July 19, 2026

The Processing Gap That Trade Statistics Cannot Capture

Most conversations about raw material dependency focus on import volumes and trade balances. But when it comes to rare earth elements, this framing misses the deeper structural reality. A country can hold vast underground reserves and still be comprehensively dependent on a foreign nation if it lacks the infrastructure to transform those reserves into usable industrial materials. This is precisely the situation India finds itself in today, and understanding why requires looking beyond headline import figures toward the full architecture of the rare earth supply chains.

Rare earth elements (REEs) are a group of 17 metallic elements critical to the functioning of modern industrial economies. Neodymium-iron-boron permanent magnets, which rely on REEs, are essential components in electric vehicle motors, wind turbine generators, military guidance systems, and consumer electronics. Without a reliable and sovereign supply of these materials, India's ambitions in electric mobility, defence self-sufficiency, and clean energy manufacturing face a structural ceiling.

When big ASX news breaks, our subscribers know first

How Deep Does India's Rare Earth Dependence on China Actually Run?

Layer One: The Raw Material Import Problem

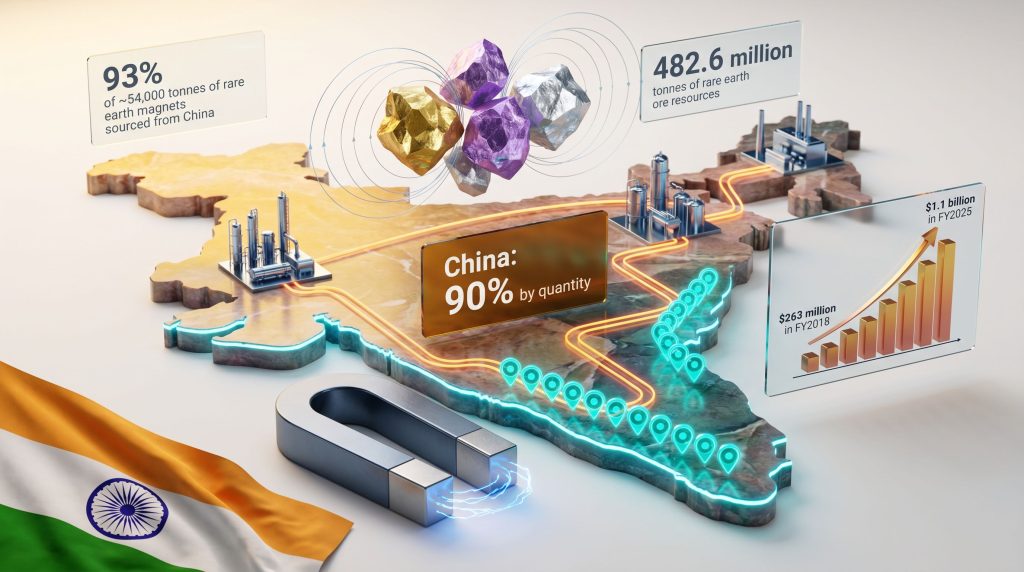

China supplied 81% of India's rare earth import value and approximately 90% by quantity in 2022, positioning India among the most exposed rare earth consumers globally. In FY2024-25, India imported close to 54,000 tonnes of rare earth permanent magnets, with an extraordinary 93% sourced from China. These numbers represent more than a trade imbalance. They reflect a fundamental absence of domestic processing and manufacturing capability.

What makes this particularly significant is that India is not a resource-poor nation. According to the Geological Survey of India, the country holds 482.6 million tonnes of rare earth ore resources, a reserve base substantial enough to support a meaningful domestic industry. Andhra Pradesh alone contains 211 million metric tonnes of beach sand mineral resources across 16 identified coastal deposits. The problem is not what lies underground. It is the near-total absence of industrial infrastructure capable of converting that ore into high-purity separated oxides and, ultimately, into permanent magnets.

Furthermore, India's dependence on China for rare earth and mining machinery has deepened considerably in recent years, compounding the structural vulnerabilities already embedded in the raw material import picture.

Layer Two: The Processing Machinery Dependency

A less-discussed dimension of India's vulnerability is its growing reliance on Chinese-manufactured processing and mining machinery. India's imports of rare earth and mining-linked equipment from China rose from $263 million in FY2018 to $1.1 billion in FY2025, while China's share of this import category expanded from 24.6% to 44.6% over the same period. Total rare earth and mining-linked machinery imports across all source countries reached $2.47 billion in FY2025.

This creates a secondary dependency loop that is often overlooked in policy discussions. Even if India were to build domestic mining operations using its own ore reserves, the processing equipment required to refine those materials would, under current conditions, likely still need to be sourced from China. Owning the ore is only the first step in a much longer industrial chain.

| Dependency Layer | Key Metric | China's Share |

|---|---|---|

| Rare Earth Import Value (2022) | Total REE imports | 81% |

| Rare Earth Import Quantity (2022) | Total REE imports | 90% |

| Rare Earth Magnets (FY2024-25) | ~54,000 tonnes imported | 93% |

| Mining/Processing Machinery (FY2025) | $1.1B sourced from China | 44.6% of total |

Layer Three: Downstream Magnet Manufacturing

Permanent magnets sit at the top of the rare earth value pyramid in terms of both technical complexity and strategic sensitivity. A country that imports finished magnets, rather than manufacturing them domestically, captures none of the value-added processing and remains entirely exposed to supply disruptions at the most critical stage of the chain. India's 93% dependence on Chinese magnets is not merely an economic inefficiency. It is a strategic chokepoint in the supply chains underpinning its most critical growth industries.

Why Replicating China's Rare Earth Infrastructure Is a Decade-Long Challenge

The Technical Barriers Are Formidable

Rare earth processing challenges are among the most technically demanding in all of industrial chemistry. The elements are chemically similar to one another, making selective separation extremely difficult. The dominant approach, solvent extraction using hydrometallurgical circuits, requires highly engineered facilities, precise reagent chemistry, and years of operational refinement to achieve the purity levels demanded by magnet manufacturers.

China built this capability over decades through sustained state investment, accepting significant environmental costs that stricter regulatory regimes in other countries would not permit. The result is that China currently processes an estimated 85-90% of the world's rare earth materials, regardless of where those materials were originally mined. This concentration is not simply a function of where rare earths are found in the ground. It reflects an enormous accumulated advantage in processing technology, skilled labour, and industrial infrastructure.

A country can mine its own rare earth ore and still ship it to China for processing, meaning resource sovereignty and supply chain sovereignty are two fundamentally different things.

The Solvent Extraction Knowledge Gap

One insight not widely appreciated outside specialist circles is that rare earth solvent extraction circuits are highly ore-specific. The chemical behaviour of REEs during separation varies depending on the mineralogy of the host deposit. Processes optimised for one ore type, such as bastnäsite-dominant deposits, do not transfer directly to other deposit types like laterites or beach sand monazite.

India's REE resources are predominantly associated with monazite-bearing beach sands, which present their own processing challenges, including the management of naturally occurring radioactive materials (NORM) such as thorium. This regulatory and technical complexity adds another layer of difficulty to India's path toward domestic processing capacity.

India's Policy Architecture: Building the Framework for Strategic Autonomy

The National Critical Mineral Mission and Budget Commitments

India's federal government has responded to these vulnerabilities with a multi-pronged policy framework. The National Critical Mineral Mission identifies rare earths as central to India's energy transition and defence manufacturing ambitions. Consequently, in February 2025, the federal budget designated four states for rare earth corridor development, encompassing the full value chain from mining through processing to magnet production.

This followed the federal government's approval of a ₹73 billion program to support rare earth magnet manufacturing, signalling that New Delhi views domestic magnet production capacity as a priority industrial target. The intersection of critical minerals and energy security has become a defining theme of India's industrial strategy, not merely an aspirational long-term goal.

Andhra Pradesh: The Most Advanced State-Level Push

Among the four identified corridor states, Andhra Pradesh has moved furthest in translating policy intent into concrete investment attraction. The state is targeting ₹500 billion ($5.2 billion) in rare earth and titanium-related investments over the next decade, with plans to issue tenders for rare earth processing facilities following cabinet approval of its rare earth corridor policy.

Capital-linked incentives are being structured to attract anchor investments, with additional benefits available for projects exceeding ₹10 billion in total investment value. The state's broader track record in investment attraction adds credibility to these ambitions. It has previously secured commitments from Google and ArcelorMittal Nippon Steel, and has set a broader target of $1 trillion in investment commitments by 2029.

India's Industrial Giants and the Private Sector Response

Approximately 10 companies have expressed interest in establishing rare earth processing facilities in Andhra Pradesh, with Reliance Industries, Vedanta, and Adani Enterprises among those that have signalled participation, according to sources with knowledge of the discussions. The involvement of India's largest industrial conglomerates reflects both the scale of capital required and the strategic significance attached to this sector.

| Company | Relevant Capabilities | Strategic Fit |

|---|---|---|

| Reliance Industries | Petrochemical processing, large-scale industrial infrastructure | Chemical separation and refining expertise |

| Vedanta | Base metals mining and smelting operations | Metallurgical processing know-how |

| Adani Enterprises | Port and logistics infrastructure, energy assets | Supply chain integration and distribution |

Each of these conglomerates brings complementary capabilities to the rare earth challenge. Reliance's deep experience in large-scale chemical processing makes it a credible candidate for hydrometallurgical separation. Vedanta's metallurgical expertise in base metals processing offers transferable skills. Adani's port and logistics infrastructure addresses a different but equally important bottleneck: the physical movement of ore and processed materials through the supply chain.

However, private capital alone will not be sufficient. Rare earth processing requires technology that India does not currently possess at industrial scale. Bridging this gap requires either technology transfer agreements with allied nations, joint ventures with established rare earth processors, or the acquisition of intellectual property from overseas operators. This is where international partnerships, particularly with Australia, Japan, and the United States, become critical enablers rather than optional supplements.

A Scenario Analysis: Three Pathways for India's Rare Earth Future

Scenario One: Accelerated Domestic Build-Out

Under optimistic conditions involving sustained federal funding, successful technology partnerships, and streamlined permitting for processing facilities, India could achieve meaningful rare earth processing independence within 10 to 15 years. This scenario requires corridor development to proceed on schedule, private investment commitments to convert into operational facilities, and technology transfer agreements to be concluded with allied nation partners.

Scenario Two: Partial Diversification Through Allied Supply Chains

The more probable medium-term trajectory involves India deepening raw material partnerships with Australia, Canada, and the United States, while domestic processing capacity develops incrementally. In addition, efforts to advance the rare earth supply chain buildout across allied nations are providing India with potential partnership frameworks it did not have access to a decade ago. Under this base case, Chinese machinery dependency persists through the late 2020s while domestic equipment manufacturing capability is gradually built. India's exposure to China narrows but is not eliminated by the early 2030s.

Scenario Three: Policy Fragmentation and Persistent Dependency

The downside scenario involves investment expressions of interest failing to convert into operational infrastructure, corridor policies stalling at the state level due to coordination failures, and technology transfer negotiations collapsing. In this outcome, India remains structurally dependent on China for refined materials and magnets well into the 2030s.

Securing ore reserves without simultaneously building processing infrastructure and achieving machinery independence will not reduce India's strategic vulnerability. It will simply shift the dependency from imported materials to domestically mined ore that still requires foreign equipment to refine.

The next major ASX story will hit our subscribers first

How India Compares Globally

| Country | Domestic REE Reserves | Processing Capacity | Key Policy Response |

|---|---|---|---|

| India | 482.6M tonnes (ore) | Minimal industrial scale | Critical Mineral Mission, REE corridors |

| United States | Moderate | Developing (MP Materials) | Defense Production Act, IRA incentives |

| Australia | Significant | Emerging (Lynas) | Critical Minerals Strategy, allied partnerships |

| European Union | Limited | Early-stage | Critical Raw Materials Act |

| Japan | Minimal | Advanced recycling | Long-term offtake contracts, recycling programs |

Japan's experience after China's rare earth export restrictions in 2010 offers the most instructive case study for India. Faced with sudden supply disruption, Japan pursued a multi-pronged response: long-term offtake agreements with overseas miners, aggressive investment in rare earth recycling from end-of-life electronics, and materials substitution research to reduce magnet REE content. India's industrial scale is far larger than Japan's, but the strategic logic of diversification, substitution, and recycling infrastructure applies equally.

Frequently Asked Questions: India's Rare Earth Dependence on China

Why is India so dependent on China for rare earths?

India's rare earth dependence on China stems primarily from a processing capability gap rather than a resource scarcity problem. While India holds substantial ore reserves, it lacks the hydrometallurgical infrastructure to separate rare earths to high-purity commercial grades. China built this processing dominance over decades and currently handles an estimated 85-90% of global rare earth refining. India historically underinvested in this sector, creating a structural reliance on Chinese processed materials and magnets that cannot be reversed quickly.

What rare earth resources does India actually hold?

India holds 482.6 million tonnes of rare earth ore resources according to the Geological Survey of India. Andhra Pradesh alone contains 211 million metric tonnes of beach sand mineral resources, including rare earths, across 16 identified coastal deposits. These resources are predominantly monazite-bearing, which presents specific processing challenges related to thorium content and radioactive material management, adding regulatory complexity to any domestic processing ambition.

What is India's National Critical Mineral Mission?

The National Critical Mineral Mission is India's overarching policy framework for securing supply chains for materials considered essential to energy transition and defence manufacturing. Rare earths feature prominently within this framework. The mission provides the policy architecture supporting rare earth corridor development, federal budget allocations for magnet manufacturing, and state-level investment attraction programs.

How long will it take India to reduce its rare earth dependence on China?

Under optimistic conditions, meaningful processing independence could be achievable within 10 to 15 years. Key milestones include corridor facility construction, technology transfer completion, and the commissioning of domestic magnet manufacturing at commercial scale. Under less favourable conditions, China exposure could persist beyond 2035. However, analysts exploring how India is reducing dependence on China suggest the policy momentum is more sustained now than at any prior point in the country's industrial history.

What are rare earth permanent magnets used for?

Rare earth permanent magnets, particularly neodymium-iron-boron types, are essential in electric vehicle drive motors, offshore and onshore wind turbine generators, military guidance and radar systems, industrial robotics, and consumer electronics including smartphones and hard drives. The permanent magnet segment represents the highest-value and most strategically sensitive end of the rare earth supply chain, which is why India's 93% dependence on Chinese-sourced magnets carries outsized strategic significance.

The Road Ahead: What India Must Execute Correctly

Three success factors will determine whether India's rare earth ambitions translate into genuine supply chain independence.

-

Processing Infrastructure Investment: Constructing domestic refining capacity specifically engineered for India's monazite-bearing ore types, reducing reliance on both imported refined materials and Chinese processing machinery.

-

Technology Partnerships: Securing rare earth separation and magnet manufacturing expertise through structured agreements with allied nations, particularly Australia, Japan, and the United States, where processing expertise is being actively developed.

-

Policy Continuity: Sustaining state-level corridor programs and federal funding commitments across political cycles, ensuring that the initiative builds cumulative momentum rather than cycling through policy starts and stops.

Key indicators worth monitoring include the annual growth rate of domestic rare earth processing volumes, the trajectory of China's share of magnet imports from the current 93% baseline, the number of operational corridor facilities commissioned, and the conversion rate from expressed investment interest to commissioned industrial capacity.

The machinery dependency problem deserves particular urgency. India risks constructing a rare earth processing industry that, while nominally domestic, remains reliant on Chinese capital equipment at every stage of the production process. Prioritising joint ventures with allied partners for the domestic manufacture of processing equipment would address this secondary vulnerability before it becomes as entrenched as the material dependency it is meant to replace.

This article is intended for informational purposes only and does not constitute financial advice or a solicitation to invest in any security or commodity. Readers should conduct their own independent research before making any investment decisions. Forward-looking statements and scenario analyses represent assessments of possible outcomes and should not be interpreted as predictions or guarantees of future performance.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts on significant mineral discoveries — including critical minerals and rare earths — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore why historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the broader market.