June 16, 2026

The Hidden Geometry of Rare Earth Supply Chains: Why Geography Is Becoming Destiny

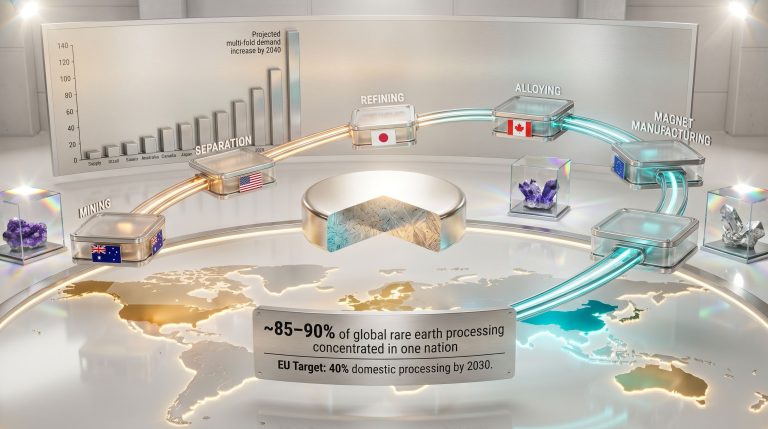

The physics of the global energy transition are deceptively simple on the surface: build more electric vehicles, install more wind turbines, manufacture more defence electronics. The geopolitics underneath, however, are anything but. Every permanent magnet motor in an EV drivetrain requires neodymium, praseodymium, and often dysprosium. Every wind turbine generator depends on the same narrow basket of elements. And today, the overwhelming majority of those elements are processed in a single country.

That concentration risk is now the defining anxiety of Western industrial policy, and it is redirecting capital at a speed rarely seen in the mining sector. Brazil, long celebrated for its iron ore and copper wealth but largely overlooked as a rare earth jurisdiction, is increasingly positioned at the centre of this realignment. The Resouro rare earths and titanium investment in Brazil story is not simply a company narrative; it is a lens through which the broader structural transformation of rare earth supply chains becomes legible.

When big ASX news breaks, our subscribers know first

Brazil's Rare Earth Endowment: Bigger Than Most Investors Realise

Brazil's geological wealth in rare earth elements is frequently underestimated in market discourse. Depending on the measurement methodology applied, the country holds either the second or third largest rare earth reserves on the planet, according to the US Geological Survey. Despite this, Brazil has historically occupied a marginal position in global REE production, exporting unprocessed or semi-processed feedstock rather than capturing meaningful value further along the chain.

Titanium is a parallel story. Brazil's titanium mineral resources, particularly ilmenite and rutile, are among the most significant globally, yet the country has rarely been framed as a titanium powerhouse in the same breath as Australia or South Africa. This dual endowment of rare earths and titanium in the same geological province creates a commodity combination that is genuinely uncommon at the scale found in Brazil's interior.

Brazil's 2026 critical minerals strategic framework formally designates rare earth elements and titanium as priority minerals under national development policy. This framework has included an active cataloguing of development-stage projects, with the Tiros project operated by Resouro Strategic Metals appearing in official project tables. It is important to note that inclusion in a government catalogue reflects policy recognition rather than confirmed project-specific funding, accelerated permitting, or official financial backing, none of which has been explicitly confirmed in public ASX disclosures.

Why the Tiros Deposit Defies Easy Comparison

Most rare earth development projects globally are single-commodity propositions. They carry rare earth mineralisation, often of a specific deposit type, and their economics live or die on REE prices and processing costs alone. Tiros breaks from this template in two significant ways: its scale and its dual-commodity structure.

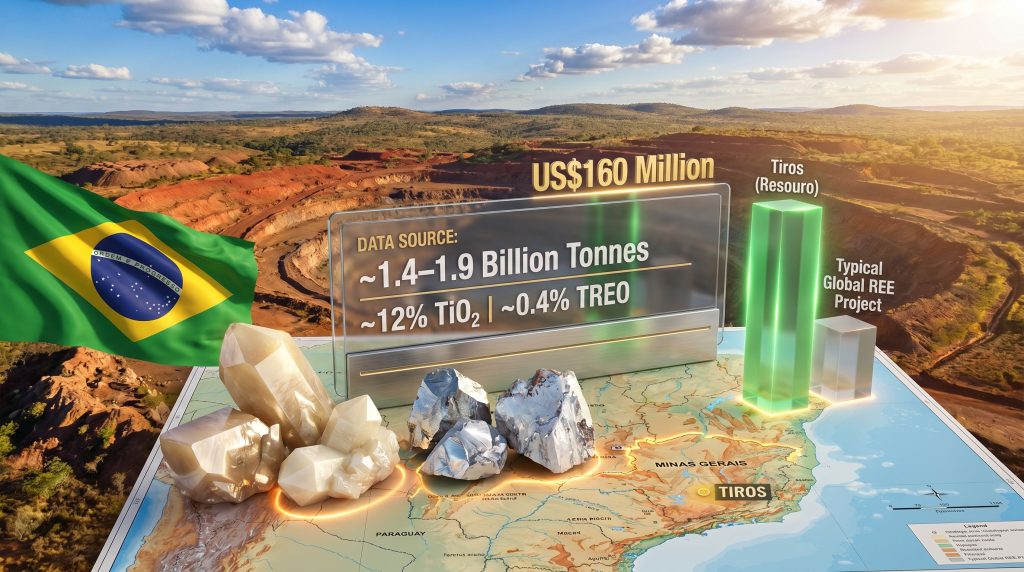

Resource estimates for the Tiros deposit range from approximately 1.4 to 1.9 billion tonnes, placing it among the largest undeveloped rare earth and titanium accumulations anywhere in the world. Average grades across the broader resource are estimated at approximately 0.4% Total Rare Earth Oxide (TREO) and ~12% TiO₂. These figures are not exceptional by grade standards alone, but the sheer tonnage transforms them into an extraordinary contained-metal inventory.

Perhaps more strategically significant is the delineation of a near-surface high-grade zone of approximately 130 million tonnes grading ~23% TiO₂ and ~9,100 parts per million TREO. In development economics, near-surface mineralisation at elevated grades is not merely a geological bonus; it represents a potential low-strip-ratio entry point that can dramatically reduce the capital intensity required to generate first revenue.

| Metric | Tiros (Resouro) | Typical Global REE Development Project |

|---|---|---|

| Total Resource Estimate | ~1.4 to 1.9 billion tonnes | 50 to 500 million tonnes |

| Average TREO Grade | ~0.4% | 0.3% to 1.5% |

| TiO₂ Co-product Grade | ~12% | Rarely present |

| Near-Surface High-Grade Zone | ~130Mt @ 23% TiO₂ / ~9,100 ppm TREO | Uncommon |

| Dual-Commodity Revenue Structure | Yes | Rare |

Magnet Rare Earths: The Revenue Subset That Actually Matters

One of the most important and least understood dynamics in rare earth investing is the enormous disparity between a deposit's total rare earth content and its actual revenue-generating potential. Cerium and lanthanum typically dominate the mass of most REE deposits, often comprising 50% or more of total rare earth content, yet they command only modest prices and face structural oversupply in many end markets.

The elements that drive revenue are the magnet rare earths: neodymium (Nd), praseodymium (Pr), terbium (Tb), and dysprosium (Dy). These four elements are the critical inputs for neodymium-iron-boron (NdFeB) permanent magnets, the technology that underlies the vast majority of high-performance electric motors and wind turbine generators. Furthermore, the critical minerals demand for these specific elements is forecast to accelerate substantially through the remainder of this decade.

The Tiros deposit is reported to contain meaningful concentrations of Nd, Pr, and Dy within its TREO basket. Dysprosium warrants particular attention. It is used in small quantities per magnet, but its function is irreplaceable: Dy raises the coercivity of NdFeB magnets, allowing them to operate at higher temperatures without demagnetising, a property essential for automotive traction motors.

The global supply of dysprosium is overwhelmingly concentrated in Chinese ionic clay deposits in Jiangxi and Guangdong provinces, making any ex-China source of meaningful Dy content a strategic asset that transcends simple commodity economics.

A deposit that contains dysprosium in commercially meaningful concentrations alongside neodymium and praseodymium is not simply a rare earth project. It is a potential input into the permanent magnet supply chains that sit at the foundation of the energy transition and modern defence manufacturing.

Understanding the FSAL Process: Proprietary Metallurgy as Differentiator and Risk

The rare earth processing challenges in rare earth development are not geological; they are chemical. Separating individual rare earth elements from complex mineralised feeds requires sophisticated hydrometallurgical circuits that few non-Chinese operators have successfully scaled. This processing bottleneck has killed more rare earth projects than any other single factor.

Resouro is advancing a proprietary extraction methodology referred to as the FSAL process, which is designed to recover rare earth elements while simultaneously upgrading titanium mineral fractions within a single integrated circuit. Early bench-scale test work has reportedly demonstrated strong recovery rates across both commodity streams.

The integrated design logic is commercially significant. Running separate rare earth and titanium processing circuits would require duplicated infrastructure, additional reagent inputs, and more complex waste management. A single-circuit solution that handles both streams could, if validated, materially reduce both capital expenditure and ongoing operating costs.

However, the investment community must apply rigorous scrutiny at this stage. Bench-scale results are a proof-of-concept milestone, not a commercial guarantee.

The staged validation pathway that investors should monitor includes:

- Bench-scale metallurgical testing – Establishes initial recovery rates and circuit chemistry in small volumes

- Continuous pilot plant operation – Tests circuit stability, reagent consumption, and material handling at intermediate scale

- Independent third-party verification – External confirmation of recovery rates and processing parameters

- Definitive feasibility study integration – Locks FSAL assumptions into bankable capital and operating cost estimates

- Environmental and social licensing – Particularly complex in Brazil given overlapping federal IBAMA and state regulatory authority

- Offtake agreement execution – Commercial validation that buyers will accept product specifications and volumes

- Project financing close – Requires the above milestones plus demonstrated sovereign risk comfort from lenders

It is worth noting that the rare earth sector has a long history of processing technologies that performed exceptionally at bench scale but encountered significant challenges during continuous pilot plant operation, where reagent consumption, circuit stability, and by-product management frequently reveal complexity not apparent in batch testing.

The US$160 Million Capital Estimate: What It Reveals and What It Leaves Unanswered

A development capital estimate of approximately US$160 million positions Tiros at the more capital-efficient end of the rare earth project spectrum. For context, MP Materials' Mountain Pass restart and Lynas Rare Earths' Mt Weld operations have both involved capital commitments measured in the hundreds of millions to billions of dollars when processing infrastructure is fully included.

The US$160 million figure is notable precisely because of what it may not include. Rare earth project capital estimates frequently omit downstream separation and refining costs, which in many cases are comparable in magnitude to or larger than the mining and concentrating capital. Investors evaluating this figure should seek explicit clarification on whether a rare earth separation circuit and titanium product finishing facilities are included within that envelope or represent a second-stage capital requirement.

The 2026 acquisition of Serra Verde by USA Rare Earth for approximately US$2.8 billion provides the most instructive benchmark for understanding how the market values advanced Brazilian rare earth assets. Serra Verde is an ionic clay deposit, mineralogically distinct from Tiros's hard-rock titanium-REE system, but the transaction establishes that Western capital is willing to deploy transformative sums for non-Chinese rare earth supply anchored in Brazil. For a deeper overview of Resouro's strategic position, independent analysis underscores why the Tiros asset continues to attract investor attention.

The Brazilian Jurisdiction Risk Matrix

Brazil is simultaneously one of the most geologically prospective and regulatorily complex mining jurisdictions in the world. Investors considering Resouro rare earths and titanium investment in Brazil must weigh both dimensions honestly.

| Risk Factor | Assessment | Investor Implication |

|---|---|---|

| Metallurgical scale-up | High uncertainty until pilot validation | Monitor FSAL pilot plant milestones closely |

| Environmental licensing (IBAMA + state) | Potentially multi-year timeline | Build schedule risk into valuation models |

| Indigenous land rights | Increasing regulatory complexity | Requires proactive community engagement |

| Rare earth price volatility | Subject to Chinese export policy | Price sensitivity analysis essential |

| Domestic separation infrastructure | Currently absent in Brazil | Product may be exported as concentrate |

| Currency exposure (BRL/USD) | Significant for USD-denominated capex | Hedging strategy required |

| First-of-kind processing technology | FSAL not yet commercially proven | Technology risk premium warranted |

Brazil currently has no operational rare earth separation facility at commercial scale. This means that Tiros product would most likely be exported as a mixed rare earth concentrate or a partially upgraded intermediate, almost certainly at a meaningful discount to the pricing achievable for separated individual rare earth oxides.

This discount, sometimes referred to in the industry as the concentrate penalty, can have substantial implications for project-level revenue projections and should be explicitly modelled in any financial assessment.

Jurisdiction Benchmarking: Where Brazil Stands in the Global Race

| Factor | Brazil | Australia | Canada | Select African Nations |

|---|---|---|---|---|

| Rare Earth Reserve Scale | 2nd to 3rd globally | Top 5 | Significant | Varies |

| Processing Infrastructure | Early-stage | Established (Lynas) | Limited | Very limited |

| Geopolitical Alignment (Western) | Improving | Strong | Strong | Variable |

| Environmental Licensing Complexity | High | Moderate to High | High | Lower in some cases |

| Dual REE and Titanium Potential | High (Tiros model) | Moderate | Low to Moderate | Low |

Australia's rare earth sector, anchored by Lynas Rare Earths, took approximately two decades from initial resource delineation to achieving consistent profitable production. Canada's rare earth developers continue to grapple with processing infrastructure gaps despite strong political will. Brazil's trajectory may differ given the scale of Western capital now targeting the jurisdiction, but historical timelines provide a sobering reference point. In addition, the ongoing critical minerals race among Western nations continues to accelerate capital deployment into emerging jurisdictions like Brazil.

The next major ASX story will hit our subscribers first

The Investment Calculus: Weighing Asymmetric Outcomes

The bull case for Resouro rare earths and titanium investment in Brazil rests on a convergence of factors that are individually compelling and potentially transformative in combination. A multi-billion-tonne resource containing magnet-critical rare earths and high-grade titanium, supported by a proprietary processing approach, situated in a jurisdiction experiencing unprecedented capital inflows, with a development capital estimate that implies strong project economics if the metallurgy proves scalable.

The bear case is equally well-structured. Brazil's rare earth sector has a documented history of projects that advanced through early-stage enthusiasm before encountering the hard realities of environmental licensing, processing scale-up, and financing in the absence of domestic infrastructure. The FSAL technology, however promising at bench scale, has not yet passed the pilot plant test that determines whether its recovery rates are reproducible under continuous operating conditions.

For sophisticated investors, the framework that applies here is optionality valuation rather than traditional discounted cash flow analysis. At pre-production stages with unvalidated processing technology, the value lies in the asymmetric return profile: limited downside relative to the potential upside if key technical and permitting milestones are achieved on schedule.

What distinguishes Tiros from the broad population of undeveloped rare earth projects globally is the dual-commodity structure that provides two independent revenue streams, the near-surface high-grade zone that enables a staged development approach, the genuine scale of the resource that supports long mine life, and the growing body of Western strategic interest in Brazilian critical mineral supply.

The distance between a promising bench-scale metallurgical result and a producing mine generating revenue remains significant in any honest assessment. But in a world where the concentration of rare earth processing in a single country has become a recognised systemic risk, the long-term strategic logic underpinning the Resouro investment thesis is difficult to dismiss.

This article is intended for informational purposes only and does not constitute financial or investment advice. Readers should conduct their own independent research and consult qualified financial advisers before making investment decisions. Forward-looking statements, resource estimates, capital cost figures, and processing performance data referenced in this article are subject to material risks, uncertainties, and assumptions that could cause actual outcomes to differ significantly from those projected.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across critical minerals including rare earths, instantly transforming complex data into actionable investment insights for both short-term traders and long-term investors — explore historic discoveries that have generated extraordinary returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.