June 30, 2026

When Scarcity Drives Strategy: The New Logic of Copper Asset Acquisition

The mining industry has entered a period where the geology of the past is being repriced by the economics of the future. Across the global copper sector, a structural reality is taking hold: the pipeline of genuinely large, development-ready copper deposits has essentially run dry. Rio Tinto raises stake in Los Azules copper project discussions reflect precisely this scarcity-driven logic, where majors are no longer competing primarily for ore in the ground — they are competing for access to ore that can realistically reach production within the next decade.

Furthermore, exploration success rates for world-class discoveries have declined sharply over the past two decades, even as drilling budgets expanded. The underlying copper supply crunch leaves major producers with few credible alternatives for meaningful copper volume growth before the 2030s, making strategic stake-building an increasingly rational response.

When big ASX news breaks, our subscribers know first

The Asset That Cannot Be Replicated

Resource Scale and Why Grade Matters

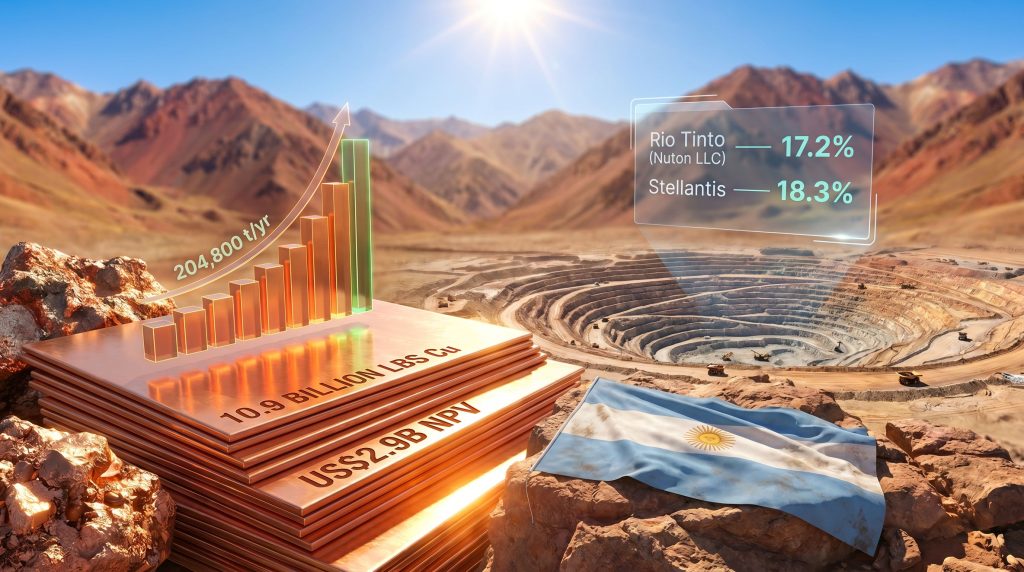

Los Azules sits in San Juan Province, Argentina, at high altitude in the Andes, and its resource profile places it in a category occupied by only a handful of projects globally. The project's indicated resource stands at 10.9 billion pounds of copper at a grade of 0.40% Cu, a figure that meaningfully exceeds the average grade of many comparable porphyry copper systems currently in development.

Copper grade is a critical variable that investors sometimes underweight. For heap-leach processing — the method being evaluated through Rio Tinto's Nuton LLC venture — feed grade has a direct bearing on recoverable metal per tonne of material moved, which in turn drives operating costs and project economics. A grade of 0.40% Cu for an indicated category is considered robust for a large-scale, bulk-tonnage operation.

The project's core metrics are summarised below:

| Metric | Detail |

|---|---|

| Location | San Juan Province, Argentina |

| Indicated Resource | 10.9 billion lbs Cu at 0.40% Cu grade |

| After-Tax NPV (October 2025 Feasibility Study) | US$2.9 billion |

| Average Annual Production (First 5 Years) | ~204,800 metric tonnes copper cathode |

| Target First Production | 2030 |

| Estimated Construction Start | 2027 |

| Initial Capital Requirement | ~US$4 billion |

The October 2025 feasibility study provides the project with an important commercial credibility marker. A completed feasibility study transforms a resource from a geological inventory into a bankable asset, enabling project finance debt syndication and formal valuation benchmarking — both of which are prerequisites for a project of this capital intensity.

Who Holds the Equity and Why It Matters

The current ownership structure of McEwen Copper, the entity that holds 100% of the Los Azules project, reflects a deliberate assembly of strategic partners rather than a purely financial shareholder base.

| Stakeholder | Ownership / Investment | Strategic Rationale |

|---|---|---|

| McEwen Copper (McEwen Mining subsidiary) | 100% project developer | Operator and primary developer |

| Rio Tinto (via Nuton LLC) | 17.2% stake; ~US$100M invested | Technology partner and potential capacity acquirer |

| Stellantis | 18.3% stake; ~US$275M invested | Raw material security for EV battery manufacturing |

Stellantis's position is particularly instructive for understanding the broader forces at play. The automaker's decision to invest approximately US$275 million for an 18.3% stake in a pre-production mining entity represents a direct upstream integration strategy — bypassing the spot market in favour of secured access to copper cathode at the source.

This is a pattern increasingly adopted by automotive original equipment manufacturers as EV production ramps, and it signals institutional-level conviction in both the project's viability and Argentina's investment environment. In addition, understanding sound copper investment strategies is becoming increasingly essential as these dynamics reshape the competitive landscape.

Rio Tinto's Nuton Technology: More Than a Financial Bet

How Leaching Technology Changes the Development Calculus

Nuton LLC is Rio Tinto's proprietary copper technology venture, and its involvement in Los Azules carries significance beyond the approximately US$100 million invested to date. Nuton is actively testing its leaching methodology directly on Los Azules ore samples, meaning the site functions simultaneously as a strategic investment target and a real-world validation environment for technology that could reshape Rio Tinto's approach to copper processing more broadly.

Heap-leach processing for copper — particularly for oxide ores and certain transitional sulphide zones — offers a fundamentally different capital and operational footprint compared to conventional concentrator-based processing:

- Traditional sulphide processing requires large, capital-intensive concentrators, ball mills, and flotation circuits, generating significant quantities of tailings requiring long-term management

- Heap-leach operations stack crushed ore on lined pads and apply a leach solution, recovering copper through solvent extraction and electrowinning (SX-EW) directly into cathode form

- This produces London Metal Exchange Grade A copper cathode without requiring smelting, which is a commercially distinct advantage given increasing smelter capacity constraints globally

- In high-altitude, water-constrained environments such as San Juan Province, the reduced water consumption profile of optimised heap-leach systems carries both operational and social licence advantages

The production of copper cathode directly from a leach circuit, rather than concentrate requiring further processing, is strategically significant in a market where smelter capacity has become a genuine bottleneck for copper producers. Cathode requires no further processing before use by copper fabricators.

Crucially, Nuton's technology appears to target a specific challenge within the heap-leach space: improving copper recovery rates from primary sulphide ores, which historically have responded poorly to conventional leaching. If the technology can demonstrate viable recovery economics on Los Azules sulphide material, it would represent a meaningful technical breakthrough with implications extending well beyond this single project. The future of copper mining may well hinge on precisely these kinds of processing innovations reaching commercial scale.

Why Rio Tinto Raises Stake in Los Azules: The Strategic Rationale

The Copper Pipeline Problem

Rio Tinto's position heading into the late 2020s reflects a tension common across the major mining sector: existing copper operations face grade decline and increasing operational complexity, while the pipeline of genuinely large replacement assets is extremely limited. The collapse of merger discussions with Glencore placed additional pressure on the company to pursue organic and near-organic copper growth through stake-building and project partnerships rather than corporate consolidation.

In this context, according to Reuters, McEwen Copper's managing director Michael Meding confirmed that Rio Tinto is actively pursuing copper volume through its development pipeline, and that discussions with Nuton regarding a deeper position in Los Azules have been productive. The framing is important: Meding characterised the conversation as one between parties with aligned strategic interests, where Nuton's leaching technology creates a natural commercial fit with the project's processing requirements.

Scenario Analysis: What a Larger Position Could Look Like

No formal announcement of a stake increase had been made as of May 2026, and Rio Tinto declined to comment publicly on the discussions. However, the range of plausible outcomes merits structured consideration:

| Scenario | Implications |

|---|---|

| Rio increases to 25–30% | Strengthens financing credibility; accelerates Nuton technology integration; minimal governance change |

| Rio acquires majority control | Los Azules effectively becomes a Rio Tinto-operated asset; McEwen Mining retains minority interest |

| Formalised joint venture structure | Shared development costs and co-governance; clearest pathway to construction capital deployment |

| Status quo maintained | Rio retains optionality while IPO proceeds in late 2026; stake decisions deferred to post-listing valuation |

Each scenario carries different implications for the project's US$4 billion capital raise. A larger Rio Tinto commitment would materially de-risk the financing process by introducing a globally recognised balance sheet as a co-guarantor, which typically improves the terms available for project finance debt.

The Financing Architecture: IPO, Debt, and Strategic Capital

Building a US$4 Billion Capital Stack

Funding a development-stage copper project requiring US$4 billion in initial capital demands a layered financing approach. McEwen Copper's planned initial public offering, targeting approximately US$300 million and anticipated toward the end of 2026, represents only a portion of the total requirement. The balance would typically be sourced from:

- Project finance debt, structured against the project's cash flow profile and underpinned by the feasibility study

- Strategic partner equity contributions, including any incremental investment from Rio Tinto or Stellantis

- Streaming or royalty agreements with specialist finance providers

- Potential convertible instruments or mezzanine financing during the construction period

The IPO serves a function beyond pure capital raising. By establishing a public market price for McEwen Copper as a standalone entity, the listing creates a transparent valuation reference point that informs any subsequent negotiations over Rio Tinto's stake size and pricing. This makes the IPO timing commercially significant for all existing shareholders and potential new investors simultaneously.

The after-tax NPV of US$2.9 billion at feasibility study base-case copper price assumptions provides the primary anchor for equity valuation, though investors should note that copper price sensitivity is a material variable. Project NPVs of this type are typically modelled across a range of long-term price scenarios, and a sustained copper price decline below US$3.50 per pound would compress the economic margin meaningfully. Understanding the key copper price growth drivers is, consequently, essential for any investor modelling these scenarios accurately.

Argentina's Investment Environment: Context Without Guarantee

A Changed But Not Risk-Free Jurisdiction

Argentina's mining investment landscape has undergone a visible shift, with the country attracting an estimated US$40 billion in copper-focused investment commitments as of 2026. Los Azules is positioned to become Argentina's first significant copper mine in over three decades, which adds both symbolic and practical significance to its development timeline.

Stellantis's willingness to commit US$275 million to an Argentine copper development project reflects institutional-level confidence in the country's ability to support large mining investments through the construction period. That said, investors with exposure to the project should maintain awareness of residual risk factors that have historically complicated Argentine resource development:

- Currency and monetary policy risk: Argentina's history of currency controls and rapid monetary policy shifts remains a structural consideration for projects with long capital deployment timelines

- Provincial royalty and taxation structures: San Juan Province has its own royalty framework, and the interplay between provincial and national fiscal terms requires careful modelling over a multi-decade mine life

- Policy continuity risk: Long-duration projects spanning presidential election cycles carry inherent political transition risk in jurisdictions with volatile policy histories

These factors do not negate the project's merits, but they appropriately belong in any risk-adjusted assessment of the development timeline and financing execution.

The next major ASX story will hit our subscribers first

How Los Azules Compares Within the Global Undeveloped Copper Landscape

Competitive Benchmarking

One of the more instructive ways to assess Los Azules is to position it against other major undeveloped copper projects competing for capital and strategic partners. For instance, the Reko Diq project in Pakistan, backed by Barrick Gold, represents a similarly large-scale development with its own distinct jurisdictional and processing challenges:

| Project | Location | Development Stage | Notable Strategic Partner |

|---|---|---|---|

| Los Azules | Argentina | Feasibility Complete | Rio Tinto (Nuton) / Stellantis |

| Reko Diq | Pakistan | Feasibility Stage | Barrick Gold |

| Josemaria | Argentina | Pre-Development | Lundin Mining |

| Resolution | Arizona, USA | Permitting Stage | Rio Tinto / BHP |

| Pebble | Alaska, USA | Permitting Blocked | Northern Dynasty |

Los Azules occupies a distinctive position in this landscape for a combination of reasons that individually might be replicated elsewhere, but which collectively are rare:

- A completed feasibility study providing commercial-grade cost and production estimates

- A high-quality strategic partner with proprietary processing technology already being tested on site

- An automotive OEM as a co-investor, providing both capital and an implicit offtake signal

- A resource scale placing it among the ten largest undeveloped copper deposits globally

- A target production profile delivering copper cathode directly, bypassing concentrate processing

The cathode distinction is worth emphasising. As global copper smelter capacity faces structural challenges, including refinery closures and tightening treatment charges, projects capable of producing LME-deliverable cathode directly from their processing circuit carry an inherent marketing advantage over concentrate producers.

Key Risks and Catalysts to Monitor

What Could Accelerate the Development Timeline

Several discrete events have the potential to meaningfully advance Los Azules's trajectory toward construction:

- Formal confirmation of Rio Tinto raises stake in Los Azules following completion of technical evaluation

- Execution and pricing of the McEwen Copper IPO in late 2026, establishing a public market reference valuation

- Commencement of project finance debt syndication with institutional lenders

- Positive results from Nuton's on-site leaching technology trials demonstrating viable recovery economics

Risk Factors That Require Ongoing Monitoring

- Copper price sensitivity: The US$2.9 billion after-tax NPV is anchored to base-case price assumptions; prolonged weakness in copper prices would erode project returns and potentially delay financing decisions

- Capital raise execution: Assembling US$4 billion in a single project financing round represents one of the more complex capital market exercises in the global mining sector, and execution risk is real

- Technology validation: Nuton's leaching technology, while scientifically credible, has not yet been validated at commercial scale on Los Azules ore; the technology trials currently underway are therefore a critical near-term data point

- Argentine political continuity: Despite the current pro-investment policy environment, long-duration infrastructure commitments carry transition risk across electoral cycles

This article is intended for informational purposes only and does not constitute financial advice. All forward-looking statements, projections, and financial estimates referenced are subject to material uncertainty. Readers should conduct independent due diligence and consult qualified financial advisers before making investment decisions. Copper price assumptions underlying project NPV figures are particularly sensitive to global economic conditions and supply-demand dynamics that can change materially over short periods.

Want To Know When The Next Major Copper Discovery Hits The ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and delivering actionable alerts before the broader market reacts. Explore historic discovery returns to understand what's at stake, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major find.