June 27, 2026

Why Rare Earth Recycling Has Become One of the Most Strategically Charged Industrial Challenges of the Decade

The supply chain for permanent magnets has quietly become one of the most geopolitically sensitive material flows on the planet. Long before electric vehicles became mainstream consumer products, engineers understood that neodymium-iron-boron (NdFeB) magnets were irreplaceable in high-performance motor design. What was not fully appreciated until recently was how catastrophically concentrated the processing infrastructure for these materials had become, and what that concentration would mean for Western industrial policy in the 2020s.

Understanding the Ionic Rare Earths recycled rare earth loop requires starting not with the company itself, but with the structural problem it is attempting to solve — a problem rooted in decades of underinvestment in Western rare earth processing capacity and an accelerating demand trajectory that primary mining alone cannot satisfy.

When big ASX news breaks, our subscribers know first

The Structural Vulnerability at the Heart of the EV Supply Chain

China currently controls approximately 90% of global rare earth refining capacity, a figure that places virtually every Western electric vehicle manufacturer, wind turbine producer, and defence contractor in a position of material dependency on a single geopolitical actor. This is not a temporary market condition — it reflects sustained, decades-long investment in separation and processing infrastructure that Western nations largely failed to replicate after stepping back from rare earth production in the 1990s.

The four elements at the centre of this dependency are neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). These are not interchangeable or easily substituted. Each plays a distinct role in the magnetic performance of NdFeB permanent magnets:

- Neodymium and praseodymium form the structural backbone of the NdFeB alloy, determining base magnetic strength

- Dysprosium is added to increase coercivity — the magnet's resistance to demagnetisation at elevated operating temperatures

- Terbium enhances this high-temperature performance further, often used in combination with dysprosium in automotive motor grades

- Together, these four elements account for roughly 80% of the total economic value embedded in a finished rare earth magnet

The policy response from Western governments has materialised primarily through regulatory frameworks rather than direct industrial intervention. The EU Critical Raw Materials Act establishes a binding benchmark requiring that at least 15% of annual rare earth consumption be sourced from recycled material by 2030. This is not an aspirational target — manufacturers and material processors operating within European supply chains must plan around this obligation today, making long-loop rare earth recycling capacity a commercial necessity rather than an environmental preference.

Furthermore, the broader context of rare earth supply chains underscores just how fragile Western procurement positions have become. Understanding China's rare earth export restrictions adds critical context to why circular processing models have moved from niche innovation to strategic imperative.

Recycling rare earths is not simply an environmental upgrade to an existing supply chain. It is a structural response to a geopolitical exposure that no amount of new primary mining in the West can fully address within the required timeframe.

Short-Loop vs Long-Loop: Why the Distinction Matters More Than Most Investors Realise

A nuance that is frequently misunderstood in public discussion of rare earth recycling is the difference between short-loop and long-loop recovery models. These are not simply variations in processing intensity — they represent fundamentally different value propositions with very different strategic implications.

| Recycling Model | Primary Output | Feedstock Requirement | End-Use Flexibility | Purity Level |

|---|---|---|---|---|

| Short-Loop | Mixed alloy or oxide blend | Pre-sorted, clean magnet scrap | Low — magnet sector only | Moderate |

| Long-Loop | Individually separated REOs | Mixed or contaminated scrap | High — any rare earth sector | Greater than 99.9% |

Short-loop recycling is essentially a magnet-to-magnet process. It can recover material efficiently from clean, sorted scrap but cannot direct that material toward defence electronics, wind energy, or any application outside of magnet manufacturing. Its feedstock sensitivity is also a significant operational constraint — mixed or contaminated scrap streams cannot be easily processed without prior sorting.

Long-loop recycling, by contrast, separates individual rare earth elements into high-purity oxide form. This means the output is functionally equivalent to primary mined and refined material, and it can be directed to any downstream rare earth consumer regardless of sector. From a sovereign supply chain perspective, this flexibility is enormously valuable. A long-loop processor is not dependent on a single off-take market — it produces a commodity that multiple industries must compete to secure.

How the Ionic Technologies Hydrometallurgical Process Works

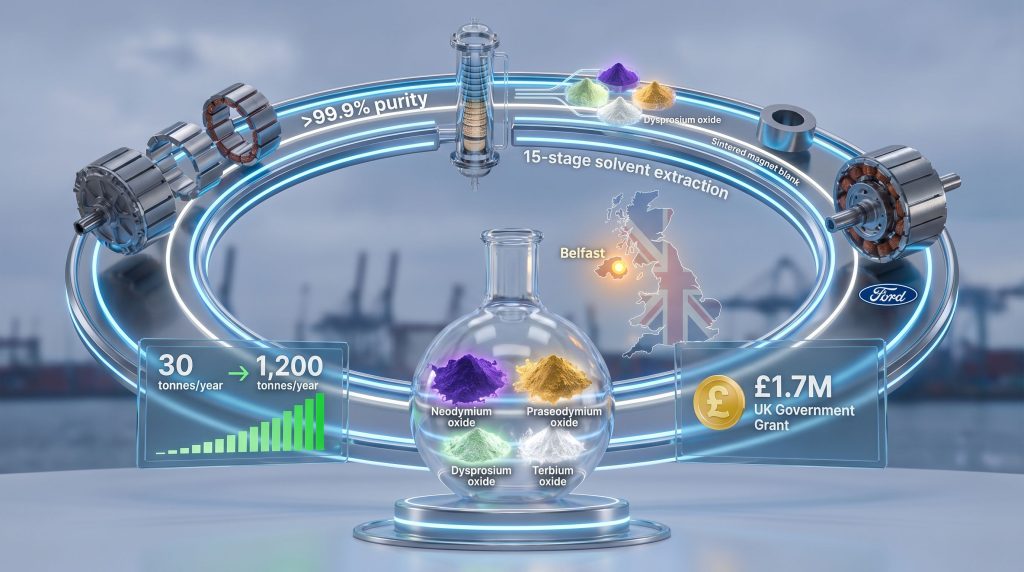

Ionic Rare Earths Limited (ASX: IXR) operates its recycling technology through its wholly owned subsidiary, Ionic Technologies, headquartered in Belfast, Northern Ireland. The core of the operation is a patented hydrometallurgical separation system developed in collaboration with Queen's University Belfast — an academic partnership that has grounded the technology in peer-reviewed materials science rather than purely commercial development.

The process centres on a 15-stage solvent extraction sequence that progressively isolates individual rare earth elements from dissolved magnet material. Solvent extraction at this stage count is not unusual in primary rare earth refining, but applying it successfully to recycled feedstock — which is chemically heterogeneous and often contaminated with iron, boron, and coating materials — represents a meaningful technical achievement.

What Makes the Process Particularly Significant for Commercial Scaling?

- It is genuinely feedstock-agnostic, accepting mixed magnet scrap from multiple waste streams without requiring pre-sorting or high-grade input selection

- The dissolution and separation steps are conducted under conditions that generate minimal hazardous waste, avoiding the high-temperature slag and emissions associated with pyrometallurgical alternatives

- The process produces four individually separated rare earth oxides at purities exceeding 99.9%, which is the standard threshold for direct substitution into magnet alloy manufacturing

Separated output products from the process:

- Neodymium oxide (Nd₂O₃)

- Praseodymium oxide (Pr₆O₁₁)

- Dysprosium oxide (Dy₂O₃)

- Terbium oxide (Tb₄O₇)

An important and often overlooked technical distinction here is that achieving greater than 99.9% individual oxide purity from recycled feedstock is considerably more challenging than achieving the same purity from primary ore. Primary ore processing begins with a relatively predictable chemical input. Recycled magnet scrap, however, is chemically complex, variable in composition, and contaminated with non-rare earth elements that must be completely separated before the solvent extraction stages can operate at design efficiency.

Belfast: From Proof of Concept to Commercial Node

The Belfast demonstration facility achieved operational status in 2023, making it the first plant in the United Kingdom capable of producing individually separated, high-purity rare earth oxides from recycled magnet material. Its current design capacity stands at 30 tonnes per year of magnet scrap input, generating in excess of 10 tonnes of separated rare earth oxides annually.

The facility received a £1.7 million UK government grant in recognition of its strategic industrial significance. This funding reflects the UK government's broader interest in developing domestic critical mineral processing capability — a priority that aligns closely with the wider push for critical raw materials transition across the industrialised West.

The commercial plant under development at Belfast Harbour represents a step-change in ambition:

| Facility | Scrap Input Capacity | Separated REO Output |

|---|---|---|

| Belfast Demonstration Plant (operational) | 30 tonnes per year | Greater than 10 tonnes per year |

| Belfast Harbour Commercial Plant (planned) | 1,200 tonnes per year | Approximately 400 tonnes per year |

| Scale Multiplier | 40x increase | 40x increase |

Moving from 30 tonnes per year to 1,200 tonnes per year is not simply a capacity increase — it is a transformation of Belfast's role within the Western rare earth supply chain. At 400 tonnes of separated REOs annually, the commercial plant would represent a genuinely material contribution to European critical mineral processing capacity, particularly given how little long-loop recycling infrastructure currently exists outside of China.

The Ford EV Rotor: A Commercial Threshold, Not Just a Technical Milestone

The practical significance of the Ionic Rare Earths recycled rare earth loop became concrete with the production and assessment of a Ford electric vehicle rotor built entirely from rare earth material derived from recycled sources. This rotor was assessed as performing at a level comparable to rotors manufactured from virgin mined rare earth inputs — a finding that carries substantial commercial weight.

To understand why this matters, it helps to trace the value chain that produced this component:

- End-of-life magnet collection — NdFeB scrap sourced from decommissioned motors, wind turbine generators, and manufacturing waste

- Hydrometallurgical separation — Ionic Technologies' 15-stage solvent extraction process isolates individual high-purity REOs from the mixed scrap feedstock

- Alloy and sintering production — Separated oxides are converted into NdFeB alloy and sintered into magnet blanks by specialist magnet manufacturers

- Rotor assembly — Finished sintered magnets are assembled into EV motor rotor configurations by automotive component suppliers

- Performance validation — The completed rotor undergoes assessment against OEM specifications, with results indicating performance parity with virgin-material rotors

This sequence represents a fully closed industrial loop, and the performance equivalence finding is the critical commercial data point. OEM procurement decisions are governed by specification compliance, not supply chain philosophy. The demonstration that recycled rare earth material can meet the same technical standards as primary-sourced material removes the most significant barrier to circular supply chain adoption at scale.

When recycled material is validated as performing at the same level as virgin product, the conversation shifts from whether circular supply chains are feasible to when they will become the standard procurement approach.

The next major ASX story will hit our subscribers first

Comparing Recycling Technologies: Where Hydrometallurgical Separation Fits

Rare earth recycling is not a single technology — it is a family of approaches with very different cost, purity, and flexibility profiles. Understanding where solvent extraction-based long-loop processing sits within this landscape is essential for evaluating its commercial positioning.

| Approach | REE Recovery Rate | Output Purity | Feedstock Flexibility | Environmental Profile | Strategic Utility |

|---|---|---|---|---|---|

| Hydrometallurgical solvent extraction (long-loop) | High | Greater than 99.9% individual REOs | High | Minimal waste | Very High |

| HCl closed-loop acid leaching | Approximately 97% | Mixed or separated | Moderate | Acid waste management required | Moderate-High |

| Pyrometallurgical re-melt (short-loop) | Moderate | Mixed alloy | Low | Slag and emissions | Low |

| Direct magnet-to-magnet reprocessing | High (clean scrap only) | Alloy grade | Very Low | Minimal | Low |

Academic research published in peer-reviewed materials science literature confirms that hydrometallurgical approaches can achieve high REE recovery rates from NdFeB scrap at technically viable scales. The distinguishing competitive advantage of the Ionic Technologies process lies in combining three attributes that most competing approaches cannot simultaneously deliver: high individual oxide purity, feedstock agnosticism, and a low environmental impact profile.

A less commonly discussed aspect of pyrometallurgical short-loop recycling is that it tends to concentrate heavy rare earth elements — dysprosium and terbium in particular — within slag phases that are difficult and expensive to recover. Consequently, short-loop processes can actually destroy value in the highest-priced components of the magnet composition, even whilst efficiently recovering the bulk neodymium and praseodymium fractions.

The Investment Logic: Feedstock Curves, Policy Pull, and Geographic Hedging

From an investor perspective, the commercial thesis for long-loop rare earth recycling rests on three converging structural forces rather than any single catalyst.

1. Growing Feedstock Availability Through the 2030s

The volume of end-of-life NdFeB magnets available for recycling is directly linked to the adoption curve of EVs and wind turbines from the previous decade. First-generation electric vehicles sold between 2015 and 2022 are now approaching end-of-service life, and the magnets within their motors are entering the waste stream in increasing quantities. This creates a growing feedstock availability curve that will accelerate through the late 2020s and into the 2030s, aligning with the ramp-up timeline for commercial recycling infrastructure.

2. Mandatory Demand Pull From EU Regulatory Requirements

The EU Critical Raw Materials Act's 15% recycling mandate by 2030 creates structural commercial demand that does not depend on spot price dynamics or voluntary corporate sustainability commitments. Manufacturers operating within European supply chains face a compliance obligation, meaning certified recycled REO supply will command a premium over uncertified primary material in regulated procurement contexts.

3. Geopolitical Price Volatility in Virgin Rare Earth Supply

Primary rare earth prices are subject to export control decisions, quota changes, and processing restrictions in China that Western buyers cannot anticipate or control. Domestically produced recycled REOs provide a price-stable alternative for procurement teams seeking to reduce supply chain exposure — a value proposition that strengthens rather than diminishes during periods of geopolitical tension. The rare earth processing challenges associated with primary refining further reinforce the case for building domestic recycling capacity.

Beyond the UK operation, Ionic Rare Earths is also advancing a joint venture with Viridis Mining in Brazil, centred on the Colossus REE project. This dual-geography strategy — combining primary extraction in Brazil with recycling infrastructure in the UK — creates a dual-source supply model that hedges against feedstock scarcity risk in the early commercial years when recycled magnet volumes are still building. Furthermore, this approach to rare earth supply chain buildout reflects a structurally sensible hedge: if end-of-life magnet availability proves slower to materialise than projected, primary ore can supplement the feedstock base without requiring a fundamental change to the processing technology.

Critical Milestones That Will Define the Commercial Trajectory

Investors and industry observers tracking the development of the Ionic Rare Earths recycled rare earth loop should monitor several distinct inflection points over the coming years:

- Belfast Harbour commercial plant progression from feasibility study through engineering design, permitting, and construction represents the most significant near-term value inflection point

- Expansion of OEM partnerships beyond the Ford proof-of-concept is critical — automotive and wind energy manufacturers adopting recycled REO specifications at volume would validate the supply chain at commercially meaningful scale

- EU 2030 recycling mandate approach will progressively intensify demand for certified recycled REO supply, rewarding processing infrastructure that achieves commercial-scale certification earliest

- Colossus JV advancement in Brazil provides a feedstock optionality pathway that strengthens the overall supply architecture

- Feedstock partnership agreements with EV manufacturers, motor recyclers, and wind turbine operators will determine how quickly the commercial plant can access sufficient scrap volumes to operate at design capacity

Frequently Asked Questions

What Rare Earth Elements Does the Ionic Technologies Recycling Process Recover?

The process separates neodymium, praseodymium, dysprosium, and terbium into individual high-purity oxides exceeding 99.9% purity. These four elements represent the primary value-bearing components of NdFeB permanent magnets and together account for approximately 80% of the economic value embedded in finished magnet material.

Why Is Long-Loop Recycling Strategically Superior to Short-Loop Approaches?

Long-loop processing produces individually separated rare earth oxides that can be directed to any downstream sector — EV motors, defence electronics, wind turbines, and advanced manufacturing. Short-loop recycling, however, produces mixed alloys or oxide blends that can only re-enter magnet production, creating a single-sector dependency that limits strategic value. Long-loop also handles mixed and contaminated feedstock more effectively.

How Significant Is the Belfast Harbour Commercial Plant Target?

At 1,200 tonnes of magnet scrap input per year and approximately 400 tonnes of separated REOs annually, the planned commercial facility would represent a 40-fold scale increase over the existing demonstration plant. This would position Belfast as one of the most significant rare earth processing nodes in the Western world outside of primary mining jurisdictions.

What Does the Ford EV Rotor Result Mean for the Broader Recycling Industry?

It establishes a validated proof of performance equivalence between recycled and virgin rare earth material at OEM specification level. This is the primary technical barrier to circular supply chain adoption at scale, and its removal opens the door for automotive procurement teams to consider recycled REO sources as compliant alternatives to primary-mined supply.

How Does EU Policy Create Commercial Demand for Recycled Rare Earths?

The EU Critical Raw Materials Act mandates that 15% of annual rare earth consumption within European supply chains be sourced from recycled material by 2030. This is a binding regulatory requirement, not a voluntary target, meaning manufacturers face compliance obligations that translate directly into structural commercial demand for certified recycled REO supply.

This article is intended for informational purposes only and does not constitute financial advice. Statements regarding future projects, production targets, commercial plant development timelines, and market trajectories involve forward-looking elements that are subject to material risks and uncertainties. Readers should conduct independent due diligence and consider their personal circumstances before making any investment decisions. Past performance of supply chain milestones or demonstration plant results is not necessarily indicative of future commercial outcomes.

Want to Know When the Next Major Rare Earth Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant rare earth and critical mineral discoveries before the broader market reacts — explore historic discoveries and their returns to understand what early positioning can mean, then begin your 14-day free trial at Discovery Alert to stay ahead of the next major find.