June 8, 2026

The global gold mining landscape continues to evolve as production costs fluctuate and operational complexities intensify across major producing regions. Mining companies face mounting pressure to optimise asset portfolios while maintaining competitive cost structures amid volatile input prices and regulatory challenges. Understanding how individual operators navigate these dynamics provides valuable insight into broader industry trends and investment opportunities, particularly when examining Resolute Mining full-year guidance targets for 2026.

Understanding Resolute's Strategic Position in Global Gold Production

What Makes Resolute Mining's Full-Year Guidance Significant for Investors?

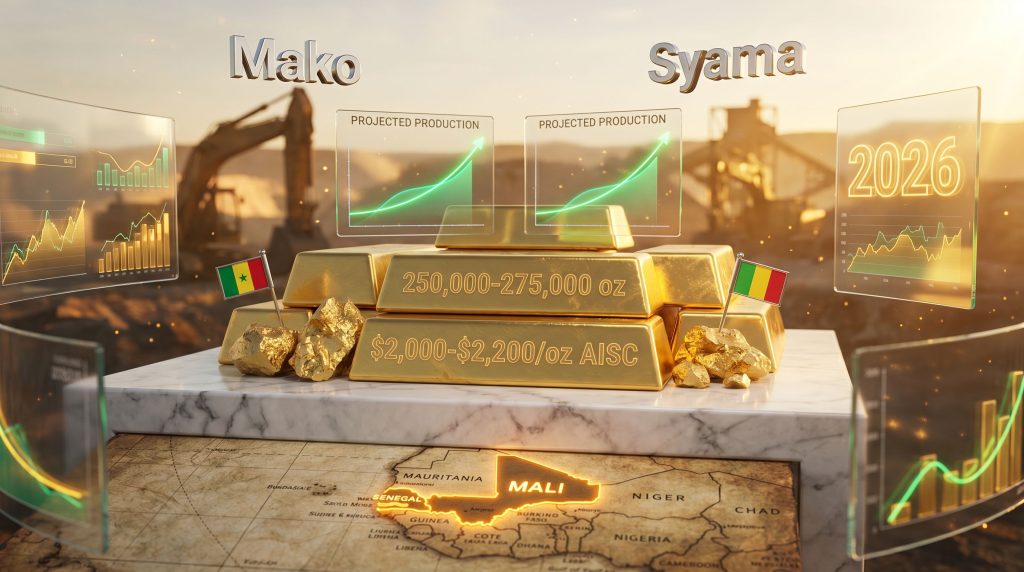

The mining company's 250,000-275,000 ounce production target for 2026 represents a substantial increase from previous performance levels, positioning the operation among mid-tier gold producers globally. This guidance framework, combined with all-in sustaining costs (AISC) projections of $2,000-$2,200 per ounce, places operational efficiency within competitive benchmarks for West African mining operations.

First quarter 2026 results demonstrate the company's tracking toward these targets, with 59,603 ounces produced at an AISC of $2,210 per ounce. The quarterly performance generated $119.8 million in operating cash flow before capital expenditure and exploration investments, supported by a robust net cash position of $315.4 million.

Management's confidence in achieving Resolute Mining full-year guidance stems from operational visibility rather than optimistic projections. CEO Chris Eger emphasised that production targets remain weighted toward the second half of 2026, coinciding with the commissioning and ramp-up of the Syama sulphide conversion project. This timeline-specific approach reflects sophisticated project management rather than evenly distributed quarterly expectations.

The balance sheet strength provides strategic flexibility during operational transitions, with cash, cash equivalents, and bullion totalling $327.6 million as of March 2026. This financial positioning enables sustained capital investment without external financing dependencies, particularly critical during the Syama conversion phase when operational cash flows may experience temporary volatility.

How Do Current Market Conditions Support Resolute's Guidance Confidence?

Gold price dynamics in early 2026 have created both opportunities and challenges for mining operations. Record-high realised gold prices during the first quarter enhanced revenue generation but simultaneously triggered elevated royalty payments across West African jurisdictions, demonstrating the complex relationship between commodity prices and operational economics. This environment has contributed to the current historic gold price surge, which affects all market participants.

The company's AISC of $2,210 per ounce in Q1 2026 reflects this dynamic, as cost reductions partially offset higher royalty payments resulting from premium gold pricing. This illustrates how mining companies must balance operational efficiency improvements against commodity-linked cost escalation mechanisms embedded in regulatory frameworks.

Geopolitical factors continue influencing operational planning, though direct supply chain disruptions remain limited. Middle East conflicts have not created immediate logistical challenges, but management maintains heightened monitoring of fuel price volatility and potential supply chain complications. Rising fuel costs represent a potential catalyst for increased AISC in subsequent quarters, requiring proactive risk management protocols.

Currency considerations across multi-jurisdictional operations add complexity to cost projections, with exposure to CFA franc fluctuations and USD-denominated input costs creating additional variables in AISC calculations. The company's operations spanning Senegal, Mali, and Côte d'Ivoire require sophisticated hedging strategies to manage exchange rate volatility. Furthermore, comprehensive gold market technical analysis reveals these currency dynamics form part of broader market complexities.

When big ASX news breaks, our subscribers know first

Operational Excellence Framework: Breaking Down Production Targets

What Drives Mako's Stockpile Processing Strategy in Senegal?

The Mako operation's transition to stockpile processing targeting 55,000-65,000 ounces annually represents an asset monetisation strategy optimised for mature mining infrastructure. This approach generates substantial cash flows with projected AISC of $1,600-$1,800 per ounce, positioning Mako among the lowest-cost producers globally.

Stockpile processing performance during Q1 2026 exceeded expectations, maintaining operational continuity while technical teams advance the Mako Life Extension Project (MLEP). Internal studies indicate potential for 75,000-85,000 ounces annually over seven years from the Tomboronkoto and Bantaco deposits, requiring capital investment of $125-150 million for underground conversion.

The strategic value of stockpile processing extends beyond immediate cash generation, providing operational stability during the MLEP permitting and optimisation phase. This dual-track approach ensures revenue continuity while developing longer-term production capacity, demonstrating sophisticated asset lifecycle management.

Technical optimisation continues across processing circuits, with management expressing confidence in further project improvements. The MLEP represents a fundamental shift from open-pit to underground mining methodologies, requiring specialised equipment, modified processing protocols, and enhanced safety systems.

Key Mako Performance Metrics:

• Stockpile processing efficiency exceeding Q1 expectations

• AISC positioning in lowest global cost quartile

• Seven-year production timeline for MLEP underground conversion

• $125-150 million capital requirement for life extension

• 75,000-85,000 ounce annual production target post-conversion

How Will Syama's Sulphide Conversion Project Transform Mali Operations?

The Syama sulphide conversion represents the most significant operational transformation within Resolute's portfolio, targeting 195,000-210,000 ounces during the commissioning and ramp-up phase. This transition from oxidised ore processing to primary sulphide metallurgy involves complex technical challenges and substantial capital investment.

Projected AISC of $1,950-$2,150 per ounce during the commissioning phase reflects the operational complexities of sulphide ore processing, including higher reagent consumption and potentially lower initial recovery rates. These cost dynamics typically improve as processing teams optimise metallurgical protocols and achieve nameplate throughput capacity.

The H2 2026 weighting of production guidance directly correlates with Syama's commissioning timeline, indicating management visibility on technical milestones and ramp-up trajectories. Underground mining transitions require systematic optimisation of:

• Reagent consumption protocols for primary sulphide leaching

• Gravity separation and flotation circuit modifications

• Recovery rate optimisation during operational learning phases

• Throughput scaling to achieve nameplate processing capacity

Sulphide ore processing demands more sophisticated metallurgical approaches compared to oxidised ores, typically involving cyanide or thiosulfate leaching systems with enhanced environmental controls. The commissioning phase requires careful monitoring of recovery rates, reagent efficiency, and overall processing throughput.

Risk mitigation strategies for the Syama conversion include phased commissioning protocols, experienced technical teams, and financial reserves to manage potential timeline extensions or cost overruns. The project's success directly impacts Resolute's achievement of Resolute Mining full-year guidance and long-term operational sustainability.

Capital Allocation Strategy: Investment Framework Analysis

Where Is Resolute Directing Growth Capital for Maximum Returns?

Capital expenditure during Q1 2026 totalled $33.4 million, with strategic allocation across sustaining operations, growth projects, and exploration initiatives. The quarterly spending breakdown demonstrates balanced investment priorities:

Q1 2026 Capital Expenditure Distribution:

| Category | Amount (USD Million) | Strategic Purpose |

|---|---|---|

| Non-sustaining | $14.3 | Capacity expansion |

| Sustaining operations | $6.9 | Operational continuity |

| Exploration | $5.1 | Resource base development |

| Doropo & MLEP combined | $7.1 | Future production platforms |

The Doropo project in Côte d'Ivoire represents the company's most significant growth investment, with first gold production targeted for H2 2028. Achieving major milestones during Q1 2026, including receipt of the mining permit and final investment decision approval, demonstrates project advancement through critical regulatory phases.

Ground clearance activities commenced in April 2026, indicating operational momentum toward construction and development phases. The Doropo investment signals long-term commitment to West African operations and geographic diversification across established mining jurisdictions.

Doropo Development Timeline:

• Q1 2026: Mining permit received and final investment decision approved

• April 2026: Ground clearance activities initiated

• H2 2028: First gold production target

• Integration with existing West African operational footprint

What Does the ABC Project Signal About Long-Term Strategy?

The ABC project in Côte d'Ivoire demonstrates Resolute's systematic approach to resource base expansion, with an existing mineral resource estimate of 2.2 million ounces across the Kona South and Central deposits. Recent drilling results, including 73 metres grading 0.8 grams per tonne from surface, indicate potential for resource expansion beyond current estimates.

A scoping study based on the existing mineral resource estimate commenced during Q1 2026, with results expected in Q2 2026. This technical analysis will provide initial economic parameters and development timelines for potential future production capacity.

Strategic focus on strike extensions of known deposits reflects disciplined exploration methodology, targeting areas with established geological understanding and infrastructure proximity. This approach minimises exploration risk while maximising potential for resource base enhancement.

The ABC project complements Doropo development within Côte d'Ivoire, creating potential for operational synergies and shared infrastructure utilisation. Regional concentration of development projects enables economies of scale in logistics, procurement, and technical expertise deployment.

Financial Performance Trajectory: From Historical Results to Future Projections

How Do 2025 Results Validate Management's Operational Capabilities?

The 2025 operational performance of 176.3 thousand ounces at $2,008 per ounce AISC demonstrates management's ability to meet guidance parameters and maintain cost discipline. Revenue generation of $865.6 million during 2025 provides a baseline for evaluating 2026 projections and growth trajectories.

Comparative Performance Evolution:

• 2025 Actual: 176.3 koz production, $2,008/oz AISC

• 2026 Target: 250,000-275,000 oz (42-56% increase)

• Projected revenue progression to approximately $1,313 million

• Foundation for 36% projected earnings growth through operational leverage

The substantial production increase target relies primarily on Syama's sulphide conversion contribution rather than across-the-board operational improvements. This concentrated growth approach carries both opportunities and risks, with execution success determining overall guidance achievement.

Financial metrics indicate strong cash generation capabilities, with Q1 2026 operating cash flow of $119.8 million before capital expenditure representing robust underlying profitability. The company's ability to self-fund growth investments while maintaining dividend capacity demonstrates mature cash flow management. Additionally, industry CEOs' gold insights suggest this performance aligns with sector leadership expectations.

What Factors Enable Projected Earnings Growth?

Operational leverage represents the primary driver of projected earnings expansion, with production increases generating proportionally higher revenue growth due to relatively fixed operational cost structures. The 42-56% production increase target creates significant earning potential assuming successful Syama commissioning.

Cost efficiency improvements across the asset portfolio contribute to margin expansion, particularly through Mako's low-cost stockpile processing and optimised logistics networks. These operational enhancements compound the impact of higher production volumes on overall profitability.

Market timing advantages from elevated gold price environments provide additional earnings support, though commodity price volatility introduces uncertainty into financial projections. Current gold pricing near $2,420-$2,450 per ounce creates favourable revenue assumptions if sustained throughout 2026. However, the broader gold price forecast indicates potential volatility requires careful planning.

Earnings Growth Catalysts:

• Operational leverage from 167% increase in production run-rate

• Cost efficiency gains from optimised processing circuits

• Premium gold price realisation in current market environment

• Financial leverage from debt-free balance sheet structure

Regional Market Impact: West African Gold Sector Positioning

How Does Resolute's Expansion Affect Regional Supply Dynamics?

West African gold production continues gaining significance within global supply chains, with established mining jurisdictions offering regulatory stability and infrastructure development opportunities. Resolute's expansion across Senegal, Mali, and Côte d'Ivoire contributes to regional production capacity while supporting local economic development.

The company's multi-jurisdictional approach provides geographic diversification benefits and reduces political risk exposure compared to single-country operations. This strategy aligns with broader industry trends toward portfolio diversification across stable African mining jurisdictions.

Infrastructure development contributions extend beyond direct mining operations, including road improvements, power system upgrades, and logistics network enhancements that benefit broader regional economies. These investments create lasting value beyond mine life cycles and strengthen community relationships.

Competitive positioning relative to major regional producers requires continuous operational optimisation and cost management discipline. The company's AISC targets position operations competitively within West African benchmarks while maintaining profitability margins. Furthermore, understanding mining equities impact helps contextualise regional competitive dynamics.

What Role Does Guinea Exploration Play in Long-Term Strategy?

The strategic memorandum of understanding with Nimba Mining Company for Guinea project evaluation represents geographic expansion into an additional West African jurisdiction. This partnership approach reduces exploration risk while providing access to prospective geological terrain.

Guinea's mineral endowment and exploration potential offer long-term growth opportunities beyond current operational assets. The country's geological formations, similar to productive gold regions in neighbouring countries, suggest potential for significant resource discovery and development.

Pipeline development for sustained growth beyond current assets requires systematic exploration investment and technical expertise deployment. The Guinea initiative demonstrates management's commitment to maintaining long-term production growth potential through strategic partnerships.

Guinea Exploration Strategic Elements:

• Partnership approach reducing individual company risk exposure

• Access to underexplored geological terrain with regional similarities

• Long-term production pipeline development beyond current assets

• Geographic diversification within West African mining corridor

Risk Management Framework: Navigating Operational Challenges

How Is Resolute Addressing Geopolitical and Supply Chain Risks?

Current geopolitical developments, particularly Middle East conflicts, require enhanced monitoring protocols despite minimal direct operational impact to date. Supply chain resilience depends on diversified sourcing strategies and proactive contingency planning for potential disruptions.

Fuel price volatility represents a more immediate operational concern, with rising costs potentially impacting AISC projections in subsequent quarters. Management has implemented proactive risk management protocols, though specific hedging strategies or cost mitigation measures remain undisclosed.

Multi-jurisdictional operational benefits include risk diversification across Senegal, Mali, and Côte d'Ivoire, reducing dependence on any single regulatory environment or political system. This geographic spread provides operational flexibility during localised challenges or policy changes.

Key Risk Mitigation Strategies:

• Continuous monitoring of Middle East conflict impacts on supply chains

• Proactive fuel price management protocols

• Geographic diversification across three West African countries

• Financial reserves providing operational flexibility during volatility periods

What Contingency Plans Support Guidance Reliability?

Operational flexibility across Senegal and Mali assets enables production balancing during temporary disruptions or optimisation periods. The ability to adjust processing schedules and resource allocation between operations provides management tools for maintaining overall guidance parameters.

Cost management protocols address volatile input pricing through strategic procurement practices and operational efficiency improvements. These systems help offset external cost pressures while maintaining AISC targets within guidance ranges.

Production scheduling optimisation allows management to time market delivery for optimal pricing conditions while maintaining operational continuity. This flexibility proves particularly valuable during commodity price volatility or seasonal demand fluctuations.

Financial reserves totalling $315.4 million net cash provide substantial contingency capacity for managing unexpected operational challenges, equipment requirements, or market disruptions. This financial strength enables sustained operations during temporary setbacks while maintaining investment capacity for growth projects.

The next major ASX story will hit our subscribers first

Investment Implications: Analyst Expectations vs. Management Targets

Why Are Analyst Forecasts Aligned with Company Guidance?

Professional analyst projections of $362 million earnings and $1,313 million revenue targets demonstrate broad consensus supporting management's production and cost guidance parameters. This alignment suggests market confidence in operational capabilities and project execution timelines.

Revenue growth assumptions supporting the $1,313 million target rely primarily on production volume increases rather than commodity price appreciation, providing more conservative modelling approaches. This methodology reduces sensitivity to gold price volatility while emphasising operational execution importance.

Production cost modelling validation across operational assets incorporates both current performance data and projected efficiency improvements from Syama commissioning. Analyst models appear to account for commissioning-phase cost elevations while projecting optimisation benefits over time.

Consensus Modelling Factors:

• Production volume leverage as primary revenue growth driver

• Conservative commodity price assumptions reducing market risk

• AISC progression modelling through Syama commissioning phases

• Balance sheet strength supporting dividend sustainability and growth investment

What Metrics Should Investors Monitor for Guidance Achievement?

Quarterly production milestone tracking provides the most direct indicator of guidance achievement, particularly Syama's commissioning progress and production ramp-up timing. Deviations from expected quarterly contributions could signal timeline adjustments or technical challenges.

AISC trend analysis relative to guidance ranges offers insight into cost management effectiveness and operational efficiency improvements. Sustained performance above guidance ranges may indicate systematic cost pressures requiring management attention.

Capital expenditure deployment efficiency measures determine whether growth investments achieve expected returns within projected timelines. Monitoring actual spending against budgets and milestone achievement provides early indicators of project execution success.

Critical Performance Indicators:

• Quarterly production distribution relative to H2-weighted guidance

• AISC performance within $2,000-$2,200 per ounce range

• Syama commissioning milestones and ramp-up trajectory

• Capital spending efficiency against budget allocations

• Cash flow generation supporting dividend sustainability

Market Outlook: Positioning for Strategic Performance

How Do Current Gold Market Fundamentals Support Resolute's Strategy?

Central bank demand patterns continue supporting gold price stability, with institutional accumulation providing underlying market strength beyond speculative trading activity. This demand foundation creates favourable pricing environments for production planning and revenue projections.

Industrial demand growth from technology sector applications, particularly in electronics and renewable energy systems, adds fundamental support to gold consumption patterns. These applications create demand sources less sensitive to economic cycles compared to traditional jewellery markets.

Currency debasement trends across major economies enhance precious metals allocation appeal among institutional investors and sovereign wealth funds. This macroeconomic environment supports sustained gold price premiums relative to historical averages.

Market Support Factors:

• Sustained central bank accumulation across diverse jurisdictions

• Technology sector demand growth in industrial applications

• Currency debasement supporting precious metals allocation strategies

• Geopolitical uncertainty driving safe-haven demand characteristics

What Catalysts Could Drive Outperformance Relative to Guidance?

Earlier-than-expected Syama ramp-up completion would accelerate production contributions and potentially enable guidance range outperformance. Technical optimisation successes during commissioning could compress the learning curve and enhance operational efficiency.

Doropo development timeline acceleration opportunities exist given strong project momentum and regulatory milestone achievement. Earlier production startup would provide additional cash flow generation and enhanced asset portfolio diversification.

Exploration success expanding resource base assumptions could drive long-term value appreciation beyond current operational projections. Particularly promising developments at ABC or through Guinea partnerships might enhance strategic positioning and growth potential.

Outperformance Catalysts:

• Accelerated Syama commissioning and recovery rate optimisation

• Doropo timeline advancement through regulatory efficiency

• Resource base expansion through exploration successes

• Strategic partnerships creating operational synergies and cost reductions

Investment decisions should consider operational execution risks, commodity price volatility, and geopolitical factors affecting West African mining operations. This analysis does not constitute financial advice and investors should consult qualified professionals before making investment decisions.

Ready to Capitalise on the Next Major Gold Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring how major finds transform company valuations, then begin your 14-day free trial today to position yourself ahead of the market.