June 7, 2026

The Processing Bottleneck Nobody Prepared For

Somewhere between a rare earth ore body and a functioning electric motor magnet lies one of the most consequential industrial gaps in the modern global economy. The chemistry is difficult, the infrastructure is scarce, and the expertise required took decades to accumulate. Understanding why rare earth processing outside China remains so stubbornly difficult requires looking past the headlines about mining discoveries and confronting the harder reality of what happens after ore leaves the ground.

The global conversation around rare earths has accelerated sharply, but much of it conflates extraction with production. Finding a deposit and converting it into commercially usable materials are fundamentally different problems, separated by years of technical development, capital investment, and chemical engineering. The world has plenty of the former challenge partially addressed. The latter remains largely unsolved.

When big ASX news breaks, our subscribers know first

China's Processing Monopoly Was Decades in the Making

China's dominance over rare earth processing did not emerge suddenly. It was constructed through deliberate, sustained policy over roughly 25 years, during which Western economies largely looked away. While China invested in separation facilities, refining infrastructure, and the accumulated technical expertise required to process rare earths at commercial scale, Western governments prioritised cheap imports over domestic capability.

The result is an asymmetry that is more extreme at the processing stage than at the mining stage. China accounts for approximately 70% of global rare earth mining but controls an estimated 90% of global processing and refining capacity. That gap between the two figures tells the real story: China's competitive advantage is not primarily about ore in the ground. It is about what happens to that ore afterward.

As Ivan Murphy, executive chairman of Hera Resources, explained at the One:1 Mining Investment Conference in London, the West essentially took Chinese rare earth supply for granted while the strategic dependency deepened. The recognition that this dependence had become a structural vulnerability arrived late, and the challenge now is not just finding alternative deposits but building entire processing and refining ecosystems outside China from close to a standing start. Furthermore, China's export restrictions have intensified the urgency of this task considerably.

Why Processing Dominance Is Harder to Reverse Than Mining Dominance

Mining a rare earth deposit requires capital, engineering, and logistics. Processing rare earths requires all of that plus highly specialised chemical knowledge, infrastructure purpose-built for chemically intensive separation, and decades of operational refinement. China's processing advantage compounds over time because it is rooted in accumulated expertise, amortised infrastructure, and regulatory environments that have historically tolerated environmentally intensive operations.

This structural stickiness means that even as new mining projects emerge across Australia, Brazil, the United States, and Africa, the processing bottleneck remains the rate-limiting factor. A mine without a processing pathway delivers ore. It does not deliver supply chain security. Consequently, the rare earth supply chains that Western governments are attempting to construct face this fundamental challenge at every stage.

Why Finding Rare Earths Does Not Solve the Supply Problem

The rare earth value chain breaks into four distinct stages: exploration, mining, separation and processing, and refining into commercially usable materials. Western policy attention has concentrated heavily on the first two stages. The latter two, which are where China's control is most absolute, have received comparatively less investment and less public understanding.

Key Insight: A rare earth deposit is only the starting point. The strategic chokepoint sits in chemical separation and downstream refining, where raw ore is converted into the oxides, alloys, and materials required for permanent magnets, motors, and electronics. China's dominance at these stages significantly exceeds its dominance in mining alone.

This distinction matters enormously for investors evaluating rare earth projects. A company announcing a large deposit is not necessarily announcing a supply chain solution. The critical questions are what happens after extraction, and whether the project has a credible, commercially proven pathway through separation, processing, and refining. According to reporting on global reserves, the distribution of known deposits is far broader than the distribution of processing capacity, which underscores the scale of the infrastructure gap.

The Basket Composition Problem: Why Grade Is the Wrong Metric?

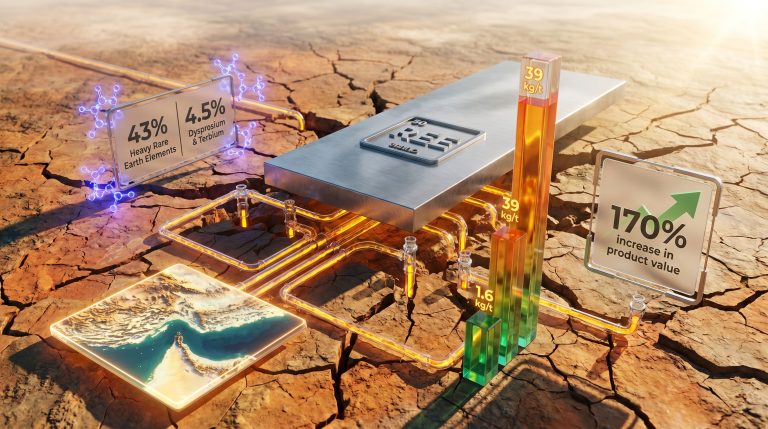

In gold mining, evaluation is relatively straightforward. Grade multiplied by spot price provides a workable proxy for project economics. The same logic applied to rare earth projects produces dangerously misleading conclusions. Rare earths are not a single commodity. They are a family of 17 elements with highly differentiated values, demand profiles, and processing requirements.

What matters in a rare earth project is not simply the total grade of rare earth oxides present in the ore. What matters is the end-concentrate basket: the specific mix of elements that the project will deliver after processing is complete. A project with a lower overall grade but a concentrate rich in neodymium, praseodymium, dysprosium, or terbium may be substantially more valuable than a higher-grade project dominated by cerium or lanthanum, which command significantly lower prices.

Murphy described this challenge directly at the conference, noting that grades alone do not reveal what the end concentrate will contain, whether it will be weighted toward magnet metals or lighter rare earths, or whether it will carry contaminants that undermine commercial viability entirely. This is the analytical trap that catches investors applying gold-project logic to rare earth assets.

Light Versus Heavy Rare Earths: Understanding the Value Hierarchy

The rare earth family divides broadly into two categories with very different strategic significance:

- Light rare earths (cerium, lanthanum, praseodymium, neodymium) are more abundant, more widely distributed, and generally lower in per-unit value, though neodymium and praseodymium are critical magnet metals

- Heavy rare earths (dysprosium, terbium, erbium, yttrium) are scarcer, more difficult to process, higher in value, and more strategically critical for high-performance permanent magnets used in defence, electric vehicles, and industrial motors

China's processing dominance is most acute in heavy rare earth refining. Even projects capable of producing concentrate today face a severely limited number of ex-China refining destinations for heavy rare earth material. This is the stage requiring the most urgent capital attention globally, and the rare earth processing challenges at the heavy end of the spectrum are particularly formidable.

Why Deposit Type Determines Everything

Not all rare earth projects face identical processing challenges. The type of geological deposit from which rare earths are extracted fundamentally shapes the processing pathway, timeline to production, capital requirements, and concentrate profile.

| Project Type | Processing Complexity | Typical Timeline to Production | Concentrate Profile |

|---|---|---|---|

| Hard Rock | High | 5 to 10+ years | Often light rare earth dominant |

| Ionic Clay | Moderate | 2 to 4 years | Higher proportion of magnet metals and heavy rare earths |

Ionic clay deposits offer a structurally faster and less chemically intensive processing pathway than hard rock alternatives. They also tend to deliver concentrate profiles weighted toward magnet metals, which are the rare earth sub-category in highest demand globally and the area of greatest ex-China supply shortage. Importantly, ionic clay deposits are the dominant deposit type in China's own producing regions, which partly explains China's accumulated expertise in processing this deposit type.

The strategic significance of ionic clay projects was reinforced by a high-profile acquisition in Brazil, where the Serro Verde ionic clay deposit was acquired for approximately $2.8 billion by a U.S.-aligned buyer. Murphy cited this transaction at the London conference as evidence that institutional capital is beginning to distinguish between project types rather than treating all rare earth assets equivalently. The Serro Verde deal signals that market participants are starting to price deposit type, processing pathway, and concentrate basket composition as primary valuation variables, not secondary considerations.

This does not mean hard rock projects lack merit. They will deliver production, but likely over longer timelines. In a supply chain environment defined by urgency, that timing difference carries real strategic and commercial weight.

Who Is Building Rare Earth Processing Capacity Outside China?

United States: Sovereign Speed as a Competitive Advantage

The United States has moved more decisively than any other Western economy in deploying capital toward rare earth processing capacity. The critical differentiator is the model of government participation. The U.S. International Development Finance Corporation (DFC) operates with a mandate that blends national security objectives with investment discipline, functioning with the analytical rigour of a private investment fund while pursuing strategic supply chain outcomes on behalf of the American government.

Murphy described this model approvingly, identifying the DFC's businesslike approach as a genuine innovation in sovereign investment. The combination of government mandate and commercial-speed decision making has enabled the U.S. to move into co-investment relationships with rare earth operators at a pace that European equivalents have not matched. America's rare earth supply chain development has consequently advanced more rapidly than comparable Western efforts.

MP Materials anchors U.S. rare earth production but faces a specific structural challenge: its concentrate output is weighted toward light rare earths, leaving a gap in the magnet metal and heavy rare earth categories that the American critical minerals strategy requires. Filling that gap requires sourcing heavy rare earth concentrate from projects outside China, creating both a commercial opportunity and a strategic imperative for ionic clay projects producing magnet-metal-weighted baskets.

Niron Magnetics represents a parallel technology hedge, developing permanent magnets that reduce or eliminate rare earth content. If commercialised at scale, this technology could structurally reduce demand pressure on certain rare earth elements, though the timeline and commercial viability of rare-earth-free magnet technology at industrial scale remain subjects of ongoing development.

Australia: The World's Largest Non-Chinese Rare Earth Producer

Lynas Rare Earths holds the most significant position in global ex-China rare earth supply. Its Mount Weld mine in Western Australia is among the highest-grade rare earth deposits on earth, and its Kuantan processing facility in Malaysia represents the single largest rare earth processing operation outside China. Lynas is also expanding into the United States, with a processing facility in Texas. Lynas became the first producer of heavy rare earths outside China, marking a pivotal milestone in the diversification of global supply.

The Lynas story is instructive in both directions. It demonstrates that world-class rare earth production outside China is achievable. It also illustrates the geographic concentration risk embedded in the current ex-China supply structure: a meaningful proportion of global non-Chinese rare earth processing relies on a single company operating a single major facility.

Brazil: The Reserve Giant Finding Its Moment

Brazil holds the world's second-largest rare earth reserves, and its ionic clay deposits are attracting significant institutional attention precisely because of their processing characteristics and concentrate profiles. The Serro Verde acquisition has repositioned Brazil as a strategic rare earth jurisdiction rather than a peripheral one, and subsequent development activity is expected as U.S. and European offtakers seek to secure non-Chinese feedstock.

The key question for Brazilian projects, as for all ex-China producers, is not whether the ore exists but where the concentrate will be refined. A confirmed refining pathway is what separates a project with strategic value from a project with strategic potential.

Europe: Policy Framework Without Matching Capital Velocity

The European Union's Critical Raw Materials Act establishes explicit targets for domestic sourcing and processing of strategic minerals, including rare earths. Existing processing operations, including facilities operated by Solvay and other European chemical players, represent meaningful but limited capacity. Expansion discussions are underway, and French operations in particular have been identified as candidates for scaling.

The honest assessment, however, is that Europe remains in the policy articulation phase while the United States has moved into active co-investment. Murphy was direct on this point at the conference: white papers and policy frameworks are necessary but insufficient. Capital deployment, at speed, is what translates strategic intent into processing infrastructure. The broader rare earth geopolitics at play here are reshaping how governments prioritise industrial strategy decisions.

Malaysia and Myanmar: Fragility Points in the Current System

Malaysia hosts Lynas's primary processing facility, making it the most consequential rare earth processing location outside China today. The concentration of ex-China processing capacity at a single site in a single country represents a systemic fragility that the broader supply chain diversification effort is supposed to address.

Myanmar has emerged as a significant, often underappreciated, source of medium and heavy rare earth feedstock, historically directed toward Chinese refiners. Political instability and supply disruptions in Myanmar have periodically introduced volatility into global heavy rare earth availability, illustrating that even China's processing dominance depends on geographically diverse feedstock inputs. This feedstock dependency is a vulnerability that Western supply chain planners should factor into scenario modelling.

A Due Diligence Framework for Rare Earth Investors

The critical minerals investment cycle is producing a volume of new projects far exceeding the number that will ultimately succeed. Applying rigorous project-level analysis rather than sector-level enthusiasm is the distinguishing characteristic of investors who will navigate this cycle well.

Murphy proposed a practical framework for separating genuinely viable rare earth projects from those that present well on headline metrics but collapse under detailed scrutiny:

Four-Question Rare Earth Due Diligence Framework:

- What deposit type is it? Hard rock or ionic clay determines the processing pathway, capital intensity, and realistic production timeline.

- What does the end-concentrate basket look like? Is the project's output weighted toward magnet metals and heavy rare earths, or dominated by lower-value light rare earths?

- Is the metallurgical separation pathway commercially proven? Has the project demonstrated that its specific ore chemistry can be separated at commercial scale, or does this remain an assumption?

- Where will the concentrate be refined, and is that capacity confirmed? A project without a named, credible refining destination is an incomplete investment thesis regardless of its geological credentials.

Murphy described visiting projects that appeared compelling on paper but revealed fundamental separation problems upon direct inspection, confirming that the metallurgical failure point is where many projects quietly collapse before they ever become a public headline.

Understanding the Critical Minerals Hierarchy

A definitional clarity issue compounds the difficulty of rare earth project evaluation. The term critical minerals encompasses 50 to 60 or more materials, including uranium, graphite, lithium, cobalt, and others. Rare earths are a specific subset of this broader category. Within rare earths, magnet metals (primarily neodymium, praseodymium, dysprosium, and terbium) represent the highest-demand, highest-strategic-value sub-category.

Investors conflating these layers of the hierarchy risk misallocating capital toward projects that qualify as critical minerals in a regulatory sense but do not address the specific processing bottlenecks that define the current geopolitical and commercial priority. Murphy specifically flagged this at the conference, noting that the critical minerals category now includes uranium and graphite and continues to expand, which is appropriate from a policy perspective but creates analytical noise for investors trying to identify rare earth-specific exposure.

Definitional Clarity: Critical minerals is a broad policy category. Rare earths are a subset. Magnet metals are a high-priority sub-category within rare earths. Investors should be clear about which layer of this hierarchy their capital is actually targeting.

The next major ASX story will hit our subscribers first

AI and Rare Earth Processing: A Feedback Loop With Strategic Implications

Artificial intelligence is beginning to reshape how rare earth projects are evaluated, developed, and optimised. At the exploration stage, AI tools are accelerating the interpretation of drilling data, compressing the time between field activity and resource estimation. At the processing stage, the impact may be even more significant.

Murphy described the practical application at the conference with notable clarity. Pilot plant operations, which are inherently iterative, involve constant adjustment of chemical processing variables to maximise concentrate quality and recovery rates. AI can run vastly more processing scenarios in parallel than human engineers can evaluate sequentially, identifying optimal configurations more rapidly and enabling faster convergence on commercially viable parameters.

The circular dimension of this relationship is worth noting. Rare earth magnets are essential components in the data centre infrastructure, robotics, and electric motors that underpin AI systems. AI is simultaneously being deployed to improve the efficiency of rare earth recovery. The technology depends on the material, and the material's recovery is being optimised by the technology. This feedback loop reinforces the structural long-term demand case for magnet metals independently of short-term pricing cycles.

Murphy observed that AI systems improve through iterative learning, and when applied to commercial processing scenarios, they begin generating novel suggestions for processing combinations that human operators might not have considered. Applied to ionic clay pilot plant operations, this could meaningfully compress the optimisation timeline and improve the commercial viability of projects earlier in their development trajectory.

What the Rare Earth Market Needs to Reach Competitive Scale Outside China

The primary constraint on expanding rare earth processing outside China is not technical capability. The expertise, the engineering knowledge, and the scientific understanding exist in Western economies. The constraint is capital volume and deployment speed.

Murphy was unambiguous on this point at the conference, identifying investment as the single most important accelerant for the sector. Three capital channels need to operate simultaneously for meaningful progress:

- Private investment in projects with proven metallurgy and confirmed basket composition

- Government co-investment in processing and refining infrastructure, following the DFC model of sovereign-backed commercial-speed deployment

- Offtake agreements that de-risk early-stage producers by confirming downstream demand before first production

The scenario analysis for when competitive ex-China rare earth processing capacity might reach meaningful scale depends critically on whether this capital trinity is assembled and sustained:

| Scenario | Conditions Required | Estimated Timeline |

|---|---|---|

| Incremental Progress | Current pace continues; ionic clay projects reach production | 3 to 5 years |

| Accelerated Build-Out | Sustained government co-investment; refining capacity expands in U.S. and EU | 5 to 7 years |

| Competitive Parity With China | Coordinated Western industrial policy; full value chain built ex-China | 10 to 15 years |

Murphy's own assessment at the conference pointed toward the 5 to 10-year range for significant improvement, contingent on the investment momentum of the past three years being maintained and extended.

The Language Shift That Changed Mining's Political Status

One underappreciated development in the rare earth investment landscape is the political reframing of mining itself. The addition of the word security to mineral has repositioned the sector in government and public perception. Mineral security now carries the same policy weight as energy security, which means mining activity is increasingly viewed through a national interest lens rather than an extractive industry lens.

This linguistic and conceptual shift has material consequences. It unlocks government support that would previously have been unavailable, reduces political friction for project permitting in aligned jurisdictions, and expands the pool of institutional capital that can justify rare earth investment on strategic grounds rather than purely financial ones. Projects operating in jurisdictions with supportive mining ministries and stable regulatory environments carry structural advantages that are difficult to quantify but very real in terms of development timeline.

The Shakeout Is Coming: How to Identify Projects That Will Survive

The current phase of the rare earth investment cycle shares characteristics with earlier momentum phases observed in gold, technology, and other sectors. Broad capital deployment across a wide range of projects is followed by consolidation, in which projects with real operational substance survive and those built primarily on narrative are repriced sharply downward.

Murphy was candid about this at the conference, describing the current environment as one where substantial capital is being deployed across many projects simultaneously, with the expectation that some will succeed and some will not. This is rational portfolio behaviour for large strategic investors. For individual project investors, however, it underscores the importance of distinguishing between genuine operational viability and exposure to a theme.

Projects likely to survive the consolidation phase share identifiable characteristics:

- Proven separation chemistry demonstrated at pilot scale or above

- End-concentrate basket composition confirmed as commercially valuable and aligned with current demand

- A named, credible refining destination or an active relationship with a refining-capable strategic partner

- Jurisdictional stability and in-country government engagement that supports rather than complicates development

- Alignment with government or strategic partner capital that reduces financing risk through the development timeline

Projects without these characteristics, regardless of their deposit size or headline grade, are structurally exposed in the consolidation phase that experienced observers like Murphy see as an inevitable feature of this investment cycle.

Frequently Asked Questions: Rare Earth Processing Outside China

What percentage of rare earth processing does China control?

China controls an estimated 90% of global rare earth processing and refining capacity, despite accounting for approximately 70% of global mining output. The processing gap is wider than the mining gap, which is why refining and separation infrastructure represents the most critical and most underfunded part of the ex-China supply chain development challenge.

What is the difference between light and heavy rare earths?

Light rare earths such as cerium, lanthanum, and neodymium are more abundant and generally lower in per-unit value. Heavy rare earths such as dysprosium and terbium are scarcer, more strategically significant, and used in high-performance permanent magnets. It is worth noting that the term magnet metals is more commercially precise than heavy rare earths as a category, since not all magnet metals are heavy rare earths and not all heavy rare earths are magnet metals.

Why are ionic clay deposits considered strategically important?

Ionic clay deposits offer a faster and less chemically intensive processing pathway than hard rock alternatives, with typical timelines to production of two to four years compared to five or more years for hard rock projects. They also tend to produce concentrate profiles weighted toward magnet metals, the rare earth category in highest demand. These two characteristics combined make ionic clay projects more competitive in the current supply chain urgency context.

Which countries are most advanced in building rare earth processing outside China?

As of 2025, Australia through Lynas Rare Earths, the United States through MP Materials and DFC-backed co-investment structures, and Brazil through emerging ionic clay projects including Serro Verde represent the most developed non-Chinese positions in the global rare earth processing landscape.

How long will it take to build a competitive ex-China rare earth market?

Industry participants estimate that five to ten years of sustained investment could produce a significantly more competitive ex-China rare earth processing market. Full competitive parity with China's integrated supply chain is a longer horizon objective, likely requiring ten to fifteen years under conditions of coordinated Western industrial policy and consistent capital deployment.

What is the biggest risk for rare earth investors right now?

The most significant risk is project-level misvaluation driven by applying commodity investment frameworks, particularly grade-based analysis borrowed from gold mining, to assets that require basket composition analysis, metallurgical separation assessment, and confirmed refining pathway evaluation. The consolidation phase that follows sector momentum cycles is likely to disproportionately affect projects that have not demonstrated operational viability beyond headline metrics.

Key Takeaways: The State of Rare Earth Processing Outside China in 2025

- China's dominance in processing and refining (approximately 90%) significantly exceeds its mining dominance (approximately 70%), and the processing gap is the more strategically urgent problem

- Deposit type determines viability: ionic clay projects offer faster timelines, lower processing complexity, and magnet-metal-weighted concentrate profiles compared to hard rock alternatives

- The refining bottleneck is the most acute gap in the ex-China supply chain: concentrate without a confirmed refining destination has limited commercial value regardless of deposit quality

- The U.S. DFC co-investment model represents the most replicable template for deploying sovereign capital at commercial speed in the rare earth sector

- Australia, Brazil, the United States, and parts of Europe are the most advanced non-Chinese positions, but none approaches offsetting China's integrated processing capability at current scale

- AI-assisted metallurgical optimisation is emerging as a meaningful efficiency accelerator, particularly for ionic clay pilot plant operations seeking to maximise concentrate value

- Investors should apply deposit type, basket composition, separation viability, and refining pathway analysis rather than grade-based frameworks when evaluating rare earth projects

- The investment cycle is approaching a consolidation phase: projects with proven processing pathways, confirmed basket value, and strategic partner relationships are structurally better positioned to survive it

- Rare earths are a specific subset of the broader critical minerals category: investors should understand precisely which layer of the critical minerals hierarchy their capital is targeting

This article contains forward-looking statements and market analysis based on publicly available information and industry commentary. It does not constitute financial advice. Readers should conduct their own due diligence before making any investment decisions. Statements regarding timelines, production capacity, acquisition values, and market forecasts are subject to change and should be independently verified.

Want to Identify the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across rare earths and other critical commodities, instantly translating complex geological data into actionable investment insights — so subscribers can act before the broader market catches on. Explore how historic discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself at the forefront of the next major find.