May 12, 2026

The Hidden Complexity Behind Every Kilogram of Copper

Most conversations about copper's role in the energy transition focus on volume. How many millions of tonnes will electric vehicles require? How much conductor material will offshore wind farms consume? These are legitimate questions, but they increasingly miss the deeper structural shift reshaping the metal's commercial landscape. The more consequential question for copper producers, traders, manufacturers, and investors in 2026 is not one of quantity alone. It is one of origin, process, and accountability.

Responsible mineral supply chains in copper have moved from a niche ESG consideration to a hard commercial and regulatory requirement. The entities writing procurement contracts today, from EV manufacturers to grid infrastructure developers to institutional capital allocators, are embedding sourcing standards into legally binding supplier agreements. In this environment, a tonne of copper from an audited, certified, low-emissions mine is not the same commercial product as a tonne from an undocumented source. The divergence in market access between these two categories is widening, and it is widening fast.

When big ASX news breaks, our subscribers know first

Why Copper's Identity Has Fundamentally Changed

For most of modern industrial history, copper was assessed in markets primarily by grade, form, and price. Cathode was cathode. Rod was rod. Today, the identity of copper as a material has expanded to include the conditions under which it was produced, the emissions intensity of its processing, the governance environment of its country of origin, and its verifiable recycled content percentage. This is not sentiment. It is procurement policy.

The ICA CEO Juan Ignacio Diaz articulated this trajectory clearly during the Future Minerals Forum's panel session titled Let us be known by our deeds: How to scale up transparency and responsible mineral supply? The session, which brought together representatives from the London Metal Exchange, the Extractive Industries Transparency Initiative (EITI), the Global Battery Alliance, and the OECD, reinforced a point that is becoming increasingly difficult to dispute: the copper sector's transformation from purely extractive to genuinely transformative depends on whether accountability frameworks can scale at the same pace as demand.

As Diaz noted during the discussion, the copper industry's significance goes well beyond resource extraction. Copper is integral to the infrastructure of a decarbonising world, from EV powertrains and battery management systems to offshore wind transmission and urban digital grids. Framing the industry's responsibility in those terms resets the accountability bar. Furthermore, understanding broader copper market trends helps contextualise why these accountability frameworks are becoming commercially indispensable.

What Responsible Mineral Supply Chains in Copper Actually Require

The phrase "responsible sourcing" carries enough definitional vagueness that it risks becoming meaningless unless anchored to specific, auditable pillars. In copper's context, four domains collectively define what responsible supply chains actually look like in practice.

Environmental Stewardship

This encompasses measurable emissions reduction across Scope 1 and 2 operations, water recycling rates in water-stressed mining regions, land rehabilitation commitments post-closure, and tailings management standards. In arid copper-producing regions like northern Chile, water scarcity is not a future risk; it is an operational reality that directly affects mine viability and community relations. Mines operating in the Atacama and surrounding zones face meaningful constraints on freshwater use that require significant capital investment in desalination and water recycling infrastructure.

Declining ore grades globally add further complexity. As copper mineralisation at existing deposits thins, more rock must be processed per tonne of copper recovered. This raises energy consumption, water requirements, and waste volumes per unit of output, meaning that environmental intensity increases as accessible ore depletes. This dynamic is not widely appreciated outside the technical mining community, but it materially affects the per-tonne ESG footprint of primary copper production over the life of a mine.

Social Accountability and Community Engagement

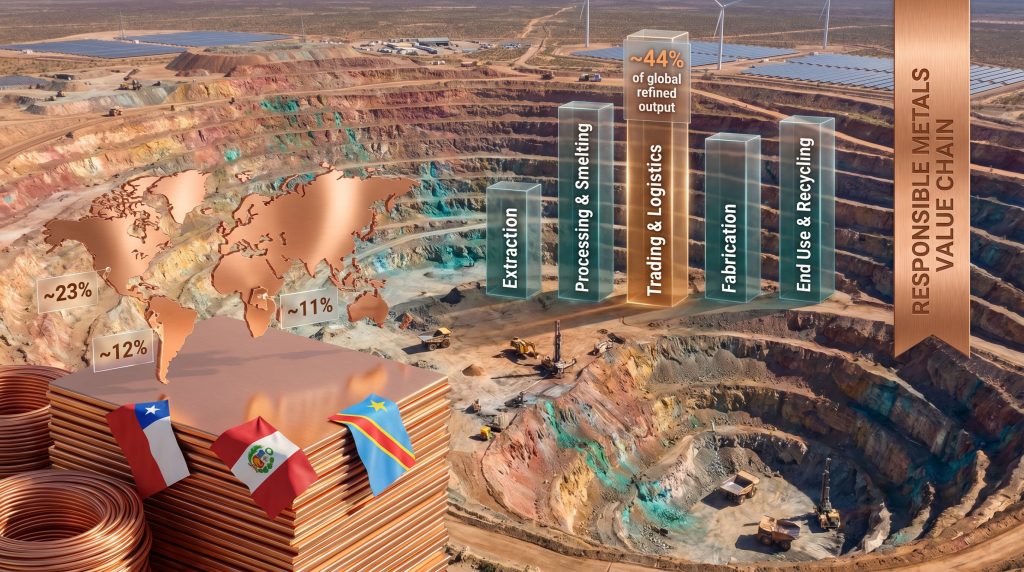

Labour rights, indigenous consultation, community benefit-sharing, and free, prior, and informed consent (FPIC) protocols sit at the core of social accountability in copper mining. Projects that fail to secure and maintain community consent face permit suspension, operational blockades, and reputational damage that extends to downstream buyers. Peru's production record, representing approximately 12% of global output, has been periodically interrupted by community opposition events that demonstrate how social licence failures translate into direct supply chain disruption.

Governance Transparency

Anti-corruption frameworks, beneficial ownership disclosure, and conflict financing risk management constitute the governance pillar. This is particularly acute in high-risk jurisdictions like the Democratic Republic of Congo (DRC), which contributes roughly 11% of global copper output but is designated a conflict-affected and high-risk area (CAHRA) under the OECD's Due Diligence Guidance. For buyers with EU-facing supply chains, compliance with CAHRA provisions is not optional.

Circular Economy Integration

Copper's near-infinite recyclability without degradation in material quality gives it a unique circular economy profile. A significant proportion of all copper ever mined remains in productive use today, embedded in building wiring, industrial equipment, and transport infrastructure. The energy required to recycle copper is substantially lower than primary smelting, and secondary production carries meaningfully lower ESG exposure at the extraction stage. For downstream buyers, specifying recycled content thresholds alongside ESG certifications is becoming a standard procurement practice rather than an aspirational target.

The Geographic Risk Landscape: Where Production Concentrates and Where Accountability is Tested

Responsible mineral supply chains in copper cannot be assessed without understanding the geographic distribution of both production and refining, and the specific risk profiles each jurisdiction presents.

| Country / Region | Share of Global Output | Primary ESG Risk Exposure | Responsible Sourcing Complexity |

|---|---|---|---|

| Chile | ~23% (mined) | Water scarcity, declining ore grades | Moderate |

| Peru | ~12% (mined) | Political instability, community conflict | High |

| DRC | ~11% (mined) | Governance deficits, conflict financing, ASM | Very High |

| Indonesia | ~5-7% (mined) | Environmental permitting, land rights | High |

| United States | ~5% (mined) | Regulatory delays, social licence | Moderate |

| China | ~44% (refined) | Traceability, geopolitical concentration | High |

The Chile copper outlook reflects how water scarcity and ore grade decline are creating long-term structural pressures on what remains the world's single largest producing nation. China's outsized role in refining, accounting for approximately 44% of global refined copper output, creates a structural vulnerability for downstream buyers seeking traceable, diversified responsible supply. A manufacturer in Germany or the United States sourcing copper cathode through conventional channels may find that the majority of that material passed through a Chinese smelter with limited chain-of-custody documentation.

Artisanal and small-scale mining (ASM) adds a further layer of complexity that is rarely understood by non-specialist audiences. In DRC, Peru, and Indonesia, ASM operators produce copper outside formal regulatory frameworks, creating both a human rights risk and a traceability gap for downstream supply chains. However, ASM is not simply a risk vector; it also represents a formalization opportunity. Programmes that connect ASM operators to the CRAFT Code compliance pathway and Conflict Minerals Reporting Template (CMRT) documentation systems can bring informal production into certified supply chains, creating commercial incentives for responsible practices at the mine face.

The Framework Ecosystem: How Certification and Audit Are Reshaping Accountability

Multiple overlapping frameworks are now shaping what responsible mineral supply chains in copper look like in practical terms. Understanding how they interact, and where gaps remain, is essential for producers seeking market access and buyers navigating due diligence obligations.

| Framework | Governance Type | Primary Coverage | Verification Method |

|---|---|---|---|

| Copper Mark | Industry-led | Value chain ESG, traceability | Third-party site audits |

| RMI RMAP | Industry-led | Smelter and refiner conformance | Third-party audits |

| IRMA | Multi-stakeholder | Community and environment | Independent audits |

| OECD Guidance | Intergovernmental | Conflict risk, human rights | Self-assessment and audits |

| EU CRMA | Regulatory | Strategic supply security | Regulatory compliance |

The Copper Mark and Value Chain Accountability

The Copper Mark has established coverage across approximately 40% of mined copper ore and around 30% of refined copper globally, operating through third-party site audits that assess ESG performance against defined criteria. Its responsible metals value chain platform connects mines, smelters, fabricators, and OEMs into a single accountability ecosystem that consolidates GHG accounting, chain-of-custody verification, human rights due diligence, and recycled content transparency.

A critical but underappreciated aspect of the Copper Mark's design is that its Responsible Value Chain Charter uses exclusive forum access and dedicated analytical tooling as commercial incentives for producer participation. This market-facing mechanism is deliberately designed to make responsible sourcing certification a business advantage rather than a compliance cost, which changes the incentive structure for smaller producers who might otherwise defer ESG investment.

RMI and Downstream Sourcing Discipline

The Responsible Minerals Initiative's Responsible Minerals Assurance Process (RMAP) provides publicly accessible conformant smelter and refiner lists that function as a reference tool for downstream due diligence. Manufacturers incorporating RMAP into their procurement policies can verify that their metal inputs come from audited facilities. The Downstream Assessment Program (DAP) extends this discipline further upstream by encouraging manufacturers to mandate RMAP-conformant sourcing and require Conflict Minerals Reporting Template (CMRT) documentation across their supplier base.

IRMA: The Community-Centred Standard

The Initiative for Responsible Mining Assurance applies more than 400 audit requirements covering environmental, social, and governance dimensions, with a governance structure specifically designed to give affected communities and civil society verifiable oversight rather than limiting accountability to industry self-assessment. IRMA's independence from direct industry control distinguishes it from other frameworks and provides a higher credibility signal for socially engaged investors and community advocates.

The OECD Five-Step Framework as Regulatory Baseline

The OECD Due Diligence Guidance establishes a five-step process that is increasingly referenced by regulatory bodies as a minimum compliance baseline:

- Establish strong management systems for supply chain due diligence

- Identify and assess actual and potential risks in the supply chain

- Design and implement risk mitigation strategies

- Commission independent third-party audits where appropriate

- Report annually on supply chain due diligence activities

For companies with EU operations or EU-market exposure, alignment between OECD guidance and EU Critical Raw Materials Act obligations creates a compliance convergence that effectively mandates adoption of this framework across the copper value chain.

How Each Segment of the Value Chain Is Responding

Upstream: Mines and Smelters

ICA member companies are investing significantly in renewable energy integration at mine sites, water recycling infrastructure, and tailings management systems to reduce Scope 1 and 2 emissions intensity. The pace of this transition varies considerably by jurisdiction, with Chilean operators generally further advanced than peers in DRC or Indonesia, reflecting both regulatory environment and capital access differences.

At the smelting stage, co-investment in traceability infrastructure allows operators to demonstrate CRAFT Code compliance for ASM-sourced material. Traders are increasingly mapping ASM supply origins as a risk mitigation strategy, a practice that was negligible five years ago but is now commercially necessary for any operator serving European or North American buyers. In addition, Chile's copper supply gap is accelerating investment in responsible sourcing infrastructure as the nation seeks to maintain its competitive position with downstream buyers who impose stricter ESG requirements.

Downstream: Manufacturers and Technology Buyers

EV manufacturers and electronics OEMs are embedding copper sourcing requirements into supplier codes of conduct, specifying RMAP conformance and CMRT documentation as minimum standards. Multi-year premium contracts structured to reward responsible producers are beginning to create upstream investment signals: a certified mine can lock in longer-term off-take with better pricing visibility, while an uncertified competitor may face narrowing market access regardless of price competitiveness.

The Underaddressed Gap: Community and Rights-Holder Engagement

Capacity-building for affected communities, legal support for rights-holders, and genuine audit access for civil society remain underdeveloped in most current frameworks. The risk of replicating extractive-era power imbalances is real when community benefit-sharing is treated as a peripheral compliance checkbox rather than a structural design requirement. Best-practice models are emerging in jurisdictions where FPIC is embedded into project approval processes, but these remain the exception rather than the norm across major producing regions.

The next major ASX story will hit our subscribers first

Policy Architecture: The Regulatory Levers Accelerating Change

EU Critical Raw Materials Act

The CRMA designates copper as a strategic material and establishes domestic processing benchmarks intended to reduce European dependence on concentrated supply from single jurisdictions. European manufacturers are using CRMA compliance obligations as a driver for supply chain diversification, with Copper Mark and RMAP certifications increasingly referenced as alignment tools within compliance documentation.

Development Finance and Bilateral Cooperation

German development cooperation through BMZ-led programmes has been directing traceability investment toward Great Lakes ASM copper in DRC, alongside governance strengthening initiatives in Peru, Mongolia, and DRC. This bilateral development finance approach attempts to de-risk responsible sourcing investment in high-risk jurisdictions, recognising that certification frameworks alone cannot function without baseline governance infrastructure in producing regions.

EITI as Transparency Foundation

EITI membership in producing nations creates the baseline revenue transparency and anti-corruption reporting architecture that underpins broader supply chain due diligence. Where EITI reporting is functioning effectively, it provides downstream buyers with a documented record of fiscal flows and government revenue from extraction activities, which reduces conflict financing exposure at the governance level.

Durable responsible supply chains require a convergence of mandatory regulatory baselines, voluntary industry standards, and targeted development finance support in high-risk producing regions. No single lever is sufficient without the others.

Copper's Circular Economy Case: Secondary Production as a Strategic Supply Tool

Copper's recyclability is among its most strategically significant physical properties. The metal can be recycled repeatedly without any measurable degradation in electrical conductivity or mechanical performance, making it fundamentally different from materials that lose quality through secondary processing cycles.

The energy intensity of recycling copper is substantially below that of primary smelting from ore. This difference in energy consumption per tonne translates directly into lower Scope 2 emissions for buyers who specify recycled content, lower operating costs for secondary processors, and reduced land and water disturbance compared with mining fresh ore. An urban mining strategy — the systematic recovery of copper from end-of-life electronics, retired EV battery systems, demolished building infrastructure, and decommissioned power cables — is emerging as a supply diversification approach that reduces dependence on high-risk primary producing regions.

The Copper Mark's Responsible Metals Value Chain platform is enabling recycled content tracking across complex multi-tier supply chains through chain-of-custody verification systems. For downstream buyers beginning to specify minimum recycled content thresholds alongside ESG certifications, this infrastructure is not a nice-to-have. It is the operational mechanism that makes those specifications auditable and enforceable.

Technology-Enabled Traceability: From Paper Audit to Digital Architecture

The traceability gap between responsible sourcing commitments and operational verification is being addressed through a range of emerging technologies that were largely absent from copper supply chain conversations even three years ago.

- Blockchain and distributed ledger systems are being applied to chain-of-custody documentation, creating tamper-resistant records of provenance, ownership transfer, and certification status from mine gate to fabricator

- Digital product passports embed emissions intensity data, recycled content percentage, and certification status directly into material records that travel with the physical shipment

- Satellite monitoring and remote sensing allow environmental compliance verification at mine sites without requiring physical inspection presence, particularly relevant for remote operations in high-risk jurisdictions

- AI-driven supply chain mapping tools identify undisclosed ASM sources within complex multi-tier supplier networks, surfacing risk before it reaches the buyer's due diligence review

A less widely understood challenge in the framework landscape is compliance fatigue. The proliferation of separate audit requirements, each with different methodologies, reporting formats, and verification schedules, creates significant administrative burden for smaller producers. Integrated platform models that consolidate GHG accounting, human rights due diligence, and traceability into a single coordinated system represent the most commercially viable path to scaling responsible sourcing beyond large-cap operators.

Frequently Asked Questions: Responsible Mineral Supply Chains in Copper

What makes copper a critical mineral for responsible sourcing?

Copper's role as the foundational conductor material for EVs, renewable energy systems, and digital infrastructure places it under the same responsible sourcing scrutiny as battery minerals like cobalt and lithium. The surge in critical minerals demand driven by the energy transition means that sourcing origin and ESG performance now directly affect market access for copper producers.

What is the Copper Mark?

An independently administered responsible production standard covering approximately 40% of mined copper ore globally, verified through third-party site audits against defined ESG criteria.

How does the OECD Due Diligence Guidance apply to copper?

The five-step OECD framework requires companies throughout the copper supply chain to identify, assess, and mitigate risks related to human rights abuses, environmental harm, and conflict financing, with heightened obligations in designated CAHRAs.

What is RMAP?

The Responsible Minerals Assurance Process provides a publicly available list of audited, conformant copper smelters and refiners, allowing downstream manufacturers to verify the responsible sourcing credentials of their metal inputs.

How can ASM be integrated into responsible copper supply chains?

Through formalization support, CMRT documentation systems, CRAFT Code compliance pathways, premium contract structures, and capacity-building programmes that connect ASM operators to certified supply chains.

What are the biggest barriers to responsible copper supply chains?

- Geographic fragmentation of production

- Political instability in key producing nations

- Declining ore grades increasing per-unit environmental intensity

- Heavy concentration of refining capacity in a single jurisdiction

- The cost of multi-framework compliance for smaller operators

The Path to 2030: From Framework to System

The copper industry's responsible sourcing architecture is more developed today than it was five years ago, but the gap between current certification coverage and the scale required to meet energy transition demand remains substantial. Expanding Copper Mark coverage beyond its current 40% share of mined ore, achieving meaningful ASM formalization in DRC, Peru, and Indonesia, and embedding recycled content transparency as a standard procurement requirement across EV and electronics supply chains are the concrete milestones that would define success by the end of this decade.

What the Future Minerals Forum panel made clear, with representatives from across the minerals value chain present, is that this is not a challenge any single actor category can resolve independently. Producers can invest in certification. Buyers can write sourcing requirements into contracts. But without aligned regulatory baselines, development finance in high-risk regions, and community engagement that is structural rather than performative, responsible mineral supply chains in copper will remain aspirational in coverage rather than comprehensive in practice.

The transformation that Juan Ignacio Diaz and the ICA are describing is real and commercially grounded. Copper is not only essential to building a decarbonised world. How that copper is produced, traced, and verified is becoming equally essential to whether that world can be built on terms that are economically stable, environmentally credible, and socially legitimate.

Readers interested in the ICA's broader policy work on responsible production and copper's role in the energy transition can explore the organisation's resource library at internationalcopper.org.

This article contains references to forward-looking projections and coverage targets related to responsible sourcing frameworks. Such projections involve inherent uncertainty and should not be interpreted as guarantees of future outcomes. Readers making investment or procurement decisions should conduct independent due diligence and consult primary source documentation from the relevant certification bodies.

Want to Know Which ASX Copper Explorers Are Making Significant Discoveries Right Now?

As responsible sourcing standards reshape copper's commercial landscape and demand from the energy transition accelerates, identifying early-stage ASX copper discoveries ahead of the broader market has never been more important. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, transforming complex geological data into actionable investment insights — explore the historic returns major copper and mineral discoveries have generated and begin a 14-day free trial to position yourself at the forefront of the next significant find.