June 11, 2026

The Geology That Started a Geopolitical Race

Not all rare earth deposits are created equal. The mineral world has long understood that the economic viability of a rare earth project depends less on how much ore sits in the ground and more on what that ore looks like at the molecular level. This geological reality is precisely why, when US strategic planners began mapping the world for alternative rare earth supply sources, their attention converged on a specific deposit type found abundantly in two countries: Brazil and Malaysia.

Ionic clay rare earth deposits are fundamentally different from the hard-rock and carbonatite-hosted mineralisation that characterises most of the world's known reserves. In ionic clay systems, rare earth elements are adsorbed onto clay minerals in a loosely bound ionic state, which means they can be liberated through relatively simple leaching processes rather than the energy-intensive crushing, grinding, and smelting required for harder rock types.

This geological characteristic dramatically reduces capital costs, shortens project development timelines, and lowers the technical barriers to entry for new producers.

This single geological fact has shaped billions of dollars of US investment decisions and redefined how Washington views its critical mineral relationships in Latin America. The US-Brazil rare earths partnership, now backed by a proposed $2.8 billion acquisition and over $1 billion in prior financing commitments, represents the most consequential test of whether Western nations can translate geological advantage into genuine supply chain independence.

This article contains forward-looking statements, financial projections, and geopolitical scenario analysis. Readers should treat these as analytical perspectives rather than investment advice or confirmed policy outcomes.

When big ASX news breaks, our subscribers know first

Why Rare Earths Resist Simple Solutions

Understanding the strategic urgency behind the US-Brazil rare earths partnership requires appreciating why rare earth supply chains are uniquely resistant to diversification efforts that have succeeded in other commodities.

Unlike oil, where geographic distribution of reserves across dozens of nations creates natural diversification, rare earth supply chains are bottlenecked not at the extraction stage but at the processing stage. China controls an estimated 85–90% of global rare earth processing capacity, built over several decades through deliberate industrial policy, subsidised energy, and accumulated technical expertise that cannot be replicated quickly elsewhere.

The four magnetic rare earth elements at the centre of current Western strategy each perform indispensable roles:

- Neodymium (Nd) serves as the primary magnetic component in neodymium-iron-boron (NdFeB) permanent magnets, providing the base magnetic strength

- Praseodymium (Pr) is typically co-produced with neodymium and enhances magnetic performance, often traded together as a combined oxide known in the industry as NdPr

- Dysprosium (Dy) is added to NdFeB magnets to maintain magnetic properties at elevated temperatures, a requirement critical for electric vehicle traction motors that generate significant heat during operation

- Terbium (Tb) serves a similar thermal stabilisation function and can partially substitute for dysprosium, with both elements classified as heavy rare earths that are considerably scarcer and more strategically sensitive than light rare earth elements

The separation process to isolate each of these elements from mixed rare earth concentrate involves hundreds of sequential solvent extraction stages, achieving purity levels typically exceeding 99.95% for magnet-grade applications. Furthermore, the rare earth processing challenges involved are precisely why nations with significant reserves but no processing infrastructure remain strategically exposed despite their geological wealth.

Securing rare earth ore supply solves only the first link in a chain that spans separation, refining, alloying, and magnet manufacturing. Partial solutions have historically failed to reduce dependence on Chinese processing at any meaningful scale.

Brazil's Rare Earth Paradox: Second in Reserves, Near-Absent in Production

Brazil presents one of the most striking asymmetries in the global critical minerals landscape. The country holds the world's second-largest rare earth reserves yet contributes less than 1% of global rare earth output, according to reporting by Argus Media. This gap between geological endowment and industrial output has persisted for structural reasons that the US partnership framework is specifically designed to address.

The Ionic Clay Advantage in Practice

Brazil's rare earth endowment is concentrated predominantly in ionic clay formations, particularly across the Goiás state region in the country's interior. Compared to the hard-rock and carbonatite-hosted deposits that characterise other major rare earth provinces, ionic clay mineralisation offers producers a fundamentally different cost and risk profile.

The extraction chemistry involved in ionic clay processing relies on ion-exchange reactions, where ammonium sulphate or similar leaching solutions displace the loosely adsorbed rare earth ions from clay minerals. This approach requires significantly less capital infrastructure than conventional mining and avoids the highly energy-intensive smelting processes associated with other deposit types. The practical effect is faster project development, lower upfront capital requirements, and reduced technical risk during commissioning.

This is precisely why the White House identified Brazil alongside Malaysia as priority partnership targets, specifically because their reserves are predominantly found in ionic clay, which is considerably easier to process than alternative deposit configurations, as reported by the Financial Times in June 2026.

Brazil's Geopolitical Neutrality as a Strategic Asset

Beyond geology, Brazil brings a geopolitical characteristic that no other major rare earth-endowed nation can offer: active diplomatic relations with every United Nations member state. In a world where commodity supply chains have become instruments of geopolitical pressure, this diplomatic breadth transforms Brazil's mineral assets into something qualitatively different from those of other potential partners.

Brazil's secretary for climate, energy and environment Mauricio Lyrio observed at a critical minerals seminar held by Brazil's mining institute Ibram in Brasília in June 2026 that Brazil's mineral assets accumulate strategic value during periods of global geopolitical tension precisely because the country can engage commercially with every nation — a capability that has become increasingly rare as other major mineral producers align with competing geopolitical blocs.

This positioning creates a unique dynamic: Brazil can negotiate with both Western and non-Western buyers simultaneously, which gives it genuine leverage when setting partnership terms rather than simply accepting the conditions offered by any single bloc.

| Metric | Brazil's Position |

|---|---|

| Global rare earth reserve ranking | 2nd largest |

| Share of current global production | Less than 1% |

| Primary deposit type | Ionic clay |

| Key producing region | Goiás state |

| UN diplomatic coverage | All 193 member states |

| Strategic processing advantage | Lower capital intensity, simpler extraction chemistry |

The Financial Architecture of the US-Brazil Rare Earths Strategy

The financial commitments are operating within an institutional policy architecture that provides structural continuity across administrations and diplomatic cycles. Furthermore, the scale of US financial commitment to Brazilian rare earths distinguishes this partnership from the policy declarations and letters of intent that have characterised previous Western supply chain diversification attempts.

Serra Verde: The Centrepiece Investment

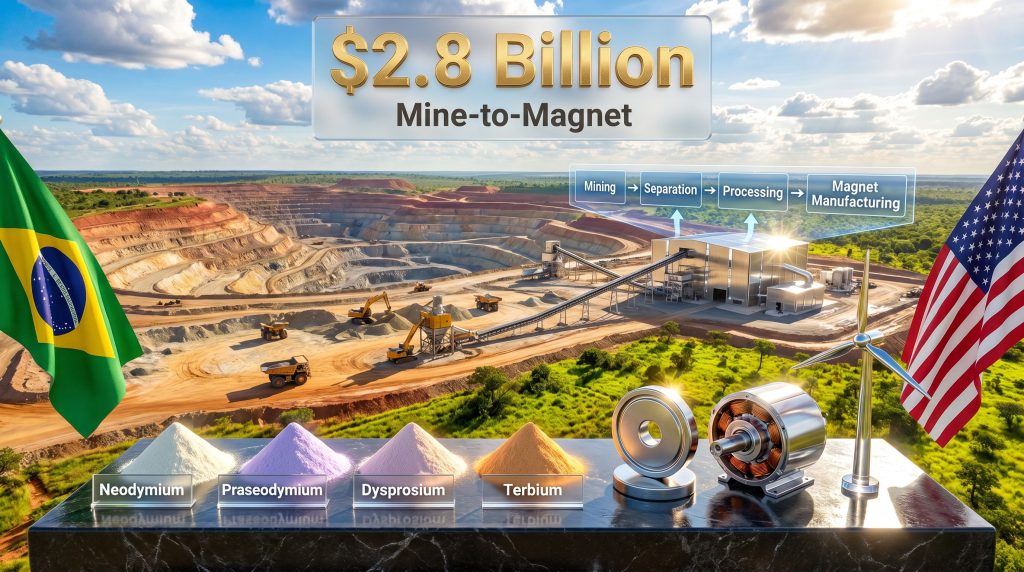

Serra Verde Group's Pela Ema operation in Goiás state occupies a unique position in the global rare earth landscape. It is described as the only scaled producer outside Asia with the operational capacity to supply all four key magnetic rare earth elements simultaneously, making it particularly valuable to the mine-to-magnet integration strategy the US is pursuing.

The proposed acquisition of Serra Verde, valued at approximately $2.8 billion, follows a financing package of approximately $560 million extended prior to the acquisition announcement, as reported by Argus Media. This sequencing matters analytically: the prior financing reflects sustained institutional commitment rather than a single opportunistic transaction, indicating that the acquisition is the culmination of a multi-stage engagement rather than an impulsive strategic bet.

The US International Development Finance Corporation (DFC) has committed up to $465 million to Serra Verde, bringing US government-backed capital directly into the project's financial structure. This DFC involvement signals a level of sovereign commitment that makes the partnership more durable against diplomatic turbulence than purely commercial transactions would be.

Additional US financing commitments have also been extended to Aclara Resources, another emerging Brazilian rare earth producer, which consequently broadens the investment footprint and reduces concentration risk across a single project.

What Mine-to-Magnet Integration Actually Means

The phrase mine-to-magnet is used frequently in discussions of rare earth strategy but rarely explained in operational terms. The integration model aims to capture value at every stage of the rare earth value chain, eliminating the dependency on Chinese processing that has undermined previous supply chain diversification efforts:

- Mining — extraction of ionic clay ore at Pela Ema through ion-exchange leaching

- Separation — isolation of individual rare earth oxides from mixed rare earth concentrate through sequential solvent extraction

- Processing — conversion of separated oxides into rare earth metals and alloys through specialised metallurgical processes conducted under controlled atmospheric conditions

- Magnet manufacturing — production of sintered NdFeB permanent magnets through powder metallurgy techniques including jet milling, magnetic field alignment, and precision sintering

Each stage represents a technical competency that China has built and defended over decades. The strategic logic of vertical integration is that partial solutions — securing ore supply without corresponding processing capacity — consistently fail to reduce actual dependence on Chinese rare earth products because the processing bottleneck simply shifts downstream rather than being resolved.

The Bilateral Policy Framework Beyond Private Capital

A bilateral US-Brazil Critical Minerals Working Group already exists as a formal coordinating mechanism, providing a structured channel for aligning permitting timelines, investment screening, and joint venture frameworks between the two governments. This institutional layer is what differentiates the current partnership from the commercial transactions that preceded it, as it creates government-to-government accountability for project progression.

Christopher Garman, Eurasia Group managing director for the Americas, described the US as ready to move at exceptional speed to deepen its rare earth partnership with Brazil, characterising the White House's posture as one of active readiness rather than passive interest, as reported by Argus Media from a critical minerals seminar held in Brasília in June 2026.

Diplomatic Friction and Partnership Durability

The reimposition of US tariffs on Brazilian goods and the classification of certain Brazilian organised crime groups as terrorist organisations created interpretive questions about whether strategic mineral collaboration could survive diplomatic friction. However, the analytical consensus from those familiar with White House operations is that these policy actions represent parallel decision-making tracks developed independently of mineral strategy, rather than signals of deteriorating alignment on critical minerals.

Garman noted that geopolitical strategy would continue to drive pragmatic US engagement with Brazil specifically because of the value of Brazil's mineral assets, suggesting that commodity-level strategic partnerships have a durability that short-term diplomatic tensions do not typically override.

The US-Brazil rare earths relationship is being anchored by the structural value of Brazil's geological endowment rather than ideological alignment. History suggests that strategic mineral partnerships, once capitalised at scale, tend to outlast the diplomatic frictions that surround them.

Benchmarking the Brazil Approach Against Competing Western Strategies

The US-Brazil partnership does not exist in isolation. It sits within a broader Western rare earth strategy that spans multiple bilateral frameworks at varying stages of maturity. In addition, America's rare earth supply chain ambitions extend well beyond any single partnership, making the comparative context essential for understanding the Brazil model's strategic position.

| Partnership Model | Key Features | Development Stage | Capital Commitment |

|---|---|---|---|

| US-Brazil (Serra Verde) | Mine-to-magnet, ionic clay, DFC financing | Advanced, Q3 2026 close targeted | ~$2.8B acquisition + $465M DFC |

| US-Australia (Lynas, MP Materials) | Processing agreements, domestic refinery investment | Operational | Multi-billion across programmes |

| US-Japan Framework | Coordinated investment, stockpiling, project selection | Policy-level coordination | Ongoing |

| US-Canada Critical Minerals | Domestic sourcing, USMCA alignment | Operational and expanding | Multi-programme |

| Malaysia Ionic Clay | Parallel ionic clay targeting | Early engagement | Not publicly disclosed |

The Brazil model is distinguished by the combination of upstream mine ownership, integrated downstream ambition, and the specific ionic clay geological advantage that reduces processing complexity throughout the value chain. Malaysia was identified alongside Brazil as a priority partner for identical geological reasons, suggesting that the US is running parallel ionic clay-focused partnership tracks rather than concentrating its entire strategic exposure in a single bilateral relationship.

The next major ASX story will hit our subscribers first

Critical Risk Dimensions Across the Partnership

Regulatory and Permitting Uncertainty

Brazil's mining permitting environment, while undergoing improvements, remains a source of timeline uncertainty for large-scale projects. The country's National Mining Agency (ANM) and environmental licensing processes introduce variables that can extend project development schedules beyond initial projections.

Brazilian officials including Lyrio have themselves acknowledged the tension between recognising Brazil's strategic opportunity and the institutional pace at which regulatory processes operate, emphasising that Brazil needs a strong sense of urgency to capitalise on its position before competing supply sources emerge elsewhere.

The Processing Infrastructure Gap

Even with upstream rare earth ore secured through the Serra Verde acquisition, the Western world faces a more fundamental challenge: insufficient separation, processing, and magnet manufacturing capacity outside Asia. Building new facilities requires not just capital but specialised technical expertise that has been concentrated in China for decades, along with supply chains for ancillary chemicals and equipment that do not yet exist at scale in Western industrial ecosystems.

This infrastructure gap means that full supply chain independence remains a decade-long structural objective rather than a near-term outcome of any single acquisition.

Price Volatility and Market Risk

Rare earth prices carry a history of severe volatility, often driven by China's export restrictions and production policy decisions that can rapidly reshape project economics for non-Chinese producers. The mine-to-magnet integration model is partly designed to address this vulnerability by capturing value across multiple stages of the supply chain, reducing sensitivity to upstream price movements.

Long-term offtake agreements with end-users in the electric vehicle and defence sectors are expected to provide additional pricing stability, though these arrangements introduce their own counterparty and volume risks.

Chinese Countermeasure Risk

A strategically underappreciated risk is the possibility that China could accelerate export restrictions on processed rare earth products and magnets precisely during the window when Western processing alternatives are being constructed but not yet operational. This scenario would be most damaging if it occurred in the 2026–2030 period, before new Western separation and magnet manufacturing capacity reaches commercial scale, creating a period of maximum vulnerability between the commitment to build and the ability to produce.

Long-Term Structural Implications for Global Supply Chains

The US-Brazil rare earths partnership represents the most advanced attempt by any Western nation to build a genuinely integrated rare earth supply chain outside Asia. Its rare earth geopolitical impact extends beyond the bilateral relationship itself: success or failure will determine whether the friend-shoring model for critical minerals is operationally viable or whether it remains an aspiration that consistently founders on processing infrastructure realities.

Brazil's leverage in this relationship is substantial but time-bounded. As Lyrio articulated at the Brasília seminar, the country needs to actively shape the terms of its mineral partnerships rather than simply respond to external demands — a posture that reflects an understanding that geological assets are most valuable before competing supply sources mature.

The downstream industrial implications for US manufacturing are equally significant. Securing rare earth supply ultimately serves domestic production objectives in electric vehicles, wind energy, and defence systems. If the mine-to-magnet integration model succeeds in connecting Brazilian ionic clay geology to US magnet manufacturing capacity, it would represent the first genuine structural challenge to Chinese dominance in permanent magnet supply chains since that dominance was established.

Frequently Asked Questions: US-Brazil Rare Earths Partnership

What rare earth elements are central to the partnership?

The four magnetic rare earth elements driving the US-Brazil strategic engagement are neodymium, praseodymium, dysprosium, and terbium. These elements are essential inputs for sintered NdFeB permanent magnets used in electric vehicle traction motors, wind turbine generators, and a broad range of military systems including guidance technologies and naval propulsion.

Why are ionic clay deposits strategically preferred?

Ionic clay rare earth deposits allow extraction through ion-exchange leaching chemistry rather than the energy-intensive crushing and smelting required for hard-rock mineralisation. This reduces capital intensity, shortens development timelines, and lowers technical barriers for new producers, making ionic clay-hosted projects significantly faster and cheaper to bring into production.

What US government financing has been committed?

The US International Development Finance Corporation has committed up to $465 million to Serra Verde. This followed a prior financing package of approximately $560 million to Serra Verde and separate financing commitments to Aclara Resources. The proposed acquisition of Serra Verde itself is valued at approximately $2.8 billion.

What is the mine-to-magnet model?

Mine-to-magnet refers to vertical integration across the entire rare earth value chain, from ore extraction through separation, oxide-to-metal conversion, alloying, and final permanent magnet manufacturing. The objective is to eliminate dependency on Chinese processing at every stage, as partial supply chain solutions have historically failed to provide genuine independence from Chinese rare earth products.

How large are Brazil's rare earth reserves?

Brazil holds the world's second-largest rare earth reserves, yet currently contributes less than 1% to global production output. This gap between geological endowment and industrial output represents the core strategic opportunity driving the US partnership investment.

How durable is the partnership given diplomatic tensions?

Analysis from those familiar with current US-Brazil dynamics suggests that strategic mineral partnerships anchored by large-scale capital commitments tend to operate on a separate and more durable track than diplomatic tensions arising from trade policy or security classifications. The structural value of Brazil's ionic clay rare earth endowment is considered the primary driver of US engagement, rather than ideological alignment. For additional context, the Columbia University Energy Policy centre has published detailed analysis of Brazil's potential role in diversifying US critical mineral supply.

Assessing the Strategic Stakes

The US-Brazil rare earths partnership has moved beyond the declaratory phase that has characterised most previous Western supply chain diversification efforts. With $2.8 billion in acquisition capital, $465 million in DFC commitments, and a formal bilateral working group providing institutional continuity, the partnership possesses the financial and structural foundations to potentially deliver something genuinely new: a scaled, integrated rare earth supply chain operating entirely outside Asia.

The conditions for success are knowable. They require regulatory velocity in Brazil to match the urgency of US investment timelines, successful close of the Serra Verde transaction, and sustained progress toward the downstream processing and magnet manufacturing capacity that completes the mine-to-magnet chain. Brazil's acknowledgement that a strong sense of urgency is required to capitalise on its opportunity suggests that at least some of the necessary institutional momentum exists on the Brazilian side.

The conditions for failure are equally clear: permitting delays, rare earth price suppression by Chinese producers, or the emergence of politically driven obstacles on either side of the bilateral relationship could derail project economics before the supply chain reaches operational maturity.

What is not in doubt is the geological case. Brazil's ionic clay rare earth endowment, its diplomatic neutrality, and the specific combination of neodymium, praseodymium, dysprosium, and terbium available from the Pela Ema deposit make the US-Brazil rare earths partnership the most strategically coherent Western attempt to challenge Chinese critical mineral dominance that has yet been assembled. Whether that coherence translates into operational supply chain reality will define whether friend-shoring becomes a genuine geopolitical tool or remains an aspirational framework that consistently falls short of its structural ambitions.

For ongoing rare earth pricing, trade flow analysis, and market intelligence, Argus Media publishes dedicated coverage of the rare earths sector at argusmedia.com.

Want to Know When the Next Major Rare Earth Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across rare earths and over 30 other commodities — translating complex geological data into actionable investment insights before the broader market reacts. Explore how historic discoveries have generated exceptional returns on the Discovery Alert discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major find.