May 21, 2026

Why the Stagflation Playbook Matters More Than Ever for Precious Metals Investors

Monetary history has a habit of repeating itself in ways that most investors only recognise after the fact. The convergence of persistent price pressures, slowing economic output, and policy paralysis is not a new phenomenon, but it remains one of the most misunderstood macro environments for portfolio positioning. When inflation refuses to retreat and growth simultaneously stalls, the standard toolkit of central bank responses becomes nearly useless. Rate hikes deepen the economic wound; rate cuts pour fuel on the inflation fire. This is the stagflationary trap, and understanding it is foundational to evaluating why silver upside over gold in stagflation has become one of the more compelling structural arguments in commodity markets today.

When big ASX news breaks, our subscribers know first

The Mechanics of Stagflation and Why Conventional Assets Struggle

Stagflation occupies a uniquely destructive corner of the macroeconomic map. Unlike a standard recession, which tends to be deflationary and allows central banks room to stimulate, or a growth boom with rising inflation that can be cooled with rate increases, stagflation breaks both tools simultaneously.

The downstream effects on traditional asset classes are broadly negative:

- Equities face margin compression from rising input costs while revenue growth slows due to weakening consumer demand.

- Fixed income erodes in real terms as inflation outpaces coupon payments.

- Real estate becomes increasingly unaffordable as interest rates remain elevated and income growth stagnates.

- Commodities, particularly monetary metals, have historically served as one of the few reliable stores of value when financial assets are being structurally eroded.

The 1970s remain the definitive historical case study. During that decade, both gold and silver delivered extraordinary gains while equities and bonds lost significant real value over extended periods.

A critical, and often overlooked, distinction in inflation analysis is that consumer price increases are downstream consequences of monetary expansion, not the inflation itself. As economist Peter Schiff has consistently argued, inflation is fundamentally a monetary phenomenon driven by money supply growth. CPI and PPI readings are lagging indicators of that monetary reality, operating through what economists call long and variable lags.

This framework explains why inflation can persist and even accelerate even as short-term policy signals suggest containment, and why the structural bull case for precious metals cannot be quickly reversed by headline policy adjustments. For a deeper look at gold safe haven dynamics in this context, the interplay between monetary policy and hard assets becomes even clearer.

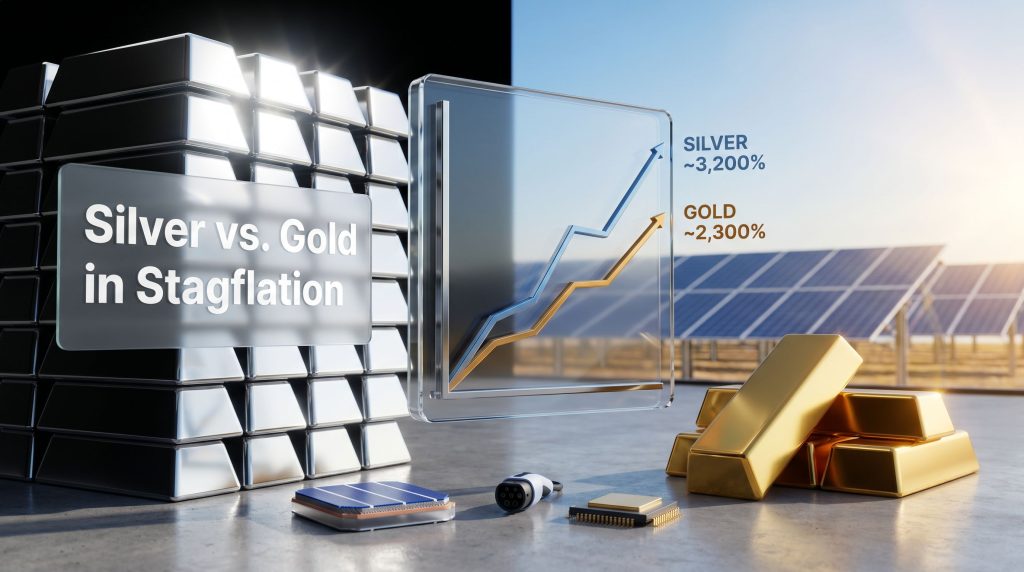

The 1970s Precedent: Benchmarking Silver Against Gold

Historical performance during the last major stagflationary cycle provides a useful, if imperfect, benchmark for the current environment.

| Metal | Price (Early 1970s) | Price (Peak ~1980) | Approximate Gain |

|---|---|---|---|

| Gold | ~$35/oz | ~$850/oz | ~2,300% |

| Silver | ~$1.50/oz | ~$49.45/oz | ~3,200% |

Silver's percentage gain exceeded gold's over this period, though it is essential to contextualise that performance accurately. The silver market in the late 1970s was significantly distorted by the Hunt Brothers' attempt to corner the market, creating a speculative spike that was not purely driven by macro fundamentals. The more instructive takeaway is the directional magnitude: in an environment where inflation dominated and real interest rates turned sharply negative, silver demonstrated greater upside torque relative to gold.

What drove silver's relative outperformance then, and what could drive it again now, comes down to its dual identity as both a monetary asset and an industrial input. During the 1970s, monetary demand was the primary driver. Today, a second structural demand layer — industrial consumption tied to electrification — adds an entirely new dimension that was absent in the previous cycle. Furthermore, according to Forbes and CME Group research, gold's stagflation performance alone underscores why adding silver's industrial kicker changes the return profile dramatically.

Silver's Structural Advantage: The Dual Demand Framework

Monetary Demand: The Inflation Hedge Foundation

Like gold, silver benefits from environments where real interest rates are negative or falling. When central banks expand money supply and inflation erodes the purchasing power of fiat currency, non-yielding hard assets become relatively more attractive. The opportunity cost of holding silver decreases as real rates decline, and demand from investors seeking protection from currency debasement tends to accelerate.

This monetary demand dynamic is well understood. Where silver diverges from gold — and where its potential upside advantage becomes clearest — is in its industrial demand profile. The broader precious metals outlook reinforces how these diverging demand drivers create meaningfully different return profiles across macro scenarios.

Industrial Demand: The Electrification Kicker

Silver possesses the highest electrical conductivity of any element, a physical property that makes it irreplaceable across a growing range of modern technologies. This is not a marginal demand story; it is a structurally expanding demand floor that gold simply does not share.

Key industrial demand drivers for silver include:

- Solar photovoltaic manufacturing: Silver paste is used in the production of photovoltaic cells, and solar deployment continues to accelerate globally across utility-scale and distributed generation installations.

- Electric vehicles: EV powertrains, charging infrastructure, and battery management systems all incorporate silver components.

- Data centre construction: The artificial intelligence infrastructure buildout requires enormous quantities of conductive metals, including silver, for bus bars, connections, and high-density electrical assemblies.

- Semiconductor and electronics manufacturing: Silver's conductivity properties make it a preferred material in advanced electronics production.

- Power transmission and grid infrastructure: Grid modernisation and expansion programmes across major economies create sustained industrial silver demand.

The scale of potential future demand is difficult to overstate. Jensen Huang of Nvidia has suggested that global energy infrastructure may need to scale by a factor of 1,000 times current capacity to meet the demands of fully integrated, always-on artificial intelligence systems. Even applying significant discounts to that projection, the transmission and connectivity infrastructure required to move that energy — much of which depends on copper and silver — represents a multi-decade demand story.

Think of silver as a high-volatility inflation hedge with an industrial kicker. Gold acts as the stabilising safe haven anchor. In a stagflationary environment where inflation is the dominant force, silver's dual demand profile has the structural potential to generate amplified upside relative to gold.

The Amplifier Effect: Why Silver Moves More Than Gold

Silver's market is substantially smaller than gold's in total value terms. This size differential means that equivalent capital flows into silver create proportionally larger price movements. When monetary demand and industrial demand align simultaneously, as they can in a stagflationary environment with active electrification investment, silver can experience compounding demand pressure from two directions at once.

The gold-silver ratio analysis is also worth examining closely here. This ratio currently sits at historically elevated levels, and periods of such elevation have historically preceded significant silver outperformance relative to gold as the ratio mean-reverts toward its long-run average. Consequently, this relative valuation signal adds a further layer to the structural silver upside over gold in stagflation argument.

Supply Constraints: Silver's Hidden Structural Tailwind

The Byproduct Problem

One of the most underappreciated aspects of the silver investment thesis is how its supply dynamics differ fundamentally from gold. The majority of silver produced globally is extracted as a byproduct of base metal mining, primarily copper, zinc, and lead operations. This means silver supply is largely determined by the economics of other metals rather than by silver's own price signal.

If base metal production slows due to economic weakness, energy cost pressures, or capital expenditure reductions at major mining operations, silver supply is constrained as a secondary consequence, even if silver prices are rising. This creates an asymmetry that is structurally favourable for prices: demand can accelerate while supply is simultaneously being held back by factors entirely outside the silver market. The ongoing silver supply deficits only deepen this structural imbalance.

Mining's Structural Moat

Mining, broadly, operates with one of the most durable competitive moats of any industry. The timeline from mineral discovery to production typically spans a decade or more, incorporating exploration, resource definition, environmental permitting, feasibility studies, financing, and construction phases. High prices do not cure supply shortages quickly in mining; the industry's structural lead times are simply too long.

This dynamic is particularly relevant in the copper-silver nexus. The copper supply crunch is widely regarded as a multi-decade structural story. Major new discoveries of the scale needed to meaningfully shift the supply picture are extraordinarily rare. One recently celebrated major discovery in South America had actually been held in a mining company's portfolio for approximately 30 years before reaching development stage, illustrating how even known deposits take decades to bring into production.

New copper production capacity needs to come online at a rate of several major mines per year simply to meet projected demand growth, and the pipeline of projects capable of delivering that supply simply does not exist at current development rates.

The Real Risks to the Silver Upside Thesis

Scenario Dependency: The Critical Conditional

The silver upside over gold in stagflation thesis is conditional, not unconditional, and understanding that conditionality is essential for sound risk management. The scenario matrix below illustrates how outcomes diverge depending on which macro force dominates.

| Scenario | Gold Outlook | Silver Outlook | Dominant Force |

|---|---|---|---|

| Stagflation (inflation dominant) | Strongly bullish | Very bullish, outperforms gold | Monetary + industrial demand |

| Mild stagflation, limited growth | Bullish | Bullish, tracks gold closely | Monetary demand leads |

| Deep recession (growth collapse) | Bullish safe haven | Underperforms gold | Industrial demand collapses |

| Deflationary crash | Mixed, volatile | Significant downside risk | Risk-off, industrial selloff |

The critical risk is straightforward: if economic contraction becomes the dominant macro force rather than inflation, silver's industrial demand component becomes a liability rather than an asset. Manufacturing slowdowns, reduced capital expenditure on electrification infrastructure, and collapsing industrial activity can overwhelm silver's monetary demand support. In deep recessions, gold's pure safe-haven status tends to make it the more resilient performer.

Market Mispricing: Risk and Opportunity in the Same Package

Markets frequently operate on flawed logic. A persistently incorrect mechanism that continues to influence price action is the assumption that inflation signals imply higher interest rates, which in turn implies selling pressure on gold and silver because they yield nothing. The experience of 2025 has demonstrated repeatedly that this framework is simply wrong, yet many algorithmic trading programmes continue to be built on it.

This mispricing creates dislocations between fundamental value and market price. Short-term price action in precious metals is frequently driven by algorithmic responses to headlines rather than by fundamental analysis. A notable example of this dynamic is how geopolitical events affecting oil supply can trigger selling in precious metals because markets conflate the oil shock inflation signal with the flawed higher rates narrative.

Sovereign and central bank selling adds another layer of complexity. Recent data has shown that between Turkey and Russia alone, central bank gold sales in a recent reporting period exceeded the combined purchases of all other buyers. Yet gold has demonstrated resilience at historically elevated price levels even in the face of this unusual selling pressure. If gold can hold strong absolute price levels against that magnitude of institutional selling, the underlying demand structure appears genuinely robust.

Being right about a fundamental thesis and actually making money from it are two entirely different outcomes. The gap between them is filled by timing, liquidity management, and the discipline to separate what should happen from what Mr. Market is doing right now.

Energy Costs and Mining Margin Risk

A frequently overlooked operational risk for both gold and silver miners is energy cost exposure. Many mining operations are located in remote areas where grid power is unavailable, requiring mines to operate on diesel generator sets. These systems consume substantial volumes of diesel fuel, and operating margins are directly exposed to diesel price volatility and supply availability.

Geopolitical disruptions affecting major oil-producing regions can translate into higher diesel costs and, in more severe scenarios, supply constraints for remote mining operations. Management teams rarely provide advance warning of deteriorating fuel cost conditions; investors typically learn about these impacts through quarterly reporting after the fact. The direction of margin change tends to matter more to investors than the absolute level of profitability.

Investor Psychology and Portfolio Positioning in Stagflation

The Emotional Investing Trap

Precious metals markets attract highly conviction-driven investors, which creates predictable and exploitable emotional patterns. When prices rise, momentum chasers pile in, often late. When prices correct from elevated levels, the same investors who were enthusiastically bullish interpret perfectly normal consolidation as a catastrophic failure of the investment thesis.

A useful framing: gold at $4,500 per ounce on the way up generates excitement and optimism. The same price on the way down, from a previous high of $5,600, generates fear and capitulation — even though the underlying business fundamentals of mining at $4,500 gold remain extraordinary by any historical measure. This asymmetry in investor psychology is not a bug in the market system; it is one of the most reliable sources of mispricing and, therefore, opportunity for disciplined investors.

The Case for Liquidity: Preparing for Asymmetric Opportunity

Maintaining elevated cash reserves in an elevated-risk environment is not a bearish call on precious metals. It is strategic preparation for the asymmetric buying opportunities that dislocations create. Historical precedent is instructive: investors who entered the 2008 financial crisis with significant liquid reserves were positioned to acquire assets at generational valuations that fully-invested peers could only watch from the sidelines.

The probability of a significant market reversal in the current environment — driven by any combination of geopolitical escalation, private credit stress, speculative asset bubble deflation, or macroeconomic deterioration — is meaningfully elevated above historical base rates. This does not mean a crash is the base case; it means the tail risk is sufficiently elevated that holding higher-than-usual cash reserves represents sound risk management rather than excessive caution.

Balancing Gold and Silver Exposure

For investors seeking precious metals exposure in a stagflationary environment, a framework that treats gold and silver as complementary rather than competing positions captures the full range of the opportunity. Furthermore, WisdomTree's analysis on stagflation highlights precisely how these two metals can diverge meaningfully in return profiles depending on which macro force dominates.

- Gold as portfolio anchor: Lower volatility, pure monetary demand driver, performs across a wider range of macro scenarios including deep recession.

- Silver as upside vehicle: Higher volatility, dual demand driver, greatest relative upside when inflation is the dominant macro force.

- Entry timing awareness: Silver's volatility means buying at momentum peaks carries meaningful short-term downside risk even when the long-term thesis is intact.

- Liquidity management: Maintaining cash reserves for potential dislocation events preserves optionality and the ability to deploy capital at compelling entry points.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Silver Upside Over Gold in Stagflation

Does silver always outperform gold during stagflation?

No. Silver's potential to outperform gold in stagflation is conditional on inflation remaining the dominant macro force. If economic contraction deepens into a full recession, silver's industrial demand component can drag performance significantly below gold's. The 1970s historical precedent shows greater percentage gains for silver, but with substantially higher volatility and important market-specific distortions.

What is the gold-to-silver ratio and why does it matter?

The gold-to-silver ratio measures how many ounces of silver are required to buy one ounce of gold. When this ratio is historically elevated, silver is considered undervalued relative to gold on a relative basis. Mean reversion toward historical averages implies silver has proportionally more upside potential from a relative value perspective, independent of the direction of gold prices.

How does the current macro environment align with stagflation conditions?

Both CPI and PCE measures carved out a bottom several months ago and have been trending upward consistently. PPI data has repeatedly beaten expectations, and producer-side cost pressures have not yet fully flowed through to consumer prices, suggesting a second inflation wave is a credible risk. Simultaneously, energy supply disruptions tied to geopolitical conflict are creating oil shock dynamics, while the Federal Reserve faces the classic stagflationary policy paralysis. These conditions collectively align with the macro setup historically most supportive for precious metals.

What are the biggest risks to the silver bull thesis?

Primary risks include: a deeper-than-expected economic recession that collapses industrial demand; short-term algorithmic selling triggered by incorrect inflation-rate interpretations; large-scale sovereign or institutional gold and silver selling temporarily suppressing prices; diesel fuel cost escalation compressing mining margins; and entry timing risk for investors purchasing at momentum peaks.

How does the copper thesis relate to silver's industrial demand story?

Copper and silver share significant industrial demand overlap, particularly in transmission, connectivity, and electrification applications. Copper's structural multi-decade supply deficit reinforces the broader thesis for conductive metals. When copper moves on industrial demand signals, silver frequently responds in kind, reflecting shared demand drivers across the electrification investment cycle. The copper supply pipeline, measured against projected demand from data infrastructure, grid expansion, and EV manufacturing, does not support supply sufficiency for decades to come.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial advice. Precious metals investments involve significant risk, including the potential for capital loss. Past performance during historical periods such as the 1970s is not indicative of future results. All forecasts, projections, and scenario analyses discussed are inherently speculative and subject to material uncertainty. Readers should conduct their own due diligence and consult a qualified financial adviser before making any investment decisions.

Want to Catch the Next Major Silver or Gold Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and their returns to understand the magnitude of what early positioning can achieve, then begin your 14-day free trial at Discovery Alert to gain a market-leading edge in precious and conductive metals.