDI stock): Representing a proportionally modest share relative to Asia's weight in global FDI flows, this segment has meaningful growth potential as Gulf-Asia economic corridors deepen and bilateral trade volumes expand.

Underrepresented Sources and Future Growth Corridors

The relatively modest Asian share of inward FDI presents both a puzzle and an opportunity. Given that Asian economies collectively represent a dominant share of global capital formation and FDI outflows, a 7% Asian contribution to Qatar's inward stock suggests significant untapped potential.

India represents a particularly interesting case. Qatar hosts one of the largest Indian expatriate communities in the world, and bilateral trade and remittance flows are substantial. However, formal Indian FDI into Qatar remains modest, suggesting that personal economic connections have not yet translated into institutional investment relationships at scale.

Chinese capital deployment through Belt and Road-adjacent frameworks has been active across parts of the Gulf region, but Qatar's positioning relative to these flows remains underdeveloped compared to some regional peers. Consequently, as economic corridor development progresses and Gulf-China trade relationships deepen, the Asian share of Qatar's inward FDI base could expand materially through the remainder of the decade.

How Does Qatar's FDI Performance Compare Regionally?

Qatar vs. Saudi Arabia: Scale, Trajectory, and Quality

Any regional FDI comparison must acknowledge the fundamental scale differential between Qatar and Saudi Arabia. Saudi Arabia's inward FDI stock reached approximately USD 280 billion in 2025, roughly six times Qatar's inward position. Saudi Arabia also recorded 90% net FDI inflow growth in Q4 2025, reflecting the large-scale capital mobilisation associated with Vision 2030 mega-project development.

However, raw scale comparisons can obscure more than they reveal. Qatar's FDI position on a per-capita basis is substantially higher than Saudi Arabia's, reflecting a small-population, high-intensity economic model rather than a large-population, broad-base development strategy. The broader geopolitical mining landscape further illustrates how sovereign strategy, rather than scale alone, increasingly determines capital attraction outcomes across resource-rich nations.

The FDI Quality Argument: Why Growth Rates Can Mislead

Qatar's 2% inward FDI growth rate in 2025 should be interpreted through the lens of existing base-level commitments rather than viewed as evidence of declining investor interest. A large portion of Qatar's inward FDI stock represents long-duration infrastructure capital tied to LNG facilities, refinery capacity, and financial sector operations that were established through multi-decade agreements.

The distinction between greenfield FDI (capital deployed to create new productive capacity) and M&A-driven FDI (ownership transfers of existing assets) is critical here. A country dominated by greenfield, infrastructure-anchored FDI will naturally show lower headline growth rates than one experiencing large-scale ownership transfers, even if the underlying investment quality is higher.

Key Risks and Constraints on Qatar's FDI Trajectory

Structural Concentration Risk

The single greatest vulnerability in Qatar's inward FDI profile is its 44.9% concentration in mining and quarrying. While LNG infrastructure is highly capital-intensive and creates durable FDI commitments, this concentration creates exposure to two long-term structural headwinds:

- Energy price cycles: Extended periods of weak LNG pricing could dampen the appetite of international energy majors for capacity expansion investment, slowing FDI growth in the dominant sector

- Global decarbonisation pressure: Long-term transition away from fossil fuels in major consuming economies could gradually reduce the strategic value of LNG infrastructure commitments, particularly for European investors facing energy transition policy mandates

Reducing this concentration by attracting meaningful foreign capital into technology, healthcare, education, and renewable energy investment sectors is both the central challenge and the central opportunity of Qatar's post-2030 investment strategy.

Regulatory Friction Points

Several regulatory constraints continue to limit the depth and breadth of Qatar's inward FDI universe:

- The 49% banking and insurance cap restricts full-scale financial sector FDI from global institutions seeking majority or wholly-owned operations

- Telecommunications sector dominance by state enterprises limits the entry of foreign digital infrastructure providers

- A perception gap may persist among international investors who are unaware of the extent of reforms enacted since 2018, effectively excluding potentially interested capital that underestimates Qatar's current openness

Geopolitical and Regional Risk Factors

Qatar's investment climate is not insulated from broader regional geopolitical dynamics. The 2017 to 2021 Gulf diplomatic crisis, during which Qatar faced an economic blockade imposed by several neighbouring states, provided a stress test for investor confidence that had measurable short-term impacts on capital flows. The resolution of this crisis and the subsequent normalisation of regional relationships have partially addressed this risk factor, but the episode serves as a reminder that Gulf regional stability is a prerequisite for sustained investor confidence.

Qatar's multi-vector foreign policy approach, maintaining relationships with the United States, European partners, regional Arab states, and other global actors simultaneously, functions as a structural risk diversification mechanism. However, this approach also creates complexity for investors seeking to assess geopolitical alignment risk, a challenge well documented in analysis of the US investment climate statement for Qatar.

Can Qatar Reach Its $100 Billion FDI Goal by 2030?

Scenario Analysis: Three Pathways to the Target

With inward FDI stock at approximately USD 45.5 billion at end-2025 and five years remaining to reach the USD 100 billion cumulative target, Qatar faces a significant but not insurmountable capital attraction challenge. The plausibility of reaching the goal depends on which structural conditions materialise over the remainder of the decade.

| Scenario | Key Conditions | Projected Inward FDI by 2030 |

|---|---|---|

| Base Case | Stable energy prices, incremental reform, continued LNG expansion | USD 65 to 75 billion |

| Accelerated Diversification | Meaningful non-hydrocarbon FDI in technology, healthcare, and finance | USD 80 to 90 billion |

| Full Liberalisation | Banking and telecom market opening, digital economy surge | USD 95 to 110 billion |

Disclaimer: These projections are illustrative scenarios based on structural assumptions and should not be interpreted as forecasts or investment advice. Actual outcomes will depend on macroeconomic conditions, policy implementation, and global capital market dynamics that cannot be predicted with precision.

Sectors Most Likely to Drive Future FDI Growth

Several non-hydrocarbon sectors carry genuine potential for meaningful FDI attraction over the next five years:

- Technology and digital economy: Qatar's smart city infrastructure investment and nascent AI capability development create conditions for attracting technology-sector FDI from global firms seeking regional operational bases

- Healthcare and education: The human capital pillar of QNV 2030 generates institutional demand for world-class medical and educational facilities, sectors where foreign expertise and capital are natural complements

- Tourism and hospitality: The infrastructure legacy from hosting the 2022 FIFA World Cup provides a developed platform for sustained hospitality-sector FDI, supported by an expanding aviation hub at Hamad International Airport

- Renewable energy: Qatar's solar energy ambitions, still at an early development stage, represent a new FDI frontier that could attract project finance capital from international clean energy developers

The Policy Changes Required to Close the Gap

Reaching the upper end of the 2030 FDI range will require deliberate policy action across several dimensions:

- Removing or raising ownership caps in banking and insurance to attract full-scale financial sector investment from global institutions

- Opening the telecommunications market to meaningful foreign private participation

- Expanding the double taxation treaty network to cover more emerging market economies where bilateral capital flows remain restricted

- Deepening Qatar Stock Exchange access for foreign portfolio investors, increasing secondary market liquidity and attracting institutional equity capital

- Strengthening dispute resolution frameworks across the broader Qatari economy to match the internationally recognised standards of the QFC environment

The gap between where Qatar currently stands and where it needs to be to reach its 2030 FDI target is not a capital availability problem. It is a regulatory and structural diversification problem. Addressing the remaining ownership restrictions and sector limitations is the most direct lever available to policymakers seeking to accelerate inbound capital attraction.

Frequently Asked Questions: Qatar Inward Foreign Direct Investment

What is Qatar's total inward FDI stock as of 2025?

Qatar's inward FDI stock reached QAR 165.4 billion, equivalent to approximately USD 45.5 billion, at the end of 2025. This represents a 2% increase from 2024 and was reported through preliminary data released by the National Planning Council in collaboration with the Qatar Central Bank.

Which sector attracts the most foreign direct investment into Qatar?

Mining and quarrying accounts for 44.9% of all inward FDI positions, making it by a substantial margin the dominant destination for foreign capital. This primarily reflects long-duration equity commitments in Qatar's LNG and hydrocarbon infrastructure by international energy companies.

What is Qatar's FDI target under Qatar National Vision 2030?

Qatar has set a cumulative inward FDI target of USD 100 billion by 2030 as part of its broader QNV 2030 economic diversification strategy. At the end of 2025, the country had reached approximately 45% of this target.

Can foreign investors own 100% of a business in Qatar?

Yes, in most sectors. The 2018 Foreign Investment Law permits full foreign ownership across the majority of Qatar's economic activities. Banking, insurance, and commercial agency sectors are subject to a 49% foreign ownership ceiling under Law 1/2019, with exceptions available through Cabinet approval.

What is Qatar's corporate tax rate for foreign investors?

Qatar applies a corporate income tax rate of 10%, placing it among the most competitive major economies globally for business taxation. No personal income tax applies to individuals operating in Qatar.

How does Qatar's inward FDI compare to its outward FDI?

Qatar's outward FDI stock of QAR 210 billion at end-2025 exceeds its inward FDI stock of QAR 165.4 billion by QAR 44.6 billion, confirming Qatar's position as a net capital exporter. This net position expanded by 39% in 2025 alone, reflecting the accelerating international reach of Qatari capital relative to domestic capital attraction.

Want to Stay Ahead of the Next Major Mineral Discovery?

While Qatar's sovereign capital continues flowing into global mining and resource sectors at scale, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced — turning complex exploration data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the market.