June 22, 2026

The Rare Earth Processing Bottleneck That Explains Everything

For decades, Western governments focused their critical minerals anxiety on mining — who controls the ore in the ground. What that framing missed was the far more consequential question of who controls what happens after mining. Rare earth elements must be cracked, separated, converted into metals, and then alloyed into functional materials before they can power a jet engine, spin a wind turbine, or drive a torpedo guidance system. Each of those steps requires a completely separate industrial infrastructure. Owning a mine without owning the downstream processing chain is, in strategic terms, roughly analogous to owning an oil field with no refinery access.

This processing gap is precisely what makes the Energy Fuels $725 million financing commitment from the US Office of Strategic Capital so structurally significant. It is not a mining subsidy. It is an attempt to fund the construction of an integrated industrial value chain that the Western world has largely ceded to a single geographic region over the past thirty years.

When big ASX news breaks, our subscribers know first

Understanding the Rare Earth Value Chain Before Evaluating the Commitment

Why Each Stage of the Value Chain Is a Separate Industrial Problem

Most coverage of the rare earth supply chain risk collapses several distinct industrial processes into a single undifferentiated category. This creates a fundamental misunderstanding of where the real vulnerabilities lie. The actual value chain has four meaningfully separate stages:

- Mining and concentration — extracting ore and producing a mineral concentrate or mixed rare earth carbonate

- Cracking and separation — using hydrometallurgical processes to separate individual rare earth elements from one another and produce rare earth oxides (REOs)

- Metals production — converting REOs into pure rare earth metals through molten salt electrolysis or other metallurgical techniques

- Alloy and magnet manufacturing — combining rare earth metals (particularly neodymium, praseodymium, dysprosium, and terbium) into neodymium-iron-boron (NdFeB) alloys and sintered permanent magnets

Western nations have made meaningful, if incomplete, progress at Stage 1. Stage 2 remains heavily concentrated outside allied-nation control. Stages 3 and 4 are almost entirely absent from the United States. Furthermore, the rare earth processing challenges at each stage are compounded by decades of underinvestment. The $725 million commitment is explicitly targeting Stages 2 and 3, which is precisely where the strategic value of the investment is concentrated.

Industry Context: Neodymium-iron-boron permanent magnets are the highest-performance commercially available magnet technology. A single direct-drive offshore wind turbine can require approximately two tonnes of NdFeB magnets. An F-35 fighter aircraft contains roughly 920 pounds of rare earth materials. The combination of defence and energy transition demand trajectories is creating a structural demand acceleration that upstream mining alone cannot resolve.

What the Energy Fuels $725 Million Financing Commitment Actually Consists Of

Financing Structure at a Glance

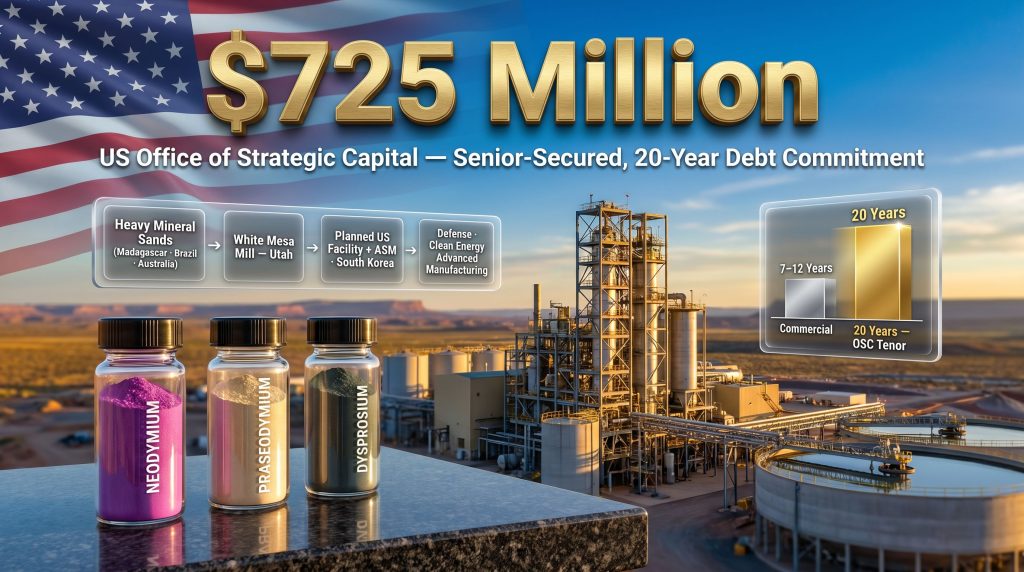

The Energy Fuels $725 million financing commitment was issued by the US Office of Strategic Capital (OSC), a body operating within the US Department of Defense with a mandate to deploy long-duration capital into strategically critical industrial sectors that private credit markets are structurally reluctant to finance at competitive terms. According to the official announcement, this conditional commitment marks a significant milestone in US domestic critical minerals strategy.

| Feature | Detail |

|---|---|

| Commitment Size | Up to $725 million |

| Instrument Type | Senior-secured debt |

| Tenor | 20 years |

| Issuing Body | US Office of Strategic Capital (OSC) |

| Status | Conditional — further due diligence required |

| Financial Advisor | Goldman Sachs & Co. LLC |

| Legal Counsel | Akin Gump Strauss Hauer & Feld LLP |

| Primary Use of Proceeds | White Mesa Mill REE expansion + planned US rare earth metals and alloys facility |

The 20-year tenor is one of the most analytically important features of this structure. Commercial project finance lenders in the mining and processing sector typically cap debt tenors at 7 to 12 years, and even reaching the upper end of that range generally requires substantial contracted revenue or offtake certainty. A 20-year government-backed senior-secured instrument fundamentally transforms the project economics, reducing annual debt service requirements and allowing capital to be deployed into infrastructure that takes years to reach full production capacity.

What "Conditional" Means in Practice

The commitment is not a binding loan agreement. Before capital is deployed, four categories of conditions must be resolved:

- Completion of further due diligence by the OSC

- Finalisation and execution of definitive financing documentation

- Satisfaction of customary closing conditions

- Receipt of applicable regulatory approvals

The engagement of Goldman Sachs as financial advisor and Akin Gump Strauss Hauer & Feld as legal counsel suggests that the documentation and closing process is already being pursued at an institutional level. These are not firms retained for preliminary or exploratory discussions. However, investors should monitor announcements relating to the completion of definitive documentation before drawing firm conclusions about the certainty of capital deployment.

⚠ Investor Caution: Conditional financing commitments, even those of this scale and with this advisory pedigree, carry execution risk. The commitment can lapse if conditions are not satisfied within agreed parameters. This article does not constitute financial advice. Readers should conduct their own own due diligence before making investment decisions.

The White Mesa Mill: A Regulatory Moat Decades in the Making

Why This Facility Is the Strategic Anchor of the Entire Plan

The White Mesa Mill in Utah is the only fully licensed and operating conventional uranium processing facility in the United States. That single sentence contains an enormous amount of embedded strategic value that is easy to underestimate.

Obtaining the licensing and permitting to construct a new conventional uranium and rare earth processing facility in the United States from scratch would require navigating the Nuclear Regulatory Commission's licensing framework, state-level environmental permitting, and National Environmental Policy Act review processes. The timeline for such an exercise, measured from initial application to operational approval, would likely run to a decade or more.

The mill already processes advanced rare earth element products alongside uranium concentrate. Its existing licensing, operational track record, and infrastructure position it as the logical hub for any large-scale US rare earth oxide separation expansion. Critically, the dual-commodity capability across uranium and rare earth elements creates a revenue diversification structure and operational flexibility that single-commodity processors simply cannot match.

This operational flexibility is not a minor operational nuance. It is a structural competitive advantage that would take a new entrant a decade and hundreds of millions of dollars to replicate. In addition, the Energy Fuels critical minerals strategy has been deliberately constructed around this facility as its central processing hub.

Mapping Energy Fuels' Four-Stage Vertical Integration Strategy

From Feedstock to Functional Alloys Across Four Countries

The $725 million financing commitment exists within a broader vertical integration architecture that Energy Fuels has been assembling across multiple jurisdictions. The strategy can be understood through four sequential stages:

Stage 1 — Mineral Feedstock Diversification

Heavy mineral sands projects spanning three continents provide feedstock diversity and reduce single-source supply risk:

- Vama Mada Project, Madagascar — 100%-owned, providing monazite-bearing mineral sands as rare earth feedstock

- Bahia Project, Brazil — 100%-owned, offering additional feedstock optionality in South America

- Donald Project, Australia — right to earn up to a 49% joint venture interest with Astron Limited, adding Australian mineral sands exposure

Monazite, the primary mineral in heavy mineral sands that carries rare earth content, is particularly rich in neodymium, praseodymium, and the heavy rare earths dysprosium and terbium. These four elements are the most demand-critical for permanent magnet production, making monazite-sourced feedstock strategically preferable to some alternative rare earth mineralisation types.

Stage 2 — Midstream Cracking and Separation

The White Mesa Mill serves as the central processing hub, converting mineral feedstocks into separated rare earth oxides. The expansion targeted under the OSC financing would substantially increase this separation capacity.

Stage 3 — Metals and Alloys Production

The planned acquisition of Australian Strategic Materials Limited (ASM), subject to ASM shareholder approval and other customary closing conditions, would add existing rare earth metal and alloy-making facilities in South Korea. These are operational facilities, not development-stage concepts, which is a critical distinction. Acquiring proven metallurgical expertise accelerates the path to producing finished rare earth metals and alloys by years compared to building that capability from zero in the United States.

Stage 4 — End-Market Supply

The integration target is the supply of domestically processed, fully traceable rare earth metals and alloys to US defence, clean energy, and advanced manufacturing sectors.

Strategic Scenario: If both the OSC financing and the ASM acquisition close on their current trajectories, Energy Fuels would control one of the most complete rare earth value chains outside of China, spanning mineral feedstock sourcing, oxide separation, metals production, and alloy manufacturing across operations in four countries.

The ASM Acquisition: Why South Korean Processing Expertise Matters

Bridging the Metals Gap Through Allied-Nation Manufacturing

One of the least-understood aspects of Western rare earth supply chain vulnerability is the near-complete absence of rare earth metals production capacity outside of Asia. The ability to convert a separated rare earth oxide into a pure metal, and then alloy that metal with iron and boron to produce a sinterable NdFeB powder, requires highly specialised pyrometallurgical and electrochemical expertise that has been concentrated in China and, to a lesser extent, Japan for decades.

ASM's facilities in South Korea represent an operational bridgehead in this capability gap. South Korea sits within the US allied-nation supply chain framework, meaning materials processed there can meet sourcing requirements for US defence procurement programmes under various domestic content and allied-supply preferences. This is an important commercial consideration for any company seeking to supply the US defence industrial base.

The interdependence between the $725 million OSC commitment and the ASM acquisition is explicit: the financing proceeds are targeted to fund both the White Mesa Mill expansion and the planned US rare earth metals and alloys facility, which would be built incorporating ASM's downstream expertise. If the ASM acquisition does not close, the downstream metals and alloys component of the strategy would need to be rebuilt organically, adding years and additional capital to the timeline.

The next major ASX story will hit our subscribers first

Benchmarking the OSC Instrument Against Other US Critical Minerals Financing Tools

A Comparative Framework for Government Capital Deployment

| Program | Administering Body | Typical Instrument | Strategic Focus |

|---|---|---|---|

| Office of Strategic Capital (OSC) | US Department of Defense | Long-tenor senior-secured debt | Defence-critical industrial capacity |

| Title XVII Loan Guarantees | US Department of Energy | Loan guarantees | Energy infrastructure and clean technology |

| DPA Title III | Department of Defense | Grants and offtake agreements | Near-term defence supply chain gaps |

| Export-Import Bank (EXIM) | Independent federal agency | Loans and guarantees | US export competitiveness |

The OSC instrument occupies a structurally distinct position in this landscape. Unlike Title XVII guarantees, which require the borrower to secure financing from commercial lenders with the government providing credit enhancement, OSC acts as the direct lender. Unlike DPA Title III grants, which target near-term supply gaps through smaller, faster-deploying instruments, the OSC's 20-year senior-secured loan is explicitly designed for large-scale infrastructure with long development and production timelines.

Furthermore, the broader context of US critical minerals production policy illustrates how the OSC instrument complements, rather than duplicates, existing government financing mechanisms. The combination of patient capital, direct lending, and senior-secured security structure creates a financing profile that has no real commercial market equivalent.

Three Structural Vulnerabilities the US Is Attempting to Address

The Geopolitical Architecture Behind the Investment Rationale

The OSC commitment does not exist in isolation. It reflects a broader US government recognition of three structural supply chain vulnerabilities that have accumulated over decades. Consequently, the critical minerals demand surge has amplified the urgency of addressing each one:

-

Processing concentration risk — The overwhelming majority of global rare earth separation capacity operates outside of allied-nation control. Even where Western nations have mining capacity, the ability to convert ores into usable separated elements has remained concentrated in ways that create single-point-of-failure risk for US defence and energy supply chains.

-

The metals and alloys gap — Mining and oxide production without downstream metals capability creates a partially de-risked supply chain that still depends on foreign conversion capacity. This gap renders upstream investment strategically incomplete until it is closed.

-

Demand acceleration without supply diversification — The simultaneous scaling of electric vehicle production, offshore wind development, and advanced defence electronics is driving rare earth demand at a pace that exceeds the growth rate of any credible Western supply alternative currently in development.

Heavy rare earths deserve particular attention in this context. Dysprosium and terbium are added to NdFeB alloys to maintain their magnetic properties at elevated temperatures, a requirement for most defence and automotive traction motor applications. These elements are produced in far smaller quantities than the light rare earths, and their production is even more geographically concentrated than the broader rare earth supply chain.

Key Risks Investors Should Monitor

Scenario Analysis: Three Potential Paths Forward

Scenario 1 — Full Execution

Both the OSC financing and ASM acquisition close broadly on their current timelines. White Mesa expansion proceeds to expanded REE processing capacity. The US metals and alloys facility commences construction. Energy Fuels establishes a vertically integrated domestic supply chain position that would be extraordinarily difficult for any competitor to replicate within a five-to-seven-year timeframe.

Scenario 2 — Partial Execution

The OSC financing closes but with modified terms or at a reduced commitment size. The ASM acquisition faces delays at the shareholder approval stage. White Mesa expansion proceeds on a longer timeline. Strategic positioning is preserved, but near-term production milestones are deferred by twelve to twenty-four months.

Scenario 3 — Execution Failure

Due diligence reveals unresolvable conditions. Definitive documentation is not completed. The ASM acquisition does not proceed. Energy Fuels retains its existing processing platform but loses the capital catalyst required for large-scale expansion.

Risk Factors to Track

- Completion status of definitive OSC financing documentation

- ASM shareholder vote timeline and outcome

- Regulatory approval timelines for the acquisition

- Rare earth oxide price movements, particularly for NdPr oxide, dysprosium, and terbium

- Shifts in US government capital deployment priorities

What a Successful US Rare Earth Supply Chain Would Mean for Critical Minerals Markets

Long-Term Market Implications Beyond the Single Transaction

If the Energy Fuels $725 million financing commitment closes and the integrated strategy executes at scale, the market-level implications extend well beyond a single company's balance sheet. Reuters reported that the loan pact represents one of the most significant US government interventions in domestic rare earth processing to date, underscoring the strategic weight behind the commitment.

-

Price discovery improvement: A credible, scaled non-Chinese supply alternative for separated rare earth oxides and refined metals could improve transparency in rare earth pricing, which currently lacks the exchange-traded benchmark infrastructure of base metals markets.

-

Demonstration effect for other critical minerals: A successful OSC-backed vertical integration in rare earths creates a replicable template for applying the same model to lithium conversion, cobalt refining, and manganese processing, all of which exhibit similar upstream mining versus downstream processing imbalances.

-

Procurement standards evolution: Allied-nation supply chain requirements for US government procurement are becoming increasingly specific about traceability and processing location, not just mining origin. A fully integrated, allied-nation-processed rare earth supply would meet requirements that a Chinese-processed product sourced from a Western mine cannot satisfy.

-

Competitive dynamics: The combination of White Mesa's existing regulatory moat, multi-continental feedstock diversity, and the planned downstream metals capability positions Energy Fuels as a multi-commodity critical materials company rather than a single-commodity miner. The uranium production capability provides a revenue foundation that pure-play rare earth developers lack entirely.

The broader implication for the critical minerals investment landscape is the emergence of government-backed long-tenor debt as a legitimate financing paradigm for industrial infrastructure that commercial capital markets have historically underserved. If this model proves executable, it fundamentally changes the risk-adjusted return calculus for large-scale rare earth processing infrastructure investment.

Further Exploration: Readers seeking additional institutional-grade analysis of the Energy Fuels $725 million financing commitment and the company's broader critical materials strategy can explore further coverage at Crux Investor, which provides in-depth mining and critical minerals research across the resource sector.

This article is for informational purposes only and does not constitute financial or investment advice. All forward-looking scenarios, projections, and market assessments involve inherent uncertainty. The Energy Fuels $725 million financing commitment remains conditional and subject to completion of due diligence and definitive documentation. Readers should conduct independent research before making investment decisions.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex mineral data into actionable insights for both short-term traders and long-term investors — explore historic examples of exceptional discovery returns to understand what's at stake, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.