June 9, 2026

The Quiet Revolution Reshaping Andean Copper Supply

Across the Andes, a structural shift is underway that rarely captures headlines but is fundamentally altering how copper supply reaches global markets. Rather than massive greenfield developments requiring decade-long timelines and billion-dollar commitments, a growing cohort of specialised mining companies is targeting something far more capital-efficient: the reactivation of dormant oxide copper operations that major diversified miners have quietly walked away from during periods of portfolio rationalisation.

This brownfield restart phenomenon is not incidental. It reflects a calculated response to tightening copper supply fundamentals, where the fastest path from resource to refined metal increasingly runs through assets that already have roads, power lines, leach pads, and processing circuits in place. Within this context, Quilla Chapi copper production in Peru has emerged as one of the most closely watched brownfield restart stories in the Andean copper corridor, combining an established production history, a proven processing method, and an ambitious expansion capital envelope of up to US$300 million.

Understanding why this project matters requires looking beyond the headline figures to examine the technical mechanics, historical production context, capital structure logic, and strategic market positioning that collectively define the Chapi opportunity. Furthermore, the broader copper supply crunch reshaping global markets makes assets like this increasingly significant.

When big ASX news breaks, our subscribers know first

Chapi's Geographic and Strategic Foundation

Location, Ownership Transition, and Brownfield Classification

The Chapi mine occupies a strategically advantageous position in southern Peru, situated approximately 50 kilometres south-southeast of Arequipa across the Moquegua and Arequipa departments. This placement within one of the Andes' most historically productive copper corridors is not coincidental; the region's geology consistently favours oxide copper mineralisation amenable to heap leach and SX-EW processing.

Quilla Resources completed its acquisition of Chapi from Nexa Resources in late 2024, marking a significant ownership transition. Nexa's decision to divest reflected a broader portfolio rationalisation common among major diversified miners, who periodically shed non-core assets to concentrate capital on flagship operations. For Nexa, whose strategic focus centres on zinc operations primarily in Brazil, Chapi represented a peripheral copper asset that consumed management attention without contributing materially to group production.

For Quilla, however, it represented precisely the opposite: a permitted, infrastructure-endowed copper asset with an established production history and meaningful expansion optionality. The brownfield classification carries substantial practical implications that are frequently underappreciated by generalist investors. Unlike greenfield projects that require constructing all infrastructure from scratch and navigating the full environmental impact assessment (EIA) process from the initial baseline, brownfield restarts operate within an existing permitting framework.

This distinction typically translates to:

- 30 to 40% lower initial capital requirements compared to equivalent greenfield capacity

- Environmental amendment processes requiring approximately 6 to 9 months, versus 18 to 24 months for entirely new EIA applications

- Pre-existing community relationships and social licence frameworks that reduce stakeholder engagement risk

- A documented operational history that supports more reliable technical assumptions in restart planning

Peru's Copper Sector and the Role of Mid-Tier Oxide Operations

A National Output Story Built on Structural Diversity

Peru ranks as the world's second-largest copper producer, with annual output consistently ranging between 2.7 and 2.8 million tonnes in recent years. Production is dominated by massive sulphide operations including Las Bambas, Cerro Verde, Antamina, and Toquepala, but the national output profile depends meaningfully on the collective contribution of mid-tier and smaller operations. In addition, Andean copper developments across the broader region are reinforcing this structural pattern of diverse, layered production growth.

What makes projects like Chapi strategically distinct within Peru's copper production hierarchy is their processing output type. Peru's copper export profile encompasses two fundamentally different product streams:

| Output Type | Processing Route | Key Characteristic |

|---|---|---|

| Copper concentrate | Sulphide flotation | Requires smelter processing, subject to TC/RC charges |

| Copper cathode | SX-EW (oxide ores) | Refined product, direct LME market access |

Copper cathode produced via SX-EW commands a processing premium over concentrate because it eliminates smelter treatment charges (TC) and refining charges (RC) entirely from the value chain. A cathode producer receives payment for essentially the full copper content of its output, while a concentrate producer effectively shares a portion of the metal's value with downstream smelters. This distinction makes SX-EW cathode operations disproportionately valuable on a per-tonne-of-copper basis, a nuance that significantly influences the economics of the Chapi restart.

Historical Production and the Restart Baseline

From Active Operation to Care and Maintenance

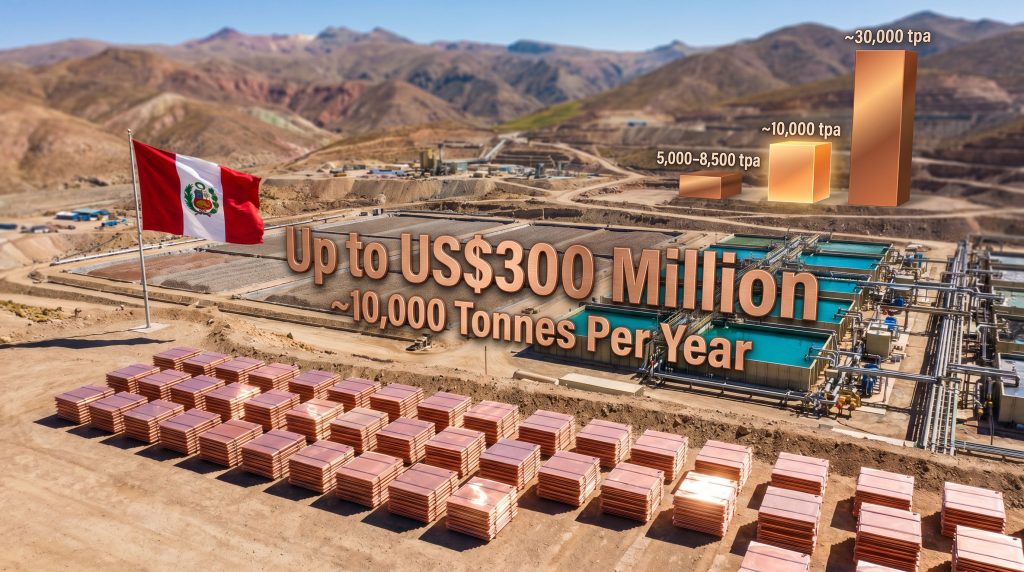

The Chapi mine operated between approximately 2006 and 2012, producing copper cathodes through its SX-EW processing circuit before being placed on care and maintenance status. During its active years, the mine generated an estimated 5,000 to 8,500 tonnes per year of copper cathode, with peak output occurring in the earlier years of operation before ore grade variability and declining copper prices compressed the operational economics of the asset.

The care and maintenance transition preserved the core processing infrastructure while suspending active production, effectively creating a time capsule of operational capacity that could be reactivated with targeted capital investment. However, care and maintenance status also introduces specific technical challenges at the point of reacquisition:

- Infrastructure deterioration: Processing equipment, pipelines, and electrical systems require systematic integrity assessments after extended inactivity

- Resource model currency: Geological data compiled prior to 2012 requires updating to reflect current reserve estimation standards and any post-operational geotechnical changes

- Metallurgical validation: Ore amenability to the existing leach circuit must be reconfirmed, as heap leach chemistry and reagent requirements can shift as ore characteristics evolve within the resource body

- Regulatory currency: Existing environmental authorisations require review and potentially amendment to reflect current Peruvian regulatory standards

What the Restart Targets Signal About the Asset's Potential

| Phase | Annual Copper Cathode Target | Key Infrastructure Focus |

|---|---|---|

| Initial Restart (Phase 1) | ~10,000 tonnes per year | SX-EW circuit rehabilitation |

| Expansion Scenario | Up to ~30,000 tonnes per year | New capital investment, expanded processing capacity |

| Historical Peak Output | 5,000 to 8,500 tpa (2006-2012) | Legacy processing infrastructure |

A critical and often overlooked insight embedded in this production table is that Quilla's initial restart target already exceeds Chapi's historical peak output. This is not a restoration exercise; it is a repositioning strategy. The plan assumes that modern SX-EW process improvements, updated metallurgical understanding, and optimised circuit design can push output beyond anything the asset previously achieved, even before the expansion-phase capital is deployed.

This implies that Quilla's technical team has identified specific efficiency improvements within the existing circuit configuration that were unavailable or unimplemented during the original operational period.

Industry engineers familiar with Peruvian oxide copper operations have observed that SX-EW technology and reagent chemistry have advanced considerably since the mid-2000s. Improvements in solvent selectivity, electrowinning cell design, and process control systems mean that rehabilitated circuits built to original 2005-era specifications can often achieve 10 to 20% higher copper recovery rates when upgraded with current-generation technology, without requiring a complete circuit replacement.

The SX-EW Processing Advantage: A Technical Deep Dive

Why the Processing Route Defines the Project's Economics

The copper leaching process at Chapi involves solvent extraction-electrowinning, a two-stage hydrometallurgical method that converts leached copper solutions into refined cathode metal through chemical separation and electrochemical deposition. Understanding how this process works illuminates why it is particularly well-suited to brownfield restart scenarios.

Stage 1: Heap Leaching

Oxide copper ore is crushed and stacked on lined leach pads, where dilute sulphuric acid solution is applied to dissolve copper minerals. The resulting copper-bearing solution (pregnant leach solution, or PLS) is collected at the base of the pad and directed to the SX plant.

Stage 2: Solvent Extraction

The PLS is contacted with an organic solvent that selectively extracts copper ions from solution, separating copper from impurities including iron, manganese, and other dissolved metals. This produces a purified copper electrolyte (advance electrolyte) and a barren aqueous raffinate that is recycled back to the heap.

Stage 3: Electrowinning

The purified copper electrolyte is passed through electrolytic cells where copper ions are deposited onto stainless steel or titanium blanks through electrochemical reduction. The resulting copper cathodes typically meet LME Grade A specifications (99.99% copper purity), enabling direct sale to fabricators and traders at the prevailing copper price without any downstream processing requirement.

The capital intensity advantage of SX-EW over sulphide concentrate operations is substantial. Concentrate operations require flotation circuits, filtration systems, and either on-site smelting or contractual smelter arrangements, all of which add capital and operating cost complexity. SX-EW produces a finished product at the mine gate, simplifying the value chain considerably.

Capital Investment Framework: Unpacking the US$300 Million Envelope

Phased Capital Deployment and What It Signals

The planned capital investment of up to US$300 million represents a phased commitment structure rather than a single upfront deployment, a structuring approach that carries significant strategic logic. Phase 1 capital targets rehabilitation of existing infrastructure to achieve the approximately 10,000 tpa restart baseline, while subsequent expansion-phase capital aims to roughly triple output toward the ~30,000 tpa scenario.

Comparing this capital envelope to peer brownfield projects in Peru's Andean copper space provides useful context for assessing its scale and ambition:

| Project Category | Typical Capex Range | Output Scale |

|---|---|---|

| Small brownfield SX-EW restart | US$20 to 80 million | 5,000 to 15,000 tpa |

| Mid-tier brownfield expansion | US$80 to 200 million | 15,000 to 40,000 tpa |

| Major brownfield/greenfield hybrid | US$200 to 500 million+ | 40,000 to 100,000+ tpa |

At up to US$300 million, Chapi's full investment plan positions it toward the upper boundary of mid-tier brownfield capital commitments in Andean copper, consistent with the ambition of reaching a ~30,000 tpa expansion scenario. The implied capital intensity of approximately US$10,000 per tonne of annual capacity at full expansion is competitive relative to comparable Peruvian oxide copper developments, where capital intensity figures of US$8,000 to US$15,000 per tonne are considered industry-standard.

Financing Pathways for Private Mining Investment

The structure of private mining investment at projects of this scale typically draws on several complementary financing mechanisms. For brownfield copper cathode operations with established infrastructure, the primary options include:

- Private equity and strategic investor structures: Common for projects requiring rapid mobilisation without the extended timelines associated with public equity markets

- Streaming and royalty financing: Metal streaming agreements allow producers to receive upfront capital in exchange for committing a portion of future copper cathode production at predetermined prices, providing non-dilutive financing

- Offtake-linked debt financing: Banks and commodity trading houses frequently provide debt financing secured against long-term offtake agreements, particularly for cathode producers whose output meets LME Grade A specifications

- Project finance structures: At the US$200 million-plus scale, project finance with ring-fenced asset structures becomes viable, allowing lenders to assess risk based on the project's specific cash flows rather than the parent company's balance sheet

The next major ASX story will hit our subscribers first

Production Timeline and Key Milestones

From Restart Confirmation to Expansion-Phase Production

Available project reporting indicates that Quilla had already reactivated cathode production at Chapi ahead of a full-scale ramp-up, with H1 2026 identified as the target window for initial copper cathode production commencement at meaningful scale. The pathway from that initial restart to the full expansion scenario involves a structured sequence of technical and regulatory milestones:

- Completion of an updated resource and reserve estimation meeting bankable feasibility-level confidence standards

- Metallurgical programme sign-off confirming ore amenability under current conditions

- Environmental and community permitting for the expanded operational scope

- Engineering, procurement, and construction (EPC) mobilisation for expanded processing capacity

- Commissioning and ramp-up to full expanded output

Brownfield SX-EW restarts in Peru have historically achieved nameplate capacity within 12 to 18 months of first pour, provided permitting and infrastructure rehabilitation are completed on schedule. This compressed timeline relative to greenfield development reflects the processing simplicity of the SX-EW route and the advantage of operating within existing infrastructure.

Risk Factors That Could Alter the Timeline

No production timeline in Peru's mining sector is without material risk factors. The key variables that could accelerate or delay Chapi's expansion programme include:

- Permitting environment: Peru's EIA amendment process, while faster than new applications, remains subject to bureaucratic variability and can be influenced by changing regulatory interpretations

- Community relations: The Moquegua and Arequipa departments have active community engagement requirements, and social licence maintenance demands continuous investment in local relationships

- Copper price sensitivity: The expansion-phase capital commitment is likely subject to copper price thresholds; a sustained decline below economically viable levels could defer Phase 2 deployment

- Metallurgical variability: Updated testwork on rehabilitated leach pad material may reveal recovery challenges not anticipated in the original restart assumptions

Strategic Implications for Peru's Mining Investment Landscape

Private Capital Recycling Into Dormant Peruvian Assets

The Chapi transaction is part of a discernible pattern across Latin American mining: major diversified companies are systematically divesting care-and-maintenance assets that fall below their minimum scale thresholds, while specialised operators with lower cost bases and higher tolerance for brownfield complexity are acquiring them at attractive entry prices. This capital recycling dynamic is creating a parallel tier of copper production growth, one that operates on shorter timelines and with lower capital requirements than the industry's headline greenfield projects.

Copper's Structural Demand Story and Its Influence on Project Economics

The long-term demand context that makes projects like Chapi economically viable extends well beyond near-term price cycles. Consequently, copper investment strategies are increasingly incorporating brownfield restart scenarios as a distinct asset class within portfolio construction. The structural drivers shaping copper consumption through the 2030s include:

- Electric vehicle penetration: Each battery electric vehicle requires approximately 83 kilograms of copper, roughly four times the copper content of an equivalent internal combustion engine vehicle

- Grid infrastructure investment: Transmission and distribution network upgrades required to support renewable energy integration are among the most copper-intensive categories of infrastructure spending

- Renewable energy generation: Wind turbines and solar installations require significantly more copper per unit of generating capacity than conventional thermal power plants

These demand drivers collectively suggest that the copper supply deficit projected by multiple industry forecasters will intensify through the late 2020s, creating a premium market environment precisely as Chapi's expansion-phase production is scheduled to come online.

What a Tripled Output Scenario Would Mean for the Region

A full expansion to approximately 30,000 tonnes per year of copper cathode would position Chapi among the more significant mid-tier copper producers in southern Peru. Furthermore, when compared to some of the largest copper mines globally, this scale underscores the strategic relevance of mid-tier brownfield operations within the broader supply picture. At that production scale, the operation would generate:

- Sustained direct employment across mining, processing, and logistics functions

- Local procurement demand for consumables including sulphuric acid, reagents, and maintenance services

- Royalty and tax revenue streams flowing to regional and national government accounts

- Infrastructure co-investment opportunities in road upgrades, power supply, and water management systems that benefit communities beyond the mine boundary

The combination of refined product output, regional economic contribution, and capital-efficient development pathway makes the Quilla Chapi copper production story in Peru one of the more instructive case studies in Andean brownfield development currently unfolding in the sector.

Frequently Asked Questions: Quilla Chapi Copper Production in Peru

What is the Quilla Chapi copper project?

Chapi is a brownfield copper mine located in southern Peru, approximately 50 kilometres south-southeast of Arequipa, spanning the Moquegua and Arequipa departments. Quilla Resources acquired the asset from Nexa Resources in late 2024 and is executing a restart and expansion strategy centred on the site's existing solvent extraction-electrowinning (SX-EW) processing infrastructure.

How much copper does Chapi aim to produce?

The initial restart phase targets approximately 10,000 tonnes per year of copper cathode, already exceeding the mine's historical peak output. A subsequent expansion programme supported by up to US$300 million in planned capital investment aims to triple that output level to approximately 30,000 tonnes per year.

When did Chapi previously operate?

The Chapi mine was in active production between approximately 2006 and 2012, generating an estimated 5,000 to 8,500 tonnes per year of copper cathode before being placed on care and maintenance.

What processing method does Chapi use?

Chapi employs a solvent extraction-electrowinning (SX-EW) circuit, processing oxide copper ores through heap leaching, chemical solvent extraction, and electrochemical deposition to produce LME Grade A copper cathodes (99.99% purity) directly on-site.

What are the key risks to Chapi's expansion timeline?

Primary risks include regulatory and permitting delays within Peru's environmental approval framework, community relations dynamics with local communities in the Moquegua and Arequipa departments, metallurgical variability in updated resource models, and copper price movements that could influence the timing and scale of expansion-phase capital deployment.

Why did Quilla acquire Chapi from Nexa?

Nexa's divestment reflected a portfolio rationalisation strategy focused on its zinc operations, while Quilla's acquisition aligned with a focused strategy of reactivating under-utilised copper assets in proven mining jurisdictions. The transaction gave Quilla access to a permitted, infrastructure-endowed asset with an established production history and substantial expansion optionality. For additional context on the royalty dimension of this asset, the Chapi royalty structure provides further background on the project's financial layering.

Disclaimer: Forward-looking statements regarding production timelines, capital deployment, and output targets involve inherent uncertainty. Actual outcomes may differ materially from projections due to operational, regulatory, market, and geological factors. This article does not constitute financial advice.

Want To Stay Ahead of the Next Major Copper Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper plays — and converting complex data into actionable investment insights for traders and investors at every experience level. Start your 14-day free trial at Discovery Alert today, or explore how historic mineral discoveries have generated exceptional returns to understand what early positioning in the right asset can mean for a portfolio.