July 18, 2026

The Hidden Architecture of Modern Crude Procurement

Every barrel of crude oil that enters a refinery represents a decision made weeks or months earlier, shaped by geopolitics, freight economics, sanctions law, and the physical chemistry of the refinery itself. For most of the past four decades, Indian refiners made that decision with a relatively predictable answer: buy from the Arabian Gulf. Proximity, established relationships, and benchmark pricing made the Gulf the obvious default. However, obvious defaults carry hidden concentration risks, and when those risks materialise simultaneously, the consequences cascade through the entire value chain.

The events of the June 2026 quarter exposed that concentration risk with striking clarity. What followed was not a reactive scramble but the visible activation of supply architecture that Reliance Industries had been quietly constructing for years, positioning Reliance Industries crude sourcing from Russia and Latin America as the defining strategic story of the quarter.

When big ASX news breaks, our subscribers know first

What the Strait of Hormuz Closure Revealed About Indian Refining's Core Vulnerability

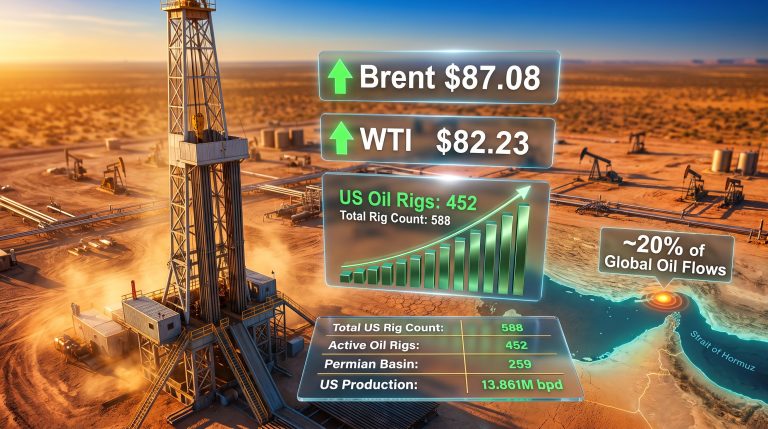

The Strait of Hormuz is one of the world's most consequential geographic chokepoints. At its narrowest, the passage spans roughly 33 kilometres, yet approximately 20 percent of global petroleum liquids transit through it on any given day. When this corridor was effectively closed during the June 2026 quarter, the disruption cascaded through global markets with unusual speed.

Approximately 13 million barrels per day of crude supply was disrupted, triggering a Brent crude average of $104.5 per barrel during the quarter, representing a year-on-year increase of $36.7 per barrel. For refiners structurally dependent on Arabian Gulf feedstock, this was not merely a price shock but a physical availability problem.

The episode illustrates a concept that procurement strategists call single-corridor dependency risk: the amplified vulnerability that emerges when both physical supply and pricing benchmarks are anchored to the same geographic source. Arabian Gulf crudes dominate Indian import volumes and also set the price reference against which most alternatives are measured. When the Gulf is disrupted, both the supply and the benchmark deteriorate simultaneously. Understanding the broader crude oil market dynamics helps contextualise why this dual deterioration is so damaging for unprepared buyers.

Refiners with pre-established alternative supply corridors and the technical flexibility to process non-benchmark crude grades are structurally insulated from this dual-deterioration dynamic in ways that pure Arabian Gulf buyers cannot easily replicate.

Jamnagar's Technical Architecture: Why Feedstock Flexibility Is Not Accidental

Understanding why Reliance Industries could pivot so effectively requires understanding what makes the Jamnagar refining complex unusual among global refining assets. The facility is not simply the world's largest single-location refinery by throughput; it is also one of the most technically versatile.

The dual-refinery configuration at Jamnagar processes crude grades across an exceptionally wide spectrum, from ultra-light condensates with API gravities above 50 degrees to heavy sour barrels with API gravities below 20 degrees and sulphur content exceeding 3.5 percent. This range is far broader than most competing facilities can accommodate without significant yield penalties.

Three elements of the secondary processing configuration are particularly relevant to Reliance's crude diversification strategy:

- Coker units convert the heaviest, lowest-value residual fractions from heavy sour crude distillation into lighter, more valuable products. Refineries without coking capacity are forced to sell or blend away the heavy residual, dramatically reducing the economic case for processing heavy crude grades.

- Fluid catalytic cracking (FCC) units process the intermediate vacuum gas oil fractions into high-octane gasoline components and propylene, allowing the refinery to capture petrochemical margin from grades that simpler refineries would underutilise.

- Hydrodesulphurisation (HDS) capacity removes sulphur from high-sulphur crude derivatives to meet product quality specifications, allowing the refinery to accept high-sulphur sour crudes that would otherwise be incompatible with finished product requirements.

This secondary unit configuration is the technical foundation upon which Reliance's geopolitical procurement flexibility rests. Without it, the shift toward Russian Urals and Venezuelan Merey would generate yield penalties large enough to eliminate the feedstock cost advantage entirely.

Reliance Industries Crude Sourcing from Russia: A Decade-Long Strategic Commitment

The scale of Reliance's engagement with Russian crude supply is not widely understood outside specialised energy trade circles. The company's relationship with Russian crude predates the 2022 supply realignment that brought many Asian refiners into the market opportunistically. However, the formal institutionalisation of that relationship reached a new level with the signing of a 10-year supply agreement with Rosneft in December 2024, valued at approximately $12 to $13 billion annually and covering volumes of up to 500,000 barrels per day.

At peak intake prior to the October 2025 U.S. sanctions on Rosneft, Reliance was India's single largest buyer of Russian crude, reportedly handling volumes equivalent to roughly 8 percent of Russia's total crude export flow since 2022. Furthermore, current crude prices at the time made these discounted Russian barrels particularly attractive relative to spot market alternatives. This scale of engagement has few parallels among non-Chinese Asian buyers.

Navigating Rosneft Sanctions Without Abandoning Russian Supply

The October 2025 U.S. designation of Rosneft under expanded Russian oil sanctions created an immediate compliance challenge. Reliance's response followed a structured sequence rather than a blanket withdrawal:

- A temporary suspension of Rosneft-linked purchases in late 2025 served as a visible compliance signal to U.S. counterparties and regulators.

- Procurement was rerouted through non-sanctioned Russian intermediary entities, most notably RusExport, which provided a legally compliant conduit for continued Russian crude acquisition.

- U.S. government waivers were secured for purchases from specific approved entities, providing a formal authorisation layer on top of the intermediary routing.

- Imports resumed in early 2026 at a modified volume of approximately 150,000 barrels per day, beginning in February 2026 under the revised compliance framework.

- A cargo of 6 million barrels was secured for March 2026 delivery as Middle East supply disruptions escalated, demonstrating the speed with which pre-established relationships can be scaled when market conditions shift.

What Reliance has effectively demonstrated is that sophisticated legal infrastructure, not just procurement relationships, is the critical differentiating capability for large-scale buyers seeking to maintain access to discounted non-Western supply while satisfying compliance obligations.

Reliance Industries has received a US licence to directly purchase crude from approved entities, a development that underscores how compliance architecture has become as strategically important as the procurement relationships themselves.

The Price Economics of Russian Crude at Scale

The financial logic of sustained Russian crude procurement rests on a durable structural discount. Russian Urals and ESPO blend crudes have historically traded at discounts of $3 to $7 per barrel below comparable benchmark grades. At a conservative mid-range discount of $5 per barrel applied to 150,000 barrels per day of intake, the annualised feedstock cost saving reaches approximately $275 million.

This figure must be weighed against elevated freight costs on longer Baltic and Pacific routing to India's west coast, which erode but do not eliminate the discount advantage. Insurance cost premiums on Russian-linked shipping arrangements in the post-sanctions environment add a further layer of cost, which RIL itself acknowledged as a margin headwind during the quarter.

The net economics are clearly sufficient to justify the operational complexity. If they were not, a company of Reliance's analytical sophistication would not have locked itself into a 10-year supply framework.

Venezuelan Merey Heavy Crude: The Atlantic Basin Dimension of RIL's Diversification

While Russian crude has received the most attention in coverage of Reliance's procurement strategy, the Venezuelan dimension represents a structurally distinct and arguably underappreciated element of the Reliance Industries crude sourcing from Russia and Latin America thesis. The Venezuelan oil market impact on global pricing dynamics has, in addition, made Latin American barrels increasingly relevant to Asian procurement decisions.

Venezuelan Merey is a heavy, high-sulphur crude grade with API gravity typically in the range of 16 to 18 degrees and sulphur content around 2.3 percent. These physical characteristics place it in a category that most refineries globally cannot process efficiently, which is precisely why it trades at a structural discount to lighter benchmarks. For a refinery with Jamnagar's coking capacity, however, this discount represents a margin capture opportunity rather than a yield risk.

How Reliance Legally Structured Its Venezuelan Procurement

Venezuela has been subject to layered U.S. sanctions since 2019, creating a complex compliance environment for buyers. Reliance navigated this through a multi-step legal and operational framework:

| Step | Mechanism | Timeline | Volume |

|---|---|---|---|

| OFAC Special License | U.S. government authorisation for direct PDVSA imports | Pre-2026 | Framework authorisation |

| Indirect purchase via trader | Spot cargo acquisition through Vitol | February 2026 | 2 million barrels (April delivery) |

| Direct PDVSA loading | Cargo loaded at Jose Terminal, Venezuela | April 2026 | 2 million barrels (Merey grade) |

| Product-for-crude swaps | Refined products delivered to Venezuela in exchange for crude | Ongoing | Variable |

The product-for-crude swap mechanism deserves particular attention as it is less commonly understood. Under this structure, Reliance delivers approved refined products, including diesel, to Venezuela in exchange for crude barrels. The arrangement is explicitly permitted under the U.S. sanctions framework because it serves Venezuela's domestic fuel supply needs, which U.S. policy has sought to protect even as it restricts revenue flows to the Maduro government.

It is also worth noting that before the October 2025 Rosneft sanctions tightened the structure, some of Reliance's historical Venezuelan crude access had been routed indirectly through Rosneft, which held significant debt repayment rights against PDVSA. The shift to direct engagement with PDVSA consequently represents both a compliance adaptation and a supply chain simplification.

O2C Segment Performance: Reading the Numbers in Context

The financial outcomes of Reliance's procurement strategy during the June 2026 quarter reflect the interplay of feedstock advantages and countervailing cost pressures, producing results that require careful interpretation.

| Metric | June Quarter 2026 | Year-on-Year Change |

|---|---|---|

| O2C EBITDA | Rs 17,010 crore | +17.2% |

| Consolidated Revenue | Rs 3.4 lakh crore | +24.5% |

| Brent Crude Average | $104.5/bbl | +$36.7/bbl |

| Hormuz Disruption Volume | ~13 million bpd | New disruption event |

The 17.2 percent year-on-year increase in O2C EBITDA occurred despite several simultaneous headwinds that would have materially compressed results for a less well-positioned refiner:

- High physical crude premiums on spot barrels in disrupted markets inflated feedstock costs above headline Brent levels for buyers without pre-established term supply.

- Elevated freight and insurance costs on longer alternative routing eroded per-barrel economics on Russian and Venezuelan supply.

- The reintroduction of the Special Additional Excise Duty (SAED) on diesel, petrol, and aviation turbine fuel compressed domestic refining margins.

- Domestic retail fuel prices were held steady to protect consumers, generating under-recoveries in fuel retailing that absorbed margin that would otherwise have flowed to the O2C segment.

- Propane and butane feedstocks were diverted toward LPG production, reducing petrochemical feedstock availability and constraining downstream margin capture.

Against this backdrop, the positive drivers were record middle distillate crack spreads, improved downstream petrochemical margins, favourable ethane cracking economics, and the planned turnaround timing of the crude distillation unit and coker unit, which limited the throughput impact by scheduling maintenance during a period of constrained feedstock availability.

Completing major refinery maintenance during periods of elevated crude price and feedstock disruption is a sophisticated operational timing decision. By scheduling the CDU and coker turnarounds during the Hormuz disruption quarter, Reliance effectively converted a forced throughput constraint into a planned maintenance window, minimising the opportunity cost of the downtime.

The next major ASX story will hit our subscribers first

How Reliance's Approach Compares to Other Asian Refining Giants

The competitive positioning of Reliance's crude diversification strategy becomes clearer when mapped against the strategies of comparable Asian refiners:

| Refiner | Russian Crude Exposure | Venezuelan Crude Access | Core Alternative Strategy |

|---|---|---|---|

| Reliance Industries (India) | High, 10-year Rosneft framework, ~150,000 bpd current | Active, licensed direct purchases and swap deals | Russia plus Latin America dual-corridor |

| Indian Oil Corporation | Moderate, primarily spot and short-term term | Limited | Middle East plus U.S. crude diversification |

| Sinopec (China) | Very high, multiple long-term frameworks | High, PDVSA equity participation | China-Russia-Venezuela triangle |

| SK Energy (South Korea) | Low, sanctions-compliant posture maintained | Minimal | Middle East plus U.S. light tight oil |

Reliance occupies a distinctive middle position: more deeply engaged with alternative supply corridors than other Indian refiners, but operating within a compliance framework that differentiates it from Chinese majors that face fewer secondary sanction constraints. This positioning gives Reliance cost advantages that IOC and BPCL cannot easily replicate without comparable legal and procurement infrastructure. According to Reuters, Reliance would likely pivot back to Middle Eastern supply if Russian volumes became unavailable, further illustrating the layered nature of its procurement strategy.

Three Scenarios for the Russia-Latin America Crude Axis Going Forward

The following scenarios involve forecasts and assumptions that carry inherent uncertainty. They should not be interpreted as investment advice or definitive predictions.

Scenario One: Geopolitical Normalisation

If Middle East tensions ease and the Strait of Hormuz returns to full operational capacity, Arabian Gulf crudes will regain competitive pricing relative to longer-haul alternatives. However, the 10-year Rosneft supply agreement ensures that Russian crude remains a structural component of Jamnagar's feedstock slate regardless of regional de-escalation. The Russia-Latin America axis would likely recede in relative importance without disappearing entirely.

Scenario Two: Sustained Disruption and Expanded Alternative Sourcing

Prolonged Middle East instability could entrench the current diversification architecture as the dominant feedstock model, potentially incentivising Reliance to expand Venezuelan import volumes beyond existing licence parameters and pursue additional waiver authorisations. This scenario would also accelerate the supply learning curve for other Indian refiners seeking to replicate Reliance's alternative corridor access. The broader trade war oil markets effect further complicates the pricing environment for any refiner attempting to lock in stable feedstock costs.

Scenario Three: Escalated Sanctions Environment

Further tightening of U.S. secondary sanctions targeting Russian and Venezuelan crude trade could narrow the compliance pathways that Reliance currently navigates. This would force a material shift back toward Middle Eastern and African alternatives, likely at significantly higher cost during a period of already elevated Brent pricing, creating a meaningful margin compression risk for the O2C segment.

What This Means for India's Broader Energy Import Geography

The Reliance Industries crude sourcing from Russia and Latin America model is not operating in isolation. Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum have all incrementally increased Russian crude intake since 2022, though none has matched the scale or institutional depth of Reliance's engagement. The pattern suggests that India's refining sector as a whole is undergoing a structural reorientation of its import geography that extends well beyond a single company's procurement decisions.

The institutionalisation of long-term Russia-India crude trade through multi-year contracts represents a durable shift that is unlikely to reverse quickly even if short-term geopolitical conditions change. Similarly, the establishment of compliant Venezuelan crude import frameworks by sophisticated buyers like Reliance creates a template that other licenced importers can follow, potentially broadening Latin American crude flows into Asia over the medium term.

For investors and energy market observers, the core lesson from Reliance's June 2026 quarter performance is that feedstock flexibility is not merely an operational feature; it is a financial asset that generates measurable returns during periods of market disruption, and the cost of building that flexibility is most apparent when it is absent.

Want to Track the Next Major Resource Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex resource data into actionable investment insights — explore historic discoveries and their returns to understand what early positioning can mean for a portfolio, then start a 14-day free trial at Discovery Alert to gain a market-leading edge on the next major find.