July 17, 2026

The Underground Shift Redefining How Mid-Tier Gold Miners Build Value

Across Western Australia's gold mining districts, a fundamental operational transition is playing out beneath the surface. As shallow open-pit ore bodies approach the end of their economic lives, producers of every scale are committing capital to underground development as the primary mechanism for sustaining and growing output. This is not simply a geological inevitability — it is a deliberate strategic pivot that carries profound implications for production economics, capital intensity, mine life extension, and ultimately, investor returns.

Understanding this transition is essential context for interpreting Regis Resources FY27 gold production guidance, which represents more than a single year's output forecast. It is a statement of directional intent from a company positioning itself at the intersection of mid-tier and senior producer scale.

When big ASX news breaks, our subscribers know first

What the FY27 Guidance Numbers Actually Signal

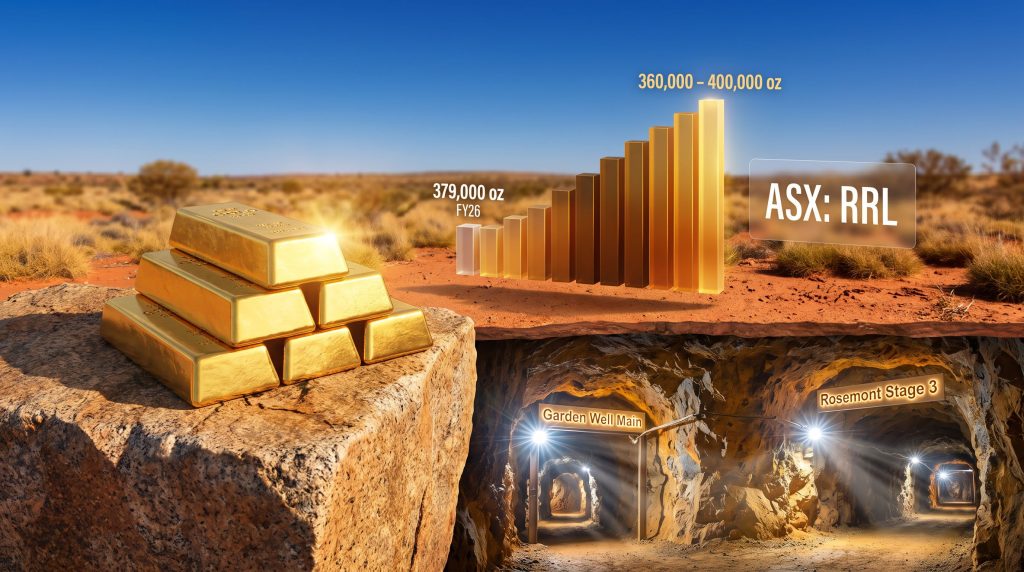

Regis Resources (ASX: RRL) has set its group gold production target for FY27 at 360,000 to 400,000 ounces, with management projecting output toward the upper boundary of that range. To appreciate the significance of this, it helps to view it against the company's recent production history.

| Metric | Detail |

|---|---|

| FY27 Guidance Range | 360,000 – 400,000 oz |

| Upper-End Target | ~400,000 oz |

| Prior Guidance Band (FY25–FY26) | 350,000 – 380,000 oz |

| FY26 Actual Production | ~379,000 oz |

| Q4 FY26 Production Growth | +12% quarter-on-quarter |

| Primary Growth Asset | Duketon (Garden Well Main + Rosemont Stage 3) |

The FY26 actual result of approximately 379,000 ounces is particularly instructive. It landed at the very top of the prior guidance band, which means management enters FY27 with both operational momentum and guidance credibility — two factors that markets tend to reward with reduced risk discounting. The 12% quarter-on-quarter production increase recorded in Q4 FY26 further reinforces that the trajectory entering the new financial year is upward, not mean-reverting.

For a company of this scale, a potential uplift of up to 50,000 additional ounces in a single year represents meaningful volume growth, particularly when it is being achieved organically rather than through acquisition. In addition, Australian gold M&A activity in recent periods has demonstrated that organic growth of this nature is often valued more highly by the market than acquisition-driven expansion.

The Twin Engines of Underground Growth at Duketon

The operational story behind Regis Resources FY27 gold production guidance centres on two underground development projects within the Duketon mining district in Western Australia's Goldfields region.

Garden Well Main

Garden Well has been a cornerstone open-pit operation within Duketon for years, but the underground extension — known as Garden Well Main — represents a transition to higher-grade ore that surface mining cannot access. Underground operations at established open-pit sites benefit from pre-existing surface infrastructure, haul roads, processing facilities, and workforce familiarity with the ore body's geological character. This reduces both development cost and commissioning risk compared with greenfield underground projects.

Rosemont Stage 3

Rosemont Stage 3 extends an already-producing underground mine deeper into the ore system. Stage progression in underground mining is a disciplined approach to capital management: rather than committing to full-depth development upfront, operators open successive stages as earlier phases generate cash flow and geological confidence improves. An underground mine expansion study conducted at comparable WA operations illustrates how this staged methodology can substantially de-risk capital deployment. By FY27, Rosemont Stage 3 is expected to be contributing at steady-state rates.

Together, these two underground assets are targeting a combined annualised steady-state output of 100,000 to 120,000 ounces. That is a material production engine by any measure, and it forms the core of the FY27 uplift case.

It is important to note that approximately 36% of this combined steady-state production target is classified as Exploration Target material under the JORC Code 2012 — a classification that carries inherently higher geological uncertainty than Mineral Resources or Ore Reserves. Investors should treat the upper-end FY27 scenario with this qualification in mind.

Understanding JORC Classifications and Why the 36% Figure Matters

The JORC Code is the Australian standard governing the public reporting of exploration results, mineral resources, and ore reserves. It establishes a hierarchical confidence framework that most retail investors are not deeply familiar with, but which carries significant weight in how production targets should be interpreted. Furthermore, proper drill results interpretation is central to understanding how Exploration Target material eventually progresses through this confidence hierarchy.

The hierarchy works as follows:

- Exploration Target — The lowest confidence category. Represents a range of tonnage and grade estimated on the basis of limited geological information. Not a Mineral Resource.

- Inferred Resource — Geological confidence sufficient to imply but not verify continuity of mineralisation. Based on limited sampling.

- Indicated Resource — Sufficient confidence to allow mine planning assumptions but not final feasibility decisions.

- Measured Resource — Highest geological confidence, suitable for detailed mine planning and reserve conversion.

- Probable/Proved Reserve — The economically mineable portion of Indicated or Measured Resources, incorporating modifying factors such as mining method, costs, and recoveries.

The fact that roughly one-third of the Garden Well Main and Rosemont Stage 3 steady-state production estimate relies on Exploration Target material means that a portion of the FY27 upper-end scenario depends on geological outcomes that have not yet been confirmed through systematic drilling and resource estimation. This is not unusual in underground mine development — it is common for miners to extend development headings into areas where geological data is still being gathered — but it introduces a variable that conservative modelling should account for.

The Four-Underground-Mine Vision: A Long-Term Architecture

Beyond FY27, Regis Resources has articulated a strategic blueprint for Duketon that goes well beyond two underground mines. The company's objective is to operate at least four concurrent underground mines within the Duketon district simultaneously, targeting a sustainable production rate of 200,000 to 250,000 ounces per annum from the district alone.

This is a structurally important distinction. Rather than relying on a single underground operation to carry the Duketon production profile, the multi-mine configuration distributes geological risk across several ore bodies and provides operational redundancy. If one mine encounters unexpected ground conditions or ore variability, the others continue contributing to mill feed.

The processing plant at Duketon is already sized to handle elevated throughput, which means that as additional underground ore sources come online, the incremental capital required to lift production is predominantly development capital rather than processing infrastructure capital. This is a key economic lever in the underground transition model.

The Duketon and Tropicana Two-Pillar Structure

Duketon's underground ambitions are additive to the Tropicana joint venture, in which Regis Resources holds a 30% interest alongside AngloGold Ashanti as operator. Tropicana is one of WA's highest-quality gold operations, characterised by low strip ratios, consistent ore grades, and a well-established processing facility in a remote but operationally mature location.

| Pillar | Asset | Ownership | Expected Role |

|---|---|---|---|

| Pillar 1 | Duketon Operations | 100% | Growth engine via 4-mine underground strategy |

| Pillar 2 | Tropicana JV | 30% interest | Stable, high-quality production baseline |

This two-pillar production architecture is a meaningful structural advantage. Geographic diversification across two distinct WA gold provinces reduces single-asset concentration risk, while the differing cost and grade profiles of each operation provide a natural internal hedge against operational variability.

Gold Price Economics: How Spot Prices Reshape Ore Decision-Making

One of the less-discussed dimensions of Regis Resources FY27 gold production guidance is the role that elevated gold prices play in the ore selection process. This is a dynamic that fundamentally alters the economics of mine planning in ways that are not immediately obvious from headline production figures.

In mining, every ore body contains material across a spectrum of grades. At any given gold price, there is a cut-off grade below which ore is uneconomic to process and is either stockpiled or classified as waste. Understanding cut-off grade economics is therefore essential when assessing how guidance ranges are constructed and what assumptions sit behind the upper-end scenarios. When the gold price rises significantly, this cut-off grade falls — meaning that material previously deemed sub-economic transitions into the cash-flow-positive category.

The practical effect is twofold:

- More tonnes become available for processing, increasing potential mill throughput and production volumes.

- Lower-grade stockpiles accumulated during lower-price periods can be blended into mill feed to supplement higher-grade underground ore.

Both effects contribute to the FY27 production uplift. The strong gold price impact on miners has been considerable throughout 2025–2026, with USD gold prices reaching historic highs and a relatively weaker Australian dollar amplifying AUD-denominated revenues, substantially improving the economics of marginal ore across Australian gold operations.

The inverse of this dynamic is equally important: a material correction in the gold price would raise cut-off grades across the portfolio, potentially removing some of the ore volumes underpinning the upper end of guidance from the economic mine plan. This price sensitivity is an embedded variable in the FY27 outlook that is easy to overlook when gold prices are elevated.

The next major ASX story will hit our subscribers first

How Australian Mid-Tier Gold Producers Compare

To contextualise the Regis Resources FY27 production target within the broader ASX gold landscape, the following framework is instructive:

| Producer Category | Approximate Annual Output | Growth Approach |

|---|---|---|

| Senior Producers (Newmont Australia, Northern Star) | 1,000,000+ oz | Stable to incremental, M&A supplemented |

| Upper Mid-Tier (Evolution Mining) | 700,000–900,000 oz | Acquisition-driven with brownfield expansion |

| Mid-Tier (Regis Resources FY27) | 360,000–400,000 oz | Organic underground development |

| Emerging Producers | Under 200,000 oz | Development and ramp-up phase |

What distinguishes Regis Resources' growth pathway is its entirely organic character. There is no acquisition premium being paid, no integration risk being absorbed, and no equity dilution being deployed to purchase someone else's production. The FY27 uplift is generated from within the existing asset base through disciplined capital allocation to underground development.

This is a capital-efficient growth model, but it requires geological confidence, operational execution discipline, and — critically — sufficient gold price support to justify the underground development economics at the margins of the ore body.

Key Risk Factors Investors Should Monitor

Any production guidance figure involves assumptions, and the FY27 target carries a specific set of risk variables that sophisticated investors should actively track through quarterly reporting:

- Exploration Target conversion rate — As development headings advance at Garden Well Main and Rosemont Stage 3, drilling programmes will progressively convert Exploration Target material into classified Mineral Resources. The rate of this conversion will signal whether the upper-end production scenario is achievable.

- Underground development metres completed per quarter — In underground mining, the rate of decline and lateral development advance is a leading indicator of future ore access. Quarterly activity reports disclosing development metres provide an early warning of potential production timing delays.

- Mill throughput and recovery rates — Processing performance at Duketon, including tonnes milled and gold recovery percentages, determines how efficiently mined ore translates into payable ounces. Unexpected ore hardness or variability can reduce both metrics.

- All-in sustaining costs (AISC) — A production increase that is accompanied by proportional cost escalation delivers lower incremental free cash flow than headline ounce growth implies. Monitoring AISC against industry benchmarks is essential for assessing the economic quality of the volume growth.

- Gold price sensitivity — Given the role of cut-off grade flexibility in the FY27 outlook, any sustained gold price decline warrants a reassessment of ore volume assumptions embedded in the guidance range.

What Guidance Credibility Means for Market Interpretation

There is a well-documented pattern in how equity markets respond to production guidance in the mining sector. Companies that consistently deliver at or above the midpoint of their stated guidance range tend to receive progressively lower risk discounts on future guidance — a phenomenon sometimes described in investor psychology as guidance trust premium accumulation.

Regis Resources enters FY27 with a strong credibility position: FY26 actual production of approximately 379,000 ounces against a guidance ceiling of 380,000 ounces is as close to top-of-range delivery as is practically achievable. This track record directly supports the market's willingness to price the FY27 guidance toward its upper end rather than anchoring conservatively at the 360,000-ounce floor.

The decision to project toward 400,000 ounces rather than guiding more conservatively is itself a signal. Management guidance language in ASX-listed mining companies is rarely casual — it reflects an internal assessment of achievable outcomes that has been stress-tested against operational assumptions and geological data available at the time of release.

The Broader Structural Case for WA Underground Gold

Western Australia's gold sector is at an inflection point that extends well beyond any single company's guidance range. The state's dominant open-pit gold operations — many of which were established during the 1990s and 2000s resource cycle — are reaching depths where open-pit economics become challenged by increasing strip ratios and waste movement costs.

The industry-wide response has been a systematic pivot to underground mining, which offers:

- Access to higher-grade ore at depth, improving revenue per tonne milled

- Elimination of strip ratio as a cost variable (underground operations have no overburden removal requirement)

- Longer mine life from ore bodies that surface mining cannot economically access

- Smaller operational footprint, which can reduce some categories of environmental permitting complexity

The trade-off is higher upfront development capital, longer lead times to steady-state production, and increased sensitivity to ground conditions and equipment reliability. These are the exact execution risks that are embedded in the FY27 production guidance for Regis Resources.

Regis Resources FY27 gold production guidance is ultimately a case study in how a well-positioned mid-tier producer converts geological assets into operational reality during a favourable commodity price cycle — and the risks that remain between guidance and delivery. For broader context on how Australian gold producers are navigating this operational and strategic transition, the Australian Mining Review provides ongoing sector coverage worth following.

This article is intended for informational and educational purposes only and does not constitute financial advice. Production guidance figures, geological classifications, and financial projections referenced herein are based on publicly available information and company disclosures. Readers should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions. Mining investments carry inherent risks including operational, geological, commodity price, and regulatory uncertainties.

For ongoing coverage of Australian gold producer operations and ASX mining sector developments, visit the ASX announcements page for the latest Regis Resources disclosures and company updates.

Want To Be First When The Next Major ASX Gold Discovery Is Announced?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex geological data into actionable opportunities — the same kind of edge that has historically generated substantial returns, as showcased on Discovery Alert's dedicated discoveries page. Begin your 14-day free trial at Discovery Alert today and position yourself ahead of the broader market.