July 8, 2026

The Case Against Silver as a Monetary Metal: Why Industrial Fundamentals Should Drive Your Thesis

Most retail investors approach silver through one of two lenses: either as a poor man's gold, prized for its centuries-long monetary pedigree, or as a high-beta industrial commodity riding the green energy wave. Both framings contain partial truths, but neither captures the full picture with the analytical precision that serious investors need heading into 2026. The reality that silver is an industrial metal not a monetary metal is not merely academic. How you categorise silver determines which signals you pay attention to, which risks you price in, and ultimately whether your investment thesis is built on solid foundations or convenient narratives.

When big ASX news breaks, our subscribers know first

Silver's Demand Composition Has Fundamentally Changed

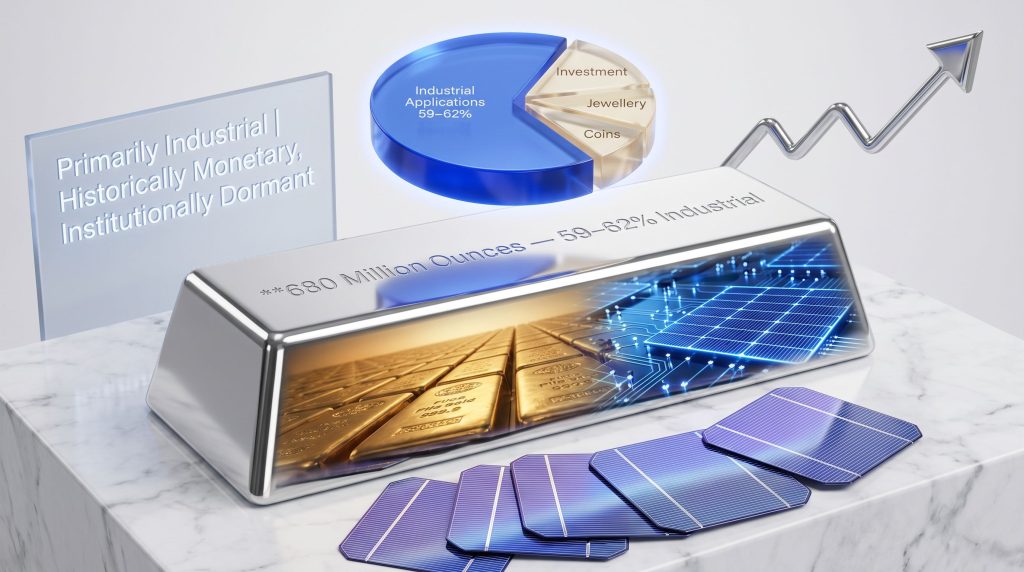

A decade ago, approximately half of global silver demand came from industrial applications. Today, that figure has shifted dramatically. Industrial applications consumed roughly 680 million ounces of silver in 2024, representing somewhere between 59% and 62% of total global silver demand. That structural transformation in demand composition is not a temporary cyclical quirk. It reflects deep, technology-driven changes in how silver is used and where it goes once it leaves the refinery.

The sectors pulling silver into irreversible industrial consumption are worth examining in detail:

- Solar photovoltaic manufacturing, which uses silver paste as a critical electrical contact material

- Semiconductor and electronics fabrication, exploiting silver's unmatched electrical and thermal conductivity

- Electric vehicle production and associated charging infrastructure

- Medical and antimicrobial applications, where silver's biocidal properties are increasingly valued

- Industrial brazing, soldering alloys, and chemical catalysis processes

The comparison between demand composition a decade ago versus today tells a revealing story:

| Demand Category | ~2014 Share | 2024 Share |

|---|---|---|

| Industrial Applications | ~48-50% | 59-62% |

| Investment and Coins | ~30-35% | ~28-32% |

| Jewellery and Silverware | ~18-20% | ~10-12% |

| Central Bank / Monetary Reserves | Negligible | Negligible |

Furthermore, one critical distinction separates silver from gold at a fundamental level: silver is consumed and destroyed in use. When silver paste is fired into a photovoltaic cell, that silver is gone from the investable supply permanently. Gold, by contrast, is almost entirely preserved, recycled, and restocked into global vaults. This difference in consumption behaviour has profound implications for how each metal's price actually forms. Silver's dual nature as both a precious and industrial material makes this distinction especially important for investors to grasp.

What History Actually Says About Silver's Monetary Role

Dismissing silver's monetary history entirely would be intellectually dishonest. Silver functioned as the primary global monetary standard for roughly five thousand years, from approximately 3000 BC through to the demonetisation wave of the 1870s. In terms of geographic breadth and duration, silver's monetary tenure was arguably more extensive than gold's.

The Nobel Prize-winning economist Milton Friedman made the counterintuitive claim that silver, not gold, was the dominant monetary metal throughout most of recorded history. This assertion challenges the modern tendency to treat gold as the singular benchmark of monetary metal status, and it deserves acknowledgment precisely because it is so frequently overlooked.

However, the critical question for 2026 investors is not what silver did in the 13th century. It is what silver does institutionally and structurally today. The demonetisation of silver during the 1870s was not a market-driven verdict on silver's intrinsic qualities. It was a political decision, shaped by the interests of creditor nations and the administrative convenience of a single gold standard.

That context matters because it means silver was removed from monetary frameworks by political fiat, not because markets organically rejected it. Even so, that demonetisation event was over 150 years ago. The institutional infrastructure that treated silver as money has been thoroughly dismantled.

Central Bank Behaviour Delivers the Institutional Verdict

The single clearest signal separating gold's ongoing monetary status from silver's comes from central bank reserve management behaviour. Central bank gold demand has been consistently strong for well over a decade, with no major central bank maintaining a strategic silver reserve of any significance.

This absence is not an oversight. It is a deliberate institutional verdict that silver does not function as a reserve monetary asset in the modern financial architecture.

When thinking about price formation, this distinction matters enormously. Gold's price is partially anchored by sovereign accumulation demand that is largely price-insensitive. Silver has no equivalent structural buyer at the institutional level. Its price is therefore far more exposed to cyclical swings in industrial demand, investor sentiment, and speculative positioning.

The gold-silver ratio analysis, which has historically ranged from around 15:1 during bimetallic standard periods to over 80:1 in modern markets, reflects this institutional divergence. When the ratio spikes, it is rarely because silver has become fundamentally cheaper in production terms. It is because gold's monetary premium expands during periods of financial stress in ways that silver's industrial demand profile cannot replicate symmetrically.

China's Solar Slowdown: The Most Underappreciated Bearish Signal for Silver

China has been the world's dominant installer of solar photovoltaic capacity, and silver paste is a non-negotiable input in conventional solar panel manufacturing. Chinese solar installation volumes therefore function as a direct leading indicator for industrial silver demand. What most Western investors do not yet appreciate is that China installed significantly less solar capacity in 2026 than it did in 2025.

This development has received minimal coverage in mainstream financial media, which has largely continued amplifying narratives about China's renewable energy ambitions. The gap between that narrative and the physical installation data creates a meaningful risk for silver investors anchored to a bullish solar demand thesis.

Several structural factors explain the installation contraction:

- Severe overcapacity in China's domestic solar panel manufacturing sector, suppressing project economics

- Grid absorption constraints caused by intermittent renewable penetration exceeding the system's dispatchable capacity

- Policy recalibration following years of aggressive subsidy-driven solar expansion

- The continued role of coal in China's baseload energy envelope, which reduces urgency for additional renewable capacity in the near term

A useful technical framework for understanding why renewable installation growth hits a ceiling involves the concept of grid dispatchability. China's coal plant strategy illustrates precisely this constraint, where coal continues to serve as backup for an intermittent renewable grid that cannot yet sustain itself independently. Once that ceiling is approached, grid stability deteriorates, and China is confronting exactly this constraint today.

| Scenario | Solar Installation Trajectory | Silver Demand Impact |

|---|---|---|

| China Solar Expansion Resumes | +15-20% year-on-year growth | Structurally bullish |

| Flat Installation Environment | 0-5% growth | Neutral to mildly bearish |

| Continued Installation Contraction | -10-15% year-on-year decline | Materially bearish |

Supply-Side Constraints: Why Silver Cannot Easily Self-Correct

Approximately 70% of global silver production is extracted as a byproduct of mining operations primarily targeting zinc, lead, copper, and gold. This structural reality means silver supply cannot respond to price signals the way primary commodities can. When silver prices rise, no miner can simply dial up a silver-dedicated operation. Silver output is largely tethered to decisions made about entirely different metals.

This supply inelasticity is frequently cited by silver bulls as a structural advantage. There is substance to that argument. The silver supply deficits that have persisted for six consecutive years draw down above-ground inventories over time, creating a structural tension that bulls point to as a long-term price catalyst.

However, above-ground silver inventories are substantial, and the rate at which deficits erode those stockpiles is a key variable that often goes unquantified in bullish narratives. The stock-to-flow ratio, popularised in monetary metal analysis, is frequently applied to silver. Because silver is consumed irreversibly in industrial applications at a rate that gold simply is not, the stock-to-flow framework borrowed from gold analysis does not translate cleanly.

The next major ASX story will hit our subscribers first

Placing Silver on the Commodity-to-Monetary Spectrum

Rather than forcing a binary answer to the industrial-versus-monetary question, it is more analytically useful to place silver on a spectrum. That spectrum runs from pure industrial commodities like copper on one end, through industrial precious metals like platinum and palladium, to monetary reserve assets like gold at the other extreme.

Platinum and palladium offer an instructive parallel. Both are precious metals with sophisticated industrial demand profiles, dominated by automotive catalytic converter chemistry. Neither is treated as a monetary asset by any institutional investor or central bank. Their price histories are driven almost entirely by automotive production cycles, emissions regulations, and substitution dynamics between the two metals.

Silver shares more structural characteristics with platinum and palladium than it does with gold. As one industry analysis on silver's dual role notes, while silver carries historical monetary associations, its price mechanics increasingly mirror those of industrial commodities rather than reserve assets.

| Attribute | Gold | Silver | Copper | Platinum |

|---|---|---|---|---|

| Primary Demand Driver | Monetary and Reserve | Industrial (59-62%) | Industrial (>90%) | Industrial and Auto |

| Central Bank Accumulation | Yes, significant | None | None | None |

| Consumed in Use | Minimal | Significant | Significant | Significant |

| Monetary History | Strong | Historically dominant | None | None |

| Price Sensitivity to Tech Cycles | Low | High | High | High |

| Inflation Hedge Reliability | High | Moderate | Low | Low |

The honest conclusion from this comparison is that silver sits materially closer to copper than to gold in its price formation mechanics, despite carrying what might be described as a residual monetary scent. That scent can generate investor sentiment-driven price spikes during periods of macro stress, but it cannot sustain a monetary premium the way gold's institutional accumulation demand does.

Building a Defensible Silver Investment Thesis

If the monetary narrative is structurally insufficient to anchor a silver thesis, what does a credible investment case actually look like? The foundation must be a rigorous, bottom-up supply-demand model built across multiple years, not a macro narrative about currency debasement or inflation hedging.

A disciplined approach involves the following steps:

- Quantify sector-specific demand growth across solar, EV production, electronics, and medical applications with realistic volume assumptions

- Stress-test Chinese solar installation volumes as the single largest swing variable in the industrial demand equation

- Model byproduct supply response linked to production cycles in zinc, lead, and copper mining

- Assess above-ground inventory drawdown rates and calculate how many years of consecutive deficit can be absorbed before physical scarcity emerges

- Apply a macro overlay covering currency dynamics, real interest rate environments, and risk-on/risk-off sentiment cycles

- Explicitly separate the monetary narrative premium from fundamental industrial pricing to identify where speculative positioning inflates spot prices beyond what supply-demand alone justifies

The case for buying silver because it will function as a monetary store of value equivalent to gold is a category error. No institutional framework supports that classification today. Buying silver because a multi-year supply-demand model demonstrates persistent deficits across growing industrial sectors is a legitimate, evidence-based investment decision.

The Dual-Nature Paradox and What It Means for Price Behaviour

Silver's hybrid character creates a unique and somewhat paradoxical asymmetric return profile. The industrial demand floor provides structural consumption that prevents the metal from behaving purely as a speculative monetary asset. Meanwhile, the residual monetary narrative can trigger sentiment-driven price spikes that temporarily push prices well above what industrial fundamentals alone would justify.

Understanding which force is dominant at any given moment is the actual analytical challenge. During periods of peak fear around currency debasement or systemic financial stress, silver tends to correlate with gold and attract speculative monetary positioning. During periods of macro stability, however, industrial demand dynamics and sector-specific variables, most notably Chinese solar installation volumes, reassert dominance over price formation.

Attributing a price spike driven by monetary narrative to validation of the bullish industrial thesis is a common and costly analytical error. The six-year consecutive demand deficit is a meaningful structural data point, but its implications for price depend heavily on inventory levels, the pace of industrial demand growth, and whether the solar installation contraction in China deepens or reverses.

Frequently Asked Questions: Silver as Industrial vs. Monetary Metal

Is silver still considered a monetary metal in 2026?

Silver retains a residual monetary narrative among retail investors and certain macro commentators, but institutionally it is not treated as a monetary asset. No central bank maintains strategic silver reserves, which is the clearest available signal of its functional classification in modern financial architecture.

Why don't central banks hold silver if it has such a strong monetary history?

The demonetisation of silver during the 1870s was a political rather than an economic decision, but its institutional consequences have proven durable. The modern reserve framework is built around gold, US Treasuries, and foreign currency assets. Silver has no mechanism for re-entry into that framework under current institutional arrangements.

How does solar panel demand affect the silver price?

Solar photovoltaic manufacturing is the single largest and fastest-growing industrial consumer of silver. Changes in global solar installation volumes, particularly in China, translate directly into demand fluctuations that can move the silver price materially.

What percentage of silver demand comes from industrial use?

As of 2024, industrial applications account for approximately 59% to 62% of total global silver demand, up from roughly 48% to 50% a decade earlier.

Is silver a better inflation hedge than gold?

Gold is a significantly more reliable inflation hedge because its price formation is anchored by sovereign accumulation demand and monetary reserve behaviour. Silver's inflation hedge properties are diluted by its sensitivity to industrial demand cycles and technology sector performance.

How does China's solar installation slowdown impact silver investors?

A sustained contraction in Chinese solar installations reduces one of the largest incremental demand drivers for silver. Investors who built bullish silver theses on the assumption of continued Chinese solar expansion need to reassess those models in light of the 2026 installation data.

What is the stock-to-flow ratio for silver and why does it matter?

The stock-to-flow ratio compares the total above-ground stockpile of a commodity to its annual production rate. For silver, this ratio is complicated by irreversible industrial consumption that continuously reduces effective above-ground stocks in ways that gold's recycling-dominant cycle does not.

Should I buy silver as a store of value or as an industrial commodity play?

The only intellectually honest answer is the latter. A credible silver thesis must be grounded in supply-demand fundamentals. Buying silver as a substitute for gold in a monetary hedge role misclassifies the asset and exposes investors to risks that a gold-based monetary thesis would not carry. Indeed, commentary from Jupiter Asset Management on silver's monetary role acknowledges this tension, noting that while silver carries monetary associations, its price behaviour is increasingly driven by industrial rather than reserve dynamics.

Key Takeaways: The Industrial vs. Monetary Verdict

| Dimension | Evidence Supporting Industrial Classification | Evidence Supporting Monetary Classification |

|---|---|---|

| Current Demand Share | 59-62% industrial consumption | ~38-41% investment and coins |

| Central Bank Behaviour | Zero sovereign accumulation | Historical reserve standard |

| Price Formation | Linked to solar, EV, electronics cycles | Correlates with gold during uncertainty |

| Supply Dynamics | Consumed irreversibly in manufacturing | Stored as monetary insurance |

| Institutional Classification | Treated as industrial input | Residual narrative premium only |

| Net Verdict | Primarily industrial | Historically monetary, institutionally dormant |

The weight of evidence confirms that silver is an industrial metal not a monetary metal in any functionally meaningful sense for 2026. Its historical monetary role is real and worth understanding, but it is not a sufficient basis for an investment thesis today. Investors who anchor their silver positioning to monetary narratives risk being blindsided by industrial demand shortfalls, particularly if China's solar installation contraction deepens or extends into 2027. A bottom-up supply-demand framework, stress-tested across realistic sector-by-sector demand scenarios, is the only rigorous foundation for a silver position in the current environment.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. All forecasts, projections, and analytical frameworks discussed involve inherent uncertainty. Readers should conduct their own independent research and consult qualified financial professionals before making any investment decisions. Past commodity price behaviour is not indicative of future results.

Want to Know When the Next Major ASX Mineral Discovery Hits the Market?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across silver, gold, copper, and more than 30 other commodities — translating complex data into clear, actionable investment insights for traders and long-term investors alike. Explore historic discoveries and their remarkable returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.